Why Use a Letter of Credit in International Trade?

A Letter of Credit bridges the trust gap between exporters and importers who may be separated by distance, different legal systems, and unknown creditworthiness. For the exporter, an LC (especially if confirmed) substitutes the bank’s credit for the buyer’s credit, significantly reducing the risk of non‑payment. For the importer, an LC assures that payment will only be made when the exporter has shipped the goods and presented the required documents (e.g., bill of lading, certificate of origin). LCs are particularly valuable for first‑time trade relationships, large‑value transactions, or when the importer’s country has political or currency instability.

⚡ Key Principle: Independence

The bank’s obligation to pay under an LC is independent of the underlying contract of sale. Even if the goods are defective or the contract is disputed, the bank must honor a complying presentation. Conversely, if documents do not strictly comply, the bank may refuse payment even if the goods arrived perfectly. This “strict compliance” rule is the foundation of LC security and the most common source of discrepancies.

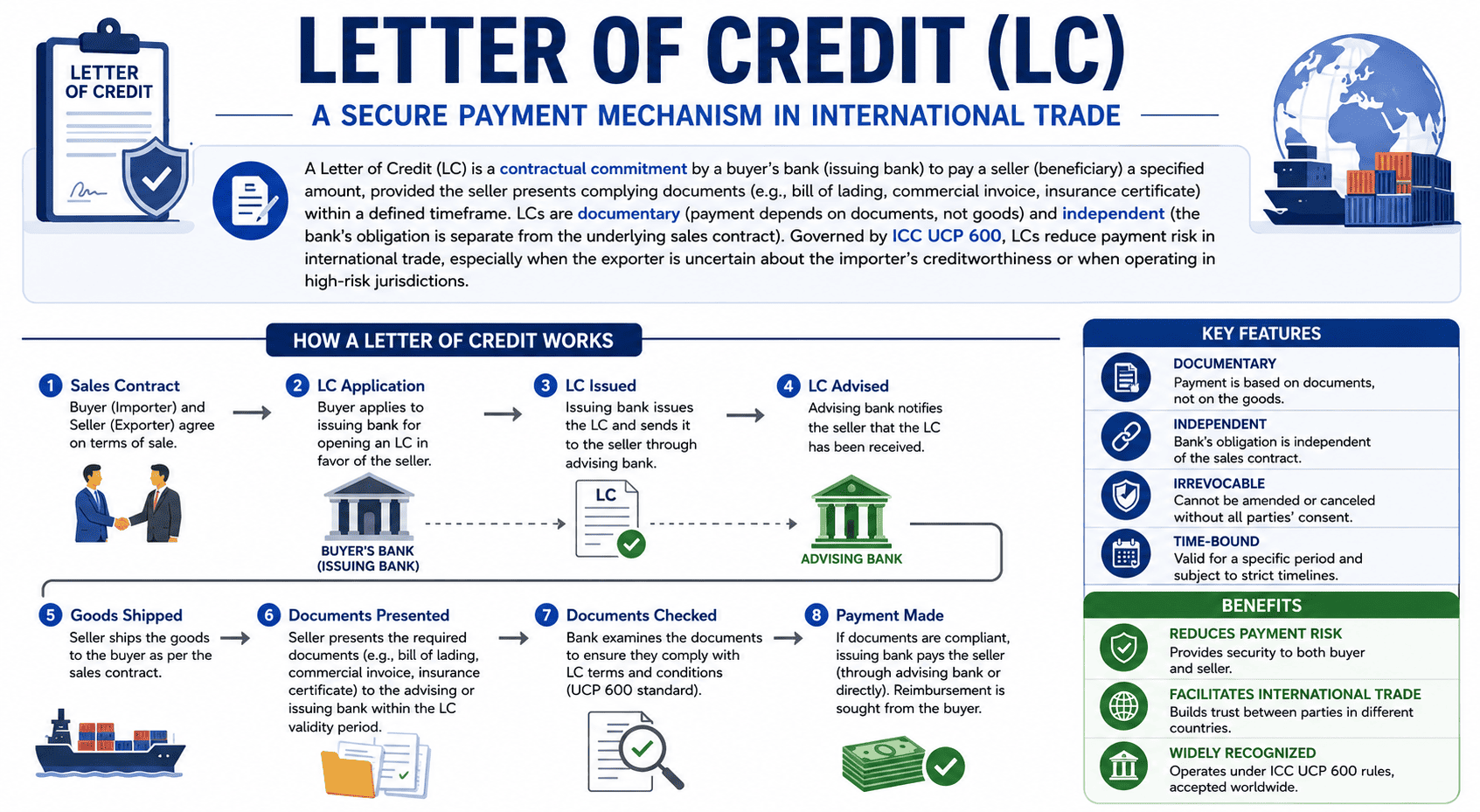

How an LC Works: 5‑Step Process

The Letter of Credit Process Step by Step

01

Sales Contract & LC Request

Exporter and importer agree on an LC as the payment method, specifying type (irrevocable, confirmed), documents required, and latest shipment date. Importer applies to its bank for an LC in favor of the exporter.

02

Issuing Bank Issues LC

The importer’s bank (issuing bank) issues the LC and sends it via SWIFT (usually MT700) to the exporter’s bank (advising bank). The LC must clearly state the documents, amount, expiry date, and any special conditions.

03

Advising Bank Notifies Exporter

The advising bank checks the LC’s authenticity and forwards it to the exporter. If the exporter requests confirmation, the advising bank (or another bank) adds its confirmation, assuming a second payment obligation.

04

Shipment & Document Presentation

Exporter ships the goods, obtains the required documents (e.g., bill of lading, invoice, packing list, insurance certificate), and presents them to the nominated bank (often the advising bank) within the LC’s validity period.

05

Document Examination & Payment

The nominated bank examines documents for compliance (usually within 5 banking days). If compliant, the bank pays the exporter (or discounts the LC). The documents are forwarded to the issuing bank, which reimburses the nominated bank and releases documents to the importer to take delivery of the goods.

Types of Letters of Credit

Types of Letters of Credit: Choosing the Right Structure

🔒

Irrevocable LC

Cannot be amended or cancelled without all parties’ consent. Under UCP 600, every LC is irrevocable unless expressly stated otherwise. Revocable LCs are virtually obsolete in international trade because they offer no security.

✔️ Standard for international trade

✔️ Provides certainty to exporter

✅

Confirmed LC

Adds a second payment undertaking from a bank in the exporter’s country (usually the advising or confirming bank). The confirming bank must pay even if the issuing bank fails. Essential when the issuing bank’s creditworthiness is questionable.

✔️ Higher cost (2‑8% extra fee)

✔️ Maximum payment security

↩️

Transferable LC

Allows the first beneficiary (middleman) to transfer part or all of the credit to a second beneficiary (actual supplier). Useful when the exporter is an intermediary that does not manufacture the goods. Only one transfer is permitted under UCP 600.

✔️ Protects intermediary’s margin

✔️ Requires express “transferable” clause

🔄

Back‑to‑Back LC

Two separate LCs: one from buyer to intermediary, and another from intermediary’s bank to the ultimate supplier. Used when a transferable LC is not available or when the intermediary wants to keep supplier and buyer unknown to each other.

✔️ Independent contracts

✔️ Complex but flexible

📆

Deferred Payment LC

Allows the importer to take possession of the goods and pay at a future date (e.g., 60 days after shipment). The bank issues a deferred payment undertaking. Provides financing to the importer.

✔️ Usance / term LC

✔️ Exporter may discount the deferred payment

⚡

Standby LC (SBLC)

Functions as a performance guarantee: it is drawn upon only if the obligor (e.g., importer) defaults in payment or performance. Governed by ISP98 rather than UCP 600. Common in construction, energy, and long‑term supply contracts.

✔️ “If not paid, then pay” structure

✔️ Lower drawing frequency

Critical Risks & Discrepancies

Common LC Discrepancies and Risks to Avoid

Banks reject documents that do not strictly comply with the LC terms. Discrepancies are the leading cause of payment delays and extra fees. Even minor typographical errors can result in refusal. Below are the most frequent discrepancies encountered in practice.

📄

Late Presentation

Documents presented after the LC expiry date or after the stipulated presentation period (usually 21 days after shipment). Banks will refuse payment even if the goods arrived perfectly.

✍️

Invoice Discrepancies

Beneficiary’s name or address not matching the LC; incorrect description of goods; unit prices or total amount exceeding the LC value; inconsistent currency.

🚢

Bill of Lading Issues

Not “clean” (claused as damaged); incorrect consignee (e.g., “to order” vs named consignee); not “shipped on board” dated; not signed by the carrier or agent; inconsistent port of loading/discharge.

📦

Insurance Certificate Issues

Insufficient coverage (must be at least 110% of invoice value unless otherwise stated); incorrect risks covered; endorsement not matching LC; currency mismatch.

⏰

Expired LC or Shipment Dates

The LC expiry date or the latest shipment date has passed. Unless the LC is amended, any presentation after these dates is automatically discrepant.

✨ Practical Guidance

To minimize discrepancies: (1) Train staff on LC requirements before shipment; (2) have documents checked by a trade finance specialist or freight forwarder; (3) ask the advising bank for a “pre‑advice” or informal check before formal presentation; (4) include a “reasonable tolerance” clause for quantity, amount, and weight in the LC (e.g., “5% more or less”). Many discrepancies can be avoided by careful drafting of the LC at the outset.

LC Costs & Payment Alternatives

Letter of Credit Costs and Alternatives

LCs are among the most secure payment methods but also among the most expensive. Fees are typically split between importer and exporter as negotiated in the sales contract. Below is a comparative overview of common payment terms in international trade, ranging from highest risk for exporter (open account) to lowest risk (advance payment).

| Payment Method | Risk to Exporter | Risk to Importer | Typical Cost | Best For |

|---|

| Advance Payment (CIA) | None (paid before shipment) | High (goods may not be shipped) | Wire transfer fees | Small orders, new relationships, high‑risk countries |

| Letter of Credit (LC) | Low (bank undertakes to pay if documents comply) | Low (payment only against documents proving shipment) | 1‑8% of value (issuance + advising + possible confirmation) | Large transactions, first‑time partners, documentary trades |

| Documentary Collection (D/P or D/A) | Moderate (importer may refuse to pay or accept) | Low (documents only released against payment or acceptance) | Lower than LC (bank handling fee) | Established relationships, standard goods |

| Open Account (O/A) | High (importer pays after receiving goods) | None (pays after inspection) | Minimal (wire transfer fees) | Long‑term trust, low‑risk countries, high‑volume buyers |

Legal Framework: UCP 600 & SWIFT

Legal Framework: UCP 600, SWIFT and Electronic LCs

The vast majority of LCs are subject to the ICC Uniform Customs and Practice for Documentary Credits (UCP 600), which provides standard rules for examination of documents, deadlines, liability of banks, and handling of discrepancies. LCs are issued via the SWIFT network using message types MT700 (issuance) and MT701 (amendment). Although LCs are issued electronically, the document examination process remains largely paper‑based, leading to inefficiencies. Efforts to digitise (e‑LC or electronic Letters of Credit) are underway, but global adoption of fully digital LCs remains limited due to legal recognition and interoperability challenges. Blockchain‑based platforms (e.g., Komgo, Bolero, Contour) are emerging to address these gaps.

🌐 SWIFT MT700 Field Basics

An MT700 message contains fields such as: 20 (LC number), 31C (date of issue), 31D (expiry date and place), 50 (applicant/importer), 59 (beneficiary/exporter), 32B (currency and amount), 44A (loading/dispatch port), 44B (destination port), 44C (latest shipment date), 45A (description of goods), 46A (documents required), 47A (additional conditions), 48 (period for presentation), and 49 (confirmation instructions).

FAQ

Frequently Asked Questions

QWhat is the difference between a confirmed and an unconfirmed Letter of Credit?

An unconfirmed LC provides only the issuing bank’s payment undertaking. A confirmed LC adds a second guarantee from a bank in the exporter’s country (usually the advising or confirming bank), which promises to pay even if the issuing bank fails to honor its obligation. Confirmed LCs are used when the exporter has doubts about the issuing bank’s creditworthiness or when there are political or currency risks in the importer’s country. Confirmation fees typically add 2‑8% to the LC cost, usually borne by the importer or split between parties.

QWhat is the difference between a revocable and an irrevocable Letter of Credit?

An irrevocable Letter of Credit cannot be amended or cancelled without the consent of all parties (issuing bank, beneficiary, and any confirming bank). A revocable LC can be modified or cancelled by the issuing bank at any time without notice to the beneficiary. Under UCP 600, all LCs are presumed irrevocable unless expressly stated otherwise. Revocable LCs are rarely used in international trade because they offer no payment security to the exporter, the bank could cancel the LC just before the exporter ships the goods.

QHow much does a Letter of Credit cost?

LC fees typically range from 1% to 8% of the transaction value, depending on the importer’s creditworthiness, country risk, and whether confirmation is added. Fees include: issuance fee (paid by importer), advising fee (paid by exporter or importer), confirmation fee (2‑8% if confirmed), amendment fees (per amendment), and document examination fees (per presentation). Additional charges may include courier fees and SWIFT message fees. Both parties should clarify who bears which costs in the sales contract. While LCs are expensive, they provide high payment security for exporters and may enable better contract terms (e.g., longer credit periods) for importers.

QWhat is a “clean” Bill of Lading and why is it required under most LCs?

A “clean” Bill of Lading is one that does not contain any clause or notation declaring a defective condition of the goods or packaging (e.g., “cartons damaged,” “drums leaking”). Most LCs require a clean shipped on board bill of lading as proof that the carrier received the goods in apparent good order and condition. If the bill of lading is “claused” (not clean), the bank will treat it as a discrepancy and may refuse payment unless the LC expressly allows clauses.

QWhat is the difference between a Transferable LC and a Back‑to‑Back LC?

A Transferable LC allows the first beneficiary (middleman) to transfer the credit to a second beneficiary (supplier) under the same LC terms, with only one transfer permitted. The original LC must explicitly state “transferable.” A Back‑to‑Back LC involves two separate LCs: one from the buyer to the middleman’s bank, and another from the middleman’s bank to the ultimate supplier. Back‑to‑back LCs offer more flexibility (e.g., different expiry dates, different document requirements) but require that the middleman has sufficient credit line with its bank. Transferable LCs are simpler but less flexible.