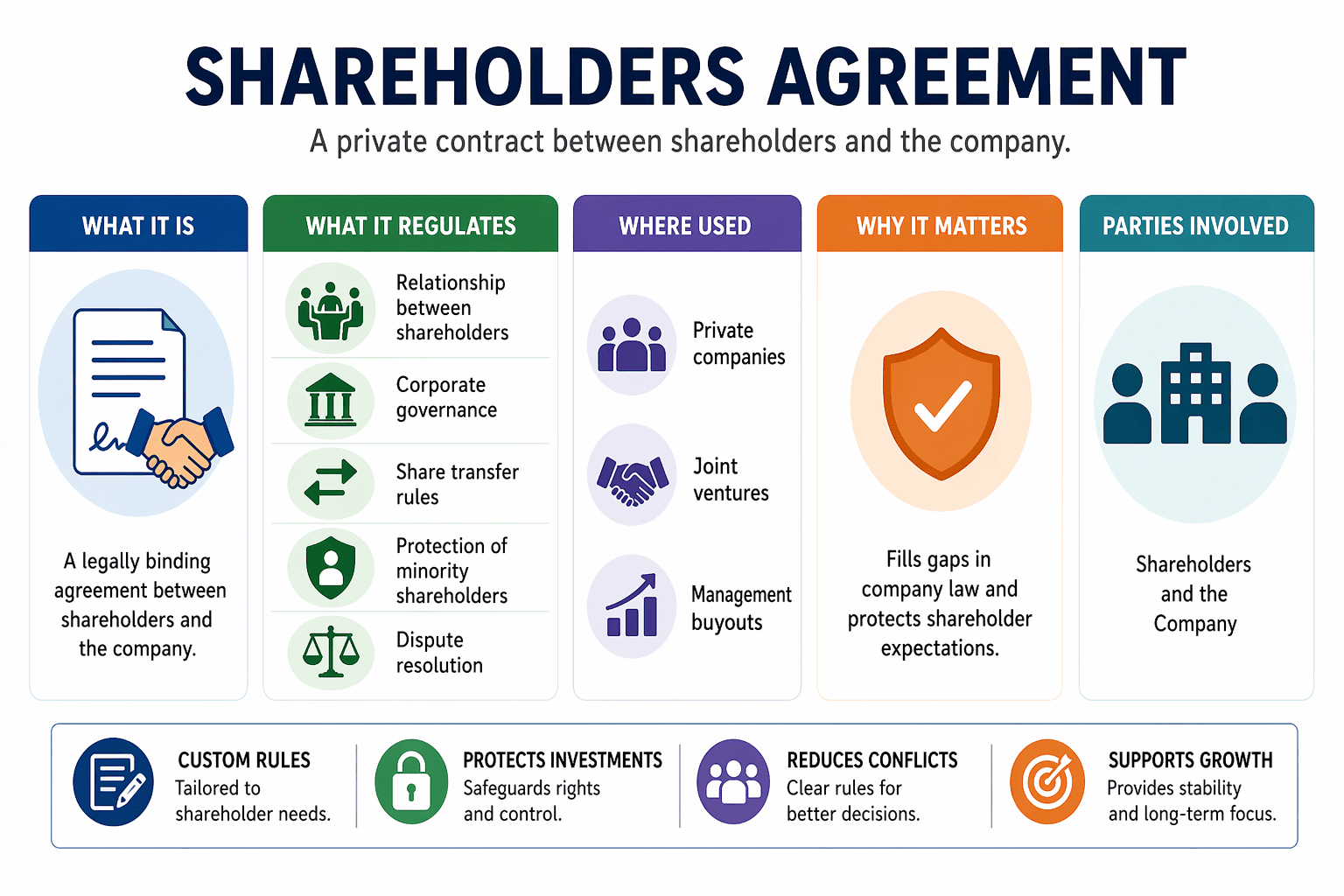

Why a Shareholders Agreement Matters

In any private company, particularly joint ventures, cross-border manufacturing partnerships, and investor-backed ventures, the default provisions of corporate law may not reflect the commercial bargain struck between shareholders. A Shareholders Agreement fills this gap, providing contractual protections that override or supplement the articles of incorporation. It governs how the company is run, how shares can be transferred, how deadlock is resolved, and what happens when a shareholder wants to exit. Without one, majority shareholders may act unilaterally, minority shareholders lack meaningful protection, and disputes escalate to costly litigation.

⚡ Critical Distinction

A Shareholders Agreement is distinct from the company’s Articles of Incorporation or Bylaws. The articles are public documents filed with the corporate registry; the Shareholders Agreement is a private contract. In most jurisdictions, the agreement can validly address matters not covered in the articles, and as between the signing shareholders, it governs. However, mandatory provisions of law cannot be overridden. For cross-border joint ventures, a well-drafted Shareholders Agreement is the single most important legal document protecting the partnership.

Key Clauses & Provisions

Essential Provisions of a Shareholders Agreement

Based on standard practice in international joint ventures and private company governance, a comprehensive Shareholders Agreement addresses the following core areas. Each provision allocates risk and defines rights between shareholders.

✓

Governance & Board Composition

Size, composition, election, and removal of directors. Rights of specific shareholders to designate board members. Formation of committees (audit, remuneration).

✓

Share Transfer Restrictions

Right of first refusal (ROFR), right of first offer (ROFO). Ensures existing shareholders control who may become a shareholder.

✓

Tag-Along Rights

Protects minority shareholders: if a majority shareholder sells to a third party, minorities can join the sale on the same terms.

✓

Drag-Along Rights

Enables majority shareholders to compel minority shareholders to sell their shares to a third party acquiring the whole company.

✓

Pre-emptive Rights

Existing shareholders have the right to subscribe to new share issuances proportionally, preventing dilution of ownership.

✓

Deadlock Resolution

Mechanisms for resolving board or shareholder deadlock, buy-sell provisions, mediation, or forced sale of shares.

✓

Information Rights

Shareholder access to financial statements, books, records, and inspection rights beyond statutory minimums.

✓

Dividend Policy

Rules governing declaration and distribution of dividends, fixed formula, board discretion, or mandatory distribution thresholds.

✓

Non-Compete & Confidentiality

Restrictions on shareholders competing with the company or using confidential information outside the venture. See also non-compete clause and NDA.

✓

Joinder & Assignment

Provisions binding new shareholders to the agreement upon transfer or issuance of shares.

✓

Termination Events

IPO, liquidation, sale of the company, or mutual agreement as triggers for termination of the agreement.

✓

Governing Law & Dispute Resolution

Choice of law and arbitration or court jurisdiction, essential in cross-border shareholder arrangements.

Minority vs Majority Protections

How a Shareholders Agreement Protects Shareholders

Default corporate law typically gives majority shareholders significant control through voting power. A Shareholders Agreement rebalances this dynamic contractually.

| Shareholder Type | Protections Under Shareholders Agreement | Risk Without Agreement |

|---|

| Majority Shareholders | Drag-along rights to force exit; pre-emptive rights against dilution; board representation proportional to stake; ROFR/ROFO to control new entrants. | Unable to force minority to sell in a full exit; dilution risk; no control over who buys minority shares. |

| Minority Shareholders | Tag-along rights; information access; higher quorum for major decisions; veto rights over critical matters (amending articles, selling assets, raising debt). | No ability to sell on same terms as majority; no access to books; outvoted on all matters; no exit mechanism. |

✨ GTsetu Guidance on Joint Venture Agreements

In cross-border manufacturing joint ventures, such as those tracked by GTsetu in the EV and automotive sectors, the Shareholders Agreement is the definitive legal framework. It governs everything from technology licensing to supply obligations between the JV and its parents. GTsetu’s verified partner network helps companies identify compatible JV partners before entering the complex negotiation of a Shareholders Agreement. GTsetu verifies companies on 6 government-sourced points (Name, Address, Registration Number, Company Status, Company Type, Date of Incorporation).

Shareholders Agreement vs Articles of Incorporation

Shareholders Agreement vs Articles of Incorporation

Understanding the relationship between these two documents is essential for any shareholder or JV participant. They serve different purposes, have different legal status, and interact in specific ways.

DimensionShareholders AgreementArticles of Incorporation / Bylaws

Legal NaturePrivate contract among shareholders (and the company)Public constitutional document filed with corporate registry

ConfidentialityPrivate, not publicly accessiblePublic, available to anyone

FlexibilityHigh, can address matters not in articles, including exit mechanics, tag-along, drag-alongLower, subject to mandatory corporate law requirements

EnforcementContractual remedies (damages, specific performance)Statutory remedies; corporate law procedures

Binding on new shareholdersOnly if they sign a joinder agreement or the agreement explicitly binds transfereesAutomatically binding on all shareholders by operation of law

Conflict resolutionTypically governs between signing shareholders; articles govern for third parties and mandatory provisionsPrevails over agreement where mandatory law applies

Shareholders Agreement in Transaction Lifecycle

Where the Shareholders Agreement Fits in the Deal Lifecycle

A Shareholders Agreement is not a preliminary document, it is the definitive binding contract that governs the entire relationship. It typically follows a sequence of pre-contractual documents that build toward final execution.

| Document | Binding Nature | Role re Shareholders Agreement | Typical Stage |

|---|

| Expression of Interest (EoI) | Non-binding commercially | Preliminary interest in forming a JV or equity partnership | Earliest stage |

| Memorandum of Understanding (MoU) | Generally non-binding | Records intent to form JV; outlines equity split, governance principles | Early-to-mid |

| Letter of Intent (LOI) | Non-binding commercially; binding exclusivity/confidentiality | Sets out commercial terms of proposed JV or investment | Mid |

| Term Sheet | Generally non-binding | Detailed economic and governance terms for the Shareholders Agreement | Mid |

| Heads of Agreement (HoA) | Often non-binding | Finalised principal terms before drafting Shareholders Agreement | Late pre-drafting |

| Shareholders Agreement | Fully binding | Definitive contract governing shareholder relationship | Post-negotiation; execution |

| Definitive Agreement (in JV context) | | The Shareholders Agreement is the Definitive Agreement for the joint venture |

For the distinction between binding and non-binding documents at each stage, see GTsetu’s guides on Non-Binding Agreement and Binding Clause. For the overarching master agreement structure, refer to Commercial Framework Agreement and Master Services Agreement (MSA).

Drafting & Enforceability

Drafting Considerations & Enforceability Across Jurisdictions

A Shareholders Agreement must be tailored to the governing law of the company’s jurisdiction. While generally enforceable as a contract, certain provisions may be subject to local mandatory corporate law. The principle of good faith negotiation is particularly relevant during the drafting phase, as many disputes arise from incomplete or ambiguous provisions.

✨ GTsetu Drafting Note

In cross-border joint ventures, the Shareholders Agreement often operates as a Conditional Agreement, its effectiveness may be conditional on regulatory approvals (competition authority, foreign investment clearance) or third-party consents. The Condition Precedent schedule should be integrated into the Shareholders Agreement to ensure that the joint venture is not formed until all prerequisites are satisfied. GTsetu’s deal tracking shows that failure to align CP timelines with regulatory calendars is a leading cause of JV termination before formation.

FAQ

Frequently Asked Questions

QWhat is the difference between a Shareholders Agreement and a Joint Venture Agreement?

In many contexts, the terms overlap. A Joint Venture Agreement is a broader term that may include the entire commercial arrangement between parties, including supply, technology licensing, and profit sharing. A Shareholders Agreement specifically governs the shareholder relationship within a corporate JV vehicle. In practice, for incorporated joint ventures, the Shareholders Agreement is the definitive contract, often supplemented by ancillary agreements (supply, licence, services). For unincorporated JVs, a standalone Joint Venture Agreement performs the same function without a shareholding structure.

QCan a Shareholders Agreement override the Articles of Incorporation?

As between the shareholders who sign the agreement, the Shareholders Agreement typically governs where there is a conflict, provided the agreement does not violate mandatory provisions of corporate law. However, third parties (creditors, regulators, new shareholders who have not signed a joinder) are not bound by the private agreement. Best practice is to align the articles with the Shareholders Agreement where possible, and to use joinder provisions to bind all current and future shareholders to the agreement.

QWhat happens if a Shareholders Agreement is not in place?

Without a Shareholders Agreement, the relationship between shareholders is governed solely by the default provisions of corporate law and the articles of incorporation. Majority shareholders generally control all decisions; minority shareholders have no tag-along rights, no pre-emptive rights, and limited ability to exit. Disputes are resolved through statutory oppression remedies or derivative actions, which are slow, expensive, and unpredictable. In cross-border joint ventures, the absence of a Shareholders Agreement is a major red flag for investors and lenders.

QIs a Shareholders Agreement legally binding?

Yes. A properly executed Shareholders Agreement is a fully binding contract under the governing law chosen by the parties. Breach of its terms gives rise to contractual remedies, damages, specific performance, injunctions. The key enforceability requirements are the same as for any commercial contract: consideration, capacity, lawful purpose, and certainty of terms. Provisions that violate mandatory corporate law (e.g., attempting to eliminate statutory inspection rights entirely) may be unenforceable, but the remainder of the agreement remains in effect.

QWhen should a Shareholders Agreement be drafted?

At the time the company is formed or when a new shareholder (investor, JV partner) joins. In JV contexts, the Shareholders Agreement is negotiated concurrently with the term sheet and finalised before the JV entity is incorporated. Waiting until after incorporation creates misalignment: the default articles may contain provisions that contradict the commercial bargain. In existing companies, a Shareholders Agreement can be entered into at any time, provided all shareholders and the company consent. See also

Definitive Agreement for the final binding nature of such contracts.