Why Is a Term Sheet Used in Fundraising & M&A?

A Term Sheet appears at the critical juncture when an investor or acquirer moves from expression of interest to a structured proposal. Its primary function is to establish alignment on the core economic and governance terms before significant legal expenses and due diligence begin. It allows both parties to negotiate the key points without yet committing to a binding agreement.

For startups, a Term Sheet from a lead VC is the formal start of a priced funding round (Series A and beyond). For M&A, it outlines the proposed structure of an acquisition. It provides clarity, sets expectations, and protects both sides during the subsequent due diligence period through binding clauses like exclusivity. It’s a tool for efficient negotiation, ensuring that time and money aren’t wasted drafting final contracts for a deal that lacks fundamental alignment.

⚡ Key Principle

A Term Sheet is a negotiation tool, not a final contract. However, its terms—especially valuation, liquidation preference, and control provisions—will profoundly shape the final binding agreements. Treating it as a mere formality is a common and costly mistake for founders.

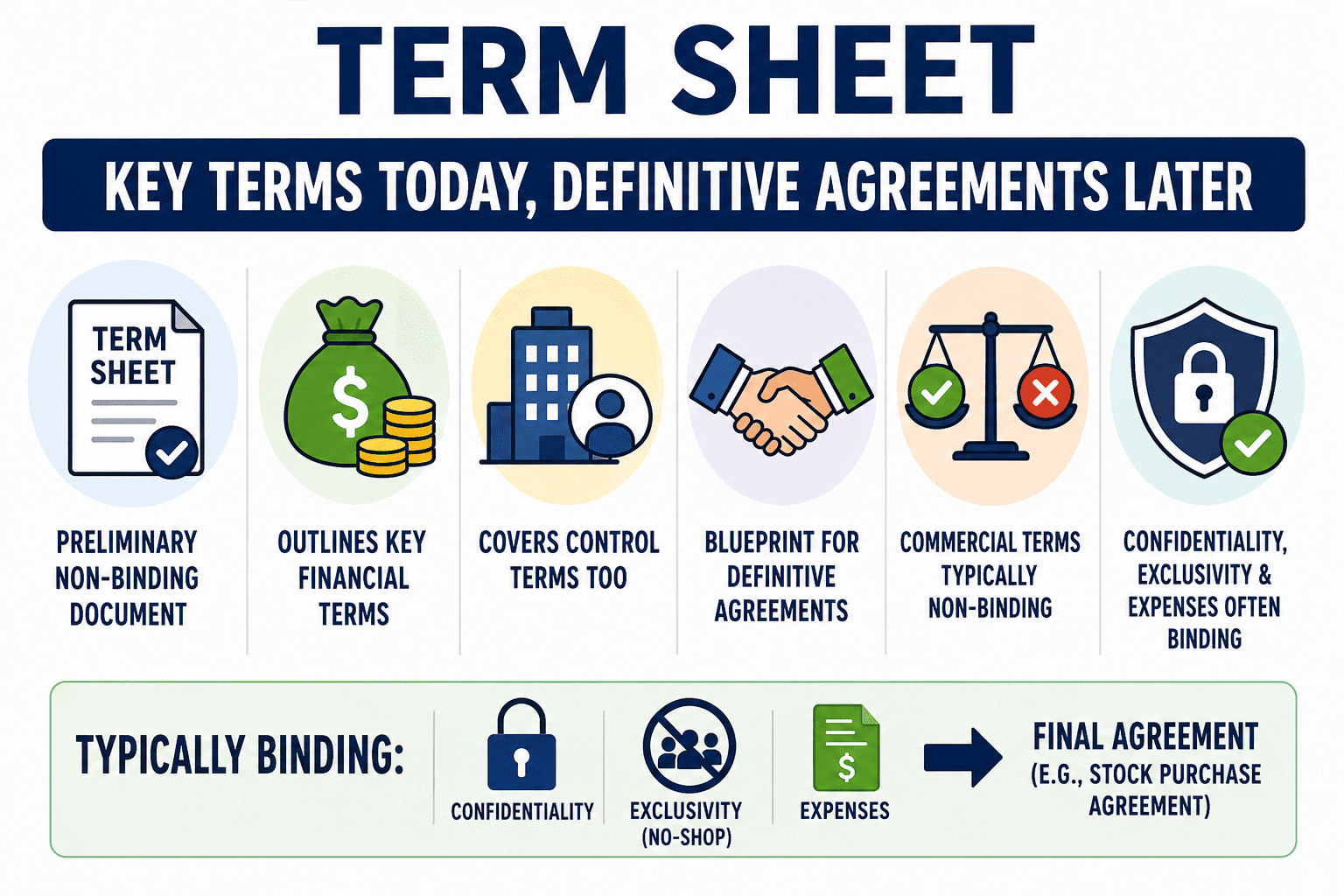

Binding vs Non-Binding

Binding vs Non-Binding: What a Term Sheet Commits You To

Like an LOI, a Term Sheet is a hybrid document. The commercial “deal points” are usually non-binding, while certain “procedural” or “behavioral” clauses are binding from the moment of signature. This distinction must be explicitly stated.

✅ Typically Binding Clauses

- Confidentiality (NDA): Prevents disclosure of deal terms and sensitive information.

- Exclusivity / No-Shop Clause: Bars the company from seeking other offers for a defined period.

- Governing Law & Jurisdiction: Specifies which laws apply to the binding parts.

- Expenses / Break Fees: Allocates costs (e.g., legal fees) if the deal fails.

- Expiration Date: The Term Sheet becomes void if a definitive agreement isn’t signed by this date.

⚠️ Typically Non-Binding Clauses

- Pre-money valuation & price per share

- Investment amount & ownership percentage

- Liquidation preference terms

- Anti-dilution provisions

- Board composition & voting rights

- Employee option pool size

- All commercial representations and warranties

✨ Practical Guidance

Never assume a clause is non-binding just because the header says “non-binding.” The document must clearly state which provisions survive as binding obligations. Always have legal counsel review the Term Sheet before signing, focusing particularly on the binding “no-shop” and confidentiality sections.

Anatomy of a Term Sheet

Key Components of a Term Sheet

Term sheets are structured around two main categories: economic terms (who gets what) and control terms (who decides what).

💰

Valuation & Offering

Pre-money valuation: company worth before investment. Post-money valuation: pre-money + new investment. Determines investor’s ownership %.

📊

Liquidation Preference

Determines payout order in a sale. Investors often get their money back (1x) before common shareholders receive anything. Can be participating or non-participating.

🛡️

Anti-Dilution

Protects investors if the company raises money later at a lower valuation (“down round”). Weighted average is standard; full ratchet is founder-unfriendly.

🗳️

Board & Control

Defines board composition (founders, investors, independents) and which major decisions (e.g., sale, budget) require investor approval (protective provisions).

📋

Option Pool

Shares reserved for future employees. Often created before the investment, which dilutes the founders’ pre-money valuation, not the investors.

🚪

Exit / Redemption

Pro-rata rights (right to invest in future rounds), drag-along rights (force minority to join a sale), and redemption rights (investors can force company to buy shares after a period).

Understanding Equity Dilution: A Worked Example

1

Founders own 1,000,000 shares (100% of the company).

2

Investor puts in £1,000,000 for 20% of the post-money valuation (£5M).

3

New shares issued: 250,000 shares to investor. Total shares now = 1,250,000.

4

Founders still own 1M shares, but now only 80% of the company. They have been diluted.

Note: Dilution isn’t necessarily bad if the £1M investment grows the value of the remaining 80% beyond the prior value of 100%.

Term Sheet vs LOI vs MoU

Term Sheet vs LOI vs MoU: Key Differences

While often conflated, these documents have distinct conventions and use cases.

| Dimension |

Term Sheet |

Letter of Intent (LOI) |

Memorandum of Understanding (MoU) |

| Primary Use |

VC/PE investment, startup financing, debt financing |

M&A, commercial contracts, supply agreements, real estate |

Institutional partnerships, government agreements, joint ventures |

| Focus |

Detailed economic & control terms (valuation, liquidation pref, anti-dilution, board seats) |

Broad commercial structure, price range, due diligence framework |

High-level principles, collaboration framework, shared objectives |

| Typical Length |

3–10 pages |

1–5 pages |

2–6 pages |

| Binding Provisions |

Confidentiality, no-shop, expenses, governing law |

Confidentiality, exclusivity, governing law |

Often entirely non-binding, but can have binding confidentiality |

Risks & Pitfalls

Common Term Sheet Pitfalls for Founders

🚩

Overvaluing the Company

A sky-high valuation seems great, but can lead to a punishing down round later if growth targets aren’t met, triggering harsh anti-dilution clauses and damaging morale.

🚩

Ignoring the Option Pool

If a 20% option pool is created pre-money, it effectively reduces the founders’ ownership by 20% before the investor’s money even comes in. The cost of the pool is borne by the founders, not the investors.

🚩

Misunderstanding Liquidation Preference

A 2x participating preference means investors get twice their money back and then share in the remaining proceeds. This can leave founders with nothing in a modest exit.

🚩

Overly Broad Protective Provisions

Giving investors veto power over operational decisions (e.g., hiring, budget, new products) can cripple founder control. These should be limited to fundamental changes (sale of company, changing share structure).

🚩

Long No-Shop Clause

Agreeing to a 90-day exclusivity period without milestones gives the investor a long time to conduct due diligence while you’re locked out from talking to other potential backers.

From Term Sheet to Closing

The Path from Term Sheet to Definitive Agreement

01

Signing the Term Sheet

Binding clauses (confidentiality, no-shop) take effect immediately. Negotiations on final documents begin.

02

Due Diligence

Investor scrutinises financials, IP, contracts, team, and legal structure. This is intensive and can take 30-90 days.

03

Definitive Agreements Drafted

Lawyers draft the Stock Purchase Agreement, Investors’ Rights Agreement, Voting Agreement, etc., incorporating Term Sheet terms.

04

Final Review & Board Approval

Both parties review final documents. Company board approves the transaction.

05

Closing & Funding

Documents are signed, funds are transferred, and new shares are issued. The deal is done.

FAQ

Frequently Asked Questions

Q

Is a Term Sheet legally binding?

A Term Sheet is typically non-binding with respect to its commercial and economic terms (like valuation and investment amount). However, certain procedural clauses are often explicitly binding, including confidentiality, exclusivity (no-shop clause), governing law, and expense provisions. The document must clearly state which sections are binding.

Q

What’s the difference between a Term Sheet and a Letter of Intent (LOI)?

While often used interchangeably, a Term Sheet is more commonly associated with venture capital financing and focuses on detailed economic and control terms (valuation, liquidation preferences, anti-dilution). An LOI is broader, often used in M&A, partnerships, or commercial contracts, and tends to outline the overall structure and commercial intent of a transaction. Both are typically non-binding precursors to definitive agreements.

Q

What is a “no-shop” clause in a Term Sheet?

A “no-shop” clause (or exclusivity clause) is a binding provision that prevents the company from soliciting, encouraging, or negotiating with other potential investors or buyers for a specified period (usually 30-90 days). It gives the investor time to conduct due diligence without the risk of the company using their offer as leverage to get a better deal elsewhere.

Q

What is a liquidation preference?

A liquidation preference determines the payout order in a liquidity event, such as a sale or IPO. It gives preferred shareholders (investors) the right to receive their investment back (and sometimes a multiple) before common shareholders (founders, employees) receive any proceeds. It is a key economic term designed to protect an investor’s downside.