How a Condition Precedent Works

In contract law, parties frequently need to commit to a transaction before every prerequisite for safe completion has been confirmed. A Condition Precedent (CP) is the legal mechanism that enables them to do so — creating a binding commitment while deferring the obligation to perform until a specified event has occurred.

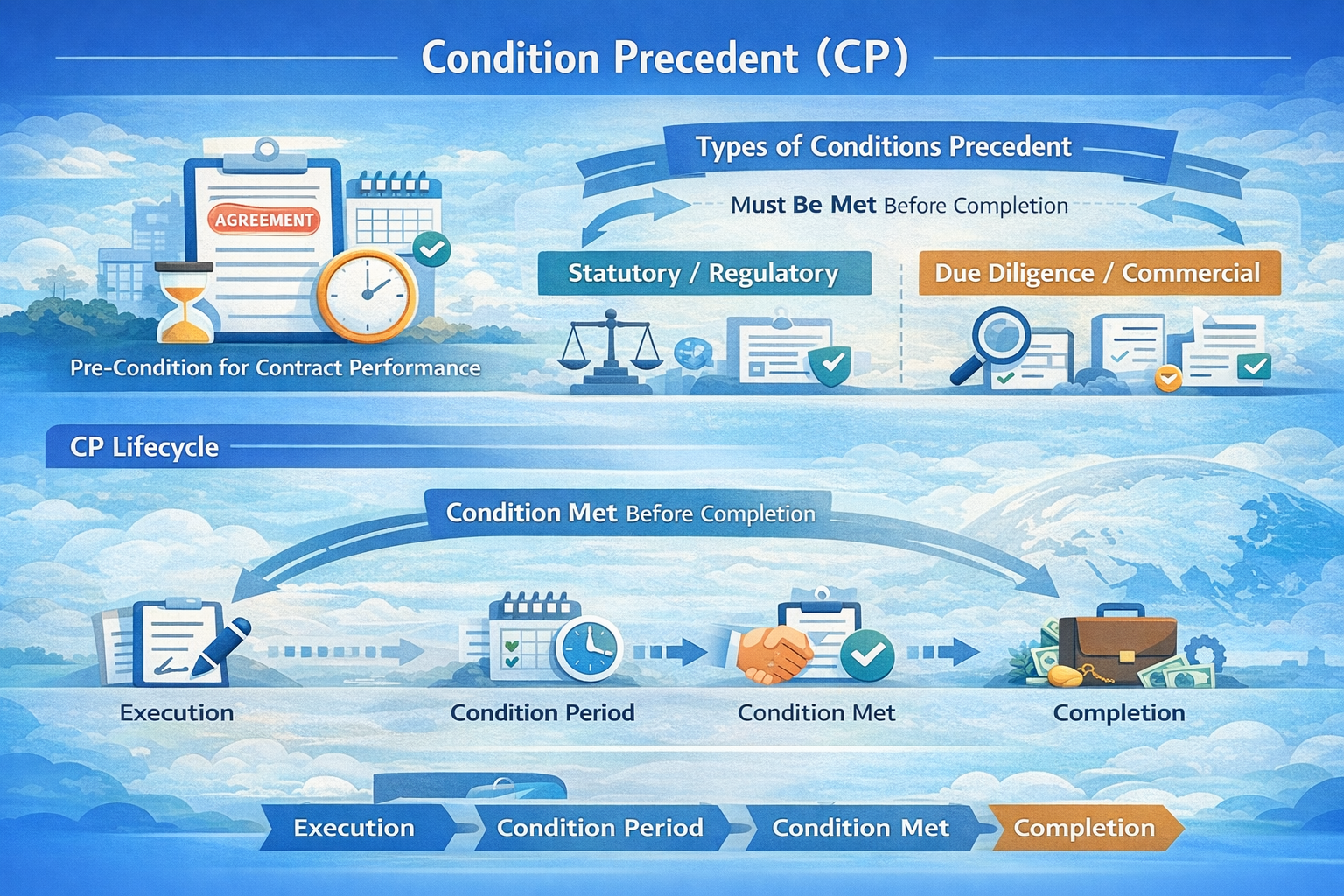

Once the parties execute a Conditional Agreement, the contract is immediately legally binding. What is conditional is not the agreement itself but the obligation to perform the principal commercial act — the transfer of shares, the purchase of land, the commencement of supply, the deployment of investment capital. Until the CP is satisfied, no party is obliged to proceed with that act. Once the CP is satisfied, performance becomes due.

The mechanism is structured around a condition period — a defined timeframe within which the relevant events must occur — and a long-stop date, which is the outer deadline by which all conditions must be satisfied. If they are not, the agreement lapses or is terminated, and the principal obligations are never triggered. This structure is particularly valuable in cross-border transactions, where regulatory timelines, due diligence complexity, and financing conditions mean that the gap between agreement and completion may be substantial.

⚡ Critical Distinction

A Condition Precedent defers the obligation to perform — it does not defer the binding force of the agreement. Ancillary obligations such as confidentiality, conduct during the condition period, notification duties, and governing law apply immediately upon execution. If a party wrongfully prevents a condition from being satisfied — for example, by withdrawing cooperation from a required regulatory filing or failing to provide requested documentation — courts across most jurisdictions will hold that party liable. The conditional structure is not a mechanism for avoiding binding commitments; it is a mechanism for structuring the timing of performance.

Types of Conditions Precedent

Types of Conditions Precedent in Commercial Agreements

In international trade and investment transactions, Conditions Precedent typically fall into two broad categories: statutory conditions precedent and due diligence conditions precedent. Understanding both categories — and how they interact — is essential to structuring the condition period effectively.

⚖️ Statutory / Regulatory CPs

Required by Law or Regulation

Conditions that arise from legal or regulatory requirements applicable to the transaction — the satisfaction of which is a prerequisite imposed not by the parties but by the relevant regulatory framework.

- Competition / merger control clearance

- Foreign investment regulatory approval

- Sector-specific licensing (financial services, pharma, telecom)

- Government or ministry consent

- Environmental or planning permission

- Import / export licence confirmation

- Exchange control approvals in regulated jurisdictions

🔍 Due Diligence & Commercial CPs

Agreed by the Parties to the Transaction

Conditions that the parties themselves define based on the commercial prerequisites they require to be comfortable proceeding — typically arising from the findings of a due diligence exercise or commercial negotiation.

- Satisfactory completion of legal and financial due diligence

- Confirmation of financing or financial close

- Third-party consent or waiver (key customers, lenders, landlords)

- Restructuring of target entity’s liabilities

- Achievement of agreed quality, technical, or certification standards

- Execution of key underlying contracts or licences

- Resolution of identified litigation or regulatory exposure

✨ GTsetu Guidance

In cross-border transactions structured with GTsetu’s support, the CP schedule is one of the most carefully negotiated components of any Conditional Agreement. The allocation of responsibility for satisfying each CP — which party bears the cost, the risk, and the legal obligation to pursue satisfaction — directly determines the commercial risk profile of the transaction. A CP schedule drafted without clear responsibility allocation and realistic timelines creates exactly the kind of disputes that terminate transactions at the condition stage.

Real-World Example

A Condition Precedent in Practice: The PayU–BillDesk Acquisition

The consequences of an unsatisfied Condition Precedent are not merely theoretical. One of the most significant recent examples in international M&A demonstrates precisely how a CP failure terminates even the largest of transactions.

📌 Case Study — M&A Transaction

In August 2021, PayU (part of the Dutch technology investment group Prosus) announced the acquisition of BillDesk, an Indian payment gateway, for approximately USD 4.7 billion — at the time the second-largest buyout of an Indian digital technology company after Walmart’s acquisition of Flipkart.

The acquisition agreement was subject to a statutory Condition Precedent: approval from the Competition Commission of India (CCI). That approval was obtained in September 2022 — more than a year after the announcement. However, the acquisition agreement contained a long-stop date of 30 September 2022. On 3 October 2022, Prosus announced that the transaction had been terminated.

The reason given was unambiguous: certain conditions precedent were not fulfilled by the September 30, 2022 long-stop date, causing the agreement to terminate automatically. The transaction — worth USD 4.7 billion — lapsed not because the parties had lost interest, but because the CP machinery operated exactly as drafted. The CCI approval, while eventually granted, arrived too late for the agreement to proceed.

This case illustrates the importance of setting realistic long-stop dates that account for regulatory timelines — and of including extension provisions in the CP schedule where regulatory approval timelines are uncertain.

For further examples of how Conditions Precedent shape real cross-border manufacturing and joint venture transactions, see GTsetu’s coverage of the Renault–Geely Brazil automotive JV, the Foxconn–Al Rajhi EV JV in Saudi Arabia, and the Tramontina–Aequs India JV — each of which involved binding commitments conditional on regulatory, financing, and operational prerequisites.

Where Conditions Precedent Are Used

Where Conditions Precedent Appear in International Business

Conditions Precedent are among the most widely deployed contractual mechanisms in cross-border commerce. They enable parties to commit to the substance of a transaction in a binding instrument while protecting themselves from the obligation to perform until specified prerequisites are in place.

🏢

Mergers & Acquisitions

Share purchase and business acquisition agreements are almost always structured as conditional — typically on merger control clearance, shareholder approvals, satisfactory due diligence, and material adverse change provisions. The CP schedule is one of the most heavily negotiated components of any M&A transaction.

🏗️

Real Estate & Land Development

Conditional contracts for the purchase of development land are almost universally structured with a planning permission CP. The developer commits to purchase the land but is only obligated to complete if the required planning consent is granted within the condition period.

🌍

Cross-Border Supply & Distribution

A binding supply agreement may be made conditional on the supplier passing a specified quality audit, obtaining required import or export licences, or achieving accreditation from a nominated standards body. See GTsetu’s coverage of the CalCom Vision–Goldmedal partnership as an example of how manufacturing prerequisites structure cross-border commitments.

💰

Project Finance & Investment

Investment commitments in infrastructure, energy, and capital projects are structured as conditional on financial close — the point at which all funding commitments, security arrangements, and pre-conditions to drawdown have been confirmed by lenders and investors.

⚖️

Regulated Sector Transactions

Any transaction requiring government or regulatory approval — financial services, telecommunications, pharmaceutical manufacturing, defence, media — is structured as conditional on that approval being obtained within the condition period. Without a CP, parties would be obligated to perform even if approval is denied.

🤝

Joint Venture Formation

A binding JV agreement may be conditional on the parties securing specific third-party contracts, technology licences, or concession rights that form the economic rationale for the venture. Without those foundations, the JV entity need never be formed. See the Wheels India–Topy Industries collaboration for how technical prerequisites structure binding JV commitments.

CP vs Condition Subsequent

Condition Precedent vs Condition Subsequent: A Practical Comparison

The two principal types of conditions in commercial agreements — conditions precedent and conditions subsequent — operate in opposite directions and allocate risk in very different ways. Understanding the distinction is essential to drafting and interpreting any conditional commercial arrangement.

| Dimension |

Condition Precedent |

Condition Subsequent |

| Direction of Effect |

Must occur before the duty to perform arises — triggers the obligation |

Occurs after performance obligations are in force — terminates an existing obligation |

| Timing |

Operates at the outset; obligation to perform is suspended until condition is met |

Operates during or after performance; brings an ongoing obligation to an end |

| Commercial Use |

Dominant in transaction agreements: M&A, real estate, project finance, supply |

More common in ongoing arrangements: service contracts, employment, licensing |

| Burden of Proof |

Party seeking to enforce performance must typically show the CP has been satisfied |

Party seeking to use the condition to end an obligation typically bears the burden of proving it has occurred |

| Court Approach |

Courts prefer to interpret ambiguous clauses as promises rather than CPs to avoid forfeiture |

Courts construe conditions subsequent narrowly; ambiguity tends to preserve the obligation |

| Consequence of Failure |

Agreement typically terminates; neither party obligated to perform principal obligations |

The specific obligation discharged by the condition ceases; agreement may otherwise continue |

| Drafting Precision Required |

High — condition must be objectively verifiable and responsibility for pursuit clearly allocated |

Very high — courts construe narrowly; ambiguity will preserve the obligation |

✨ Drafting Note

Courts across major commercial jurisdictions — including England & Wales and the United States — prefer to interpret an ambiguous clause as a promise rather than a Condition Precedent, in order to avoid the forfeiture that results from a condition failing. This means that imprecise drafting is more likely to be construed against the drafter in a way that preserves the obligation rather than creating an exit route. If the intent is to create a true condition precedent — one whose failure terminates the obligation to perform — the drafting must be unambiguous.

Key Elements of a CP Clause

What Every Condition Precedent Clause Must Address

A well-drafted Condition Precedent clause does far more than name the event that must occur. It defines the condition with sufficient precision to be objectively verifiable, allocates the responsibility for pursuing satisfaction, and specifies the consequences if the condition is or is not met. These elements are essential.

✓

Objective, Measurable Definition

The condition must be defined with sufficient specificity that both parties — and a court — can determine objectively whether it has been satisfied. Subjective formulations (“satisfactory due diligence”) without defined criteria create disputes at the point of performance.

✓

Long-Stop Date

The outer deadline by which all conditions must be satisfied. If conditions are not met by this date, the agreement terminates automatically or at the election of one or both parties. The long-stop date must be realistic given the complexity and jurisdiction of the conditions.

✓

Responsibility Allocation

Clear statement of which party is responsible for pursuing satisfaction of each condition, what standard of effort is required (reasonable endeavours, best endeavours, or absolute obligation), and which party bears the associated costs.

✓

Notification Obligations

Each party’s obligation to notify the other of progress, obstacles, and — critically — if a condition becomes impossible to satisfy. Early notification allows parties to consider extensions, renegotiation, or structured exit before the long-stop date is reached.

✓

Extension Provisions

Provisions allowing the long-stop date to be extended — at the election of one or both parties — if conditions are close to satisfaction or if regulatory timelines have slipped for reasons outside the parties’ control. Extensions must be documented in writing.

✓

Waiver Rights

The right of the party in whose favour the condition operates to waive it and proceed to completion even if the condition has not been formally satisfied. Waiver must be in writing and explicit — oral waivers or conduct-based waivers create significant uncertainty.

✓

Conduct During the Condition Period

Obligations on both parties to maintain the status quo — prohibitions on material changes to the business, assets, or contracts that are the subject of the agreement. Without these, a party may restructure the underlying business during the CP period in ways that fundamentally alter the transaction.

✓

Consequences of Non-Satisfaction

What happens to deposits, costs, confidential information, and preparatory work if the agreement terminates due to CP failure. Provisions that survive termination — confidentiality under any NDA, governing law, dispute resolution — must be explicitly carved out.

Risks & Drafting Pitfalls

Common Risks and Drafting Pitfalls in CP Clauses

🚩

Vague or Subjective Condition Definitions

A condition defined in subjective terms — “satisfactory due diligence”, “acceptable regulatory outcome”, “reasonable financing terms” — without objective, measurable criteria creates a dispute at the point of performance. One party claims the condition is satisfied; the other disagrees. Courts will look to the drafting and construe ambiguity against the drafter. Every CP must be capable of objective verification.

🚩

Unrealistic Long-Stop Dates

The PayU–BillDesk transaction is a cautionary example: regulatory approval was obtained, but the long-stop date had already passed. Setting a long-stop date without modelling the realistic timeline for each CP — particularly regulatory approvals across multiple jurisdictions — creates pressure that may force premature termination of transactions that would otherwise complete. Build in buffer, and include extension provisions for conditions where timing is uncertain.

🚩

Wrongful Prevention of Condition Satisfaction

A party that deliberately or negligently prevents a Condition Precedent from being satisfied — by withdrawing cooperation from a regulatory filing, failing to provide required documents, or actively obstructing the process — may be held to have waived the condition or be liable for breach. The principle that a party cannot rely on a condition they themselves prevented from being fulfilled is recognised across major commercial jurisdictions and in common law systems including England & Wales, the United States, Singapore, and India.

🚩

Unclear Allocation of CP Pursuit Responsibility

Without clear allocation of which party is responsible for pursuing each CP, disputes arise during the condition period about who should be taking action, who bears the cost, and who is accountable if a condition fails. Each CP in the schedule should have a clearly identified responsible party, a defined standard of effort (reasonable endeavours vs best endeavours vs absolute obligation), and a costs allocation.

🚩

Confusing a CP with a Non-Binding Document

Conditions Precedent operate within fully binding contracts — not within MoUs, Letters of Intent, or Expressions of Interest that are intentionally non-binding on commercial terms. Parties — particularly those accustomed to markets where pre-contractual documents are commonly used — sometimes mischaracterise a Conditional Agreement as non-binding. Walking away from a binding Conditional Agreement, even before all CPs are satisfied, may constitute breach of interim obligations.

🚩

No Confidentiality Protection During the Condition Period

The CP period often involves the disclosure of sensitive commercial, financial, and technical information as part of due diligence and regulatory filings. Without a standalone NDA or explicit confidentiality provisions embedded in the Conditional Agreement — and without clear provisions confirming those obligations survive termination — that information is unprotected if the agreement terminates on CP failure.

Satisfying a Condition Precedent

The CP Lifecycle: From Execution to Unconditional Agreement

Once a Conditional Agreement is executed, the condition period begins. This phase requires active management — regular monitoring, clear communication between the parties, and prompt action when obstacles arise. The steps below represent the standard lifecycle through which a transaction moves from conditional commitment to unconditional obligation.

01

Execution and Commencement of the Condition Period

The Conditional Agreement is signed and the CP period begins. Both parties immediately become bound by their interim obligations — confidentiality, conduct restrictions, notification duties, and the obligation to pursue satisfaction of their respective CPs with the agreed standard of effort.

02

Active Pursuit of Condition Satisfaction

Each responsible party commences the activities required to satisfy their conditions — regulatory filings are submitted, due diligence programmes are conducted, financing processes are initiated, third-party consents are sought. The standard of effort required (reasonable or best endeavours) is defined in the agreement and must be maintained throughout.

03

Progress Monitoring and Notification

Both parties fulfil their notification obligations — updating each other on CP status, escalating obstacles promptly, and flagging developments that could affect condition satisfaction or the underlying commercial rationale. Early escalation allows parties to consider extensions, waivers, or structured renegotiation before the long-stop date is reached.

04

Conditions Satisfied or Waived

Each condition is either formally satisfied — regulatory approval received, due diligence complete, financing confirmed — or waived in writing by the party in whose favour it operates. Waiver must be express and documented. A written notice confirming satisfaction or waiver of each condition is best practice, and is often required by the agreement itself.

05

Agreement Becomes Unconditional

Once all conditions are satisfied or waived, the agreement becomes unconditional and the principal performance obligations — completion of the acquisition, transfer of assets, commencement of supply, activation of the joint venture — become immediately due. A formal written confirmation of unconditional status is best practice in all major cross-border transactions.

06

Completion of Principal Obligations

The transaction completes. All completion mechanics, post-completion obligations, and warranties should have been defined in the original agreement so that completion is procedurally straightforward once the agreement goes unconditional. The CP period is over; the commercial arrangement begins.

CP in Context — Transaction Document Sequence

Where Conditions Precedent Fit in the International Transaction Lifecycle

A Condition Precedent does not exist in isolation — it operates within a broader transaction document sequence. Understanding where CPs sit relative to the pre-contractual documents that typically precede a binding commitment is essential to managing risk at every stage.

| Document |

Binding Nature |

Role of Conditions |

Typical Stage |

| Expression of Interest (EoI) |

Non-binding commercially |

No formal CPs; preliminary interest only |

Earliest stage; market sounding |

| MoU / LOI |

Generally non-binding commercially; select clauses binding |

May identify anticipated CPs without creating binding obligations to satisfy them |

Early-to-mid; framework and intent |

| Term Sheet |

Generally non-binding commercially |

CPs may be outlined in commercial terms but not yet legally operative |

Mid; agreed commercial terms |

| Heads of Agreement |

Often non-binding commercially; can be structured as binding |

CPs may be listed as agreed principal terms; may or may not be legally operative |

Mid-to-late; pre-formal drafting |

| Conditional Agreement |

Fully binding from execution |

CPs are legally operative — failure to satisfy by long-stop date terminates agreement |

Post-negotiation; binding commitment |

| Unconditional Agreement |

Fully binding; all obligations immediately enforceable |

No conditions — all CPs have been satisfied or waived |

Final; completion mechanics apply |

✨ GTsetu Note on Good Faith

In cross-border transactions — particularly those involving parties from civil law jurisdictions where good faith negotiation is a statutory obligation — the conduct of both parties during the CP period is closely scrutinised. A party that negotiates a CP in bad faith, or that uses the CP mechanism as a tool for prolonging uncertainty while pursuing a better commercial outcome elsewhere, may face liability under good faith doctrines that operate independently of the contract’s governing law. This is a particular risk in transactions involving parties from France, Germany, the Netherlands, Spain, and other civil law systems where pre-contractual and in-contract good faith obligations are enforced.

FAQ

Frequently Asked Questions

Q

Is a contract with a Condition Precedent legally binding before the condition is satisfied?

Yes. A

Conditional Agreement containing a Condition Precedent is fully binding from the moment of execution. The binding nature of the agreement is not conditional — only the obligation to perform the principal commercial act (the purchase, the transfer, the supply) is suspended. Ancillary obligations — confidentiality, conduct during the condition period, notification duties, governing law, and dispute resolution — are immediately enforceable. A party cannot simply walk away from the agreement before the long-stop date without potentially breaching those interim obligations.

Q

What is the difference between reasonable endeavours and best endeavours in a CP clause?

The standard of effort required to pursue satisfaction of a Condition Precedent is one of the most commercially significant elements of any CP clause, and the precise formulation used carries significant legal weight — particularly in English law contracts. Reasonable endeavours requires a party to take the steps that a reasonable person would take in the same position, but allows the party to have regard to its own commercial interests. Best endeavours — the higher standard — requires a party to take all steps that a prudent, determined person, acting in their own interests and genuinely desiring the outcome, would take. In many CP clauses, the responsible party will push for reasonable endeavours; the imposing party will seek best endeavours or, for statutory CPs with a defined action required, an absolute obligation.

Q

Can a Condition Precedent be waived?

Yes — in most Conditional Agreements, the party in whose favour a CP operates has the right to waive it, electing to proceed to completion even if the condition has not been formally satisfied. This is common in M&A transactions where an acquirer may choose to proceed despite minor unresolved due diligence points, or in real estate transactions where a developer may proceed without the exact planning permission specified. Any waiver must be given in writing, must specify the condition being waived, and should confirm that the waiver does not affect any other provisions of the agreement. Courts will scrutinise waiver carefully; conduct-based or oral waivers create significant uncertainty and litigation risk.

Q

What happens if one party prevents a Condition Precedent from being satisfied?

If one party wrongfully prevents a Condition Precedent from being satisfied — by withdrawing cooperation from a regulatory filing, refusing to provide required documents, or actively obstructing the process — courts across most commercial jurisdictions will not allow that party to rely on the unsatisfied condition as a basis for terminating the agreement or avoiding their obligations. Courts may treat the condition as having been satisfied and hold that party liable for breach of contract. This principle is well established in English law, US law, and across most civil law systems. It is one of the most significant risks in CP drafting: a CP designed as a protective mechanism can become a source of liability if one party attempts to manipulate the outcome by controlling the conditions.

Q

How does a Condition Precedent differ from a warranty or a representation?

A Condition Precedent is a prerequisite that must be satisfied before performance obligations arise — it is about the future occurrence of events. A warranty is a statement of present or past fact given by one party to the other, breach of which gives rise to a claim for damages. A representation is a statement made to induce a party to enter the contract, the falsity of which may give rise to a right to rescind or claim damages. These are distinct legal mechanisms. In a typical M&A transaction, the agreement will include all three: Conditions Precedent (regulatory approval, due diligence), warranties (statements about the state of the target business), and representations (statements made during negotiations). Each operates differently and triggers different remedies on failure.