How to Expand Your Manufacturing & Industrial Automation Business to Taiwan

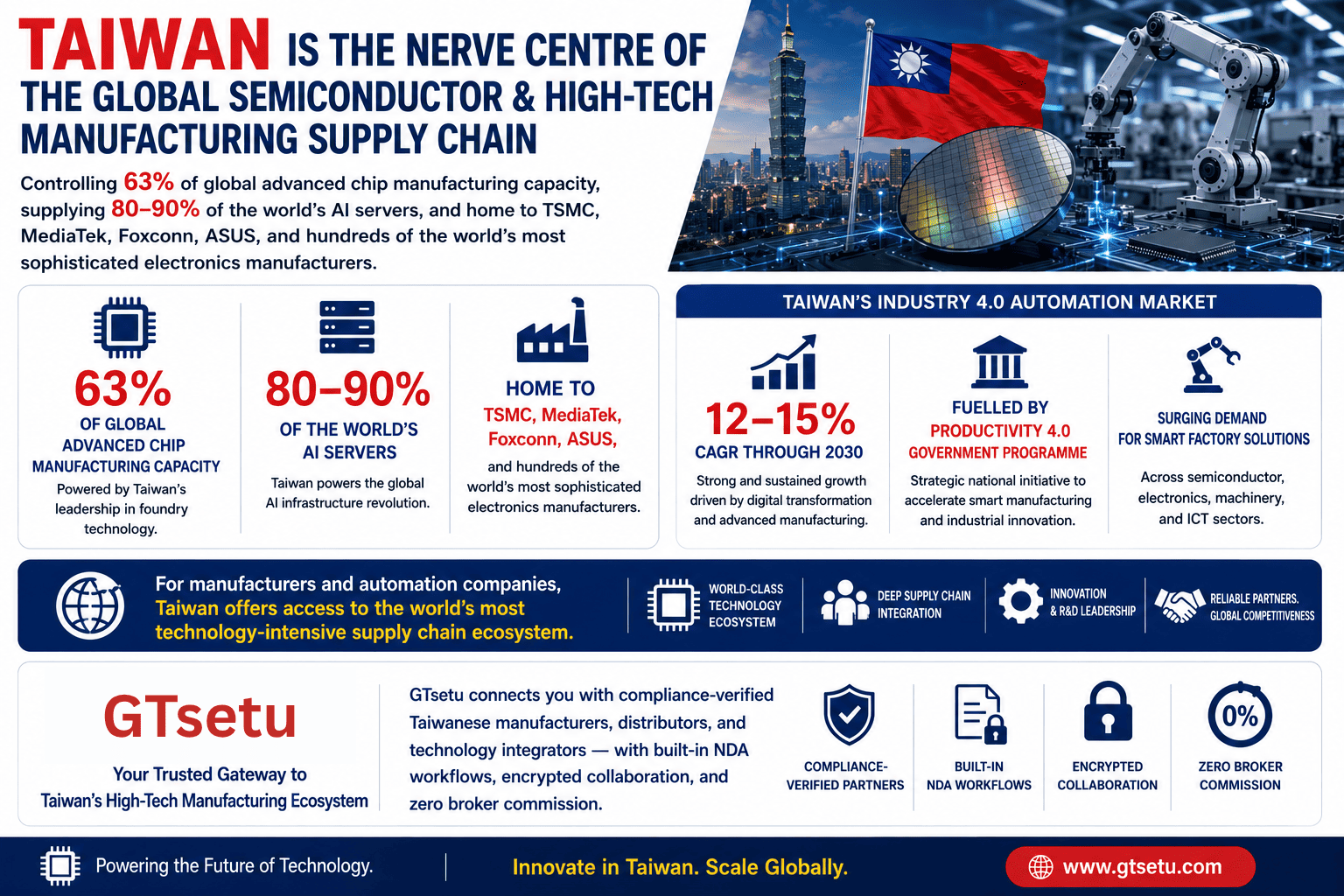

Direct Answer: Taiwan is the nerve centre of the global semiconductor and high-tech manufacturing supply chain, controlling 63% of global advanced chip manufacturing capacity, supplying 80–90% of the world’s AI servers, and home to TSMC, MediaTek, Foxconn, ASUS, and hundreds of the world’s most sophisticated electronics manufacturers. Taiwan’s Industry 4.0 Automation Market is growing at 12–15% CAGR through 2030, fuelled by the Productivity 4.0 government programme and surging demand for smart factory solutions across semiconductor, electronics, machinery, and ICT sectors. For manufacturers and automation companies, Taiwan offers access to the world’s most technology-intensive supply chain ecosystem. GTsetu connects you with compliance-verified Taiwanese manufacturers, distributors, and technology integrators, with built-in NDA workflows, encrypted collaboration, and zero broker commission.

📅 June 2026⏱ 17 min read✍️ GT Setu Editorial Team🔄 Updated regularly

63%

Global Advanced Chip Capacity

12–15%

Industry 4.0 Automation CAGR

$41.3B

Semicon Equipment Market 2030

80–90%

Global AI Server Supply Share

🌏 Also Explore: Expand to Other Global Manufacturing Markets

Taiwan is not simply a manufacturing destination, it is the foundational layer of the global technology supply chain. When TSMC produces a chip, it uses equipment from ASML (Netherlands), KLA (USA), Tokyo Electron (Japan), and hundreds of specialised Taiwanese suppliers. When that chip is packaged, tested, and assembled into a server by Foxconn, Quanta, or Wistron, it passes through a manufacturing ecosystem of extraordinary precision, density, and technological sophistication that no other geography replicates. For manufacturers and industrial automation companies, this means Taiwan represents the world’s single most concentrated market for high-precision manufacturing automation, where the customers are globally dominant companies competing on nanometre-scale process technology, and where the tolerance for anything less than best-in-class automation solutions is zero.

Beyond semiconductors, Taiwan’s broader manufacturing base, precision machinery, ICT equipment, bicycles, medical devices, specialty chemicals, is undergoing a rapid Industry 4.0 transformation driven by the government’s Productivity 4.0 programme, a pressing demographic challenge (ageing workforce, low birth rate), and competitive pressure from lower-cost Asian manufacturers. This guide covers everything required to understand and act on the Taiwan expansion opportunity across the full spectrum of manufacturing and automation.

🇹🇼 Taiwan at a Glance

Official name: Republic of China (Taiwan). Population: approx. 23.5 million. Capital: Taipei. Currency: New Taiwan Dollar (TWD/NTD). GDP: approx. USD 760 billion (2024, one of Asia’s highest per-capita GDPs). Manufacturing share of GDP: ~34%. Key industries: semiconductors (TSMC, UMC, ASE), ICT and electronics (Foxconn, ASUS, Acer, MSI), precision machinery, bicycles, chemicals, medical devices. Primary trading partners: USA, China (despite geopolitical tensions), Japan, Singapore, South Korea, Hong Kong, Netherlands.

SECTION 1

1 Why Taiwan for Manufacturing & Automation?

Taiwan’s case as a manufacturing expansion destination rests on a foundation that no other market in Asia, and arguably the world, replicates: the combination of globally dominant semiconductor and electronics manufacturing, world-class precision machinery, a deeply embedded culture of engineering excellence, and a government that has consistently invested in supporting both domestic industrial upgrading and foreign technology partnership.

$27.9B

Taiwan semiconductor equipment investment in 2025, nearly 70% year-on-year growth

65%

Combined market share of TSMC, MediaTek, Realtek, Novatek, Delta Electronics in Taiwan industrial control

NT$45.6B

Government Industry 4.0 automation funding through NTD 45.6 billion investment commitment

The Six Strategic Drivers for Taiwan Expansion

Driver

What It Means for Manufacturers & Automation Companies

Commercial Implication

Global Semiconductor Dominance

Taiwan controls 63% of global advanced chip manufacturing (7nm and below) through TSMC; 24% of global semiconductor equipment revenue flows through Taiwan; every fab expansion requires new automation infrastructure

Taiwan supplies 80–90% of the world’s AI servers through Foxconn, Quanta, Wistron, and Inventec; TSMC’s 2nm production (beginning 2H 2025) commands the most advanced process technology commercially available

AI server manufacturing requires ultraprecise automated assembly, AOI inspection, thermal management automation, and IIoT-connected quality systems, all premium automation market segments

Productivity 4.0 / Industry 4.0 Programme

Taiwan’s government programme provides NTD 45.6 billion in funding for smart factory adoption, AI integration, and industrial automation upgrades, primarily targeting precision machinery, food processing, textile, and metal fabrication SMEs

Government subsidies reduce the cost barrier for SME automation adoption, expanding the addressable market for automation solution providers beyond Tier-1 electronics to Taiwan’s 150,000+ SME manufacturers

Precision Machinery Excellence

Taiwan’s Taichung region is Asia’s largest precision machinery manufacturing cluster, CNC machine tools, industrial robots, servo drives, and automation components manufactured here supply global OEMs

Both a customer base (machinery manufacturers upgrading their own production with smart factory solutions) and a supply chain partner base (sourcing precision components for integration into automation systems)

Diversification Beyond China

US-China trade tensions and the CHIPS Act are accelerating investment in Taiwan as a supply chain anchor, with US companies investing directly in Taiwanese manufacturing partnerships and supplier development

New foreign investment in Taiwan manufacturing creates demand for automation from companies establishing operations as alternatives or complements to China-based production

Strong IPR Framework

Taiwan has one of Asia’s strongest intellectual property protection frameworks, ranked consistently high by the International Property Rights Index, making technology partnership and licensing arrangements lower-risk than in many Asian markets

Automation technology companies can enter Taiwan via licensing or technology transfer with greater IP protection confidence than most Asia-Pacific alternatives. See: technology transfer agreements

💡 Taiwan’s India Deepening Manufacturing Synergies

Taiwan and India are deepening their manufacturing collaboration across semiconductor supply chains, precision electronics, and advanced manufacturing technologies. Taiwanese companies are increasingly establishing production and sourcing partnerships in India, while Indian manufacturers are engaging Taiwan for technology and automation expertise. For companies with operations or expansion plans in both markets, this bilateral strengthening creates supply chain integration opportunities. See our guide to expanding manufacturing to India for the complementary perspective.

SECTION 2

2 Market Overview: Semiconductor, Electronics & Industry 4.0

Taiwan’s industrial automation opportunity operates across two distinct but deeply interconnected layers: the semiconductor and advanced electronics manufacturing ecosystem (the world’s most technology-intensive automation market by value), and the broader Taiwan manufacturing base (machinery, food processing, textiles, chemicals) undergoing systematic Industry 4.0 transformation.

Market Metric

Value

Period / Source

Taiwan Semiconductor Manufacturing Equipment

USD 24.7 billion

2023 (Grand View Research)

Taiwan Semicon Equipment by 2030

USD 41.3 billion

7.6–7.7% CAGR to 2030, world’s largest single-country market

Taiwan Semiconductor Equipment Investment

USD 27.9 billion in 2025

~70% year-on-year growth (TechSoda)

Taiwan Industrial Process Automation

USD 157.7 million (2024) → USD 181.6 million (2030)

2.38% CAGR (Next Move Strategy Consulting)

Taiwan Industry 4.0 Automation Market

12–15% CAGR

2024–2030 (Mobility Foresights)

Taiwan Semiconductor Market

USD 35.55 billion (2025)

7.85% CAGR to 2030 (Mordor Intelligence)

Factory Automation Industrial Control Chips

38% market share by application

AI-enabled control chips fastest at 23% CAGR (Intel Market Research)

R&D Investment in Industrial Automation

USD 78.5 million

Annual smart manufacturing solutions R&D (Taiwan industry data)

Taiwan ICT Market

USD 22.5 billion (2025) → USD 32.4 billion (2030)

7.6% CAGR, Industry 4.0 middleware and edge computing growth

The Productivity 4.0 / Industry 4.0 Transformation

🏛️

Government-Backed Industry 4.0 Strategy

Taiwan’s Productivity 4.0 and Smart Machinery Development Programme are the government’s structured responses to two existential pressures: an ageing and shrinking workforce, and competitive erosion from lower-cost Asian manufacturers. NTD 45.6 billion in government funding supports smart factory adoption, AI integration, and industrial automation across machinery, electronics, food processing, textiles, and metal fabrication. This funding directly subsidises the adoption of automation systems that foreign companies supply.

Policy Driver

🤖

Semiconductor Fab Expansion Cycle

TSMC’s 2nm commercial production (beginning 2H 2025) and ongoing 3nm expansion represent the largest single-site industrial capex cycle in global manufacturing history. Each new TSMC fab requires billions of dollars of automation equipment, automated material handling systems (AMHS), cleanroom robotics, wafer handling systems, automated optical inspection (AOI), and metrology tools. The supplier ecosystem around TSMC at Hsinchu and Tainan creates cascading demand through the supply chain.

Capital Expenditure

🔗

SME Automation Adoption Wave

Taiwan has approximately 150,000 SME manufacturers, predominantly in precision machinery (Taichung cluster), electronics components (Tainan and Hsinchu), and traditional manufacturing (textiles, footwear, food processing). The Productivity 4.0 subsidy programme, combined with rising labour costs and workforce aging, is driving an SME automation adoption wave that represents the largest volume opportunity for industrial automation companies, even if individual contract values are smaller than semiconductor fab deals.

SME Volume

🌐

AI-Integrated Manufacturing

AI and ML algorithms are being embedded in automation systems at Taiwan manufacturers with notable speed, enabling predictive analytics, anomaly detection, and adaptive control. Factory automation control chips with AI capability are growing at 23% CAGR. Collaborative robots (cobots) adoption is expanding rapidly among Taiwan SMEs. The integration of edge computing, digital twins, and AI-driven quality inspection represents the premium growth segment of Taiwan’s automation market through 2030.

AI + Automation

SECTION 3

3 Top Sectors: Where Automation Demand Is Highest

Taiwan’s industrial automation opportunity is concentrated across eight sectors that together span the country’s manufacturing breadth, from the world’s most advanced chip fabs to the bicycle manufacturing capital of the world.

💾

Semiconductors & IC Manufacturing

World’s #1 market, USD 41.3B equipment market by 2030

Taiwan’s semiconductor manufacturing ecosystem, TSMC, UMC, Powerchip, GlobalWafers, ASE Group, and hundreds of suppliers, represents the most intensive automation deployment environment in global manufacturing. Every new fab, every process node transition, every capacity expansion triggers immediate demand for AMHS, cleanroom robotics, wafer handling, photolithography automation, metrology integration, and fab-wide IIoT monitoring systems.

80–90% global AI server supply; massive assembly automation demand

Foxconn, Quanta, Wistron, Inventec, Compal, and Pegatron, Taiwan’s ODM giants, manufacture the world’s servers, laptops, smartphones, and networking equipment. AI server assembly, with its massive GPU modules and complex thermal management, is driving new waves of automation investment in automated assembly, testing, burn-in automation, and AI-driven quality inspection. SMT automation, X-ray inspection, and functional test systems are priority segments.

SMT AutomationAI Server AssemblyX-ray InspectionFunctional Test

⚙️

Precision Machinery & Machine Tools

Asia’s largest precision machinery cluster, Taichung hub

Taichung is Asia’s most concentrated precision machinery manufacturing region, CNC machine tool builders, servo motor and drive manufacturers, grinding machines, and industrial robot components. Companies like Hiwin, TBI Motion, TECO Electric, and hundreds of precision component OEMs are core customers for both IIoT-enabled smart factory upgrades and for sourcing precision automation components. This dual-sided market makes Taichung the most commercially versatile region for automation companies entering Taiwan.

Taiwan dominates global production of networking equipment, enterprise routers, wireless access points, and data centre hardware, supplied by D-Link, Zyxel, Advantech, and the vast ODM ecosystem. ICT equipment manufacturing requires precision PCB assembly automation, automated testing, packaging automation, and quality control systems. The 5G equipment manufacturing wave is adding a new layer of precision automation investment through 2028.

PCB Assembly5G Equipment ManufacturingAutomated TestingQuality Systems

🚗

Automotive & EV Components

GaN and SiC power semiconductor growth driving new automation

While Taiwan does not have a domestic automotive OEM, it is a critical supplier of automotive electronics, semiconductor components (particularly power semiconductors, GaN and SiC for EV powertrain applications), cameras, LIDAR systems, and cockpit electronics. Delta Electronics’ NT$3.2 billion investment in GaN-based power chips is part of a broader EV component manufacturing expansion that requires precision assembly and testing automation.

Power Semiconductor AssemblyGaN/SiC ManufacturingAutomotive ElectronicsLIDAR Production

Taiwan’s medical device and biotech manufacturing sectors are experiencing strong growth, supported by government biomedical investment programmes and an ageing domestic and regional population. ISO 13485-compliant manufacturing automation, cleanroom assembly, automated inspection, traceability systems, and environmental monitoring, is a growing demand segment among Taiwan’s medical device OEMs exporting to North America, Europe, and Japan.

Solar, wind, battery, Taiwan’s new export manufacturing frontier

Taiwan is building a significant green energy manufacturing base, solar panel production (the country once led global solar manufacturing), offshore wind turbine components (Yilan and Changhua wind parks), and EV battery modules. Taiwan’s precision manufacturing heritage gives it a strong foundation for high-efficiency solar cell and battery module manufacturing automation. The government’s 2050 net-zero commitment is accelerating domestic renewable energy manufacturing investment.

Solar Cell AutomationBattery Module AssemblyWind Component ManufacturingQuality Control

Taiwan has a number of globally dominant niche manufacturing sectors: bicycle manufacturing (Giant, Merida, Taiwan produces ~40% of the world’s high-end bicycles), precision optical instruments (Largan Precision, dominant global mobile phone lens manufacturer), and specialty chemicals. These sectors are pursuing smart factory upgrades under the Productivity 4.0 programme, creating targeted automation opportunities in precision assembly, quality control, and logistics automation.

Taiwan’s science parks and industrial zones are the physical infrastructure of its technology manufacturing ecosystem. Understanding the geographic specialisation of each zone is essential for customer proximity, supply chain access, and talent availability.

💾

Hsinchu Science Park (HSP), Semiconductor & ICT Capital

Best for: Semiconductors, IC design, precision equipment, automation solution providers. Hsinchu Science Park is the geographic heart of Taiwan’s semiconductor industry, home to TSMC (headquarters and major fabs), UMC, Winbond, and over 500 technology companies. The Industrial Technology Research Institute (ITRI), Taiwan’s primary applied R&D organisation, is located adjacent to the park. For automation companies, Hsinchu is the most commercially critical location in Taiwan, proximity to TSMC and its supply chain is the single most valuable geographic attribute for semiconductor automation providers.

Semiconductor Hub

🔬

Tainan Science Park (TNSP), 2nm Advanced Manufacturing

Best for: Advanced semiconductor manufacturing, photovoltaics, biotechnology. Tainan Science Park hosts TSMC’s most advanced fab complex, including the 2nm and 3nm production sites, as well as major OSAT operations. The park’s rapid expansion since 2020 has made it the fastest-growing science park in Taiwan by investment value. Automation companies serving TSMC’s advanced node fabs must have presence or representation in the Tainan region. The park also hosts significant solar panel manufacturing and biotech operations.

2nm & 3nm Fabs

⚙️

Central Taiwan Science Park (CTSP), Taichung Precision Machinery

Best for: Precision machinery, optoelectronics, semiconductor equipment, smart manufacturing. Taichung and the Central Taiwan Science Park represent Taiwan’s precision manufacturing heartland. The region hosts Asia’s densest concentration of CNC machine tool builders and precision component manufacturers, Hiwin Technologies, THK-Hiwin, Buffalo Machinery, and hundreds of machinery OEMs. For automation companies, the CTSP dual role as both a customer base (machinery OEMs upgrading their own production) and a component supply base makes it uniquely commercially valuable.

Precision Machinery

☀️

Kaohsiung Science Park, Compound Semiconductors & Green Energy

Best for: Compound semiconductors (GaN, SiC, InP), solar energy, advanced materials, shipbuilding technology. Kaohsiung, Taiwan’s second-largest city and primary port, is home to the Kaohsiung Science Park focusing on compound semiconductor manufacturing and green energy technology. The Southern Taiwan Science Park and Kaohsiung Industrial Parks host heavy manufacturing, petrochemicals, and aerospace component production. Southern Taiwan is also a growing hub for offshore wind turbine component manufacturing.

Compound Semiconductors

🖥️

Taipei & New Taipei City, ICT, Design & Corporate Headquarters

Best for: ICT companies, technology service providers, corporate headquarters, R&D, sales and marketing operations. Greater Taipei is home to the headquarters of ASUS, Acer, MSI, D-Link, Zyxel, Advantech, and most of Taiwan’s major ICT brands. For automation companies establishing a Taiwanese corporate entity, Taipei provides the best access to decision-makers at major ICT OEMs and system integrators. The Neihu Technology Park in Taipei is a dense concentration of technology company offices.

ICT Headquarters

🚲

Changhua & Yunlin, Traditional Manufacturing & SME Clusters

Best for: Bicycle manufacturing, food processing, metal fabrication, textiles, SME Productivity 4.0 upgrade market. Changhua County is home to Giant and Merida’s major production facilities and an extensive bicycle component SME ecosystem. The region and adjacent Yunlin County represent the traditional manufacturing base that is the primary target of Taiwan’s Productivity 4.0 SME automation subsidy programme, creating structured demand for entry-level smart factory solutions, collaborative robots, and basic IIoT monitoring systems.

SME & Bicycle

✅ InvesTaiwan Service Centre

The InvesTaiwan Service Centre (operated by the Industrial Development Administration, Ministry of Economic Affairs) is Taiwan’s official one-stop service for foreign manufacturing investors. They provide free guidance on investment regulations, land and facility selection in science parks and industrial zones, government incentive eligibility, and connections to relevant government agencies and industry associations. Contacting InvesTaiwan at the market research stage, before any commitment, significantly accelerates regulatory navigation. Contact: investtaiwan.nat.gov.tw

SECTION 5

5 Investment Incentives & Government Programmes

Taiwan’s investment incentive framework has evolved to prioritise high-value technology and manufacturing investment, with specific programmes targeting Industry 4.0 adoption, semiconductor ecosystem development, and strategic industry reshoring.

Incentive / Programme

Details

Eligibility

Corporate Income Tax Reduction

Standard corporate tax rate 20%; qualifying investments in specific sectors and science parks may receive accelerated depreciation and tax credit for R&D and equipment investment

Manufacturing companies; enhanced benefits for investments in strategic sectors (semiconductors, aerospace, defence, AI, biotech)

Science Park Benefits

Simplified import/export procedures; tax incentives; streamlined land acquisition; infrastructure pre-built; talent connection support; one-stop regulatory service

Companies establishing operations within designated science parks (Hsinchu, Tainan, Central Taiwan, Kaohsiung, Yilan, Chiayi)

Smart Machinery Development Programme

NTD 45.6 billion government funding for machinery manufacturers and SMEs adopting smart manufacturing technologies including IIoT, AI, robotics, and digital twins

Taiwan-registered manufacturers; primarily targets machinery, precision equipment, food processing, textiles, and metal fabrication SMEs

Productivity 4.0 Initiative

Cross-ministry programme providing subsidies, demonstration projects, training, and technical support for smart factory adoption. Connects Taiwanese manufacturers with global technology providers

SME manufacturers in qualifying sectors; government matching funds available for pilot smart factory deployments

R&D Investment Tax Credit

15–35% tax credit on qualifying R&D expenditure; additional 10% credit for expenditures exceeding prior year R&D spending

Companies conducting qualifying R&D in Taiwan; enhanced rate for technology companies meeting MOEA criteria

Reshoring Investment Programme

Facilitation of Taiwanese-origin companies returning production from China to Taiwan; fast-track regulatory approval; prioritised science park allocation

Taiwanese-owned or -origin companies; foreign companies with significant Taiwanese supply chain relationships may also qualify for facilitation support

ITRI Technology Collaboration

Industrial Technology Research Institute provides applied R&D partnership opportunities, technology licensing, and pilot deployment support for foreign technology companies entering Taiwan

Foreign technology companies in qualifying sectors (semiconductor, green energy, AI, advanced manufacturing); technology must have clear commercial application for Taiwan’s industrial base

SECTION 6

6 Market Entry Modes

Taiwan’s open investment framework and strong rule of law make it one of the most accessible Asian markets for foreign technology and manufacturing companies. The right entry mode depends on your commercial ambitions, product category, and relationship with the Taiwanese industrial ecosystem.

🏭

Wholly-Owned Subsidiary

100% foreign ownership is permitted in most manufacturing and technology sectors under Taiwan’s liberalised FDI framework. Foreign-invested enterprises are established as a Limited Company (有限公司) or a Company Limited by Shares (股份有限公司). Full ownership provides maximum control over operations, IP, and customer relationships, and is the standard structure for major technology companies entering Taiwan. Minimum capital requirements vary by sector.

Full Control / Capital Requirement

🤝

Joint Venture with Taiwanese Partner

Partnership with a Taiwanese company, sharing ownership and operations. Particularly valuable for accessing government procurement, OEM qualified vendor lists (QVL), and the deeply relationship-driven Taiwanese electronics supply chain. For technology companies without existing Taiwan market relationships, a JV with an established Taiwanese systems integrator or distributor provides immediate commercial credibility. See: joint venture vs strategic alliance.

Shared Control / Market Access

🏢

Representative / Liaison Office

A representative office can conduct market research, relationship development, and commercial liaison activities but cannot sign contracts, generate revenue, or hire employees directly in Taiwan. Useful for the initial 6–12 months of market assessment and customer relationship development before committing to full entity establishment. Straightforward to set up; no minimum capital requirement.

Low Cost / Market Testing

🚚

Distribution Partnership

For automation equipment and solution companies: appoint a verified Taiwanese distributor, systems integrator, or value-added reseller (VAR) to sell your products to Taiwanese manufacturers. The fastest route to Taiwan market revenue without entity establishment. Critical requirement: the distributor must have existing relationships with your target customers (e.g., TSMC supply chain access for semiconductor automation). GTsetu provides pre-verified Taiwanese partners. See: distribution agreement guide.

Fastest Revenue / Zero Capex

🔬

Technology Licensing / ITRI Partnership

License your automation technology or manufacturing process to a Taiwanese manufacturer or research institution under a formal technology transfer agreement. ITRI collaboration is a particularly attractive route, ITRI serves as an intermediary that validates foreign technology, runs pilot programmes, and connects proven solutions to Taiwanese industrial customers. Taiwan’s strong IPR framework makes licensing lower-risk than in most Asian markets.

IP-Based Revenue

📋

Contract Manufacturing or OEM Partnership

Engage a Taiwanese contract manufacturer (OEM or ODM) to manufacture your products using Taiwan’s precision manufacturing capabilities, accessing the supply chain quality, capacity, and expertise concentrated in Hsinchu, Taichung, and Tainan. Particularly attractive for precision automation component manufacturers wanting Taiwan-made product credentials for high-tech OEM customers. See: OEM vs ODM vs EMS.

Taiwan Manufacturing Quality

💡 The Distribution Partnership First Principle

For most automation equipment and solution companies entering Taiwan, the correct first step is a qualified distribution partnership, not direct entity establishment. The reason: Taiwan’s manufacturing supply chains are relationship-intensive. A distributor with an established relationship with TSMC, Foxconn, or a major Taichung machinery OEM can open doors in days that a newly established foreign entity would take years to access independently. GTsetu’s verified Taiwanese partner network provides exactly this, pre-verified distributors and systems integrators with confirmed sector credentials and market relationships.

SECTION 7

7 Regulatory Framework: Setting Up in Taiwan

Taiwan has a well-developed, transparent regulatory framework for foreign business investment, consistently ranked among the easier Asian markets for business establishment by the World Bank. However, specific requirements and approval processes must be navigated correctly.

Regulatory Requirement

Description

Timeline

Key Consideration

Foreign Investment Approval (FIA)

Most manufacturing and technology sector investments are approved under the Investment Commission (Ministry of Economic Affairs) framework. Most sectors open to 100% foreign ownership; a negative list specifies restricted sectors

2–4 weeks for standard approvals

Restricted sectors include certain media, utilities, and national security-sensitive industries; virtually all manufacturing and automation categories are fully open to foreign ownership

Company Registration

Register with the Ministry of Economic Affairs Company Registry. Choose between Limited Company (有限公司, simpler governance) or Company Limited by Shares (股份有限公司, for larger or public investments)

1–2 weeks after FIA approval

A Taiwanese address is required; engage a local registered agent or law firm for the registration process. At least one director can be a foreign national

Tax Registration

Register with the National Taxation Bureau for corporate income tax (20% standard), business tax (VAT equivalent, 5% standard), and withholding tax purposes

Concurrent with company registration

Taiwan’s tax system is relatively straightforward; engage a Taiwan CPA firm for initial setup and ongoing compliance

Science Park Application (if applicable)

Apply to the Science Park Administration for tenancy in the relevant science park. Application includes business plan review, technology assessment, and facility allocation

4–8 weeks

Science parks have competitive allocation processes; demonstrating technology quality and commercial substance is important for applications. ITRI endorsement can strengthen applications for technology companies

Import Licences & Product Compliance

Automation equipment imports may require product compliance with CNS (Chinese National Standards), BSMI (Bureau of Standards, Metrology and Inspection) certification for electrical equipment, and sector-specific approvals

4–12 weeks depending on product category

Many international standards (IEC, CE) are recognised or accepted with additional BSMI testing; engage a Taiwan product compliance consultant for the specific certification pathway for your product categories

Labour Regulations

Taiwan’s Labour Standards Act governs employment, working hours (40-hour standard week), overtime limits, annual leave, and mandatory severance provisions. Labour insurance and National Health Insurance contributions are mandatory for all employees

Ongoing compliance

Foreign nationals require Alien Resident Certificates and work permits (except for certain executive roles). Taiwan’s strong employee protections make HR planning important for manufacturing operations

SECTION 8

8 Challenges & How to Mitigate Them

Challenge

Specifics for Automation Companies

Mitigation Strategy

Geopolitical Risk

Taiwan’s geopolitical situation, particularly cross-strait relations with China, creates a risk category that must be assessed and managed. Most global companies with Taiwan operations have contingency planning frameworks in place

Assess and document geopolitical risk as part of Board-level investment approval; structure Taiwan operations with operational resilience (cloud-based systems, process documentation that enables rapid transfer if needed); consult specialist geopolitical risk advisers; note that operational disruption from this risk remains low historically

Relationship-Intensive Sales Cycles

Taiwan’s manufacturing supply chains, particularly at TSMC, major ODMs, and Tier-1 electronics OEMs, operate through deeply established supplier relationships and approved vendor lists. Cold approaches rarely succeed; relationship-driven introductions are the norm

Partner with a Taiwanese systems integrator or distributor who already has qualified vendor status with your target customers; attend Taiwan trade events (Computex, TPCA Show, Smart Manufacturing Expo); engage ITRI as a technology validator and customer introduction vehicle; build relationships with Taiwan-based industry associations

Labour Shortage

Taiwan faces acute skilled labour shortages, particularly in semiconductor-related roles (process engineers, equipment engineers, automation specialists). Competition with TSMC for engineering talent is commercially intense

Locate in regions with stronger talent supply (university proximity in Hsinchu, Tainan, Taichung); partner with Taiwan universities (NTHU, NCKU, NTUST) for talent pipeline; offer competitive compensation benchmarked against TSMC; consider remote work arrangements for roles that do not require on-site presence

High Competition from Established Players

Every major global automation company, ASML, KLA, Tokyo Electron, Applied Materials, Siemens, ABB, Fanuc, has a significant and long-established presence in Taiwan. New entrants compete against deeply embedded incumbents with decades of customer relationships

Focus on specific niches or emerging segments (AI-enhanced quality inspection, cobot deployment for SMEs, green energy manufacturing automation) where incumbent relationships are weaker; use technology differentiation rather than price competition; ITRI technology validation can establish credibility against established players

Water and Energy Constraints

Identified as principal headwinds for Taiwan’s semiconductor industry expansion, water-intensive chip fabrication processes and power grid capacity are structural constraints on continued fab expansion

For automation companies, this creates a specific opportunity: water recycling automation, energy monitoring systems, and power management automation are becoming priority investments for Taiwan manufacturers, align product positioning to address these operational constraints

IP Protection (Specific Contexts)

While Taiwan has a strong general IPR framework, technology-intensive relationships in semiconductor manufacturing require careful management of trade secrets, particularly when engaging with Taiwanese manufacturers who may supply to or compete with your customers elsewhere

Execute robust mutual NDAs before any technical sharing; use GTsetu’s encrypted document exchange for pre-commercial IP protection; clearly delineate what technology is licensed vs. retained in any JV or partnership arrangement; see: IP ownership

SECTION 9

9 Step-by-Step Expansion Process

01

Market Assessment & Customer Targeting

Define precisely which segment of Taiwan’s manufacturing ecosystem represents your primary commercial opportunity: Is it semiconductor fab automation (Hsinchu / Tainan, TSMC supply chain)? Precision machinery smart factory upgrades (Taichung / CTSP)? ICT electronics assembly automation (Greater Taipei / Northern Taiwan)? SME Productivity 4.0 adoption (Changhua / Yunlin)? Each requires different entry vectors, partner profiles, and commercial strategies. Map the competitive landscape: identify current equipment or solution providers at your target customers, this determines whether you are displacing incumbents or entering new territory. Related: global expansion analysis.

02

ITRI and Industry Association Engagement

Before any commercial engagement, engage ITRI (Industrial Technology Research Institute) for technology validation and initial customer introduction. ITRI’s credibility endorsement with Taiwan’s manufacturing community is a significant commercial accelerator for foreign technology companies. Simultaneously, join relevant Taiwan industry associations, Taiwan Automation Intelligence and Robot Association (TAIROA), Taiwan Electrical and Electronic Manufacturers’ Association (TEEMA), or the Taiwan Machine Tool and Accessory Builders’ Association (TMBA), for market intelligence, trade event access, and peer introductions. This is particularly important for establishing commercial credibility before your first customer meetings.

03

Verified Partner Discovery

Identify and verify your Taiwanese distribution or integration partner before any commercial commitment. Use GTsetu’s compliance-verified platform to browse pre-vetted Taiwanese companies by sector and capability. Anonymous discovery protects your market entry strategy. Execute a mutual NDA before sharing product specifications, pricing, or commercial strategies. Assess the partner’s specific customer relationships, a distributor claiming “semiconductor sector experience” should be able to name their current vendor accounts in that segment. See: business verification and partnership evaluation criteria.

04

Product Compliance and Certification

Initiate Taiwan-specific product compliance concurrently with partner development: BSMI (Bureau of Standards, Metrology and Inspection) certification for electrical and electronic products; CNS standard conformity for relevant product categories; QVL (Qualified Vendor List) application processes for any products targeting TSMC, major ODMs, or government procurement. BSMI certification can take 4–12 weeks, begin this process as early as possible to avoid commercial delays once your partner is engaged and customer interest is confirmed. Many IEC and CE certifications are partially recognised, reducing but not eliminating local testing requirements.

05

Pilot Programme Execution

Taiwan’s manufacturing customers, particularly in semiconductors and electronics, strongly prefer pilot programmes before full deployment commitments. A successful pilot at one facility generates referenceability that is disproportionately valuable for expanding to other customers in Taiwan’s closely networked manufacturing community. Prioritise executing a pilot with your first customer, even at reduced margin, to establish the reference case. ITRI can facilitate pilot programmes through its demonstration factory infrastructure, which can substitute for a direct customer pilot in early market development stages.

06

Entity Establishment and Commercial Agreements

Once revenue generation and customer traction confirm the market opportunity, establish your Taiwanese legal entity: submit Foreign Investment Approval (FIA) application to the Investment Commission (MOEA); register the company; complete tax and labour insurance registrations. Simultaneously, formalise commercial agreements with your distribution partner: distribution agreement with clear territory, pricing, volume commitments, and exclusivity provisions. Specify dispute resolution, Singapore or Hong Kong arbitration is standard for Taiwan international commercial disputes given the absence of cross-strait legal enforcement mechanisms. Consider Incoterms for logistics risk allocation.

07

Science Park Application (if manufacturing establishment)

If establishing manufacturing operations in Taiwan, apply to the relevant science park administration: Hsinchu Science Park Administration (HSPA) for semiconductors and ICT; Southern Taiwan Science Park Administration (STSPA) for Tainan and Kaohsiung; Central Taiwan Science Park Administration (CTSPA) for Taichung. Provide a detailed business plan, technology description, and employment projection. Science park tenancy provides streamlined customs, lower land rates, and administrative support, making it strongly preferable to independent industrial site selection for technology manufacturing operations.

08

Scale: Regional Asia-Pacific Hub Development

Taiwan’s geographic and commercial position makes it a natural Asia-Pacific hub for technology and automation companies operating across the region. With a Taiwan operation established, explore how it can serve as the regional technology support centre for customers in Vietnam, India, and Southeast Asia, where Taiwanese ODMs and electronics manufacturers are establishing their own production diversification. Many global automation companies use their Hsinchu or Taipei operations as the engineering base for Asia-Pacific customer support, reducing the need for separate country-level technical teams in smaller markets.

SECTION 10

10 How GTsetu Connects You with Verified Taiwanese Partners

The fastest and most commercially efficient route into the Taiwanese market for most automation and manufacturing companies is through a verified local partner, a Taiwanese systems integrator, value-added distributor, or technology partner who has established relationships with the OEM customers, supply chain buyers, and science park procurement teams you need to access. GTsetu pre-verifies every Taiwanese company on the platform against official business registries, trade licences, and relevant sector credentials, so your commercial engagement starts from a verified foundation, not cold outreach.

🏛️

Business Registry Verification

Every Taiwanese company verified against the MOEA Company Registry and trade licensing records, confirming legal identity before any engagement.

🕵️

Anonymous Discovery

Browse verified Taiwanese partner profiles by sector, semiconductor, electronics, precision machinery, ICT, without revealing your market entry plans.

📄

Built-In NDA Workflow

Mutual NDA with digital signatures and full audit trail, executed before any pricing, technical specifications, or IP is shared with a Taiwanese partner candidate.

🔐

Encrypted IP Exchange

Product specifications, integration architecture, and commercial documentation shared in AES-256 encrypted workspace, protecting precision manufacturing IP at every stage.

🌏

Asia-Pacific & Global Coverage

Verified partners in Taiwan and 100+ countries, supporting your global partner and cross-border partnership strategy across Asia-Pacific.

🚫

Zero Commission

GTsetu charges no success fee on any partnership formed. Your deal economics with your Taiwanese partner stay entirely between you.

Q Why is Taiwan a top destination for manufacturing and automation expansion?

Taiwan controls 63% of global advanced chip manufacturing capacity (7nm and below) through TSMC and related foundries, supplies 80–90% of the world’s AI servers through its ODM ecosystem, and operates the world’s most sophisticated electronics manufacturing supply chain. For industrial automation companies, this means Taiwan represents the single most concentrated, high-value demand environment for precision manufacturing automation, where the world’s most technologically demanding manufacturers are actively investing in new automation infrastructure. Beyond semiconductors, Taiwan’s Productivity 4.0 government programme and an ageing, shrinking workforce are driving systematic smart factory adoption across the country’s 150,000+ SME manufacturer base, growing the Industry 4.0 Automation Market at 12–15% CAGR through 2030.

Q How large is Taiwan’s industrial automation market?

Taiwan’s Industrial Process Automation market reached USD 157.7 million in 2024 and is projected to grow to USD 181.6 million by 2030. The broader Taiwan Industry 4.0 Automation Market is growing at 12–15% CAGR through 2030, driven by semiconductor expansion and government-backed smart factory programmes. Most significantly, Taiwan’s semiconductor manufacturing equipment market, the world’s largest single-country market, reached USD 24.7 billion in 2023 and is projected to reach USD 41.3 billion by 2030 at 7.6–7.7% CAGR. Taiwan’s semiconductor equipment investment reached USD 27.9 billion in 2025, representing nearly 70% year-on-year growth, making it the single largest annual industrial automation investment event in any country globally.

Q What is the Productivity 4.0 programme?

Productivity 4.0 is Taiwan’s government programme for smart manufacturing adoption, the Taiwanese equivalent of Germany’s Industrie 4.0. The programme provides NTD 45.6 billion in funding, subsidies, demonstration projects, training, and technical support for manufacturers adopting IIoT, AI, robotics, and digital twin technologies. It targets primarily precision machinery, electronics, food processing, textile, and metal fabrication SMEs, the 150,000+ SME manufacturers who have been slower to automate than Taiwan’s large-cap electronics sector. For automation companies, Productivity 4.0 represents government-backed demand stimulation that reduces the cost barrier and risk for SME customers considering automation investment.

Q What are the key science parks for manufacturing investment in Taiwan?

Taiwan’s key science parks are: Hsinchu Science Park (semiconductors, IC design, precision equipment, TSMC headquarters, ITRI); Tainan Science Park (advanced semiconductors, TSMC 2nm and 3nm fabs, solar panels); Central Taiwan Science Park in Taichung (precision machinery, optoelectronics, smart manufacturing); Kaohsiung Science Park (compound semiconductors, green energy, advanced materials); Southern Taiwan Science Park and Industrial Parks (heavy industry, petrochemicals, aerospace); and Yilan and Chiayi Science Parks (biotech, sports equipment, agritech). All science parks offer streamlined import/export procedures, infrastructure support, and access to the Science Park Administration’s investment facilitation services.

Q How does GTsetu help manufacturers expand into Taiwan?

GTsetu connects manufacturers and industrial automation companies with compliance-verified Taiwanese distributors, systems integrators, and manufacturing partners. Every Taiwanese company on GTsetu has been verified against official business registries and trade licences before engagement, eliminating the identity fraud and misrepresentation risks of cold outreach. Anonymous discovery protects your market entry and technology strategy during evaluation. Built-in NDA workflows ensure precision manufacturing IP, product specifications, and pricing are protected before any technical sharing occurs. All document exchange happens in an encrypted workspace with a complete audit trail. And GTsetu charges zero commission on any partnership formed, unlike broker or trade-show introduction services. This is particularly important in Taiwan where intellectual property protection and relationship trust are paramount commercial considerations.

Q What is the fastest way to generate revenue in Taiwan for an automation company?

The fastest route to Taiwan market revenue for an automation company is a verified distribution partnership with a Taiwanese systems integrator or value-added distributor who has existing Qualified Vendor status with your target OEM customers. This approach requires no entity establishment (saving 2–6 months of regulatory process time), leverages existing customer relationships (bypassing years of direct relationship development), and generates revenue within weeks of the distribution agreement execution. The critical requirement: the distributor must have real, verifiable existing relationships with your specific target customers, not just claimed sector experience. GTsetu provides pre-verified Taiwanese distributors and integrators with documented sector credentials.

Find Verified Taiwanese Manufacturing & Distribution Partners on GTsetu

Join 500+ verified manufacturers, distributors, and automation companies building international trade partnerships on GTsetu, with compliance-verified Taiwanese partner profiles, built-in NDA workflows, encrypted IP protection, and zero broker commission.

They represents the product, and research team behind GTsetu, a global B2B collaboration platform built to help companies explore cross-border partnerships with clarity and trust. The team focuses on simplifying early-stage international business discovery by combining structured company profiles, verification-led access, and controlled collaboration workflows.

With a strong emphasis on trust, and disciplined engagement, Team GTsetu shares insights on global trade, partnerships, and cross-border collaboration, helping businesses make informed decisions before entering deeper commercial discussions.