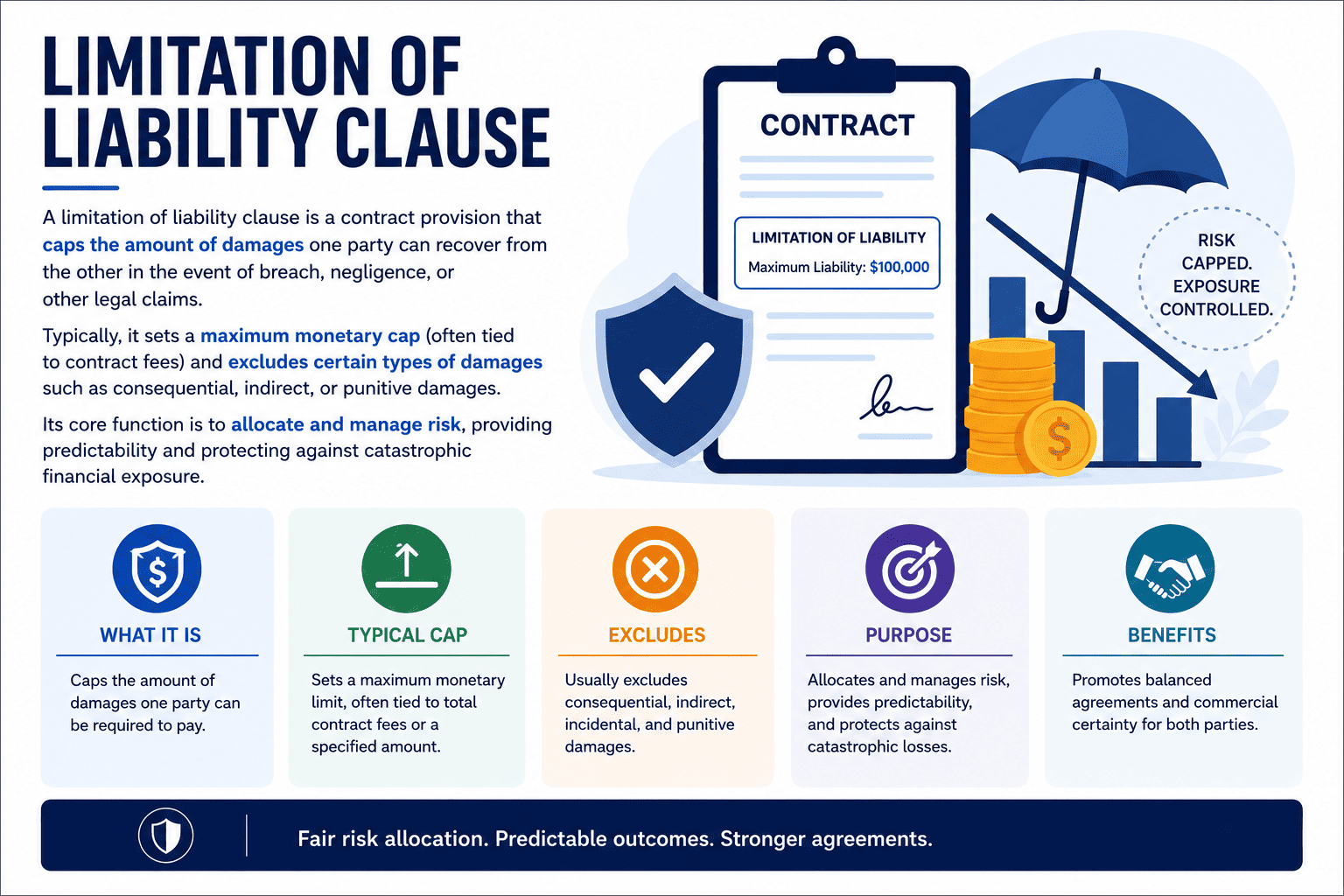

Why Limitation of Liability Clauses Are Critical

In any commercial contract, the limitation of liability clause is often the most heavily negotiated provision, and for good reason. Without it, a party could be exposed to unlimited liability for breaches that are routine in the course of business. A simple delay in delivery or a software bug could trigger claims for lost profits, business interruption, reputational damage, and other consequential losses that far exceed the contract’s value.

The clause provides predictability and risk allocation. The supplier knows its maximum exposure and can price its products or services accordingly. The customer knows the cap and can decide whether to accept it, negotiate a higher cap, or purchase insurance. According to industry data, over 80% of commercial contracts use a general liability cap, and the most common cap amount is 1X the annual fees paid under the contract.

⚡ Key Principle

The limitation of liability clause is a risk allocation tool, not an opportunity to evade responsibility. Courts enforce reasonable caps that reflect the parties’ relative bargaining power and the nature of the transaction. However, clauses that are unconscionable, hidden, or attempt to limit liability for intentional wrongdoing are routinely struck down.

Types of Liability Caps

Three Common Types of Liability Caps

📊

General Liability Cap

The default cap that applies to most claims under the contract. Most commonly set at 1X (one times) the total fees paid or payable during the preceding 12 months. For a $30,000 annual contract, the cap is $30,000. This covers direct damages unless otherwise excluded.

⬆️

Increased Liability Cap (Super Cap)

A higher cap for specified high-risk categories such as breach of confidentiality, IP infringement, or data security incidents. Typically ranges from 2X to 5X the annual contract value. Continuing the example: 5X = $150,000 cap for confidentiality breaches.

♾️

Unlimited / Uncapped Liability

No monetary limit on certain types of claims. Typically reserved for (a) gross negligence or willful misconduct, (b) fraud, (c) death or personal injury, (d) indemnification obligations for third-party IP claims, or (e) breach of confidentiality. Some jurisdictions prohibit capping certain liabilities as a matter of law.

✨ Negotiation Tip

Vendors typically push for a cap of 1X fees, excluding only direct damages. Customers push for higher caps (3X–5X) and want consequential damages included. A common compromise: general cap of 1X fees for most claims, but a “super cap” of 2X–5X for confidentiality breach, IP infringement, and data breach, with certain liabilities (gross negligence, fraud) uncapped entirely.

What Gets Excluded

Commonly Excluded Types of Damages

📉 Consequential / Indirect Damages

Losses that do not flow directly from the breach but arise as a secondary consequence, lost profits, business interruption, loss of reputation, loss of data, or cost of replacement products. These are the most frequently excluded category.

💰 Punitive / Exemplary Damages

Damages intended to punish the wrongdoer rather than compensate the victim. Most contracts exclude these because they are unpredictable and often not insurable. Many jurisdictions also prohibit punitive damages in contract cases.

📋 Special or Incidental Damages

Damages that are unusual or specific to the particular contract. Often excluded alongside consequential damages. However, the line between direct and consequential damages can be disputed, clear drafting is essential.

🔄 Lost Profits

Often explicitly excluded even when other consequential damages are not listed. Courts sometimes treat lost profits as direct damages if they were reasonably foreseeable, so explicit exclusion is recommended.

Sample Clause Language

Real-World Example: Limitation of Liability Clause

📄 LIMITATION OF LIABILITY (Vendor-Friendly, Standard Form)

EXCEPT FOR (I) BREACH OF CONFIDENTIALITY, (II) INFRINGEMENT OF INTELLECTUAL PROPERTY RIGHTS, (III) INDEMNIFICATION OBLIGATIONS, OR (IV) GROSS NEGLIGENCE OR WILLFUL MISCONDUCT, IN NO EVENT SHALL EITHER PARTY BE LIABLE TO THE OTHER FOR ANY INDIRECT, SPECIAL, INCIDENTAL, CONSEQUENTIAL, OR PUNITIVE DAMAGES, INCLUDING LOST PROFITS OR LOSS OF DATA. EACH PARTY’S TOTAL AGGREGATE LIABILITY FOR ALL CLAIMS ARISING UNDER THIS AGREEMENT SHALL NOT EXCEED THE TOTAL FEES PAID OR PAYABLE TO THE VENDOR UNDER THIS AGREEMENT DURING THE TWELVE (12) MONTHS PRECEDING THE EVENT GIVING RISE TO THE CLAIM.

✨ Drafting Tip

Always define “consequential damages”, ambiguity leads to litigation. Some courts treat lost profits as direct damages if they were within the contemplation of both parties at contracting. To avoid this, explicitly exclude “lost profits” in addition to “consequential damages.” Also, note that “excluded damages” apply to both parties, one-sided exclusions are more likely to be challenged as unconscionable.

Enforceability & Exceptions

When Limitation of Liability Clauses Are Struck Down

Courts generally enforce limitation of liability clauses that are clear, reasonable, and negotiated between sophisticated parties. However, there are well-established exceptions where courts refuse to enforce these clauses:

⚠️

Gross Negligence or Willful Misconduct

Most jurisdictions refuse to enforce a clause that attempts to limit liability for intentional wrongdoing or reckless disregard for safety. Public policy discourages parties from insuring against their own deliberate misconduct.

⚠️

Fraud or Misrepresentation

No court will enforce a liability cap where the breach arises from fraudulent conduct. A party cannot contractually immunise itself from its own fraud.

⚠️

Death or Personal Injury

In many jurisdictions (including under the UK Unfair Contract Terms Act), any clause excluding liability for death or personal injury caused by negligence is void.

⚠️

Unconscionability

A grossly one-sided clause buried in fine print may be deemed unconscionable, especially in consumer contracts or where bargaining power is vastly unequal.

⚠️

Violation of Statute

Some statutes prohibit limiting liability, e.g., certain consumer protection laws, environmental regulations, or employment laws (minimum wage cannot be waived).

LoL vs Indemnification vs Liquidated Damages

Limitation of Liability vs Related Concepts

| Aspect | Limitation of Liability | Indemnification | Liquidated Damages |

|---|

| Purpose倒 | Caps amount of recoverable damages倒 | Transfers risk of third-party claims倒 | Pre-estimates damages for specific breach (e.g., delay)倒 |

| Who pays倒 | Breaching party pays capped amount to counterparty倒 | Indemnifying party pays losses caused to indemnitee by third parties倒 | Breaching party pays fixed amount specified in contract倒 |

| Typical cap倒 | 1X–5X fees or fixed dollar倒 | Often uncapped or subject to super cap倒 | Reasonable estimate, not punitive (otherwise unenforceable as penalty)倒 |

| Third-party claims倒 | Usually does not cover third-party claims (direct losses only)倒 | Specifically designed for third-party claims (lawsuits, regulatory actions)倒 | Direct between parties, not third-party倒 |

| Negotiation leverage倒 | Vendors want low cap; customers want high or no cap倒 | Both parties want indemnity for risks they do not control; limits are negotiated倒 | Both parties want fair estimate; penalty clauses are void倒 |

Jurisdictional Variations

Jurisdictional Considerations

| Jurisdiction | Key Rules |

|---|

| United States (UCC Article 2)倒 | For sale of goods, limitation of consequential damages is prima facie valid unless unconscionable. Limitation of direct damages is also permitted. However, clauses that fail of their essential purpose (e.g., repair/replacement limitation that doesn’t work) may be struck down.倒 |

| England & Wales (UCTA 1977)倒 | Unfair Contract Terms Act imposes reasonableness test. A limitation clause must be fair and reasonable having regard to circumstances known to parties. Cannot exclude liability for death or personal injury caused by negligence. Consumer contracts have additional protections.倒 |

| European Union / Civil Law倒 | Many civil law jurisdictions (Germany, France) have statutory provisions limiting the enforceability of exclusion clauses, especially for gross negligence. Under the Unfair Contract Terms Directive, standard terms that significantly imbalance parties’ rights may be invalid.倒 |

| India倒 | Under Indian Contract Act, limitation clauses are generally enforceable if not unconscionable. However, courts strictly construe exclusion of liability for fraud, willful default, or gross negligence.倒 |

Drafting Best Practices

Best Practices for Drafting Limitation of Liability Clauses

✓ Be Specific

Define “consequential damages” explicitly. List excluded categories (lost profits, loss of data, business interruption). Avoid vague terms like “any indirect losses.”

✓ Set a Clear Cap

Use a formula tied to fees paid (e.g., “total fees paid in preceding 12 months”) or a fixed dollar amount. Ensure the cap is not so low as to be unconscionable (e.g., $100 cap on a $1M contract).

✓ Specify Exceptions

List what is NOT capped: confidentiality breach, IP infringement, indemnity obligations, gross negligence, fraud. Clarity prevents disputes over whether a claim falls under the cap.

✓ Apply Mutually

One-sided limitations (only vendor caps liability) are more likely to be challenged. Apply the same cap and exclusions to both parties unless there is a compelling business reason otherwise.

✓ Consider Insurance

Align the cap with available insurance coverage. There is little point in a $5M cap if professional indemnity insurance is only $1M. Ensure the cap does not create a coverage gap.

✓ Make It Conspicuous

Do not bury the clause in fine print or a dense appendix. Use bold text or all-caps for disclaimers. Many courts require that limitation clauses be brought to the attention of the other party.

FAQ

Frequently Asked Questions

QWhat is the difference between a limitation of liability clause and an indemnification clause?

A limitation of liability clause caps the amount of damages one party can claim from the other for breach or negligence, it limits liability. An indemnification clause requires one party to compensate the other for losses caused by third-party claims, it transfers liability. Indemnities often cover third-party IP claims, bodily injury, or property damage, while limitation of liability caps direct losses between the contracting parties. Many contracts have both: an indemnity for third-party claims (often uncapped or with a super cap) and a limitation of liability for direct claims (capped at 1X fees).

QAre limitation of liability clauses always enforceable?

Generally yes, but enforceability depends on reasonableness, clarity, and jurisdiction. Courts may refuse to enforce a clause that is unconscionable, hidden, or overly one-sided. Most jurisdictions also prohibit limiting liability for gross negligence, willful misconduct, fraud, or death/personal injury caused by negligence. Under the UK Unfair Contract Terms Act, the clause must satisfy a “reasonableness” test. In the US, UCC Article 2 allows limitation of consequential damages unless unconscionable.

QWhat is the most common liability cap amount?

The most common general liability cap in commercial contracts is 1X (one times) the total fees paid or payable under the contract during the preceding 12 months. For example, if annual fees are $50,000, the cap is $50,000. Some contracts use a higher “super cap” of 2X to 5X for specific risks like confidentiality breaches or IP infringement, and certain liabilities may be uncapped for gross negligence or fraud. According to Common Paper data, over 80% of sales contracts use only a general cap, and only 1% have unlimited liability.

QWhat is the difference between direct and consequential damages?

Direct damages are the natural, foreseeable result of a breach, e.g., the cost to repair defective goods, the difference between contract price and cover price. Consequential (indirect) damages are secondary losses that do not flow directly from the breach, e.g., lost profits from production downtime, loss of goodwill, or reputational harm. The distinction is often disputed. To avoid litigation, many contracts explicitly list what is excluded (e.g., “lost profits, loss of data, business interruption”) in addition to using the term “consequential damages.”

QCan a limitation of liability clause be completely one-sided?

Yes, one-sided clauses (only Vendor caps liability; Customer has no cap) are legally possible but risk being struck down as unconscionable or unreasonable, especially if the Customer has little bargaining power. Courts look at the relative sophistication of the parties, whether the clause was negotiated, and whether the cap is commercially reasonable. Best practice is to apply the same cap and exclusions to both parties unless there is a strong business justification for asymmetry (e.g., Customer is an individual consumer).

QWhat is the difference between limitation of liability and liquidated damages?

A limitation of liability clause sets a maximum ceiling on all damages, it does not specify a particular amount for a particular breach. A liquidated damages clause specifies a fixed, pre-agreed amount payable for a specific breach (e.g., $500 per day for delay in completion). Liquidated damages are enforceable if they are a reasonable estimate of probable loss, not a penalty. Limitation of liability caps total exposure; liquidated damages are a specific remedy for specific breaches. A contract can have both, e.g., liquidated damages for delay up to a cap, and a general liability cap for all other claims.