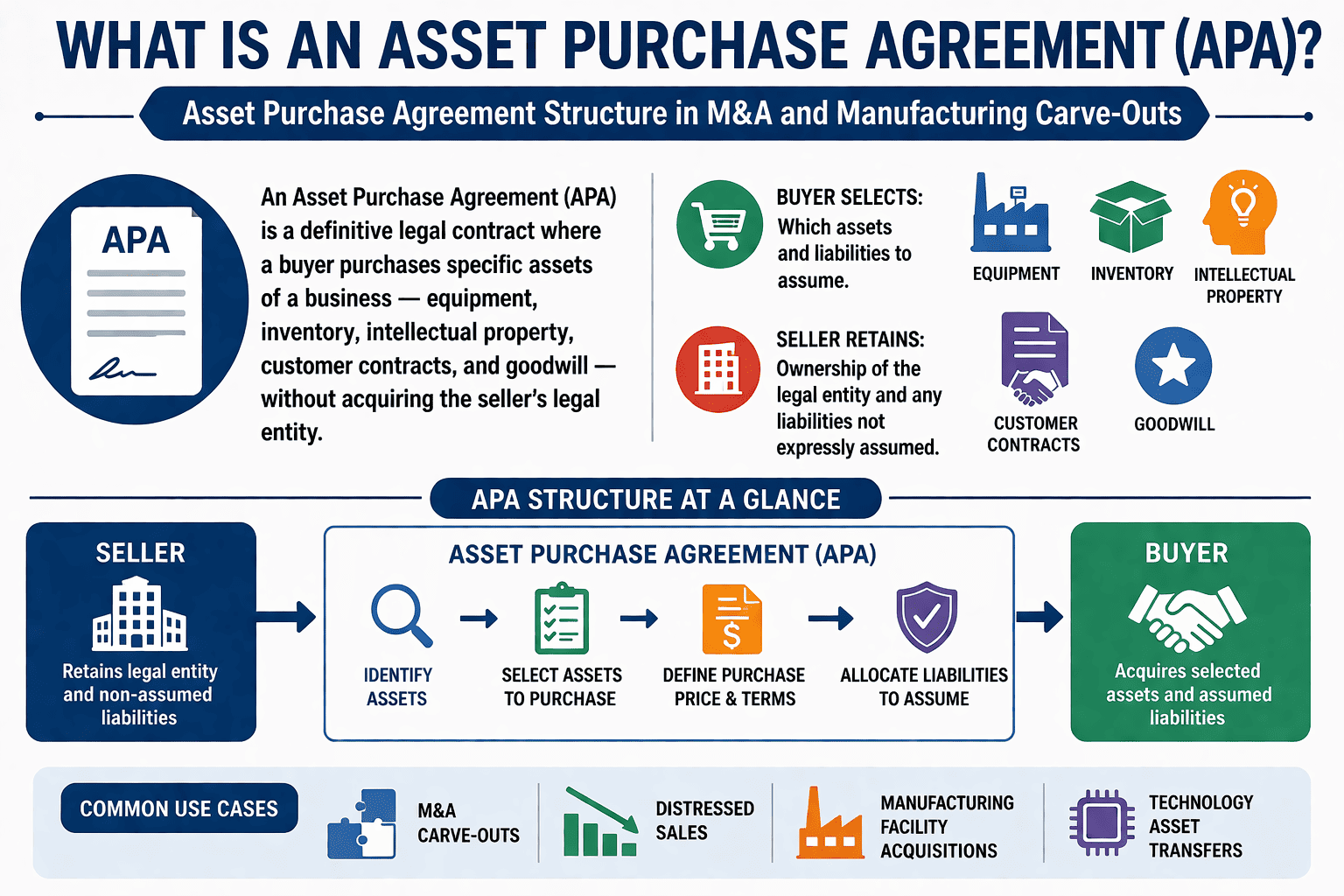

How an Asset Purchase Agreement Works

An Asset Purchase Agreement (APA) is the primary legal instrument for buying specific assets of a business rather than buying the business entity itself. Unlike a stock purchase where the buyer acquires the entire company, including all known and unknown liabilities, an APA allows the buyer to pick individual assets (equipment, inventory, IP, customer contracts, trade names) and assume only specifically listed liabilities. The seller retains the legal entity and any liabilities not explicitly assumed, such as pre-closing taxes, product liability from pre-closing sales, or employee benefit obligations.

In a typical APA transaction, the parties: (1) execute a non-binding Letter of Intent (LOI) outlining principal terms; (2) the buyer conducts due diligence on the specific assets; (3) the parties negotiate the APA defining purchased assets, excluded assets, assumed liabilities, and purchase price; (4) conditions precedent (regulatory approvals, third-party consents) are satisfied; (5) at closing, the buyer pays the purchase price and the seller transfers title via a bill of sale and ancillary documents. APAs are particularly useful in cross-border transactions where the buyer wants to isolate itself from the seller’s historical liabilities.

⚡ Critical Distinction

An APA is a Definitive Agreement, fully binding once executed. It is not a preliminary document like an LOI or MoU. The APA supersedes all prior agreements. Unlike a stock purchase, the buyer does not inherit the seller’s legal entity, only the identified assets and expressly assumed liabilities. This liability isolation is the primary reason buyers prefer APAs.

Assets vs Liabilities in an APA

What’s Included: Purchased Assets & Assumed Liabilities

📦 PURCHASED ASSETS (Typical)

Buyer selects specific assets

- Equipment, machinery, fixtures, computers

- Inventory (raw materials, WIP, finished goods)

- Intellectual property: patents, trademarks, trade names, software licences, URLs, phone numbers

- Customer contracts, supplier contracts, licences, permits

- Customer lists, supplier lists, goodwill, trade secrets

- Accounts receivable (if specified)

- Vehicles, tools, office equipment

- Exclusive right to use business name

⚠️ ASSUMED & EXCLUDED LIABILITIES

Buyer assumes only listed liabilities

- Assumed liabilities (typical): obligations under assigned contracts, product warranties for post-closing sales, liabilities explicitly listed in a schedule

- Excluded liabilities (seller retains): pre-closing taxes, product liability from pre-closing sales, employee benefit obligations, litigation arising from pre-closing conduct, environmental liabilities, debts not assumed, any liability not expressly assumed in the APA

- Third-party consents: Contracts requiring consent to assign – without consent, asset may be excluded or buyer may accept a sublease/ subcontract arrangement

✨ GTsetu Guidance

In cross-border asset deals, the schedule of purchased assets and excluded liabilities is heavily negotiated. GTsetu’s verified partner network helps buyers conduct initial commercial due diligence on manufacturing assets before entering APA negotiations. GTsetu verifies companies on 6 government-sourced points (Name, Address, Registration Number, Company Status, Company Type, Date of Incorporation). The platform’s collaboration tools allow secure sharing of asset lists, warranty information, and third-party consent documentation. Good faith negotiation during the asset definition phase is essential to avoid post-closing disputes.

APA vs Stock Purchase

Asset Purchase vs Stock Purchase: Key Differences

| Dimension | Asset Purchase Agreement (APA) | Stock Purchase Agreement (SPA) |

|---|

| What is acquired | Specific assets & liabilities (itemised) | Shares of target entity (entire company) |

| Liability assumption | Buyer assumes only listed liabilities; seller retains residual | Buyer inherits all liabilities (known and unknown) |

| Tax treatment | Buyer gets “step-up” in asset basis (depreciation benefits); seller may pay higher tax | Seller often gets capital gains treatment; no step-up for buyer |

| Third-party consents | Often required for contracts, leases, licences – consents may be costly or withheld | Generally not required (entity continues) |

| Transfer of permits/licences | Individual transfer or reapplication often required | Permits typically remain with entity |

| Employee treatment | Buyer can select which employees to hire; seller terminates others | Employees continue with entity |

| Preferred by | Buyers (liability isolation, asset selectivity) | Sellers (simplicity, tax efficiency) |

Key Clauses in an APA

Essential Clauses of an Asset Purchase Agreement

✓

Definitions & Asset Schedules

Precise definition of purchased assets, excluded assets, assumed liabilities, and retained liabilities – attached as numbered exhibits.

✓

Purchase Price & Payment Mechanics

Cash at closing, holdback/escrow amounts, earn-out provisions, working capital adjustment mechanisms, and allocation of purchase price under Code Section 1060 (Form 8594).

✓

Representations & Warranties

Seller’s reps: title to assets, financial statements, absence of liens, compliance with laws, litigation, contracts, intellectual property, employee matters. Buyer’s reps: authority, financing, etc.

✓

Covenants

Conduct of business before closing (ordinary course, no asset disposal), access to information, transition assistance, non-solicitation, non-compete (typically 2-5 years).

✓

Conditions Precedent (CPs)

Regulatory approvals (merger control, sector licences), third-party consents to assignment, accuracy of reps, performance of covenants, no material adverse change. See Condition Precedent guide.

✓

Indemnification

Survival periods (e.g., 12-36 months for general reps; up to statute of limitations for fundamental reps), caps (e.g., 10-30% of purchase price), baskets (deductibles), and exclusive remedy provisions.

✓

Non-Compete & Non-Solicitation

Seller agrees not to compete within a defined territory (e.g., 100-mile radius) for a defined period (2-5 years) and not to solicit customers or employees. See Non-Compete Clause.

✓

Closing Deliverables

Bill of sale, assignment and assumption agreement, non-foreign affidavit (FIRPTA), officer’s certificates, third-party consents, secretary’s certificate, legal opinions, UCC lien searches.

✓

Governing Law & Dispute Resolution

Choice of governing law (e.g., Delaware, New York, England), exclusive jurisdiction or arbitration (ICC, SIAC, LCIA). Essential for cross-border APAs.

Real-World Example

Asset Purchase Agreement in Practice: Distressed Manufacturing Acquisition

📌 Case Study, Carve-Out Transaction

In a typical distressed manufacturing asset purchase, a buyer acquires equipment, inventory, customer contracts, and IP from a seller in bankruptcy or financial distress. For example, an automotive parts manufacturer buys a competitor’s production line, tooling, and patents for $2.5 million. The APA excludes all pre-closing liabilities (environmental claims, product liability from pre-closing sales, employee severance). The buyer assumes only open purchase orders and warranties on post-closing production. Conditions precedent include competition authority clearance and assignment of key supply contracts. The non-compete restricts the seller from manufacturing competing components for 3 years within North America. This structure allows the buyer to expand capacity without inheriting legacy liabilities.

For further examples of asset-based transactions, see GTsetu’s coverage of manufacturing joint ventures and facility acquisitions.

Due Diligence for an APA

Due Diligence Checklist for Asset Purchase Transactions

✓

Title to Assets

UCC lien searches, title insurance, equipment leases, evidence of ownership, chain of title for IP.

✓

Third-Party Consents

Identify all contracts (customer, supplier, lease, licence) requiring consent to assignment. Material contracts without consent may be excluded.

✓

Intellectual Property

Ownership, registered IP (patents, trademarks), software licences, trade secrets, open source compliance, IP litigation history.

✓

Environmental & Regulatory

Phase I/II environmental reports, permits, compliance records, pending violations, environmental liens on assets.

✓

Employee & Benefit Matters

WARN Act compliance, employee transfer elections, pension liabilities (excluded), accrued PTO, collective bargaining agreements.

✓

Litigation & Product Liability

Pending or threatened claims, product recall history, liability for pre-closing sales (excluded).

✨ GTsetu Note on Cross-Board APAs

For cross-border asset purchases, due diligence must include export/import licences, sanctioned party checks, and compliance with local asset transfer rules. GTsetu’s business verification layer confirms the counterparty’s legal existence (Name, Address, Registration Number, Company Status, Company Type, Date of Incorporation using government tie-ups) before entering an APA negotiation, reducing the risk of dealing with shell entities. The platform’s secure document exchange supports due diligence data rooms with version control and audit trails – see NDA guide for protecting shared information.

Conditions Precedent in APAs

Conditions Precedent to Closing in an APA

Like Conditional Agreements, APAs typically include conditions precedent that must be satisfied before the buyer is obligated to close. Common CPs in asset purchase agreements: (1) antitrust/competition clearance; (2) third-party consents for material contracts; (3) accuracy of representations and warranties; (4) performance of covenants; (5) no material adverse change in the assets; (6) delivery of closing documents (bill of sale, assignments); (7) financing condition (if buyer’s commitment is a CP). If CPs are not satisfied or waived by the long-stop date, the APA terminates and the parties are released from the principal obligations (though confidentiality and break-fee provisions survive). The allocation of risk for obtaining consents must be clearly assigned.

Common Risks & Pitfalls

Common Risks and Drafting Pitfalls in Asset Purchase Agreements

🚩

Vague Asset Description

“All equipment used in the business” without an itemised schedule leads to post-closing disputes about what is included. Always attach detailed exhibits.

🚩

Undefined Excluded Liabilities

Failure to explicitly list excluded liabilities (pre-closing taxes, product claims) may result in buyer inadvertently assuming them under general assumption language.

🚩

Third-Party Consents Not Obtained

Material contracts (e.g., key supplier agreement) that require consent but cannot be assigned. Solution: include condition precedent or a “subcontract” arrangement with seller.

🚩

Overbroad Non-Compete

A 5-year worldwide non-compete on a small regional seller may be unenforceable. Geographic and duration limits must be reasonable.

🚩

Inadequate Indemnification Caps & Survival

A short survival period (e.g., 6 months) for reps leaves buyer without recourse if breach discovered later. Negotiate 18-36 months for general reps.

🚩

No Allocation of Purchase Price

Failing to agree on asset allocation (Form 8594) can cause tax disputes and impair buyer’s depreciation deductions.

APA in Transaction Sequence

Where an APA Fits in the Transaction Document Sequence

DocumentBinding NatureRole in Asset DealStage

Expression of Interest (EoI)Non-binding commercialIndicates preliminary interest in specific assetsEarliest market sounding

LOI / Heads of AgreementGenerally non-binding on price/terms; confidentiality & exclusivity bindingSets out asset scope, purchase price range, exclusivity period, due diligence accessPre-due diligence

Term SheetNon-binding commerciallyOutlines key APA terms: assets, liabilities, payment, CPsMid-stage alignment

NDABindingProtects confidential information during due diligenceExecuted before any asset-level disclosure

Asset Purchase Agreement (APA)Fully binding definitive agreementFinal contract for asset transfer; supersedes all priorPost-diligence; signing

Closing (Bill of Sale, Assignments)Transfer of titleAssets legally transferred to buyer; purchase price paidFinal

✨ GTsetu Platform Advantage

GTsetu’s Commercial Framework Agreement and partner verification tools streamline the pre-APA phase. GTsetu verifies companies on 6 government-sourced points (Name, Address, Registration Number, Company Status, Company Type, Date of Incorporation). Companies on the platform share asset lists, insurance certificates, and lien information within a controlled environment. This reduces due diligence time and helps structure the asset schedule efficiently. Start your asset acquisition journey with GTsetu’s verified manufacturing and industrial partners.

FAQ

Frequently Asked Questions

QWhat is the difference between an Asset Purchase Agreement and a Stock Purchase Agreement?

In an Asset Purchase Agreement (APA), the buyer purchases specific assets and assumes only explicitly listed liabilities. The seller retains the legal entity and residual liabilities. In a Stock Purchase Agreement (SPA), the buyer purchases the shares of the target company, acquiring the entire entity, all assets, all liabilities (known and unknown), contracts, and permits. APAs are generally preferred by buyers for liability isolation; SPAs are often preferred by sellers for tax efficiency and simplicity of transfer. The choice affects tax treatment (buyer gets stepped-up basis in an APA), third-party consent requirements, and post-closing exposure.

QWhat liabilities does the buyer typically assume in an APA?

The buyer assumes only liabilities that are explicitly listed in the “Assumed Liabilities” section of the APA. Typical assumed liabilities include: obligations under assigned contracts (post-closing performance), product warranties for goods sold after closing, liabilities for current assets (e.g., accounts payable for inventory purchased), and other expressly agreed obligations. The seller retains all other liabilities: pre-closing taxes, product liability claims arising from pre-closing sales, employee benefit obligations, environmental liabilities, litigation arising from pre-closing conduct, and any debt or obligation not expressly assumed. This liability isolation is the primary reason buyers prefer APAs over stock purchases.

QWhat are conditions precedent in an Asset Purchase Agreement?

Conditions precedent (CPs) are events that must occur before the buyer is obligated to close the asset purchase. Common CPs in APAs: (1) regulatory approvals (competition clearance, sector licences); (2) third-party consents for material contracts being assigned; (3) accuracy of seller’s representations and warranties; (4) performance of covenants (e.g., ordinary course conduct); (5) no material adverse change in the assets; (6) delivery of closing documents (bill of sale, assignments). If CPs are not satisfied or waived by the long-stop date, the buyer can terminate without liability. See GTsetu’s

Condition Precedent guide for drafting details.

QCan an Asset Purchase Agreement include only intangible assets?

Yes. An APA can be structured to purchase only intangible assets, intellectual property (patents, trademarks, software code), customer lists, goodwill, licences, and supplier relationships, without any physical equipment or inventory. This is common in technology acquisitions, IP licensing deals, brand divestitures, and software asset transfers. The same APA structure applies: a defined list of purchased intangible assets, excluded liabilities, representations on IP ownership and non-infringement, and indemnification for third-party IP claims.

QHow long does an APA process take from LOI to closing?

The timeline varies significantly. Smaller asset deals (e.g., purchase of a single production line) may close in 30-60 days. Larger or more complex transactions (e.g., acquiring a manufacturing division with multi-jurisdiction assets) can take 3-6 months or more. Factors affecting timeline: complexity of title search (UCC liens), number of third-party consents required, regulatory approval timelines (e.g., competition clearance), due diligence issues, and financing conditions. Most APAs include a long-stop date (e.g., 120 days after signing) to create deadline discipline.