When to Use CIF in International Trade

CIF is appropriate when the seller has direct access to the vessel for loading and the goods are non-containerized (bulk, breakbulk, heavy machinery, or project cargo). It is commonly used with letters of credit because the seller provides a clear invoice covering freight and insurance. The seller quotes a price that includes all costs to bring the goods to the named port of destination, including marine insurance. For containerized freight, however, CIF is not recommended, the ICC advises using FCA, CPT, or CIP instead.

⚡ Key Principle

Under CIF, costs and risk transfer at different points: the seller pays freight and insurance to the destination port, but risk transfers to the buyer once goods are loaded on board the vessel at the origin port. This means the buyer may bear the risk of loss during sea transit even though the seller arranged the transport.

Seller vs. Buyer Obligations

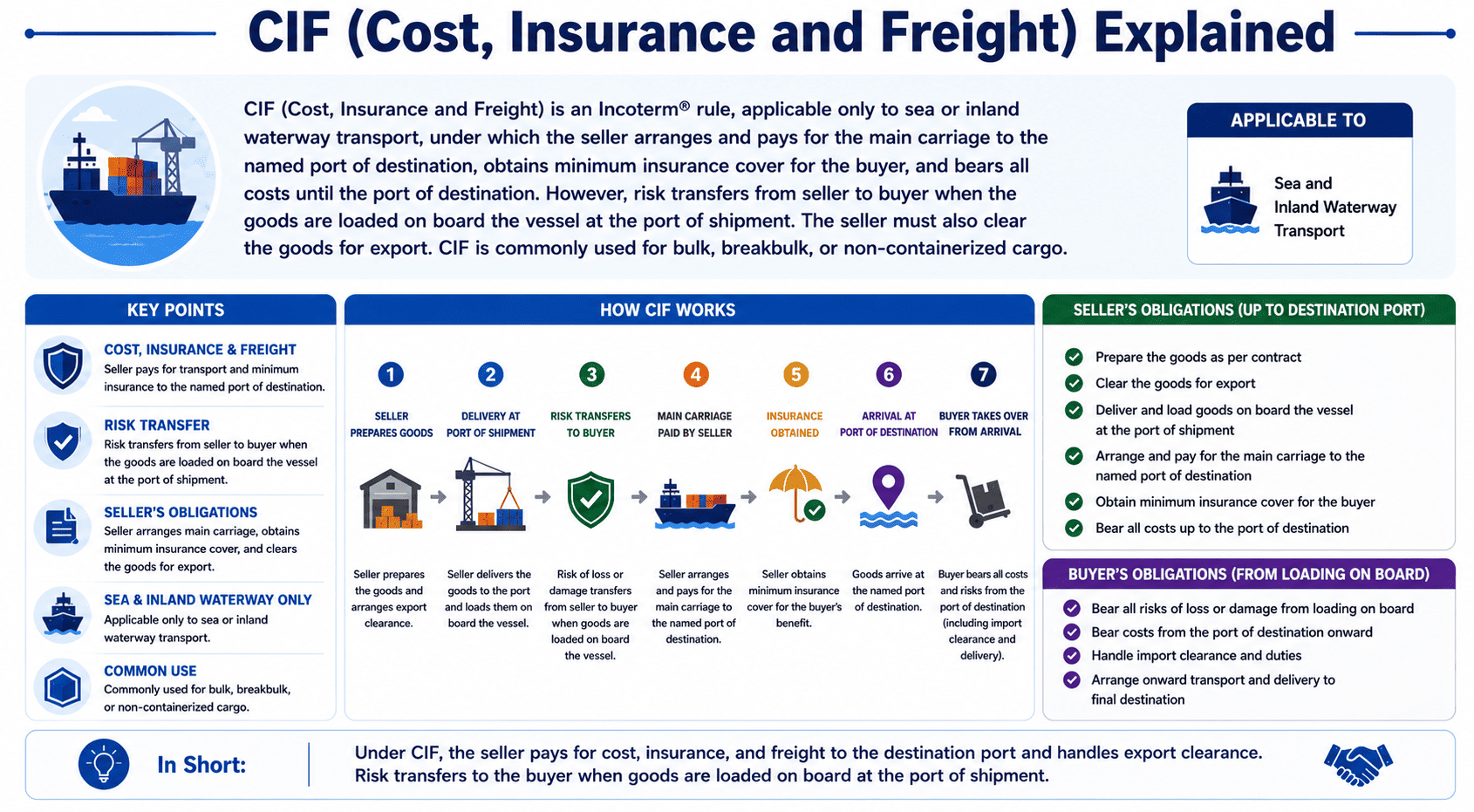

CIF Obligations: Seller and Buyer Responsibilities

📦

Seller’s Obligations

Goods, commercial invoice, and documentation; export packaging and marking; export licenses and customs clearance; pre-carriage to port of shipment; loading charges; main sea freight to named destination port; minimum insurance coverage (ICC Clause C, 110% of invoice value); proof of delivery.

✔️ Cost: Up to destination port (freight + insurance)

✔️ Risk transfers at origin port (on board vessel)

🏭

Buyer’s Obligations

Payment for goods as per contract; discharge and unloading at destination port; import formalities, customs duties, and taxes; inland transport from destination port to final warehouse; any additional insurance beyond minimum coverage (if agreed).

✔️ Risk from loading at origin port onward

✔️ Buyer bears loss during sea transit despite seller arranging insurance

Risk Transfer & Insurance

Risk Transfer and Insurance Under CIF

One of the most misunderstood aspects of CIF is that the seller pays for insurance, but the buyer bears the risk once goods are loaded on board. The seller must purchase minimum cargo insurance (Institute Cargo Clauses C) for 110% of the contract value. However, this is not “all-risks” coverage, it covers major perils (fire, explosion, sinking, collision) but excludes theft, water damage, or general average unless extended.

01

Port of Shipment (Origin)

Seller delivers goods on board the vessel. Risk transfers from seller to buyer at this exact moment. Seller pays for loading, export clearance, and all costs up to this point.

02

Main Carriage (Sea Transit)

Buyer bears the risk of loss or damage during sea transit, but the seller has arranged and paid for minimum insurance cover. In case of loss, buyer must file claim against the seller’s insurance policy.

03

Port of Destination

Seller’s cost obligation ends at the named port of destination. Buyer pays for unloading, import duties, and onward transport to final destination.

✨ Insurance Guidance

If the buyer needs higher protection (e.g., theft, water damage, all-risks coverage), they should either negotiate CIP (which mandates Clause A insurance) or explicitly agree in the sales contract that the seller will obtain broader insurance at the buyer’s cost. Under CIF, the seller is only required to provide minimum cover.

CIF vs FOB vs CIP vs CFR

How CIF Compares to Other Key Incoterms®

| Incoterm® | Mode of Transport | Risk Transfer Point | Freight Paid By | Insurance Obligation |

|---|

| CIF | Sea / inland waterway | On board vessel at origin port | Seller | Seller provides minimum cover (Clause C) |

| FOB | Sea / inland waterway | On board vessel at origin port | Buyer | No obligation (buyer arranges) |

| CIP | Any mode (multimodal) | First carrier at origin | Seller | Seller provides all-risks cover (Clause A) since Incoterms 2020 |

| CFR | Sea / inland waterway | On board vessel at origin port | Seller | No insurance obligation (buyer arranges own insurance) |

| EXW | Any mode | Seller’s premises | Buyer | No obligation |

Common Pitfalls & Misunderstandings

Common Risks and Misunderstandings with CIF

🚩

Using CIF for Containerized Cargo

CIF’s risk transfer point (“on board vessel”) creates a gray area for containers delivered to the terminal days before loading. For containers, use FCA, CPT, or CIP instead. Many traders misuse CIF for containers, leading to unassigned liability for terminal damage.

🚩

Assuming the Seller Bears Sea Risk

Under CIF, the buyer bears the risk of loss or damage during sea transit, even though the seller arranges insurance. If goods are damaged at sea, the buyer must claim against the seller’s policy, but the buyer cannot refuse to pay for the goods if insurance proceeds are insufficient.

🚩

Inadequate Insurance Coverage

Minimum cover (Clause C) excludes many common perils such as theft, pilferage, water damage, or general average. Buyers who assume they are fully protected often face unexpected losses. Negotiate higher coverage (Clause A) if needed.

🚩

Unclear Destination Charges

Unloading, terminal handling, import duties, and local transport are for the buyer’s account. Without a detailed breakdown in the sales contract, disputes arise over who pays for destination port fees.

🚩

Conflict with Local Insurance Requirements

Some countries require importers to purchase insurance from local providers. Using CIF may create conflict or double insurance. In such cases, consider CFR (buyer arranges own insurance).

FAQ

Frequently Asked Questions

QWhat is the difference between CIF and FOB?

Under FOB, the seller is responsible for all costs and risks until goods are loaded onto the vessel at the port of shipment. The buyer arranges and pays for the main sea freight and insurance. Under CIF, the seller arranges and pays for both the main sea freight and minimum insurance to the named port of destination. However, risk transfers at the same point under both rules: when goods are loaded onboard the vessel at the port of shipment. The difference is who pays for freight and insurance.

QWhy is CIF not recommended for containerized cargo?

CIF is not suitable for containers because the risk transfer point is “on board the vessel,” but containers are typically delivered to the terminal days before loading. This creates a “gray area” of responsibility: if cargo inside a container is damaged before loading (e.g., during terminal handling), it is unclear whether the seller or buyer bears the loss. For containerized freight, ICC recommends using FCA (Free Carrier), CPT (Carriage Paid To), or CIP (Carriage and Insurance Paid To) instead, as risk transfers when the goods are handed to the first carrier at the terminal.

QWhat insurance coverage is required under CIF?

Under CIF Incoterms 2020, the seller must obtain minimum insurance coverage, typically Institute Cargo Clauses (C), for 110% of the contract value. This covers major perils such as fire, explosion, sinking, capsizing, collision, and jettison. It does NOT cover theft, pilferage, water damage (except from ship sinking), breakage, or general average unless specifically extended. If the buyer requires higher protection (e.g., Institute Cargo Clauses A “all-risks”), this must be explicitly agreed in the sales contract, with the buyer paying any additional premium.

QIs CIF only for ocean freight?

Yes, CIF is strictly for sea or inland waterway transport only. It cannot be used for air, road, or rail freight. For multimodal transport (truck + ship + rail), use CIP (Carriage and Insurance Paid To), which is designed for any mode or combination of modes. Using CIF for air freight is incorrect and may void insurance coverage.

QWho pays for unloading at the destination port under CIF?

The buyer pays for unloading (discharging) the goods at the named port of destination, unless otherwise agreed in the contract of carriage. The seller’s cost obligation ends when the goods are delivered on board the vessel at the origin port for the main carriage to the destination port. Terminal handling charges, port fees, and demurrage at destination are typically for the buyer’s account.