Free for a limited time·Profile verification free·First collaboration free·500+ Companies Onboarded·6 Continents Covered·No Commission & No Profit Share·Free for a limited time·Profile verification free·First collaboration free·500+ Companies Onboarded·6 Continents Covered·No Commission & No Profit Share·Free for a limited time·Profile verification free·First collaboration free·500+ Companies Onboarded·6 Continents Covered·No Commission & No Profit Share·

Advance Payment vs LC vs Open Account: Complete B2B Trade Payment Guide | GTsetu

Home ›

Blog ›

Advance Payment vs LC vs Open Account

💳 Trade Finance & Payments

Advance Payment vs LC vs Open Account: Complete B2B International Trade Payment Guide

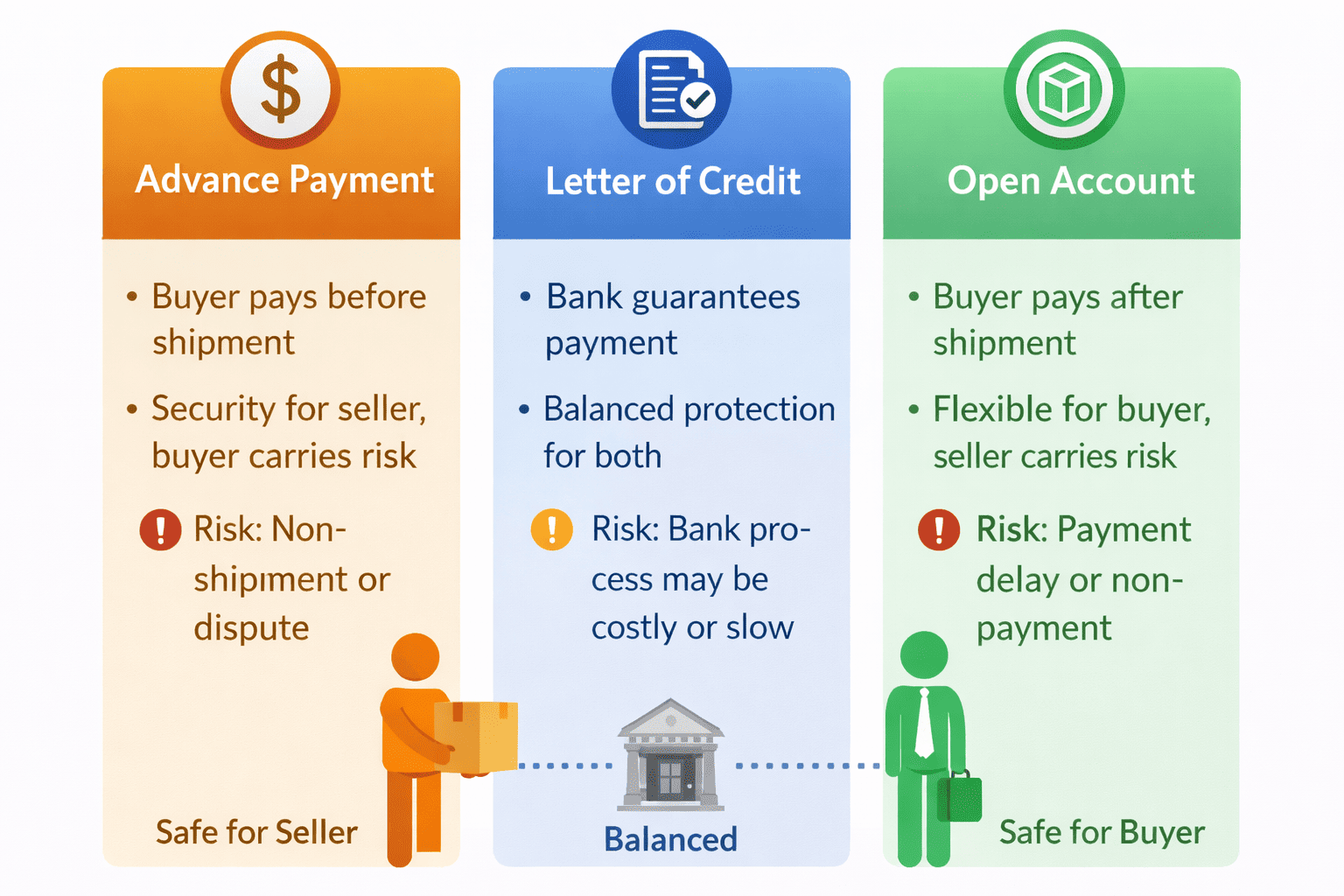

Direct Answer: In international trade, there are five main payment methods ranked by exporter security, from safest to riskiest: Advance Payment (Cash in Advance) where the buyer pays before shipment; Letter of Credit (LC) where a bank guarantees payment against compliant documents; Documentary Collection (CAD/DP and DA) where banks facilitate document exchange but don’t guarantee payment; Open Account where the buyer pays after receiving goods; and Consignment where the exporter only gets paid after the buyer sells to end customers. For manufacturers expanding into new markets, choosing the right payment method is as critical as finding the right trade partner, and GTsetu connects you with government-verified companies across 100+ countries, giving you basic verification of company credentials before you negotiate payment terms.

📅 March 7, 2026⏱ 20 min read✍️ GTsetu Editorial Team🔄 Updated regularly

6

Payment Methods Decoded

100+

Countries on GTsetu

500+

Verified Partners

0%

Broker Commission

Closing a manufacturing or distribution deal with an international partner is only half the battle. The other half, often underestimated, is deciding how payment will be structured. For a manufacturer shipping goods worth $200,000 to a new distributor in a foreign country, the difference between requiring advance payment versus offering open account terms can mean the difference between a profitable relationship and an unrecoverable loss.

This guide unpacks every major international trade payment method in full, from the safest (advance payment) to the riskiest (consignment), with step-by-step process flows, comparison tables, cost breakdowns, and a practical decision framework to help manufacturers, exporters, importers, and distributors choose the right method for every trade relationship.

1 All Payment Methods at a Glance, The Risk Spectrum

Before diving into each method, here is the most important concept in international trade payment terms: the risk spectrum. Every payment method sits on a spectrum between maximum security for the exporter and maximum benefit for the importer. As you move from advance payment toward open account, the exporter takes on progressively more risk, and the importer gains progressively more working capital advantage.

Buyer pays 100% (or partial) before goods are shipped. Exporter ships only after receiving funds.

🟢 Lowest Risk (Exporter)

LC

Letter of Credit

Bank guarantees payment to exporter once compliant shipping documents are presented.

🟡 Balanced Risk

CAD/DP

Cash Against Documents / Doc. Against Payment

Banks handle document exchange. Buyer pays at sight to get shipping documents released.

🟠 Moderate Risk

DA

Documents Against Acceptance

Buyer accepts a time draft (promise to pay) and bank releases documents before payment is made.

🟠 Higher Moderate Risk

OA

Open Account

Exporter ships goods; buyer pays after agreed credit period (30/60/90 days). No bank intermediary.

🔴 High Risk (Exporter)

CSG

Consignment

Exporter ships goods; distributor pays only after selling to end customers. Exporter retains title until sold.

🟣 Highest Risk (Exporter)

📌 The Fundamental Trade-Off

Every payment method negotiation is a risk transfer exercise. The more security the exporter demands (advance payment), the more the importer bears risk. The more credit the exporter extends (open account), the more the exporter bears risk. The right method depends on relationship maturity, transaction value, country risk, and working capital positions of both parties. Verified B2B platforms like GTsetu reduce relationship risk by providing government-linked company verification, making more flexible payment terms viable sooner.

SECTION 2

2 Advance Payment (Cash in Advance)

🎯 Definition

Advance Payment (also called Cash in Advance or CIA) is the payment method where the importer pays the full or partial amount to the exporter before goods are shipped or manufactured. The exporter only initiates production or shipment after confirming receipt of funds. This is the safest method for the exporter, zero non-payment risk, and the riskiest for the importer, who relies entirely on the exporter’s integrity to deliver as promised.

How Advance Payment Works, Step by Step

1

Terms Agreed

Exporter and importer agree on product specifications, pricing, and the requirement for full or partial advance payment before shipment.

2

Payment Transferred

Importer sends payment via wire transfer (TT), SWIFT, or another agreed payment channel to the exporter’s bank account. Common advance structures: 30% upfront + 70% before shipment, or 100% in advance.

3

Exporter Confirms Receipt & Ships

Once payment is confirmed, the exporter manufactures (if not pre-made) and ships goods, then provides shipping documents to the importer for customs clearance.

4

Importer Receives Goods

Importer clears customs and takes delivery. No further payment obligation, transaction complete.

Advance Payment: Pros and Cons

✅ Advantages

✅ Zero non-payment risk for the exporter

✅ Positive cash flow, funds received before production costs

✅ No need for trade finance or invoice discounting

✅ No collection costs, bank fees, or LC charges

✅ Simple to administer, no complex documentation

✅ Best for unknown buyers or high-risk countries

⚡ Disadvantages

⚡ Deters many buyers, especially new or cautious importers

⚡ Importer bears full risk if exporter fails to deliver

⚡ Ties up importer’s working capital before goods arrive

⚡ Can make the exporter uncompetitive vs. rivals offering credit

⚡ May not be viable for large-value orders

⚡ Currency risk between payment and delivery dates

100%

non-payment risk elimination for the exporter with full advance payment

30/70

most common split: 30% advance at order, 70% before shipping, a compromise both sides accept

T/T

Telegraphic Transfer (wire transfer) is the dominant advance payment mechanism in global B2B trade

Best for

New relationships, small-value orders, high-risk countries, custom/bespoke manufactured goods

SECTION 3

3 Letter of Credit (LC), Types, Process & When to Use

🎯 Definition

A Letter of Credit (LC) is a binding financial instrument issued by the importer’s bank (the issuing bank), guaranteeing payment to the exporter, provided the exporter presents a compliant set of shipping documents within the stipulated time and in accordance with the LC’s stated conditions. The LC balances risk between both parties: the exporter is protected by the bank’s payment guarantee; the importer is protected by the fact that payment is conditional on proof of correct shipment. It is the most widely used payment instrument in international trade for medium-to-large transactions.

How a Letter of Credit Works, The Full Process Flow

1

Sales Contract Agreed

Exporter and importer agree on the trade terms, including that payment will be made by LC. The LC’s conditions (documents required, shipment deadline, port specifications) are negotiated at this stage.

2

Importer Applies for LC

The importer (applicant) submits an LC application to their bank (the issuing bank), providing the agreed terms. The bank issues the LC, which is a commitment to pay the exporter subject to compliant document presentation.

3

LC Transmitted to Exporter’s Bank

The issuing bank sends the LC (usually via SWIFT) to the exporter’s bank (the advising bank or confirming bank). The advising bank notifies the exporter of the LC’s existence and terms.

4

Exporter Ships Goods & Collects Documents

The exporter manufactures and ships the goods, collecting the required documents: Bill of Lading, Commercial Invoice, Packing List, Certificate of Origin, Insurance Certificate, and any other LC-specified documents. These must match the LC terms exactly, even minor discrepancies can delay payment.

5

Documents Presented to Advising Bank

The exporter submits the documents to their bank within the LC’s presentation period. The bank examines the documents for compliance with the LC terms.

6

Documents Forwarded; Payment Released

If documents are compliant, the advising bank forwards them to the issuing bank. The issuing bank releases payment to the exporter (at sight or on the agreed future date for a usance/deferred LC). The importer receives documents to claim goods.

Types of Letters of Credit

01

Sight LC (Payment at Sight)

Payment is made immediately (within a few banking days) once compliant documents are presented. The most common type for standard export transactions.

📍 Most common for manufacturing & distribution deals

02

Usance / Deferred LC

Payment is made on a future date (e.g., 30, 60, 90 days after document presentation). Gives the importer time to sell goods before paying, in effect, a credit facility backed by an LC.

📍 Common in FMCG, food, and consumer goods trade

03

Confirmed LC

The exporter’s own bank adds its own guarantee (confirmation) to the LC, protecting the exporter even if the issuing bank or importer’s country faces difficulties. Costs more but is stronger protection.

📍 Used when issuing bank or country risk is elevated

04

Irrevocable LC

Cannot be amended or cancelled without agreement from all parties, the standard in modern trade. Revocable LCs (which can be cancelled unilaterally by the issuing bank) are now rarely issued.

📍 Standard form, always request irrevocable LC

05

Standby LC (SBLC)

Operates like a performance guarantee, only drawn upon if the applicant (importer) fails to fulfil their payment or contractual obligation. Often used to support open account relationships.

📍 Used to back open account trade with larger buyers

06

Revolving LC

Automatically reinstates for repeat shipments under the same credit amount without requiring a new LC each time. Efficient for regular, high-volume trading relationships.

📍 Ideal for recurring manufacturing supply agreements

Confirms country of manufacture, used for duty/tariff purposes

Chamber of Commerce / customs authority

🟠 Often required

Insurance Certificate

Proof that shipment is insured (typically CIF terms)

Insurer

🟠 Required for CIF shipments

Inspection Certificate

Third-party confirmation that goods meet specification

Inspection agency (SGS, Bureau Veritas etc.)

🟡 Specified in LC if required

Phytosanitary / Health Certificate

Regulatory compliance for food, agricultural, or pharmaceutical products

Government authority

🟡 Required for regulated products

⚠️ The Discrepancy Problem

Studies suggest that up to 70% of first presentations under LCs contain discrepancies, errors or mismatches between the documents and the LC terms. Even a typo in the product description, a port name abbreviation, or a date inconsistency can trigger payment delays or refusals. Exporters must review LC terms meticulously before shipping and ensure all documents match exactly. Working with an experienced freight forwarder or trade finance bank significantly reduces discrepancy rates.

✅ Importer assured goods shipped per specification

✅ International standard, widely understood across banks

✅ LC can be discounted (early payment by exporter’s bank)

✅ Enables trade with unknown or new buyers at scale

✅ Country risk mitigated (especially with confirmed LC)

⚡ Disadvantages of LC

⚡ Expensive, bank charges for both parties (typically 0.5–2%)

⚡ Complex documentation, high discrepancy risk

⚡ Time-consuming to open, amend, and present under

⚡ Ties up importer’s bank credit line

⚡ Protects against payment default, not fraud

⚡ Not suitable for very small or very frequent transactions

SECTION 4

4 Documentary Collection: CAD, DP & DA Explained

🎯 Definition

Documentary Collection is a payment method where both parties use their respective banks to manage the exchange of shipping documents for payment, but crucially, the banks do not guarantee payment. The exporter’s bank (remitting bank) sends shipping documents to the importer’s bank (collecting bank), which releases them to the importer only upon payment (CAD/DP) or upon acceptance of a time draft (DA). It sits between LC and Open Account on the risk spectrum, more bank involvement than open account, but without the bank guarantee of an LC.

CAD / DP vs DA: The Two Types of Documentary Collection

Dimension

CAD / D/P (Documents against Payment)

DA (Documents against Acceptance)

Also known as

Cash Against Documents (CAD), Sight Draft, D/P

Documents Against Acceptance, Time Draft, D/A

When does payment occur?

At sight, importer pays immediately to get documents

After a future date, importer accepts draft; pays later (30/60/90 days)

When are documents released?

Only after payment is made to the collecting bank

Once importer signs (accepts) the time draft

Can importer receive goods before paying?

No, documents needed to clear customs

Yes, has documents; only promised to pay

Risk to exporter

Medium, importer may refuse documents; goods stranded

High, importer has goods and documents before paying

Bank’s role

Collect payment before releasing docs

Collect acceptance; release docs; chase payment at maturity

Exporter’s protection if non-payment?

Retains goods control (goods still in transit/port)

Very limited, can only sue; goods already with importer

Typical use case

Semi-trusted relationships; when exporter wants payment assurance

Established relationships where importer needs credit period

Documentary Collection Process Flow

🔄 Documentary Collection, How It Works

Exporter ships goods & collects docs

Step 1

Exporter submits docs to Remitting Bank

Step 2

Remitting Bank sends to Collecting Bank

Step 3

Importer pays (DP) or accepts draft (DA)

Step 4

Collecting Bank releases docs & remits funds

Step 5

Importer clears goods; exporter receives payment

Step 6

✨ GTsetu Insight

Many exporters on GTsetu start new distributor relationships with CAD/DP terms after verifying the partner’s company registration on the platform, a practical middle ground between demanding 100% advance payment (which may deter good buyers) and extending open account credit (which exposes the exporter). Once a track record is established over 2–3 shipments, terms can be graduated to DA or even open account. Find government-verified distribution partners on GTsetu →

SECTION 5

5 Open Account: How It Works, Risks & When to Use

🎯 Definition

In an Open Account arrangement, the exporter ships goods to the importer and extends credit, the importer pays after an agreed period (typically Net 30, Net 60, or Net 90 days). There is no bank intermediary, no document exchange mechanism, and no payment guarantee. The exporter ships entirely on trust. Open account is the most beneficial arrangement for the importer (maximises their working capital) and the riskiest for the exporter. Despite the risk, open account is the dominant payment method in established trading relationships globally, it is the norm in intra-EU trade, US domestic trade, and long-standing B2B supply chains.

Open Account Payment Timeline

📋

Day 0, Order Placed

Importer issues a purchase order. Exporter accepts and begins production or allocates inventory.

🚢

Day 15–30, Shipment

Exporter ships goods and issues commercial invoice. Shipping documents sent directly to importer, no bank involvement.

📦

Day 30–45, Delivery

Importer receives, inspects, and accepts goods. Invoice payment clock starts on agreed terms (invoice date or delivery date).

💳

Day 60–120, Payment

Importer remits payment on due date (Net 30/60/90 from invoice). Exporter has carried full credit risk throughout this period.

Open Account: Risk Mitigation Strategies

Exporting on open account without mitigation is high risk. The following instruments can reduce, though never eliminate, that risk:

01

Export Credit Insurance

Insures the exporter against non-payment by the buyer due to insolvency or protracted default. Providers include ECGC (India), Euler Hermes, Atradius, COFACE. Typically covers 80–95% of invoice value.

📍 ECGC covers Indian exporters; Euler Hermes covers global trade

02

Factoring / Invoice Discounting

The exporter sells the open account receivable to a factor (finance company) at a discount, receiving immediate cash. The factor then collects from the importer. Improves cash flow while transferring collection risk.

📍 Common in FMCG, apparel, and electronics supply chains

03

Standby Letter of Credit (SBLC)

Importer’s bank issues an SBLC as backstop security. If the importer fails to pay on the open account, the exporter can draw on the SBLC. Combines the flexibility of open account with bank-backed protection.

📍 Used by large exporters with established buyer relationships

04

Verified Partner Discovery (GTsetu)

The most cost-effective risk mitigation: only extend open account terms to government-verified partners. GTsetu’s verification checks six key company details: Name, Address, Registration Number, Status, Type, and Date of Incorporation, giving you confidence that the company exists as a registered legal entity before you ship on credit.

📍 Government-verified partners on GTsetu → safer open account decisions

✅ Advantages of Open Account

✅ Most attractive terms for buyers, maximises competitiveness

✅ Simple to administer, no bank documentation

✅ No bank fees or LC charges for either party

✅ Builds long-term buyer relationships

✅ Standard in established, trusted B2B supply chains

✅ Importer can inspect goods before payment obligation

⚡ Disadvantages of Open Account

⚡ Full non-payment risk sits with the exporter

⚡ Significant working capital strain on exporter

⚡ No bank mechanism to enforce payment

⚡ Cross-border debt recovery is slow and costly

⚡ Currency fluctuation risk over credit period

⚡ Only viable for known, trusted, verified buyers

SECTION 6

6 Consignment Payment Method

🎯 Definition

Consignment is a variation of open account in which the exporter ships goods to a foreign distributor but retains ownership until the goods are sold to end customers. The distributor pays the exporter only after selling the goods, making this the riskiest payment method for exporters. The exporter bears both the goods risk (unsold stock) and payment risk (dependent on distributor’s sales performance) simultaneously. Consignment is typically only viable with highly trusted, government-verified, established distributors, and with appropriate insurance and legal agreements in place.

🚨 Consignment Risk Warning

Consignment should only be considered with government-verified distributors with a proven sales track record. Without proper consignment agreements, insurance, and inventory visibility, an exporter can lose both goods and payment simultaneously. GTsetu’s government-tied verification helps manufacturers identify legitimate registered companies for consignment discussions, but always conduct additional due diligence before consigning inventory.

✅ When Consignment Makes Sense

✅ Entering a new market where buyers need to “try before they commit”

✅ Working with a highly trusted, long-standing distributor

✅ Products where sell-through speed is highly predictable

✅ When the exporter has strong legal agreements and inventory visibility

✅ Commodities traded on established international exchanges

⚡ Consignment Risks

⚡ No payment until end-customer sale, cash flow severely delayed

⚡ Goods at risk of damage, loss, or theft at distributor’s premises

⚡ Distributor insolvency means goods and payment both at risk

⚡ No control over distributor’s sales effort or pricing

⚡ Complex legal arrangements needed to protect ownership title

⚡ Insurance costs can be significant

SECTION 7

7 Full Side-by-Side Comparison, All Payment Methods

The definitive comparison table. Use this as a reference when evaluating which payment method to use for a specific trade relationship, transaction value, or market entry scenario.

Factor

Advance Payment

Letter of Credit (LC)

CAD / D/P

DA (Acceptance)

Open Account

Consignment

Exporter risk level

🟢 None

🟡 Very Low

🟠 Low–Medium

🟠 Medium

🔴 High

🟣 Highest

Importer risk level

🟣 Highest

🟡 Low

🟠 Medium

🟢 Low

🟢 None

🟢 None

When does exporter get paid?

Before shipment

On document presentation (or agreed future date)

When importer pays at sight

At maturity of time draft

30–90 days after shipment

After end-customer sale

Bank guarantee of payment?

N/A (already paid)

✅ Yes, issuing bank guarantees

❌ No, banks facilitate only

❌ No, banks facilitate only

❌ No

❌ No

Bank involvement

Minimal (wire transfer only)

High (issuing + advising + confirming banks)

Medium (remitting + collecting banks)

Medium (remitting + collecting banks)

None

None

Cost to exporter

Very low

Medium–High (LC fees, discrepancy charges)

Low (collection charges)

Low (collection charges)

Low (no bank fees; but credit risk cost)

Medium (insurance, legal setup)

Complexity of administration

Very simple

High (strict document compliance)

Medium

Medium

Simple

Complex (legal, inventory tracking)

Impact on exporter cash flow

🟢 Excellent (cash before production)

🟡 Good (on presentation)

🟡 Good (on shipping)

🟠 Moderate (deferred)

🔴 Strain (30–90 day gap)

🟣 Worst (unpredictable timing)

Impact on importer working capital

🟣 Most strain (pay before goods)

🔴 Significant (bank line tied up)

🟠 Moderate (pay on arrival)

🟡 Good (pay on credit period)

🟢 Best (pay after receiving goods)

🟢 Excellent (pay after selling)

Suitable relationship stage

New, untrusted, high-risk

New to established, medium trust

Developing relationship

Established relationship

Long-standing, verified trust

Highly trusted, long-term only

Recommended transaction value

Any, especially small/custom

Medium to large ($10K+)

Small to medium

Small to medium

Any with trusted buyer

Low to medium (control is easier)

Common industries

Custom manufacturing, machinery, new B2B relationships

Commodities, capital goods, cross-border B2B

Consumer goods, moderate volume trade

Established supply chain partners

Intra-group, long-term supply chain

Retail, fashion, perishables

SECTION 8

8 Advance Payment vs Letter of Credit: Key Differences

The most common decision for manufacturers and exporters entering new international markets is choosing between requiring full advance payment and accepting an LC. This section breaks down the key decision factors.

Decision FactorAdvance PaymentLetter of Credit

Payment security for exporter

✓ Maximum, paid upfront

✓ High, bank-guaranteed

Risk to importer

✗ Maximum, no goods guarantee

~ Low, payment conditional on shipment proof

Bank involvement / cost

✓ None, just a wire transfer

✗ High, issuing, advising, confirming bank fees (0.5–2%+)

Willingness of new buyers to accept

✗ Low, requires complete trust in exporter

✓ High, buyer is protected by bank conditions

Administrative complexity

✓ Very simple, instruct bank to receive

✗ Complex, precise document compliance required

Exporter cash flow timing

✓ Before production, maximum benefit

~ On document presentation, good

Suitable for large orders?

✗ Difficult, importer hesitant to pay large advance

✓ Yes, standard for large cross-border transactions

Country risk protection

✓ Full, already received

~ Good with confirmed LC; issuing bank risk remains with standard LC

💡 Practical Recommendation

For first orders with new international buyers, a common compromise is to require 30–50% advance payment with the balance secured by an LC or CAD/DP. This reduces the importer’s risk (they haven’t paid 100% upfront) while protecting the exporter against non-payment on the balance. As the relationship matures through collaborative supplier platforms, terms can be graduated toward open account.

SECTION 9

9 LC vs Open Account: Which to Choose?

The LC vs Open Account decision is fundamentally a question of relationship maturity and risk appetite. Most international supply chain relationships begin with LC and graduate toward open account as trust and track record are established.

Scenario

Recommended Method

Why

First order with unknown overseas buyer

Advance Payment or LC

No established trust; need payment security before shipping

Second or third order, relationship developing

LC or CAD/DP

Some track record; LC provides security while offering buyer protection

Established relationship (1–2 years, consistent payments)

DA or Open Account (30 days)

Proven reliability; cost of LC no longer justified

Long-standing relationship (3+ years, verified creditworthy buyer)

Open Account (60–90 days)

Full trust established; open account maximises buyer’s working capital efficiency

High-value order to known buyer in high-risk country

Confirmed LC

Buyer trust may be fine; country or issuing bank risk needs bank confirmation

Repeat supply to intra-group entity or subsidiary

Open Account

Same corporate group, no meaningful counterparty risk

Verify company registration first; start with secure payment; graduate terms as trust builds

SECTION 10

10 Which Payment Method Is Right for Your Trade?

🧭 Payment Method Decision Guide

First order with a brand-new buyer in a new country…

→ Require Advance Payment

Cash in Advance

Zero non-payment risk. Use GTsetu government verification to confirm the buyer’s company exists before negotiating.

New buyer wants to place a large order but you don’t know them…

→ Request an Irrevocable LC

Letter of Credit

Bank guarantee protects you; buyer is also protected by shipment-conditional payment. Standard for $25K+ orders.

Developing relationship, 2–3 orders, good track record…

→ Use CAD / DP Terms

Documentary Collection

Banks facilitate; buyer pays at sight for documents. Lower cost than LC; retains some protection.

Established buyer needs credit period to manage cash flow…

→ Offer DA or Open Account (30 days)

DA / Open Account

Reward trusted buyers with credit terms. Consider credit insurance to manage residual risk.

Long-term, high-volume buyer with impeccable payment history…

→ Open Account (60–90 days)

Open Account

Maximum flexibility for your best buyers. Back with export credit insurance or SBLC if amounts are large.

Not sure if your new trade partner is a legitimate registered company?

→ Verify First on GTsetu

GTsetu Platform

Six-point government-tied verification: Name, Address, Registration Number, Company Status, Company Type, Date of Incorporation. Confirms the company exists as a registered legal entity.

SECTION 11

11 How to Reduce Payment Risk in International Trade

Selecting the right payment method is only the first layer of risk management. The following practical strategies reduce credit and payment risk across all trade payment methods.

1

Verify Your Trade Partner Before Any Commitment

The most cost-effective risk reduction is preventing bad partnerships from starting. Use government-tied business verification to check company registration status and basic credentials before discussing payment terms. GTsetu’s six-point verification (Name, Address, Registration Number, Status, Type, Date of Incorporation) confirms the company exists as a registered legal entity across 100+ countries.

2

Use a Written Contract with Governing Law Clause

A properly drafted trade contract specifying governing law, dispute resolution mechanism (arbitration preferred over litigation for international disputes), and payment consequences is essential. The International Chamber of Commerce (ICC) arbitration is the globally accepted standard. Combine this with secure B2B collaboration to protect commercial terms.

3

Match Payment Terms to Relationship Maturity

Never start with open account. Graduate terms systematically: start with advance payment or LC, then CAD/DP after 2–3 successful orders, then DA, then open account. Each step is a reward for proven reliability.

4

Take Out Export Credit Insurance for Open Account Trade

Export credit insurance (from providers like ECGC in India, Euler Hermes globally) covers 80–95% of invoice value against buyer insolvency or protracted default. It transforms open account risk into a manageable cost, typically 0.1–0.5% of insured turnover.

5

Use Factoring or Invoice Discounting to Convert Receivables to Cash

If you must offer open account terms to competitive buyers, factor your receivables immediately after shipment. You get 80–90% of invoice value upfront from the factor; the factor collects from your buyer. This removes cash flow strain and de-risks non-payment simultaneously.

6

Diversify Your Buyer Base, Avoid Concentration Risk

If 60%+ of your export revenue comes from a single buyer on open account, a single non-payment event can be catastrophic. Spread across multiple government-verified buyers across multiple markets. GTsetu’s 100+ country network makes diversification practical.

Red Flags, When NOT to Extend Credit Terms

🚩

Buyer Refuses Basic Verification

Any buyer unwilling to provide basic company registration details that can be verified through government records should be treated as high risk, regardless of order size.

🚩

Pressure to Skip LC “for speed”

Legitimate buyers understand LC timelines. Pressure to rush to open account on a first order is a common fraud pattern.

🚩

Payment History is Unclear

If you cannot get references from other exporters who have traded with this buyer on credit terms, do not extend credit.

🚩

Country-Level Restrictions

Some countries have foreign exchange controls limiting the ability to repatriate funds. Always check country risk before agreeing to open account terms.

SECTION 12

12 Payment Method Preferences by Industry

Industry

Most Common Method

Why This Method Dominates

GTsetu Relevance

Consumer Electronics

LC (large orders); Open Account (established supply chains)

High-value goods; large global OEMs use open account with audited EMS partners; new buyers require LC

Commodity markets; prices volatile; documentary security preferred; spot and futures markets have own norms

Verified B2B trading partner network with company registration checks

SECTION 13

13 How GTsetu Reduces Payment Risk Through Government-Tied Verification

🌐 Platform Spotlight, GTsetu

Know Who You’re Trading With: Six-Point Company Verification

Payment instruments like LCs, advance payment requirements, and credit insurance all manage risk after you’ve already decided to trade with a partner. The foundational risk reduction happens before the first order: by confirming that your trade partner is a legitimate, registered company. GTsetu connects manufacturers, exporters, importers, and distributors across 100+ countries, with government-tied verification of six essential company credentials:

✅ What GTsetu Verifies (6 Points):

Company Name (as registered with government authority)

Registered Address (official business address on record)

Registration Number (unique company identifier from government registry)

Company Status (active, dormant, struck off, or under liquidation)

Company Type (Private Limited, Public Limited, LLP, Sole Proprietorship, etc.)

Date of Certificate of Incorporation (when the company was legally formed)

GTsetu does not verify financial health, creditworthiness, trade references, tax documents, certifications, or operational capabilities. The verification confirms that the company exists as a registered legal entity through government data partnerships.

✅

Government-Tied Verification

Six-point company verification using official government registration data, not self-declared information.

🕵️

Anonymous Discovery

Browse verified company profiles without revealing your identity until mutual interest is confirmed.

📄

Built-In NDA Workflow

Formalise confidentiality before sharing pricing, product specs, or payment terms, with a complete audit trail.

🚫

Zero Broker Commission

No broker fees. Your commercial deal, including payment terms negotiated, stays entirely between you and your partner.

🔐

Encrypted Collaboration

Secure document and communication sharing, critical when discussing sensitive payment terms and financial arrangements.

🌍

100+ Countries

Active verified company network across Asia, Middle East, Europe, Africa, Australia, and the Americas, covering every major trade corridor.

~ Partially, confirms company exists but not creditworthiness

✗ LC still required for unknown buyers

Anonymous initial engagement

✓ Yes

✗ No

Built-in NDA before payment terms discussed

✓ Yes

~ External legal needed

Zero broker commission

✓ Always

✗ Often 5–15%

Manufacturers + distributors in one platform

✓ Single platform

✗ Separate sources needed

FAQ

? Frequently Asked Questions

QWhat is the safest payment method in international trade?

For the exporter (seller), Cash in Advance (Advance Payment) is the safest, payment is received before goods are shipped, eliminating non-payment risk entirely. For the importer (buyer), Open Account is the most favourable as they receive goods before paying. A Letter of Credit is the most balanced instrument for both parties, the bank guarantees the exporter will be paid, while the importer is assured that payment is conditional on proof of compliant shipment.

QWhat is the difference between advance payment and LC?

Advance Payment means the buyer pays the full amount before goods are shipped, maximum security for the seller, maximum risk for the buyer (who relies entirely on the seller shipping as promised). A Letter of Credit is a bank-issued instrument that guarantees the exporter will be paid once compliant shipping documents are presented, the bank provides the guarantee, and the buyer is protected because payment is conditional on proof of shipment. For new export relationships where full advance payment deters buyers, an LC is typically the preferred compromise.

QWhat does CAD, DP, and DA mean in trade?

These are all forms of Documentary Collection, a payment method where banks manage document exchange but do not guarantee payment. CAD (Cash Against Documents) and D/P (Documents against Payment) mean the same thing: the importer must pay at sight (immediately) before the collecting bank releases shipping documents. DA (Documents against Acceptance) means the importer signs a time draft (promising to pay on a future date) and the bank releases documents immediately, giving the importer possession of goods before paying, which carries more risk for the exporter.

QWhat is a Standby Letter of Credit (SBLC) and how is it different from a regular LC?

A regular LC (commercial LC) is the primary payment mechanism, it is the expected route for payment in the transaction. A Standby LC (SBLC) is a contingency instrument, it is only drawn upon if the importer fails to meet their payment obligation under an open account or other primary arrangement. The SBLC functions more like a bank guarantee or performance bond. Exporters use SBLCs to provide a safety net for open account trade with trusted buyers, without the full administrative burden of a documentary LC on every shipment.

QWhat is the difference between open account and consignment?

In an Open Account arrangement, the importer owns the goods from delivery and pays on a fixed future date (e.g., Net 60) regardless of whether they have sold the goods. In Consignment, the exporter retains legal ownership of the goods until the distributor sells them to end customers, payment to the exporter is triggered only by end-customer sales. Consignment carries higher risk: the exporter bears both goods risk (unsold or damaged inventory) and payment risk simultaneously. Both methods require highly trusted, government-verified counterparties.

QWhich payment method is best for a manufacturer entering a new export market?

For new market entry, the recommended approach is to start with Advance Payment or an Irrevocable Letter of Credit for the first 2–3 orders. Once a payment track record is established, graduate to CAD/DP, then DA terms, and eventually to open account for high-volume, proven buyers. Crucially, start with government-verified partners, using a platform like GTsetu for market entry partnerships means your counterparty’s company registration credentials are verified before any commercial commitment, giving you confidence that you are dealing with a legitimate registered business entity.

QWhat are the typical costs of a Letter of Credit?

LC costs vary by bank, transaction value, and country but typically include: issuance fee (paid by the importer, usually 0.25–0.5% of LC value + flat charges), advising fee (paid by the exporter, typically $50–$200 flat), confirmation fee if a confirmed LC is requested (additional 0.5–1.5% for high-risk issuing banks), document examination fee (per presentation, typically $50–$200), and discrepancy fees if documents have errors (typically $50–$100 per discrepancy). For a $100,000 shipment, total LC costs across both parties typically range from $500 to $2,500, a cost that must be weighed against the non-payment risk it mitigates.

QHow does export credit insurance help with open account trade?

Export credit insurance covers the exporter against non-payment by the overseas buyer due to commercial causes (insolvency, protracted default) or political causes (war, currency inconvertibility, import bans). Typically covering 80–95% of the insured invoice value, export credit insurance allows exporters to offer open account terms competitively, capturing business that would otherwise require expensive LCs, while limiting their maximum loss to 5–20% of invoice value. In India, ECGC offers this coverage; globally, providers include Euler Hermes, Atradius, and COFACE. Factoring companies will also accept insured receivables for invoice discounting at better rates.

Ready to Trade Internationally With Government-Verified Partners?

Join 500+ verified companies on GTsetu. Government-tied verification of six key company credentials across 100+ countries means you can confirm you’re dealing with a legitimate registered business entity before negotiating payment terms, with zero broker fees and built-in NDA workflows.

They represents the product, and research team behind GTsetu, a global B2B collaboration platform built to help companies explore cross-border partnerships with clarity and trust. The team focuses on simplifying early-stage international business discovery by combining structured company profiles, verification-led access, and controlled collaboration workflows.

With a strong emphasis on trust, and disciplined engagement, Team GTsetu shares insights on global trade, partnerships, and cross-border collaboration, helping businesses make informed decisions before entering deeper commercial discussions.