How a Definitive Agreement Works

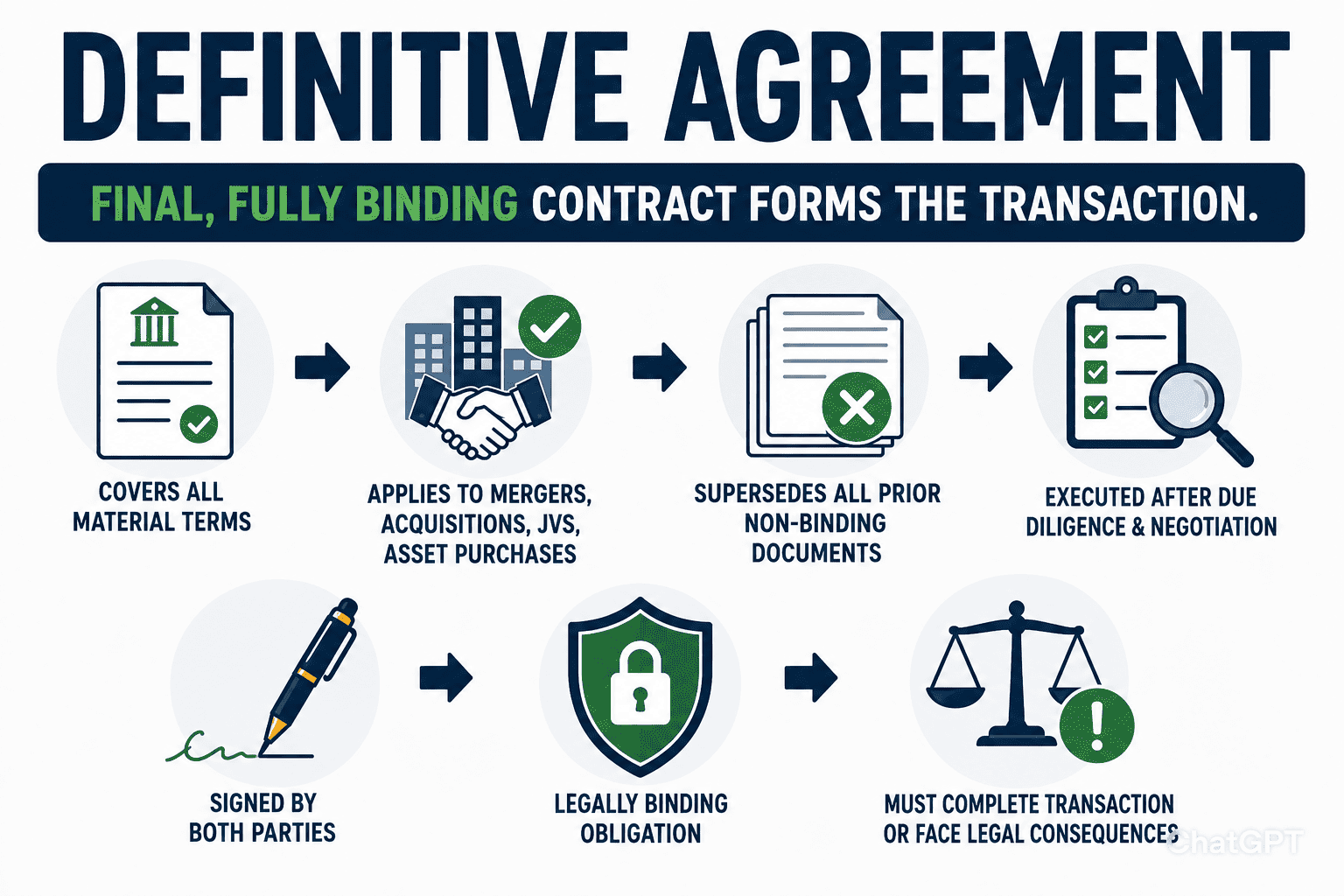

In any significant commercial transaction, whether a cross-border acquisition, a joint venture formation, or a major asset sale, the parties progress through a sequence of documents before they reach the point of irrevocable commitment. The Definitive Agreement is that final point. It is the document that makes the deal real.

Prior instruments in the transaction lifecycle, an Expression of Interest, a Memorandum of Understanding, a Letter of Intent, or a Heads of Agreement, typically record intent and establish a framework for negotiation. They are generally non-binding on the commercial substance of the deal, though they will contain binding provisions on confidentiality, exclusivity, and governing law. A Definitive Agreement is categorically different: it is fully binding in its entirety and commits both parties to perform.

In M&A practice, the Definitive Agreement is sometimes called a Definitive Purchase Agreement (DPA), a Share Purchase Agreement (SPA), an Asset Purchase Agreement (APA), or a Definitive Merger Agreement, the label varies by transaction type and jurisdiction, but the function is the same in each case. In joint venture structuring, the equivalent is the Joint Venture Agreement or Shareholders’ Agreement, which plays the same role of binding commitment once terms are agreed.

⚡ Critical Distinction

The Definitive Agreement supersedes all prior agreements and understandings between the parties, both oral and written. The commercial framework recorded in the LOI or Heads of Agreement is replaced in its entirety by the Definitive Agreement. Parties sometimes assume that terms agreed informally or recorded in an LOI carry over automatically; they do not. If a term is not in the Definitive Agreement, it is not agreed. Every material point must be drafted into the final document.

Types of Definitive Agreements

Types of Definitive Agreements in International Transactions

The two most common forms of Definitive Agreement in cross-border M&A and asset transactions are the Share Purchase Agreement and the Asset Purchase Agreement. Each allocates risk between buyer and seller in fundamentally different ways, and the choice of structure has significant tax, legal, and commercial implications.

🏢 Type 1

Share Purchase Agreement (SPA)

The seller transfers the shares of the target entity to the buyer. The buyer acquires the entire legal entity, including all its assets, liabilities, contracts, and obligations, whether disclosed or not. Also called a “Stock Purchase Agreement” in US practice.

- Buyer inherits all historical liabilities

- Contracts, licences, and permits transfer automatically

- Preferred by sellers for tax efficiency in many jurisdictions

- Requires comprehensive representations and warranties

- Common in M&A, private equity buy-outs, and cross-border acquisitions

📦 Type 2

Asset Purchase Agreement (APA)

The seller transfers individual assets to the buyer, equipment, inventory, intellectual property, customer contracts, rather than the entity itself. The seller retains ownership of the legal entity and its residual liabilities.

- Buyer can select which assets (and liabilities) to acquire

- Contracts and licences require individual novation or assignment

- Often preferred by buyers for liability isolation

- More complex to execute across multiple asset classes

- Common in distressed sales, carve-outs, and manufacturing deals

✨ Joint Venture & Other Structures

Beyond acquisition transactions, Definitive Agreements govern joint ventures (where the definitive document is the Joint Venture Agreement or Shareholders’ Agreement), long-term supply and distribution arrangements (where a Master Services Agreement fulfils the same function), and licensing transactions. In each case, the defining characteristic is the same: the agreement is fully binding, commercially comprehensive, and supersedes all prior discussions. GTsetu has observed Definitive Agreement executions across manufacturing, EV, and FMCG joint ventures, see the real-world examples below.

Key Clauses & Provisions

Key Clauses Every Definitive Agreement Must Address

A Definitive Agreement in a significant cross-border transaction is a comprehensive legal instrument, typically between 50 and 200 pages in major M&A deals, exclusive of schedules and disclosure documents. The following provisions are present in virtually every Definitive Agreement and represent the principal points of commercial negotiation between the parties.

CLAUSE 01

Definitions & Interpretation

Defines all key terms, including “Closing,” “Purchase Price,” “Material Adverse Effect,” “Business Day,” and “Affiliates”, with precision. Ambiguity in definitions drives litigation; this section anchors the entire agreement.

CLAUSE 02

Purchase Consideration & Price Adjustment

Sets out the total consideration the buyer will pay, the payment mechanics, the escrow or holdback structure, any earn-out provisions tied to post-closing performance, and the mechanism for working capital adjustments at closing.

CLAUSE 03

Representations & Warranties

Factual statements made by each party about the subject of the transaction, financial accuracy, regulatory compliance, intellectual property ownership, litigation exposure, material contracts, and employment. The most heavily negotiated section of any Definitive Agreement.

CLAUSE 04

Covenants

Obligations on both parties to take, or refrain from, specified actions between signing and closing. Typically includes obligations to operate the business in the ordinary course, restrictions on material changes, and cooperation in obtaining regulatory approvals.

CLAUSE 05

Closing Conditions

The prerequisites that must be satisfied before either party is obligated to complete the transaction, regulatory approvals, lender consents, third-party notices, and confirmation that representations remain accurate. This is where the Definitive Agreement connects to the structure of a Conditional Agreement.

CLAUSE 06

Solicitation, No-Shop & Go-Shop

A No-Shop clause prohibits the seller from soliciting or entertaining competing bids after signing. A Go-Shop allows the seller a limited window to seek better offers, used when the seller’s board needs to demonstrate it has maximised shareholder value.

CLAUSE 07

Termination Rights & Break-Up Fee

Specifies the circumstances under which either party may terminate the agreement, and what financial consequences follow. A break-up fee (payable by the seller if it accepts a superior proposal) and a reverse break-up fee (payable by the buyer if it fails to close for financing reasons) are standard in major transactions.

CLAUSE 08

Indemnification

Allocates post-closing liability between buyer and seller for breaches of representations and warranties, fraud, and specific identified risks. Typically subject to caps (maximum exposure), baskets (minimum claim thresholds), and survival periods (time limits on claims).

CLAUSE 09

Material Adverse Change (MAC/MAE)

Defines what constitutes a Material Adverse Change or Material Adverse Effect, a deterioration in the target’s business serious enough to entitle the buyer to refuse to close. MAC clauses are intensely negotiated; the COVID-19 period generated landmark litigation on their interpretation.

CLAUSE 10

Non-Compete & Non-Solicitation

Post-closing restrictions preventing the seller (and often its principals) from competing with the acquired business or soliciting its employees or customers for a defined period. See also GTsetu’s guide to non-compete clauses in international transactions.

CLAUSE 11

Confidentiality

Obligations on both parties, which survive termination, to maintain the confidentiality of information shared during the transaction process. Often supplemented by, or cross-referenced to, a standalone Non-Disclosure Agreement executed at the outset of the process.

CLAUSE 12

Governing Law & Dispute Resolution

The law governing the agreement and the mechanism for resolving disputes, litigation in a specified jurisdiction, or commercial arbitration under ICC, LCIA, SIAC, or UNCITRAL rules. A binding clause specifying seat and governing law is essential in every cross-border Definitive Agreement.

⚡ Representations & Warranties, The Heart of the Negotiation

In any Definitive Agreement, the representations and warranties section is the most commercially significant and the most intensely negotiated. The buyer seeks broad, comprehensive warranties to maximise its ability to claim post-closing if the business is not as represented. The seller seeks to narrow warranties with qualifications of materiality, knowledge, and scope, and to limit liability through caps, baskets, and survival periods. The balance struck in this section determines the economic risk allocation of the entire transaction. Sellers in well-advised cross-border deals routinely negotiate disclosure schedules and data room limitations that significantly reduce their exposure.

The Transaction Lifecycle

Where the Definitive Agreement Sits in the Deal Lifecycle

The Definitive Agreement is the culmination of a structured transaction process. Understanding its position in the deal lifecycle helps parties, and their advisers, to understand what must be resolved before the Definitive Agreement can be executed, and what happens after it is signed.

01

Expression of Interest / Initial Approach

The buyer signals commercial interest, through an Expression of Interest or informal approach. No binding commitment is made. Confidentiality arrangements are put in place, either through a standalone NDA or mutual confidentiality undertaking, to enable sharing of preliminary information.

02

Letter of Intent / Heads of Agreement

The parties execute a Letter of Intent or Heads of Agreement, recording the principal commercial terms (price, structure, key conditions) and granting the buyer a period of exclusivity to complete due diligence. The commercial terms at this stage are typically non-binding; confidentiality and exclusivity are binding.

03

Due Diligence

The buyer (and often its lenders) conducts comprehensive financial, legal, commercial, technical, and regulatory due diligence. This process, supported by a virtual data room, validates the representations the seller will be asked to make in the Definitive Agreement and identifies issues that require indemnification or price adjustment. Good faith negotiation is essential throughout this phase.

04

Negotiation & Drafting of the Definitive Agreement

Lawyers for both parties draft and negotiate the full Definitive Agreement, including the disclosure schedules through which the seller qualifies its warranties. This phase is often the longest and most resource-intensive, involving multiple rounds of mark-ups on representations, indemnification caps, closing conditions, and covenants.

05

Signing (“Exchange”)

The parties execute the Definitive Agreement. Both parties are now legally bound. In many transactions, particularly those requiring regulatory approval, there is a gap between signing and closing. The agreement will set out what must happen in this period, including any conditions precedent that must be satisfied before closing can occur. This is where the Definitive Agreement operates as a Conditional Agreement pending regulatory and other approvals.

06

Closing (“Completion”)

All closing conditions are satisfied or waived, and the transaction completes, shares or assets transfer, purchase price is paid, and ancillary documents (board resolutions, regulatory filings, transfer instruments) are executed. Post-closing obligations, earn-out calculations, transition services, integration covenants, continue to bind the parties under the Definitive Agreement.

Where Definitive Agreements Are Used

Where Definitive Agreements Are Used in Cross-Border Business

Definitive Agreements are the foundational legal instrument in every category of significant cross-border commercial transaction. The following are the principal use cases GTsetu has observed in international trade and partnership facilitation.

🤝

Mergers & Acquisitions

The Share Purchase Agreement or Asset Purchase Agreement is the definitive instrument in every M&A transaction, from small cross-border bolt-on acquisitions to multi-billion-dollar strategic mergers requiring competition authority clearance.

🏭

Joint Ventures & Manufacturing Partnerships

The Joint Venture Agreement or Shareholders’ Agreement is the Definitive Agreement in any JV, binding both parties to equity contributions, governance arrangements, profit distribution, and exit mechanics. No JV should operate without one.

🌍

Cross-Border Distribution & Supply

Long-term exclusive distribution or supply agreements, particularly those involving significant upfront investment by either party, require a Definitive Agreement that commits both parties to the commercial framework and allocates risk comprehensively.

💡

Technology Licensing & IP Transfers

The definitive licence agreement or IP assignment agreement formalises the terms on which proprietary technology, patents, know-how, software, manufacturing processes, is licensed or transferred across borders.

⚡

Project Finance & Infrastructure

Energy, infrastructure, and capital project transactions are documented through a suite of Definitive Agreements, including offtake agreements, EPC contracts, and concession agreements, that collectively constitute the contractual framework for the project.

🏗️

Real Estate & Development Transactions

The purchase and sale agreement for commercial real estate, including conditional agreements subject to planning and financing, is the Definitive Agreement in property transactions. It records every term of the transfer and survives completion through post-closing obligations.

🌐 GTsetu Global Trade & Partnership

Structuring a Cross-Border Deal? GTsetu Helps You Connect with Verified Partners.

GTsetu connects manufacturers and distributors across 100+ countries through 6-point government tie‑up verification (legal name, registered address, registration number, company status, company type, date of certificate of incorporation), built-in NDA workflows, and zero broker commissions. Once you’ve found a verified partner, GTsetu’s platform enables secure document sharing and collaboration to help you move from first contact toward a Definitive Agreement. GTsetu does not provide legal advice, facilitate negotiations, or structure transactions; that is the role of qualified legal counsel in your jurisdiction.

Explore GTsetu →

Risks & Drafting Pitfalls

Common Risks and Drafting Pitfalls in Definitive Agreements

🚩

Over-Reliance on the LOI as a Proxy for the Definitive Agreement

Parties, particularly those new to cross-border transactions, sometimes treat the Letter of Intent as commercially sufficient and allow the Definitive Agreement to become a formality. This is a serious error. The Definitive Agreement supersedes the LOI in its entirety. Terms that were agreed informally but not captured in the Definitive Agreement are not binding. Every material commercial point must be negotiated into the final document.

🚩

Insufficiently Qualified Representations and Warranties

Sellers who agree to broad, unqualified representations and warranties without adequate disclosure schedules, materiality qualifiers, or knowledge limitations create significant post-closing exposure. A warranty that is accurate at signing may be breached if circumstances change between signing and closing, representations must be carefully drafted to cover both moments, with appropriate bring-down conditions.

🚩

MAC/MAE Clauses That Are Too Broad or Too Narrow

A Material Adverse Change clause that is drafted too broadly may allow buyers to exit transactions opportunistically during market downturns. One that is too narrow may leave buyers trapped in transactions where the target’s business has fundamentally deteriorated. The scope of MAC carve-outs, for general economic conditions, industry-wide events, or pandemic-level disruption, requires careful bespoke negotiation for every transaction.

🚩

Vague or Unmeasurable Earn-Out Provisions

Earn-out arrangements, where part of the purchase price is contingent on post-closing performance, are among the most litigated provisions in Definitive Agreements. The performance metric must be defined with precision: what accounting standard applies, who controls the business during the earn-out period, and what actions by the buyer might interfere with performance must all be addressed in the drafting.

🚩

Inadequate Closing Conditions and Failure to Align With Regulatory Timelines

In cross-border transactions requiring competition authority or sector-specific regulatory approval, the closing conditions and long-stop date must be calibrated to realistic timelines for each jurisdiction. Overly optimistic long-stop dates create pressure on both parties and may force premature decisions about whether to extend, waive, or terminate. The connection between the closing conditions of a Definitive Agreement and the structure of a Conditional Agreement must be explicitly and carefully drafted.

🚩

Ambiguous Governing Law in Multi-Jurisdictional Transactions

In a cross-border Definitive Agreement, the governing law clause determines which jurisdiction’s courts will interpret the agreement and what remedies are available on breach. Parties sometimes select a governing law without considering whether local mandatory rules override it, whether local courts will recognise and enforce a foreign arbitral award, or whether the chosen dispute resolution mechanism is practical given where the parties’ assets are located. A standalone binding clause specifying governing law and dispute resolution must be drafted with full awareness of cross-border enforcement realities.

Definitive Agreement vs Pre-Contractual Documents

How a Definitive Agreement Compares to Other Transaction Documents

The Definitive Agreement sits at the apex of the transaction document hierarchy. Every prior document, the Expression of Interest, the MoU, the LOI, the Heads of Agreement, leads to it. Understanding the structural and legal differences between each document type is essential for any party entering a significant cross-border transaction.

| Dimension |

Definitive Agreement |

LOI |

MoU |

Heads of Agreement |

| Binding Nature |

Fully and unconditionally binding in its entirety

| Commercially non-binding; confidentiality & exclusivity binding

| Generally non-binding on commercial terms; selected clauses binding

| Variable; may be binding or non-binding depending on drafting

|

| Stage in Transaction

| Post-due diligence; commitment to complete the deal

| Pre-due diligence; signals intent and grants exclusivity

| Early stage; records framework and shared understanding

| Post-negotiation of principal terms; pre-formal drafting

|

| Commercial Detail

| Comprehensive, every material term, clause, and schedule

| Summary, principal commercial terms only

| Framework, objectives and cooperation structure

| Detailed summary, agreed principal terms before formal draft

|

| Due Diligence

| Completed before execution; findings reflected in schedules

| Triggers (and precedes) due diligence process

| May precede or run alongside initial discussions

| May follow initial due diligence; precedes Definitive Agreement

|

| Consequence of Withdrawal

| Breach of contract; damages, specific performance, break-up fee

| Generally no liability unless exclusivity/break-fee breached

| Generally no commercial liability

| Depends on whether characterised as binding; may attract liability

|

| Supersedes Prior Documents

| Yes, supersedes all prior agreements and understandings

| No, sits alongside earlier documents

| No, may be supplemented by later documents

| Partially, may supersede LOI on commercial terms

|

| Typical Length

| 50–200+ pages (excl. schedules and disclosure documents)

| 2–10 pages

| 3–15 pages

| 5–20 pages

|

| Role of Legal Counsel

| Essential, specialist M&A or transaction lawyers required

| Advisable, to protect binding provisions

| Advisable, to ensure truly non-binding on commercial terms

| Essential, to assess binding nature and protect key positions

|

✨ The Standard Transaction Sequence

In most complex cross-border transactions, the document sequence runs: Expression of Interest → NDA → LOI or Heads of Agreement → Due Diligence → Definitive Agreement (conditional) → Regulatory Approvals → Closing (unconditional). The Definitive Agreement, once executed, is the only document that matters legally. Everything before it is preparatory. GTsetu supports parties throughout this sequence, from initial partnership identification through to deal closing, with 6-point government tie‑up verification and secure collaboration tools.

FAQ

Frequently Asked Questions

Q

What is the difference between a Definitive Agreement and a Letter of Intent?

A

Letter of Intent is a preliminary, typically non-binding document that records the commercial framework of a proposed transaction, price, structure, key conditions, and the basis for negotiation, and grants the buyer a period of exclusivity to conduct due diligence. A Definitive Agreement is the final, fully binding contract executed once due diligence is complete and all terms are agreed. The LOI is the stepping stone to the Definitive Agreement; the Definitive Agreement is the destination. The LOI commits parties to negotiate in good faith; the Definitive Agreement commits them to complete the transaction. In most jurisdictions, only the specific protective provisions of an LOI, confidentiality, exclusivity, governing law, break-fee, are enforceable. Everything else is replaced in its entirety by the Definitive Agreement.

Q

When is a Definitive Agreement signed in a merger or acquisition?

A Definitive Agreement is signed, a moment known as “exchange” or “signing”, after the buyer has completed due diligence and the parties have fully negotiated every material term of the transaction. In many transactions, particularly those requiring regulatory approval or financing confirmation, there is a gap between signing and closing. During this period, the Definitive Agreement functions as a

Conditional Agreement: both parties are fully bound, but the obligation to complete the principal transaction (the transfer of shares or assets) is deferred until all closing conditions are satisfied. The distinction between signing and closing is fundamental in cross-border M&A practice.

Q

What happens if a party breaches a Definitive Agreement?

A breach of a Definitive Agreement, including a refusal to close, a failure to satisfy a condition within the agreed period, or a material misrepresentation in the representations and warranties, gives the non-breaching party access to legal remedies. These include damages (compensation for loss caused by the breach), specific performance (a court order compelling the breaching party to complete the transaction), and, where provided for in the agreement, a break-up fee or reverse break-up fee. Indemnification provisions address post-closing breaches of warranties. The exact remedies available depend on the governing law, the specific provisions of the agreement, and, in cross-border transactions, whether any mandatory local law rules restrict the parties’ chosen remedy regime.

Q

Is a Definitive Agreement the same as a Share Purchase Agreement?

A Share Purchase Agreement (SPA) is one of the principal forms that a Definitive Agreement takes in M&A transactions, specifically where the buyer is acquiring the equity of a target entity rather than its individual assets. The term “Definitive Agreement” is the broader category; the SPA is a specific type within that category. In an asset transaction, the Definitive Agreement takes the form of an Asset Purchase Agreement (APA). In a merger, it is a Merger Agreement or Scheme of Arrangement. In a joint venture, it is a Shareholders’ Agreement or Joint Venture Agreement. All of these documents share the defining characteristic of a Definitive Agreement: they are fully binding, commercially comprehensive, and supersede all prior instruments.

Q

What is a No-Shop clause and why does it matter?

A No-Shop clause, included in the solicitation provisions of a Definitive Agreement, prohibits the seller from soliciting, encouraging, or entering into discussions with competing bidders after the Definitive Agreement is signed. It protects the buyer’s investment in due diligence and negotiation by preventing the seller from using the signed agreement as leverage to attract a higher bid. The alternative, a Go-Shop clause, allows the seller a defined window (typically 30–60 days) to actively solicit superior proposals after signing. Go-Shop clauses are more commonly used in private equity transactions where the seller’s board needs to demonstrate it has fulfilled its fiduciary duty to maximise shareholder value. Both structures must be carefully drafted to define what conduct is permitted, what constitutes a “superior proposal,” and what break-up fee applies if the seller accepts a competing bid.