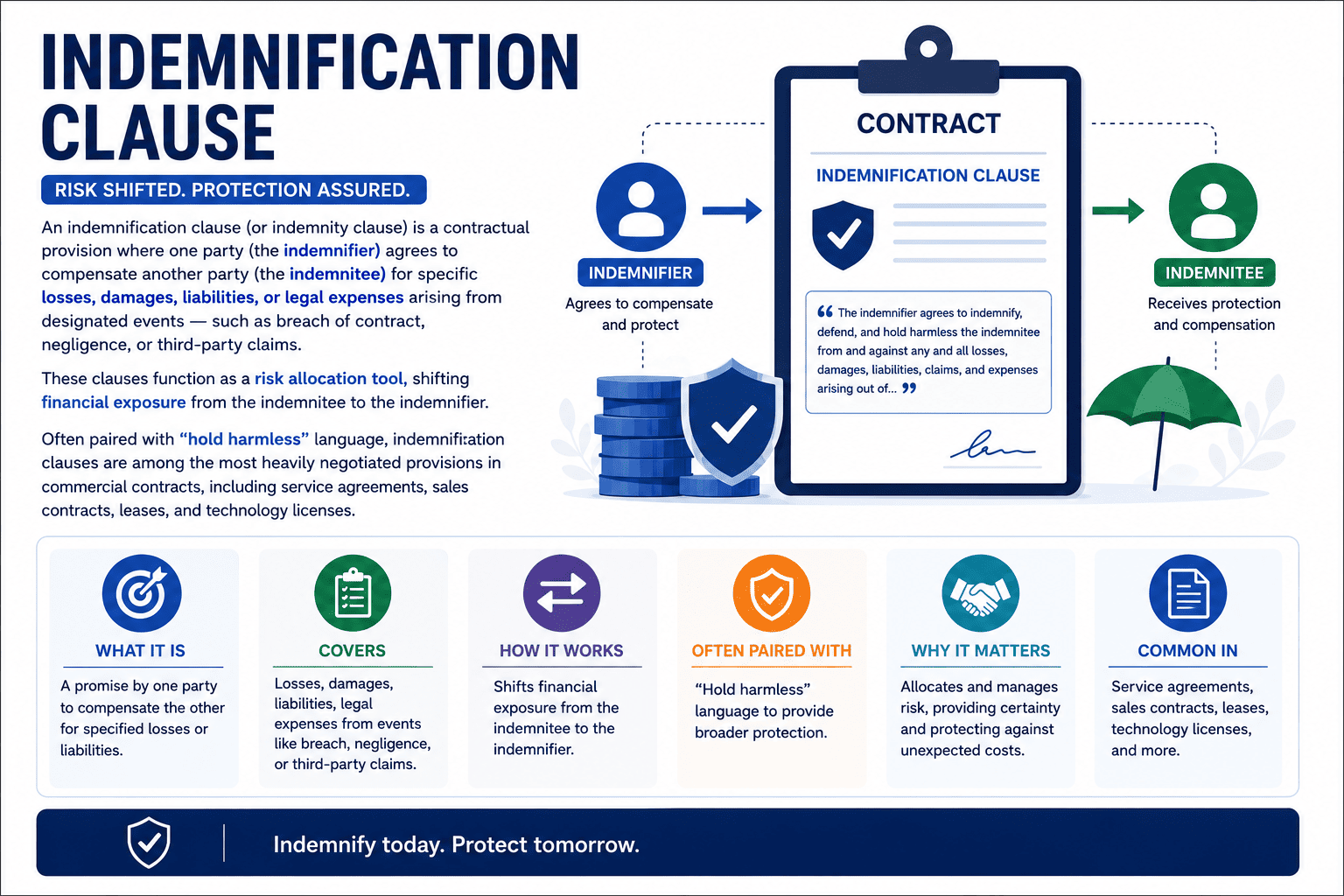

Why Indemnification Clauses Are Critical in Commercial Contracts

Indemnification clauses answer a fundamental question before any dispute arises: who pays when something goes wrong? Without a clear indemnity provision, the parties may be left to common law remedies that often exclude consequential damages, limit recovery to direct losses, and require proving causation. A well‑drafted indemnification clause provides contractual certainty, allocates risk to the party best able to control or insure against it, and can cover defense costs, third‑party claims, and even indirect losses if expressly included. For these reasons, indemnity provisions are routinely negotiated in supply agreements, outsourcing contracts, real estate leases, construction contracts, and M&A transactions.

⚡ Key Principle: Independence

An indemnification obligation is typically independent of the underlying contract. Even if the indemnified party is partially at fault, a broadly worded indemnity clause may still require the indemnifier to pay, unless the clause expressly excludes coverage for the indemnitee’s own negligence. However, many states refuse to enforce indemnification for a party’s sole negligence, gross negligence, or intentional misconduct as a matter of public policy.

Core Components of an Indemnity Clause

Key Elements of an Indemnification Provision

🎯

Scope of Indemnity

Defines which losses, damages, and expenses are covered. May include direct damages, third‑party claims, legal fees, settlements, and sometimes consequential or indirect losses if expressly stated.

✔️ Typically covers “any and all claims, losses, damages, liabilities, costs and expenses (including reasonable attorneys’ fees)”

⚡

Triggering Events

Specific acts or omissions that activate indemnification: breach of contract, negligence, bodily injury, property damage, IP infringement, or violation of law.

✔️ Negotiated heavily, indemnitees want broad triggers; indemnifiers seek narrow, specific events

⏳

Duration / Survival

Specifies how long indemnification obligations last after contract termination or expiry. Common survival periods range from 1 to 7 years, with fundamental representations (title, authority) often surviving indefinitely.

✔️ Survival clause should be coordinated with statute of limitations

🔒

Limitations & Exclusions

Monetary caps (e.g., “indemnification shall not exceed US $500,000”), exclusions for certain damage types (consequential, punitive), and carve‑outs for the indemnitee’s own negligence.

✔️ Liability caps often exclude indemnification for IP infringement or willful misconduct

One‑Sided vs. Mutual Indemnification

One‑Sided vs. Mutual Indemnification: Choosing the Right Structure

The choice between unilateral and reciprocal indemnity reflects the parties’ relative bargaining power, control over risks, and industry practice. One‑sided clauses require only one party to indemnify the other, while mutual clauses create symmetrical obligations.

| Aspect | One‑Sided (Unilateral) Indemnity | Mutual Indemnity |

|---|

| Who indemnifies? | Only one party (typically the vendor, service provider, or lessee) | Both parties indemnify each other for losses arising from their respective actions |

| Risk allocation | Concentrates risk on one party; common when one party has significantly more control over liabilities | Balanced; each party bears risk for its own negligence or breach |

| Common use cases | Software licensing (vendor indemnifies for IP claims), vendor agreements, construction subcontracts | Joint ventures, strategic partnerships, manufacturing agreements, commercial leases (both ways) |

| Negotiation leverage | Favors the party with stronger bargaining power (e.g., large customer vs. small supplier) | Refers a more equal relationship or where both parties create meaningful risk |

| Court scrutiny | May be reviewed for unconscionability, especially in consumer or adhesion contracts | Generally viewed as fairer and more enforceable |

📄 Sample One‑Sided Indemnification Clause (Vendor → Customer)

“Vendor agrees to indemnify, defend, and hold harmless Customer, its affiliates, and their respective officers, directors, employees, and agents from and against any and all claims, losses, damages, liabilities, costs, and expenses (including reasonable attorneys’ fees) arising out of or relating to (i) any breach of this Agreement by Vendor, (ii) any bodily injury or property damage caused by Vendor’s products or services, (iii) any violation of applicable law by Vendor, or (iv) any third‑party claim alleging that Vendor’s deliverables infringe any intellectual property rights.”

📄 Sample Mutual Indemnification Clause

“Each party (the ‘Indemnifying Party’) shall indemnify, defend, and hold harmless the other party (the ‘Indemnified Party’) from and against any and all claims, losses, damages, liabilities, and expenses (including reasonable attorneys’ fees) arising out of or resulting from (a) any breach of this Agreement by the Indemnifying Party, (b) any negligent act or omission of the Indemnifying Party, or (c) any violation of applicable law by the Indemnifying Party. The indemnification obligations in this Section shall not apply to the extent the claim is caused by the gross negligence or willful misconduct of the Indemnified Party.”

Common Triggers & Exclusions

Typical Indemnification Triggers and Exclusions

| Category | Examples | Typical Negotiation Outcome |

|---|

| Breach of contract | Breach of representations, warranties, or covenants | Usually covered; may be subject to de minimis threshold (basket) and cap |

| Third‑party claims | IP infringement, personal injury, property damage, product liability | Almost always covered in commercial contracts; often with no cap for IP claims |

| Violation of law | Non‑compliance with environmental, labor, data privacy, or anti‑bribery laws | Covered by indemnitee; indemnifiers may seek carve‑out for unknown violations |

| Indemnitee’s own negligence | Loss caused solely or partly by indemnitee’s fault | Often excluded or limited to comparative fault; some broad clauses cover indemnitee’s negligence (enforceability varies by state) |

| Consequential / indirect damages | Lost profits, loss of use, business interruption | Frequently excluded or subject to separate cap; sometimes included for IP claims |

| Punitive or exemplary damages | Damages intended to punish | Generally excluded as against public policy to indemnify for punitive damages |

Procedural Steps: How Indemnification Works

The Indemnification Claims Process: Notice, Defense, and Settlement

Indemnification clauses typically include procedural obligations that, if not followed, can waive or reduce the indemnity. Careful attention to notice periods, control of defense, and settlement approval rights is essential.

01

Prompt Written Notice

Indemnitee must notify indemnifier of any claim or potential claim within a specified period (often 10‑30 days). Failure to give timely notice may relieve indemnifier of obligations if it was prejudiced by the delay.

02

Tender of Defense (Third‑Party Claims)

For third‑party lawsuits, indemnitee tenders defense to indemnifier. Indemnifier typically has the right to assume control of the defense using counsel of its choice, subject to no conflict of interest.

03

Cooperation and Information

Indemnitee must cooperate reasonably in the defense, provide relevant documents and information, and make employees available for testimony.

04

Settlement Restrictions

Indemnifier generally cannot settle a claim without indemnitee’s consent if the settlement imposes any obligation on indemnitee (e.g., admission of wrongdoing, non‑monetary relief). Indemnitee cannot settle without indemnifier’s consent if indemnifier will pay.

05

Payment of Indemnity

Indemnifier pays covered losses, either as they are incurred or after final resolution. Some clauses require indemnifier to advance defense costs pending final disposition.

✨ Drafting Tip: Defense Control

Indemnitees should retain the right to participate in the defense at their own expense and to approve any settlement that does not include a full release. Indemnifiers should require timely notice and the right to assume defense to avoid being bound by unfavorable settlements arranged by the indemnitee. Ambiguity in these procedural provisions is a common source of litigation.

Common Pitfalls & Enforceability Risks

Indemnification Risks: Overbroad Language, Unenforceability, and Uninsured Exposure

⚖️

“Any and all claims” without limitation

Overly broad language that purports to indemnify the indemnitee for its own sole negligence may be unenforceable in many states. Courts often strike “no‑fault” indemnities as violative of public policy.

💰

No liability cap

Uncapped indemnification exposes the indemnifier to potentially unlimited financial liability. Even in one‑sided clauses, indemnifiers should negotiate a cap (e.g., amount equal to contract value or a fixed sum), with higher caps for IP infringement or confidentiality breaches.

📋

Indemnification for indemnitee’s own negligence

Clauses requiring a party to indemnify another for the indemnitee’s own negligence are strictly construed and may be void in construction, transportation, or consumer contracts under state anti‑indemnity statutes. Always check applicable law.

⏰

Failure to comply with notice provisions

Strict notice deadlines (e.g., “within 10 days of becoming aware”) are often enforced. Indemnitees that miss a deadline may lose their indemnity entirely, even for meritorious claims.

🚫

Inconsistent with insurance

Indemnification obligations that exceed available insurance coverage can bankrupt a small indemnifier. Review the clause alongside the indemnifier’s insurance policies to ensure coverage. Additional insured endorsements may be required.

Limitation of Liability vs. Indemnification

How Indemnification Interacts with Limitation of Liability Clauses

A common drafting challenge is whether the liability cap in a limitation of liability clause applies to indemnification obligations. Unless the contract explicitly states otherwise, courts may interpret that the cap applies to all claims, including indemnity. To avoid uncertainty, drafters should state clearly: “The limitation of liability in Section X shall not apply to (i) a party’s indemnification obligations under Section Y, (ii) breach of confidentiality, or (iii) infringement of intellectual property rights.” Most commercial contracts carve out indemnity obligations from the general liability cap, because the purpose of indemnity is to shift specific risks that could exceed the cap.

| Risk Allocation Tool | Primary Function | Typical Cap / Limit | Typical Carve‑Outs from Cap |

|---|

| Limitation of liability | Caps total aggregate liability for all claims under the contract (e.g., amount of fees paid or US $500k) | Almost always applies to direct and indirect damages | Indemnification, IP infringement, confidentiality breach, gross negligence, willful misconduct |

| Indemnification clause | Shifts specific, identified risks to the party best able to bear them | Often has a separate cap (or no cap for IP/infringement) | Indemnification itself may be carved out of general liability cap |

FAQ

Frequently Asked Questions

QWhat is the difference between a one‑sided and a mutual indemnification clause?

A one‑sided (unilateral) indemnification clause requires only one party to indemnify the other. This is common when one party has significantly more control over risks, such as a vendor indemnifying a customer for product defects or IP infringement. A mutual indemnification clause requires both parties to indemnify each other for losses arising from their respective actions, negligence, or breaches. Mutual clauses are typical in joint ventures, partnerships, and complex service agreements where both parties create meaningful risk.

QWhat is the difference between indemnification and a hold harmless clause?

While often used together, indemnification typically involves one party reimbursing another for losses already incurred (e.g., paying a settlement or judgment). A hold harmless clause prevents one party from bringing claims against the other, acting as a release. Many contracts combine both using “indemnify and hold harmless” language. In practice, most courts interpret the phrases together as creating a duty to compensate for losses and to release the other party from liability. However, some jurisdictions distinguish between them, making precise drafting important.

QAre indemnification clauses enforceable if they are too broad?

Courts often scrutinize overly broad indemnification clauses and may refuse to enforce them, especially if they appear unconscionable or violate public policy. Most states do not permit a party to indemnify another for its own gross negligence, recklessness, or intentional misconduct. ‘Broad form’ or ‘no‑fault’ indemnities that require one party to cover all losses regardless of fault may be held unenforceable. Clear, specific language that limits indemnification to reasonable, foreseeable scenarios improves enforceability. Jurisdictions such as Texas, New York, and California have specific anti‑indemnity statutes for construction and certain other industries.

QWhat types of damages can be recovered under an indemnification clause?

Indemnification can cover direct damages (contract damages, repair costs, refunds), third‑party claim payments (settlements, judgments), defense costs (attorneys’ fees, expert witness fees), and, if expressly stated, consequential damages (lost profits, business interruption). Unlike common law damages, indemnity clauses can also recover attorneys’ fees and costs of enforcement. However, most indemnification clauses exclude punitive damages, fines, and penalties as a matter of law or policy.

QWhat is a “basket” or “floor” in an indemnification clause?

A basket (or deductible) is a threshold that must be exceeded before indemnification applies. A “de minimis basket” means that no indemnity is payable for individual claims below a certain amount (e.g., US $5,000). An “aggregate basket” means that indemnity applies only after total covered losses exceed a specified amount (e.g., US $50,000), after which the indemnifier pays either all losses or only the excess. Baskets are heavily negotiated and are designed to avoid administrative burdens of processing small claims.