Why a Subscription Agreement Matters in Private Capital Raising

Startups, private companies, and investment funds use subscription agreements to raise equity capital efficiently without the cost and complexity of a public offering. The agreement serves multiple critical functions: it creates a binding commitment from the investor to fund the purchase of shares; it provides the company with enforceable representations about the investor’s accredited status and sophistication; it includes legally required risk disclosures; and it establishes the closing mechanics, including payment and share issuance. For investors, the subscription agreement sets out their rights, the price, and the conditions under which their capital will be deployed. For both parties, it is the definitive record of the transaction.

✨ GTsetu Insight, Counterparty Verification in Capital Raises

Before accepting a subscription agreement, companies should verify the investor’s identity, accredited status, and source of funds. GTsetu verifies companies using government tie‑ups across six points: legal name, registered address, registration number, company status, company type, and date of certificate of incorporation. Import licences, certifications, financial standing, and accredited investor status are not verified by GTsetu and must be validated directly between parties. This provides a verified baseline for counterparty identity before proceeding with capital raising discussions. Learn more in our good faith negotiation and business verification guides.

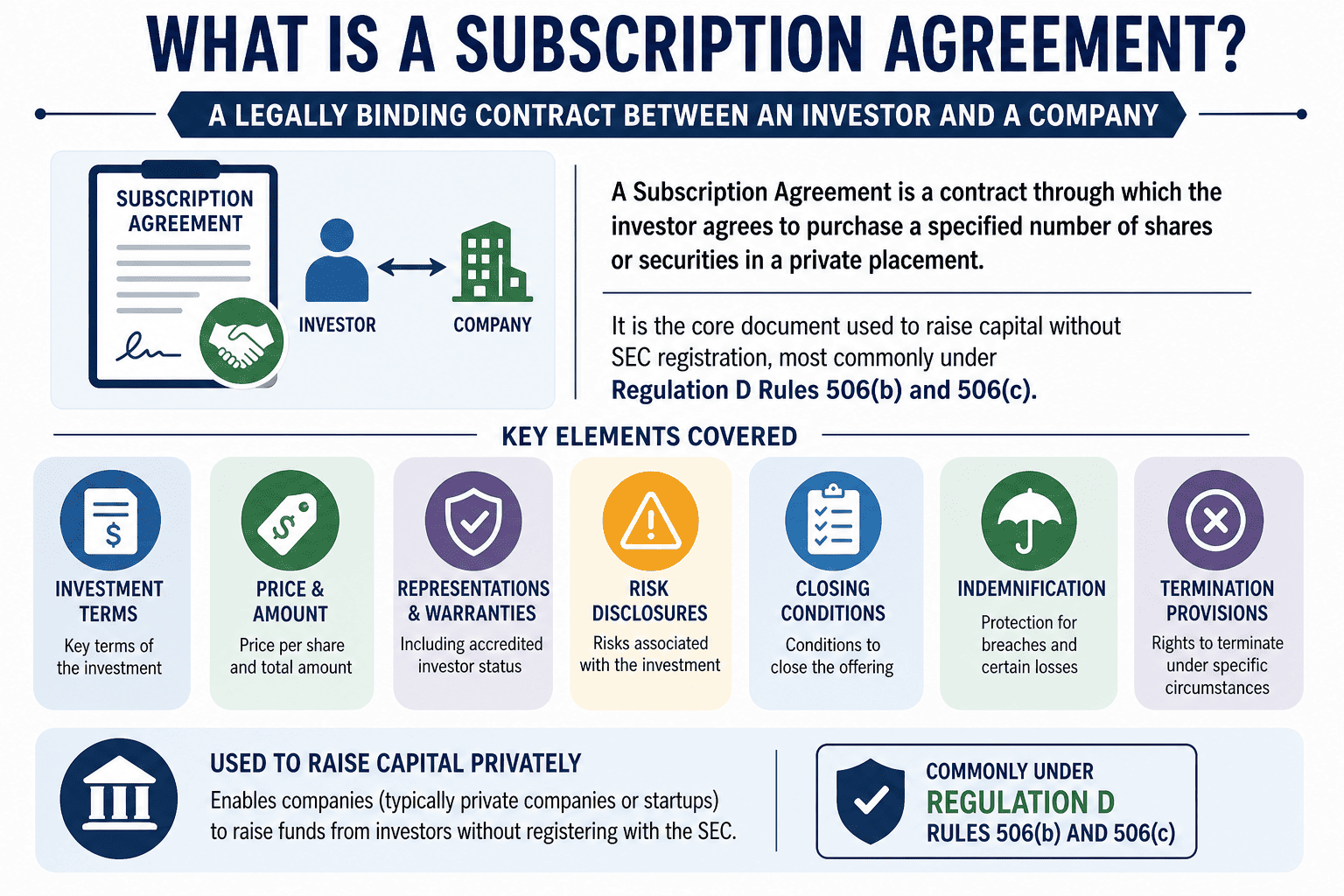

Key Components of a Subscription Agreement

🧑💼

Investor Information

Legal name, address, contact details, and (for entities) organisational documents.

💰

Investment Terms

Number of shares, price per share, total consideration, and security type (common, preferred, convertible).

✅

Representations & Warranties

Investor accredited status, sophistication, access to information, and understanding of risks. Company authority to issue shares.

⚠️

Risk Disclosure

Legally required description of material risks, illiquidity, loss of capital, dilution, regulatory risks.

🔒

Closing Conditions

Minimum subscription amount, due diligence completion, board approval, no material adverse change.

🛡️

Indemnification

Investor agrees to indemnify the company for losses caused by breach of representations.

⚖️

Governing Law & Dispute Resolution

Choice of law, jurisdiction, and arbitration or court forum, essential in cross-border subscriptions.

Regulation D, Rule 506(b) vs. 506(c)

| Feature | Rule 506(b) | Rule 506(c) |

|---|

| General solicitation / advertising | ❌ Prohibited | ✅ Permitted (JOBS Act) |

| Investor type | Unlimited accredited investors + up to 35 non‑accredited (sophisticated) | All accredited investors |

| Verification of accredited status | No prescribed verification (reliance on investor representations) | Reasonable steps required (e.g., tax returns, third‑party letters) |

| Capital raising limit | No limit | No limit |

| Form D filing required | Yes (within 15 days of first sale) | Yes (within 15 days of first sale) |

| Preemption of state law | Yes, “blue sky” preempted | Yes, “blue sky” preempted |

Subscription Agreement vs. Stock Purchase Agreement

| Dimension | Subscription Agreement | Stock Purchase Agreement (SPA) |

|---|

| Nature of transaction | Primary issuance, company issues new shares | Secondary transfer, existing shares sold by shareholder |

| Capital goes to | The company (treasury increases) | The selling shareholder |

| Typical context | Private placement, startup financing, crowdfunding | M&A, secondary sale, venture capital secondary |

| Key representations | Investor accredited status, company authority to issue | Seller title to shares, company representations and warranties |

✨ GTsetu Guidance, Cross‑Border Subscriptions

When an investor and company are located in different jurisdictions, the subscription agreement must address securities law compliance in both jurisdictions, foreign exchange controls, and tax withholding. A well‑drafted governing law and dispute resolution clause is essential. GTsetu’s cross‑border collaboration framework helps parties engage with government‑tie‑up verified counterparties (6 points: name, address, registration number, status, type, incorporation date) from the outset. See our Conditional Agreement and Definitive Agreement resources for related transaction structures.

Real‑World Example: Standard Subscription Agreement Structure

📄 Signature Page Excerpt (SEC Filing)

“The undersigned (the ‘Subscriber’), desires to become a holder of common shares … in consideration of $0.10 per share. The Subscriber acknowledges that the Company reserves the right, in its sole and absolute discretion, to accept or reject this subscription.”

Source: SEC Form D filing, typical for Rule 506(b) offerings.

🧾 Standard Closing Mechanics

- Investor delivers executed signature page

- Investor wires funds to escrow or company account

- Company countersigns and issues share certificate

- Closing occurs upon countersignature and fund receipt

Common Risks & Drafting Pitfalls in Subscription Agreements

🚩

Failure to verify accredited investor status (Rule 506(c))

Under Rule 506(c), the company must take “reasonable steps” to verify accredited status. Relying solely on a check‑the‑box representation is insufficient and can jeopardise the exemption, exposing the company to SEC enforcement and rescission rights.

🚩

Inadequate risk disclosures

Subscription agreements must include a clear, specific, and non‑boilerplate description of risks, illiquidity, dilution, loss of capital, and any industry‑ or company‑specific risks. Vague disclosures may be challenged as misleading, particularly if a non‑accredited investor is involved.

🚩

No governing law or jurisdiction clause

Cross‑border subscriptions without an explicit governing law clause create uncertainty about which country’s securities laws apply. Always include a binding clause specifying governing law and dispute resolution forum.

🚩

Confusing subscription agreement with a term sheet or LOI

A subscription agreement is a definitive, binding purchase contract, not an Expression of Interest or Letter of Intent. Parties sometimes treat it as a preliminary step, but once countersigned, it is fully enforceable.

How a Subscription Agreement Is Executed

01

Term sheet / LOI (non‑binding)

Parties agree principal terms, investment amount, valuation, security type, and any conditions, in a non‑binding term sheet. This step often includes a confidentiality agreement and exclusivity provision.

02

Due diligence & disclosure

Company provides offering documents, risk disclosures, and financial information. Investor conducts its own due diligence and confirms accredited status, where required.

03

Subscription agreement drafting & negotiation

Company provides its form subscription agreement. Investor negotiates representations, indemnification scope, and closing conditions. Both parties should involve securities counsel.

04

Execution & closing

Investor signs signature page and delivers funds. Company countersigns, accepts subscription, and issues shares (or confirms share issuance). Closing occurs; Form D filed within 15 days.

Frequently Asked Questions

QIs a subscription agreement legally binding?

Yes, a properly executed subscription agreement is fully legally binding. Once the investor signs and delivers funds, and the company countersigns (or accepts the subscription), both parties are obligated to perform: the investor to pay the subscription amount, the company to issue the shares. The agreement is not conditional on further negotiation unless the parties expressly include closing conditions.

QWhat is an accredited investor, and why does it matter?

An accredited investor is an individual or entity that meets specific income or net worth thresholds (e.g., $200k individual income, $1M net worth excluding primary residence). In private placements under Regulation D, offerings to accredited investors are significantly easier to conduct, there is no cap on the number of accredited investors, and under Rule 506(c), only accredited investors may participate. The investor’s representation of accredited status is a core warranty in any subscription agreement.

QWhat is the difference between a subscription agreement and a share purchase agreement (SPA)?

A subscription agreement is used for a primary issuance, the company creates and issues new shares directly to the investor, and the capital goes to the company. A share purchase agreement (or stock purchase agreement) is used for a secondary transfer, an existing shareholder sells their shares to a buyer, and the consideration goes to the selling shareholder. In M&A, an SPA is the definitive agreement for an acquisition. In startup financing, a subscription agreement is the standard document for a priced equity round.

QDo I need a lawyer to draft or sign a subscription agreement?

Yes, both investors and companies should engage securities counsel before signing a subscription agreement. The agreement involves complex securities law compliance, risk disclosure obligations, and representations that have long‑term consequences. Using a template without legal review can lead to unenforceable provisions, failed exemptions, and investor rescission claims. For companies relying on Rule 506(c), the verification of accredited status must be documented and legally defensible, a process that requires legal guidance.

QWhat happens if an investor breaches a representation in the subscription agreement?

Most subscription agreements contain an indemnification clause requiring the investor to cover losses the company suffers as a result of a breach of representations, for example, if the investor misrepresents their accredited status and the company loses its Regulation D exemption. The company may also have the right to void the subscription and return funds. These provisions are heavily negotiated; investors should ensure their representations are accurate and their indemnification obligation is capped appropriately.