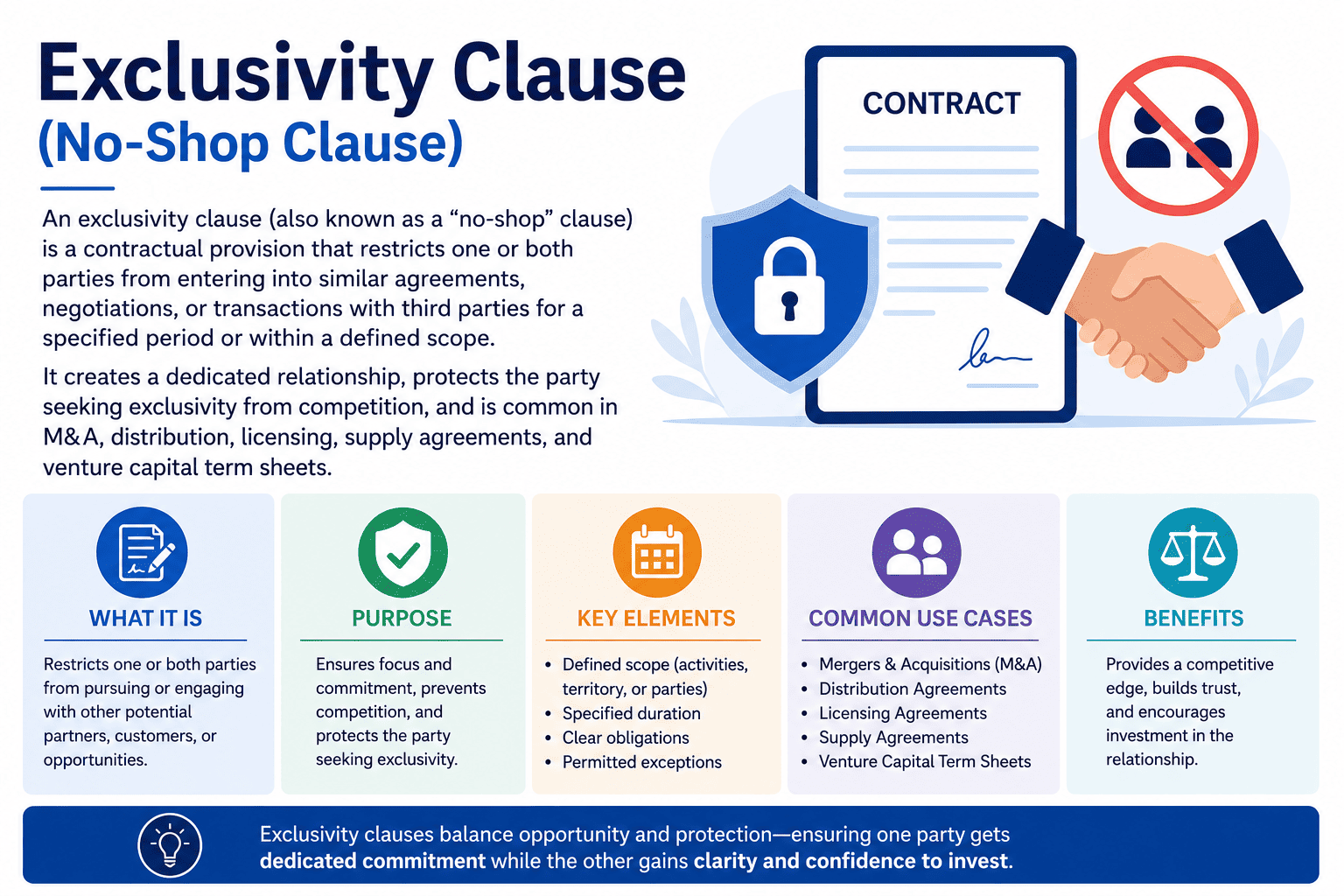

Why Exclusivity Clauses Matter

Exclusivity clauses serve a fundamental purpose in contract law: they provide certainty and protect investment. When a party agrees to exclusivity, it signals commitment and prevents the counterparty from “shopping” the deal to competitors. For the party receiving exclusivity (e.g., a buyer in M&A, a distributor, or an investor), it ensures that time, resources, and due diligence efforts are not wasted on a deal that could be undermined by a better offer to the other party.

However, exclusivity creates tension. The party granting exclusivity loses flexibility and may miss better opportunities. Courts therefore scrutinise exclusivity clauses for reasonableness, they must be limited in duration, scope, and geographic reach. Overly broad or indefinite exclusivity clauses risk being declared unenforceable as unreasonable restraints of trade under Section 27 of the Indian Contract Act, 1872, or equivalent competition laws in other jurisdictions.

⚡ Key Principle

An exclusivity clause is not automatically illegal. It becomes unenforceable only if it is unreasonable, meaning it goes beyond what is necessary to protect the legitimate interests of the party seeking exclusivity. Reasonableness is judged by duration, geographic scope, and the activities restricted.

Types of Exclusivity

Common Types of Exclusivity Clauses

🤝

Mutual Exclusivity

Both parties agree not to work with competitors. Common in joint ventures, strategic partnerships, and long-term supply agreements where both sides commit exclusively to each other.

🔒

Unilateral (One-Sided) Exclusivity

Only one party is restricted. Examples: a distributor agrees to sell only the supplier’s products (but supplier can sell through other channels), or a seller in M&A agrees not to shop for other buyers.

🚫

No-Shop / No-Talk

Most common in M&A and venture capital. The target company (or founder) agrees not to solicit, initiate, or engage in discussions with other potential acquirers or investors for a set period (typically 30–90 days).

🗺️

Territorial Exclusivity

The distributor or licensee is the only party allowed to sell products in a defined geographic region (e.g., “exclusive distributor for North America”).

🏷️

Product or Field-of-Use Exclusivity

The licensee has exclusive rights to use intellectual property within a specific product category or technical field, while the licensor may license the same IP to others for different fields.

⏱️

Employment Exclusivity

Requires an employee to work only for that employer (no second job). In many jurisdictions, exclusivity clauses are banned for zero-hours or low-earning workers.

Essential Elements

What a Well-Drafted Exclusivity Clause Must Include

1. Clear Scope of Restriction

Specify exactly what activities are prohibited: soliciting, negotiating, providing information, or entering agreements with third parties.

2. Defined Duration

A fixed time period (e.g., “60 days from signing” or “for the term of the agreement”). Indefinite exclusivity is highly risky and often unenforceable.

3. Geographic Limits

If territorial, define the region (country, state, city, or global). Vague terms like “worldwide” may be reasonable for some products but overbroad for others.

4. Carve-outs and Exceptions

Permitted activities: existing relationships, unsolicited offers, strategic partnerships outside the scope, or fiduciary duty exceptions for public companies.

5. Fiduciary Out (for Public Companies)

Allows the board to consider unsolicited superior proposals if required by fiduciary duties, typically with a matching right for the exclusive party.

6. Break Clauses / Milestones

Allows the restricted party to terminate exclusivity if the other party fails to meet deadlines (e.g., “if Investor does not provide draft SPA within 30 days, exclusivity terminates”).

Sample Clause Language

Real-World Example: M&A No-Shop Clause

📄 EXCLUSIVITY / NO-SHOP PROVISION (M&A Context)

From the date of this Agreement until the earlier of the Closing and the termination of this Agreement, Seller shall not, and shall cause its Affiliates and representatives not to, directly or indirectly: (i) solicit, initiate, facilitate or encourage the submission of any Acquisition Proposal; (ii) participate in any discussions or negotiations regarding, or furnish to any Person any non-public information with respect to, or take any other action to facilitate or encourage any inquiries or the making of any proposal that constitutes, or could reasonably be expected to lead to, any Acquisition Proposal; or (iii) enter into any agreement with respect to any Acquisition Proposal. Seller shall immediately cease and terminate any existing discussions or negotiations with any Person (other than Buyer) with respect to any Acquisition Proposal.

✨ Drafting Tip

Always include a fiduciary out clause for public companies: “Nothing in this Section shall prevent the Board from considering an unsolicited bona fide written Acquisition Proposal if the Board determines in good faith that failing to do so would breach its fiduciary duties.” Also include a matching right period (e.g., 5 business days) for the exclusive party to revise its offer.

Enforceability & Risks

Legal Enforceability: When Exclusivity Clauses Are Struck Down

Courts in common law jurisdictions (India, UK, US) generally uphold exclusivity clauses that are reasonable. The test, derived from Section 27 of the Indian Contract Act, 1872 (which voids agreements in restraint of trade), is whether the restriction:

- Protects a legitimate business interest (e.g., confidential information, customer relationships, investment in due diligence).

- Is no wider than necessary to protect that interest.

- Is reasonable in duration, geographic scope, and the activities restricted.

- Is not contrary to public policy.

Common Reasons for Unenforceability

❌ Excessive Duration

A 2-year exclusivity period in a fast-moving industry (e.g., software licensing) may be struck down, while 60–90 days for M&A due diligence is standard.

❌ Overly Broad Geographic Scope

“Worldwide” exclusivity for a small local distributor is unreasonable; for a global software license, it may be fine.

❌ No Carve-out for Unsolicited Offers

Courts are reluctant to enforce absolute no-talk clauses that prevent a party from even receiving an unsolicited superior offer, especially for public companies.

❌ Ambiguity

If the clause does not clearly define what is prohibited (e.g., “shall not engage in competing activities” without defining “competing”), it may be void for vagueness.

⚠️ Jurisdictional Caution

Under Section 27 of the Indian Contract Act, 1872, any agreement in restraint of trade is void. However, exclusivity clauses that are limited in time and scope and ancillary to a legitimate commercial transaction (e.g., M&A, distribution) are generally enforced. In employment contracts, post-termination non-competes are void in India. For EU competition law, exclusivity clauses in vertical agreements may benefit from the Vertical Block Exemption Regulation if market share thresholds are met.

Exclusivity vs Non-Compete vs Non-Solicit

How Exclusivity Differs from Non-Compete and Non-Solicit Clauses

| Aspect | Exclusivity Clause | Non-Compete Clause | Non-Solicit Clause |

|---|

| Timing | During the contract term (or a defined negotiation period) | Typically post-termination | Usually post-termination (but can be during) |

| What it restricts | Working with, negotiating with, or selling to competitors | Working for or starting a competing business | Soliciting clients, customers, or employees of the counterparty |

| Common in | Distribution, M&A term sheets, VC term sheets, supply agreements | Employment contracts (restricted in many jurisdictions), business sale agreements | Employment contracts, business sale agreements, referral agreements |

| Typical duration | 30–90 days (negotiation) or term of agreement (long-term) | 6 months – 2 years (post-termination) | 6 months – 2 years (post-termination) |

| Enforceability level | Generally enforceable if reasonable | Highly scrutinised; often unenforceable against employees in many jurisdictions | Generally enforceable if reasonable and protects legitimate interests |

VC Term Sheets & M&A

Exclusivity in Venture Capital Term Sheets and M&A

In venture capital, the exclusivity clause (often called “no-shop”) is a standard term sheet provision. The investor wants assurance that the founder will not use the term sheet to shop for better offers while the investor spends time and money on due diligence and legal documentation. For founders, exclusivity can be dangerous if the investor is slow or later withdraws.

Founder-Friendly Negotiation Points

- Short exclusivity period: 30 days for early-stage, 45–60 days for complex deals, rather than 90 days.

- Milestone-based termination: Exclusivity ends automatically if investor fails to provide draft documents or complete due diligence by specified dates.

- Carve-out for unsolicited offers: Founder may receive but not solicit alternative offers; if a superior offer comes, the investor gets a matching right (e.g., 5 business days).

- Fiduciary duty exception: For corporate boards, the ability to consider superior proposals if legally required.

- Reciprocity: Ask the investor to commit to “good faith” efforts to close within the exclusivity period.

01

Term Sheet Signed

Exclusivity period begins (typically 30–90 days). Founder cannot solicit other investors.

02

Investor Conducts Due Diligence

Investor reviews legal, financial, and commercial matters. Founder provides access to data room.

03

Definitive Documents Drafted

SPA, SHA, and other agreements prepared. Founder may negotiate terms but cannot seek competing offers.

04

Closing or Exclusivity Expiry

If conditions met, deal closes. If not, exclusivity ends and founder may approach other investors.

Employment Context

Exclusivity Clauses in Employment Contracts

In employment, exclusivity clauses require the employee to work only for that employer and not hold a second job. Many jurisdictions restrict or ban exclusivity clauses for certain worker categories to protect flexible working.

- UK: Exclusivity clauses are banned for zero-hours workers and those earning below the Lower Earnings Limit (£129 per week). Employers cannot dismiss or treat such workers unfavourably for breaching an exclusivity clause.

- India: While exclusivity (no second job) is generally permitted during employment, post-termination non-compete clauses are void under Section 27 of the Contract Act. However, exclusivity is different from non-compete, it applies only during the employment period.

- US: Most employment is at-will; exclusivity clauses are permitted unless restricted by state law. Some states prohibit exclusivity for low-wage workers.

📋 Employer Note

Exclusivity clauses in employment contracts should clearly state the consequence of breach (e.g., disciplinary action, termination). For senior executives, the clause may be coupled with a “no other business interests” provision requiring disclosure of outside directorships. Always check local labour laws, in many jurisdictions, exclusivity cannot be enforced against workers on zero-hours or low-income contracts.

FAQ

Frequently Asked Questions

QIs an exclusivity clause legally binding?

Yes, if it is clear, reasonable in scope and duration, and supported by consideration. Courts will enforce exclusivity clauses unless they are found to be unreasonable restraints of trade under applicable law (e.g., Section 27 of the Indian Contract Act, or competition laws in the EU/US). The clause must be specific about prohibited activities, geographic scope, and time period. Vague or indefinite restrictions are likely unenforceable.

QWhat is the difference between an exclusivity clause and a non-compete clause?

Exclusivity clauses govern the current relationship, requiring a party to deal only with the counterparty during the contract term (e.g., a distributor selling only one brand’s products, or a seller not shopping for other buyers during M&A negotiations). Non-compete clauses apply post-termination, preventing a party from engaging in competing activities after the relationship ends (e.g., a former employee cannot work for a competitor for one year). Non-competes face stricter legal scrutiny, especially in employment contexts.

QCan an exclusivity clause be one-sided?

Yes, exclusivity can be unilateral (one party restricted) or mutual (both parties restricted). Unilateral exclusivity is common in distribution (distributor sells only the supplier’s products, but supplier may sell through other channels) and in M&A (seller cannot shop for other buyers, but buyer is free to pursue other targets). Mutual exclusivity appears in joint ventures and strategic partnerships where both parties commit exclusively to each other in a defined field. The courts do not require mutuality, but the restriction must still be reasonable.

QHow long can an exclusivity clause last?

For M&A and VC term sheets, typical exclusivity periods are 30–90 days. For distribution or supply agreements, exclusivity may last the entire contract term (e.g., 1–5 years). Longer periods are subject to reasonableness review, courts may strike down exclusivity that extends beyond what is necessary to protect the counterparty’s legitimate interests. In fast-moving industries (tech, software), courts are more likely to find long exclusivity periods unreasonable.

QWhat happens if a party breaches an exclusivity clause?

The non-breaching party can sue for breach of contract. Remedies may include: (i) damages to compensate for losses (e.g., lost opportunity, wasted due diligence costs); (ii) injunctive relief to prevent the breaching party from continuing to negotiate with a third party; (iii) termination of the underlying agreement. In M&A, a breach of exclusivity (e.g., seller negotiating with another buyer) often triggers a termination fee payable to the original buyer.

QAre exclusivity clauses allowed under competition law?

Generally yes, if the parties are not dominant in the relevant market. In the EU, exclusivity clauses in vertical agreements (between supplier and distributor) are exempted under the Vertical Block Exemption Regulation (VBER) if the supplier’s market share is below 30%. Above that threshold, an individual assessment is required. In the US, exclusivity clauses are analysed under the rule of reason, they are lawful unless they have anticompetitive effects that outweigh procompetitive justifications. In India, the Competition Act, 2002, prohibits anti-competitive agreements, but normal exclusivity arrangements are not automatically void.