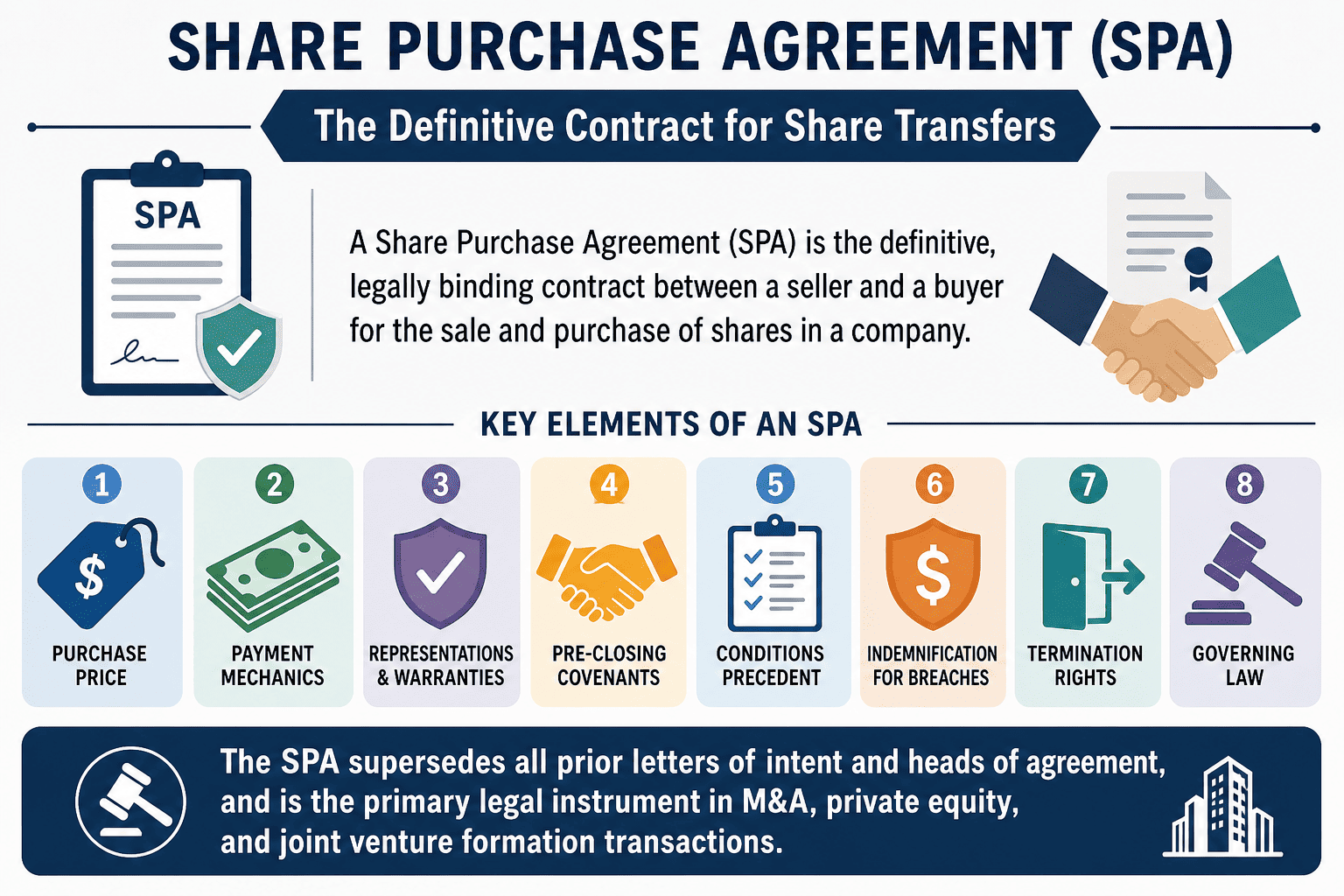

Why a Share Purchase Agreement is the Cornerstone of M&A

In any transaction where a buyer acquires shares of a company, whether a controlling stake, a minority investment, or a full acquisition, the Share Purchase Agreement is the single most important legal document. It records the commercial bargain, allocates risk between buyer and seller through representations, warranties, and indemnities, and governs every aspect of the transaction from signing to closing and beyond. Unlike a Letter of Intent or Memorandum of Understanding, which are typically non-binding on commercial terms, an SPA is fully and immediately binding on its execution, subject only to the satisfaction of agreed conditions precedent.

⚡ Critical Distinction

A Share Purchase Agreement is the definitive agreement, it supersedes all prior documents. Terms agreed in a Letter of Intent or Term Sheet that are not carried forward into the SPA are not binding. Conversely, an SPA often operates as a Conditional Agreement when closing is subject to regulatory approvals or other conditions precedent. Understanding the relationship between the SPA and pre-contractual instruments is essential to avoid gaps in the contractual framework.

SPA vs Asset Purchase Agreement

Share Purchase Agreement vs Asset Purchase Agreement

One of the most fundamental structural choices in any acquisition is whether to structure the transaction as a share purchase (SPA) or an asset purchase (APA). The choice has profound tax, liability, and execution implications.

| Dimension | Share Purchase Agreement (SPA) | Asset Purchase Agreement (APA) |

|---|

| What is transferred | Shares of the target company, the entire legal entity | Individual assets (equipment, inventory, IP, contracts) and specified liabilities |

| Liability assumption | Buyer inherits all historical liabilities, disclosed and undisclosed | Buyer selects which liabilities to assume; seller retains residual liabilities |

| Tax treatment | Often more tax-efficient for sellers (capital gains); less favourable for buyers (no step-up in asset basis in many jurisdictions) | Buyer gets stepped-up basis in acquired assets; seller may face higher ordinary income tax |

| Third-party consents | Generally fewer consents, share transfer may not trigger change-of-control provisions in all contracts | Each material contract may require novation or assignment; landlord, customer, and lender consents often required |

| Complexity & execution | Simpler, single transfer of shares, one set of transfer documents | More complex, asset-by-asset transfer, multiple conveyancing documents, potential VAT/transfer tax on each asset category |

| Typical use cases | M&A, private equity buyouts, joint venture investments, strategic acquisitions | Distressed sales, carve-outs, acquisitions where buyer wants to exclude specific liabilities |

For most cross-border strategic acquisitions, the Share Purchase Agreement is the preferred structure because of its relative simplicity and the ability to acquire an ongoing business as a going concern. However, buyers must price the risk of inheriting unknown liabilities through intensive due diligence and robust indemnification provisions in the SPA.

Key Clauses of an SPA

Essential Clauses of a Share Purchase Agreement

A well-drafted Share Purchase Agreement is a comprehensive legal instrument, typically 50 to 200 pages plus schedules. The following clauses appear in virtually every SPA and represent the principal points of negotiation between buyer and seller.

✓

Parties & Recitals

Identifies seller(s), buyer(s), the target company, and sets out the commercial background and intent of the transaction.

✓

Sale & Purchase of Shares

Specifies the number, class, and percentage of shares being transferred; confirms that shares are sold free of all encumbrances.

✓

Purchase Price & Payment Mechanics

Total consideration, currency, deposit, closing payment, escrow or holdback amounts, earn-out provisions, and working capital adjustment mechanism.

✓

Conditions Precedent (CPs)

Regulatory approvals, third-party consents, due diligence completion, accuracy of reps, and other prerequisites before closing. See Condition Precedent.

✓

Representations & Warranties (Seller)

Factual statements by seller: ownership of shares, financial statements accuracy, compliance with laws, no litigation, IP ownership, tax status, material contracts, ESG compliance.

✓

Representations & Warranties (Buyer)

Authority to enter the transaction, availability of funds, status as an accredited investor or corporate entity.

✓

Pre-Closing Covenants

Seller’s obligation to operate the business in the ordinary course between signing and closing, restrictions on dividends, asset sales, debt incurrence, and material contracts.

✓

Indemnification

Obligation of seller to compensate buyer for losses arising from breach of reps, warranties, or specified liabilities. Key terms: basket (threshold), cap (maximum liability), survival period (time limit), escrow funding.

✓

Closing Mechanics & Deliveries

Date, place, and manner of closing; share certificates, transfer forms, board resignations, legal opinions, and ancillary documents to be delivered.

✓

Termination Rights

Grounds for termination before closing: failure of conditions precedent by long-stop date, material breach, mutual agreement. Consequences: return of deposits, break fees, reverse break fees.

✓

Non-Compete & Non-Solicitation

Post-closing restrictions on seller competing with the acquired business or soliciting employees/customers. See Non-Compete Clause.

✓

Confidentiality & NDA

Protection of transaction-related information and ongoing confidentiality obligations post-closing. See NDA.

✓

Governing Law & Dispute Resolution

Choice of governing law (e.g., English law, New York law) and dispute mechanism (arbitration under SIAC, ICC, LCIA, or litigation in specified courts). Essential for cross-border SPAs.

✓

Schedules & Disclosure Letter

Attachments containing details of shares, financial statements, IP registrations, material contracts, and exceptions to representations and warranties (the disclosure letter).

✨ GTsetu Guidance on SPA Negotiation

The representations and warranties section is the most heavily negotiated part of any Share Purchase Agreement. Sellers seek to narrow warranties with materiality qualifiers, knowledge limitations, and robust disclosure schedules. Buyers seek broad, unqualified warranties to maximise post-closing indemnification claims. Achieving the right balance requires both parties to act in good faith throughout the due diligence and drafting process. GTsetu’s verified partner network helps companies identify counterparties with proven transaction discipline, reducing the risk of bad-faith negotiating tactics during SPA finalisation.

Conditions Precedent in an SPA

Conditions Precedent: What Must Happen Before Closing

Most Share Purchase Agreements are structured as Conditional Agreements, both parties are bound immediately, but the obligation to close (complete the share transfer and pay the price) is deferred until specified conditions are satisfied or waived. Conditions precedent are critical risk-allocation devices; they allow the buyer to walk away without liability if key prerequisites are not met.

| Category | Typical Conditions Precedent in an SPA | Party Protected |

|---|

| Regulatory | Competition/merger control clearance; foreign investment approval; sector-specific licences (banking, telecom, pharma, defence). Both. |

| Third-party consents | Consent of lenders, key customers, landlords, joint venture partners where change of control triggers termination rights. Buyer |

| Due diligence | Satisfactory completion of legal, financial, technical, and ESG due diligence; no material adverse change (MAC). Buyer |

| Financial | Confirmation of financing; financial close; release of escrowed funds; no material indebtedness outside disclosed amounts. Buyer |

| Corporate approvals | Shareholder approval (seller’s and buyer’s shareholders); board resolutions authorising the transaction. Both |

| Representations & warranties | Accuracy of seller’s reps and warranties as of closing (bring-down condition). Buyer |

| Covenant compliance | Seller’s performance of pre-closing covenants, no material breach. Buyer |

| No litigation | No material legal proceeding threatened or pending that would prohibit the transaction. Both |

Each condition precedent must be capable of objective verification. A condition defined as “satisfactory completion of due diligence” without objective criteria creates a dispute opportunity, the buyer could claim the condition is unsatisfied for any reason, effectively holding a unilateral termination right. Sophisticated SPAs define due diligence conditions with reference to specific material adverse findings, or replace them with a general MAC clause and robust representations.

Representations, Warranties & Indemnities

Representations, Warranties & Indemnification, The Risk Allocation Engine

The representations and warranties (R&W) section of an SPA is the primary mechanism for allocating risk between buyer and seller. Representations are factual statements about the company, its business, and its affairs. Warranties are promises that those factual statements are true. If a representation is inaccurate (breach of warranty), the buyer is entitled to claim indemnification from the seller for losses suffered.

🔍 Most Heavily Negotiated R&W Categories

Financial statements (accuracy, no undisclosed liabilities) • Title to shares (no encumbrances) • Tax compliance and payment • Intellectual property ownership and infringement • Material contracts (validity, no breach) • Litigation and regulatory proceedings • Environmental compliance • Employment and labour relations • Data privacy and cybersecurity (GDPR, DPDP) • Anti-corruption (FCPA, UK Bribery Act) • ESG compliance (modern slavery, supply chain due diligence).

The indemnification section then defines the procedural and financial framework for claims:

- Basket (threshold): The minimum loss amount that must be reached before the buyer can make an indemnity claim. Typically 0.5%–1% of purchase price. Losses below the basket are borne by the buyer.

- Cap (maximum liability): The maximum aggregate amount the seller can be required to pay under indemnification. Typically 10%–30% of purchase price, but in some transactions the cap equals 100% of consideration.

- Survival period: The time after closing during which the buyer can bring indemnification claims. Typically 12–24 months for general warranties; tax and fundamental warranties (title, authority) often survive longer (statute of limitations or indefinitely).

- Escrow / holdback: A portion of the purchase price (often 10%) held back at closing or placed into an escrow account to secure the seller’s indemnification obligations for the survival period.

✨ GTsetu Note on Cross-Bridge SPA Negotiations

In cross-border SPAs, the interaction between indemnification provisions and local law mandatory rules can create unexpected outcomes. For example, under Indian law, indemnification claims for breach of representations are treated as contractual claims subject to the Limitation Act; under English law, different limitation periods apply. The choice of governing law in the SPA determines not only the interpretation of clauses but also the availability of indemnification as a remedy. Always engage legal counsel in both the buyer’s and seller’s jurisdictions before finalising the indemnification framework.

SPA in the Transaction Lifecycle

Where the Share Purchase Agreement Fits in the Transaction Lifecycle

The Share Purchase Agreement is the culmination of a structured deal process. Understanding its position in the sequence of documents is essential for both buyers and sellers.

| Document | Binding Nature | Role in M&A Process | Typical Stage |

|---|

| Expression of Interest (EoI) | Non-binding commercially | Initial expression of interest; often includes indicative price range | Earliest stage |

| NDA | Fully binding | Protects confidentiality of information exchanged during due diligence | Before any material disclosure |

| Letter of Intent (LOI) / Heads of Agreement | Commercial terms non-binding; exclusivity & confidentiality binding | Records principal terms: price, structure, key conditions | Mid; before due diligence |

| Term Sheet | Generally non-binding | Detailed economic and governance terms as basis for SPA negotiation | Mid; post LOI |

| Share Purchase Agreement (SPA) | Fully binding | Definitive contract for the share transfer | Post due diligence; execution |

| Unconditional / Definitive Agreement | Once all conditions precedent are satisfied or waived, the SPA becomes unconditional and closing occurs. |

Common Drafting Pitfalls

Common SPA Drafting Pitfalls and How to Avoid Them

⚠️

Vague defines

Ambiguous definitions (e.g., “Material Adverse Change” without carve-outs) lead to disputes at closing. Define every key term precisely in the definitions section.

⚠️

Realistic long-stop dates

A long-stop date that is too short for regulatory approvals (e.g., CCI clearance in India takes 6–12 months) forces premature termination.

⚠️

Missing bring-down condition

Without a provision requiring representations to be true at both signing and closing, the seller could breach a warranty between signing and closing without penalty.

⚠️

Incomplete disclosure schedule

A disclosure letter that does not specifically qualify each representation leaves the seller exposed to indemnification claims for matters they thought were disclosed but were not clearly listed.

⚠️

Ignoring Indian Section 27

Post-closing non-compete clauses in an SPA governed by Indian law may be void under Section 27 of the Contract Act unless the restriction is limited to the sale of goodwill. See non-compete clause guide.

FAQ

Frequently Asked Questions

QWhat is the difference between a Share Purchase Agreement and a Shareholders Agreement?

A Share Purchase Agreement (SPA) governs the transaction by which a seller transfers shares to a buyer, it is a one-time transfer contract. A Shareholders Agreement governs the ongoing relationship between shareholders after the acquisition, it covers governance, board composition, transfer restrictions (right of first refusal, tag-along, drag-along), dividend policy, and dispute resolution. In many acquisitions, both are executed: the SPA for the transfer, and a revised or new Shareholders Agreement for the post-closing relationship among the buyer and any remaining minority shareholders.

QCan a Share Purchase Agreement be terminated after signing?

Yes, under the termination provisions set out in the SPA. Typical termination grounds include: failure of a condition precedent to be satisfied by the long-stop date; material breach of a representation, warranty, or covenant that is not cured within a specified period; or mutual agreement of the parties. If the buyer terminates due to the seller’s breach, the SPA may provide for return of any deposit plus payment of a break fee. If the buyer terminates because it cannot obtain financing, a reverse break fee may be payable to the seller. Termination does not affect obligations that survive, typically confidentiality and governing law.

QWhat is an escrow in an SPA context?

An escrow arrangement involves depositing a portion of the purchase price (typically 10–20%) into a separate account held by an independent escrow agent at closing. The escrow amount is released to the seller after the survival period (e.g., 18 months post-closing), minus any amounts claimed by the buyer for indemnification. Escrow gives the buyer financial security for the seller’s indemnification obligations without requiring the buyer to pursue the seller directly for each claim. The terms of the escrow, release conditions, dispute mechanism, interest accrual, are set out in a separate Escrow Agreement referenced in the SPA.

QWhat are the most common representations and warranties in an SPA?

Standard seller representations cover: title to shares (no encumbrances); authority to enter the transaction; financial statements (accuracy, no undisclosed liabilities); tax filings and payments; ownership of intellectual property; material contracts (validity, no breach); environmental compliance; labour and employment matters; litigation (no pending proceedings); data privacy compliance (GDPR, DPDP, CCPA); anti-corruption (FCPA, UK Bribery Act); and ESG/supply chain compliance. The disclosure letter attached to the SPA qualifies each representation, anything disclosed there is carved out from the seller’s warranty and is not subject to indemnification.