How to Expand Your Manufacturing & Industrial Automation Business to Romania

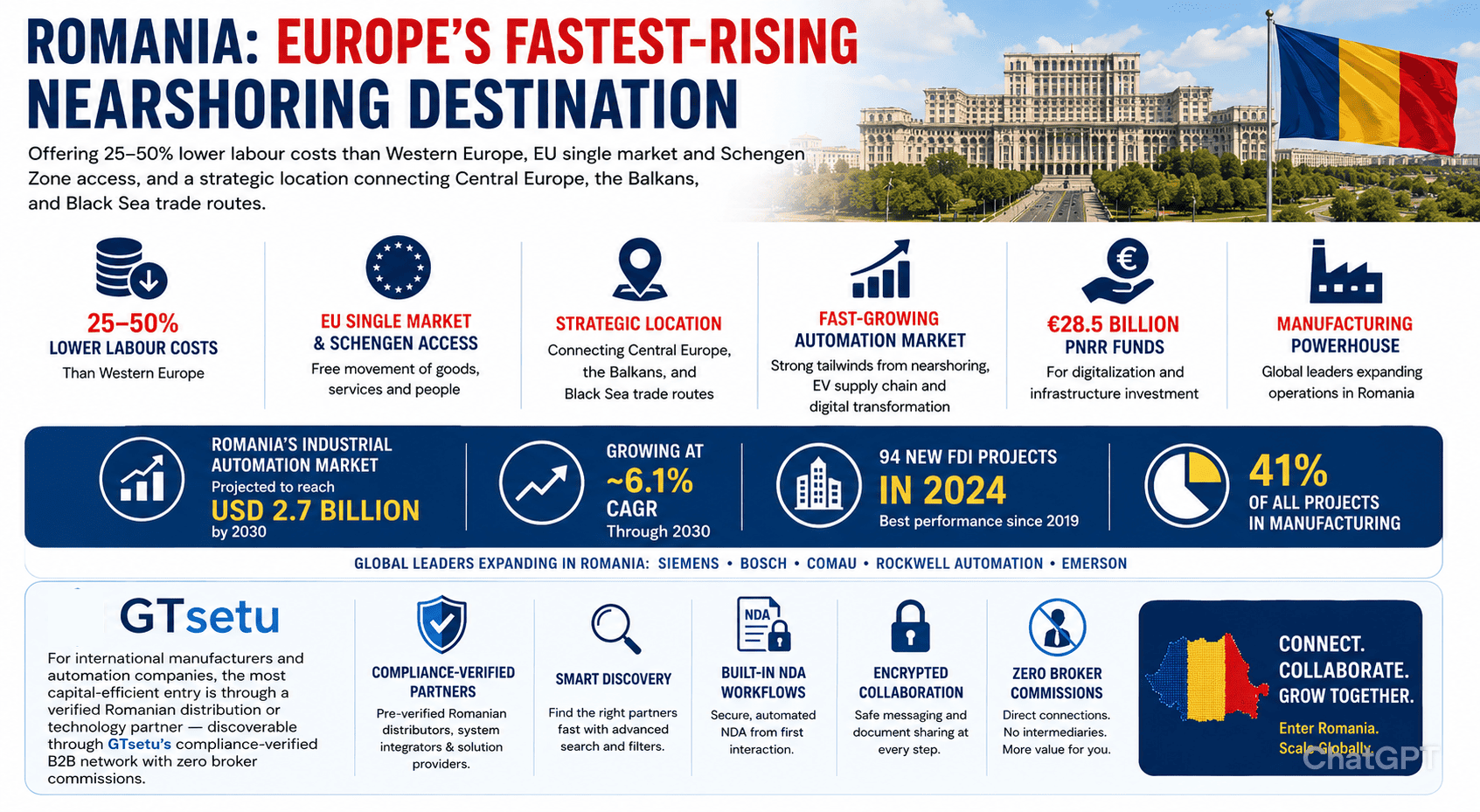

Direct Answer: Romania is Europe’s fastest-rising nearshoring destination, offering 25–50% lower labour costs than Western Europe, EU single market and Schengen Zone access, and a strategic location connecting Central Europe, the Balkans, and Black Sea trade routes. Romania’s industrial automation market is projected to reach approximately USD 2.7 billion by 2030 at ~6.1% CAGR, driven by nearshoring investment, EV supply chain expansion, and €28.5 billion in PNRR digital and infrastructure funds. In 2024 alone, Romania attracted 94 new FDI projects, its best performance since 2019, with manufacturing accounting for 41% of all projects and companies including Siemens, Bosch, Comau, Rockwell Automation, and Emerson expanding Romanian operations. For international manufacturers and automation companies, the most capital-efficient entry is through a verified Romanian distribution or technology partner, discoverable through GTsetu‘s compliance-verified B2B network with zero broker commissions.

📅 June 4, 2026⏱ 22 min read✍️ GT Setu Editorial Team🔄 Updated regularly

$2.7B

Industrial Automation Market by 2030

~6.1%

Automation Market CAGR 2025–2030

€28.5B

PNRR, National Recovery & Resilience Plan

0%

GTsetu Broker Commission

Romania has emerged as one of Europe’s most compelling stories in manufacturing investment and industrial nearshoring. While Western European economies have stagnated, Romania has attracted 94 new FDI projects in 2024, a 57% surge and its best performance since 2019, climbing four places in the European FDI attractiveness index to 13th overall, and 2nd in Central and Eastern Europe. Manufacturing accounted for 41% of all FDI projects, with German, Italian, and US companies leading the wave: Siemens establishing a technology hub in Cluj-Napoca for factory automation and IoT solutions, Bosch operating an engineering centre focused on automotive technology and AI-powered manufacturing, Comau expanding robotics and industrial automation operations, Emerson investing in smart factory solutions, and Rockwell Automation strengthening IoT-enabled manufacturing and predictive maintenance across Romania’s industrial sector.

For international manufacturers, industrial automation OEMs, robotics companies, and sensor and control system providers, Romania in 2026 represents a convergence of structural demand drivers that makes it one of Europe’s most underserved and highest-potential automation markets: 25–50% lower operational costs than Western Europe; EU single market and newly joined Schengen Zone access; €28.5 billion in PNRR digital and infrastructure funds actively subsidising manufacturing modernisation; an expanding automotive, aerospace, furniture, and food processing manufacturing base; and a 70.7% expansion-driven hiring ratio (not replacement) confirming that growth is structural. This guide covers the complete picture, from market sizing and sector-by-sector opportunity, to incentive frameworks, regulatory navigation, partner discovery, and the commercial terms that govern successful Romania market entry. Explore our guides on the advantages and disadvantages of global expansion and international business development consulting for broader strategic context.

🇷🇴 Who Is This Guide For?

This guide is written for international manufacturers, industrial automation OEMs, robotics and control system providers, technology integrators, and industrial equipment companies seeking to enter or expand in the Romanian market, whether through a distributor partnership, technology licensing, contract manufacturing, joint venture, or direct subsidiary establishment. It is also relevant for companies currently selling into Romania via informal channels who want to formalise their presence. If you are exploring other European markets alongside Romania, see our country guides for Germany, Poland, United Kingdom, UAE, and Egypt.

SECTION 1

1 Why Romania for Manufacturing & Industrial Automation?

🎯 The Strategic Case

Romania sits at a structural inflection point, simultaneously Europe’s most cost-competitive EU member state for manufacturing, its most actively growing nearshoring destination, and the single market with the highest untapped automation potential relative to its installed manufacturing base. For international automation companies, Romania offers the rare combination of EU regulatory alignment that removes product compliance barriers, labour costs 25–50% below Western Europe creating urgent automation economics, €28.5 billion in PNRR funds actively subsidising manufacturing digitalisation, and a manufacturing FDI boom that is pulling international automation technology demand with every new greenfield facility.

57%

Surge in FDI projects in 2024 (94 projects vs. 60 in 2023), Romania’s best performance since 2019 and 2nd in CEE

25–50%

Lower operational costs vs. Western Europe, labour, facilities, and logistics, the core nearshoring value proposition

70.7%

Of Romanian job openings are expansion-driven (not replacement), confirming structural growth rather than cyclical hiring (BrainSource 2026)

🇪🇺

EU Single Market & Schengen Access

Romania’s EU membership and 2024 Schengen Zone accession provide tariff-free exports to all 27 EU member states and frictionless goods movement across Europe. Products CE-marked for any EU market require no additional Romanian certification, a major advantage for European manufacturers.

💰

Lowest Labour Costs in the EU

Romania offers average monthly net salaries of approximately €1,069, among the lowest in the EU, with operational costs 25–50% below Western Europe. Rising wages are creating automation economics, but Romania remains highly cost-competitive as a manufacturing base relative to Germany, France, or the UK.

🌍

Premier Europe Nearshoring Hub

Romania has transitioned from a peripheral logistics node into a central distribution and manufacturing corridor connecting Central Europe, Southeastern Europe, and Black Sea trade routes. Global supply chain reconfiguration, driven by the Russia-Ukraine war, Red Sea disruptions, and post-COVID supply chain resilience strategies, is systematically shifting production toward Romania.

🏭

Deep Manufacturing FDI Pipeline

Germany, Italy, and the US are actively expanding Romanian manufacturing operations, Volkswagen supply chain relocation, Gestamp automotive parts factory (Argeș County), Nokian Tyres zero-CO2 factory (Oradea), and major electronics manufacturing investments. Each new facility pulls automation technology demand with it as production lines are equipped and scaled.

💻

World-Class Engineering Talent

Romania produces approximately 10,000 ICT graduates annually, and its engineering talent pool includes software developers, automation engineers, robotics specialists, and mechatronics graduates who have made Romania a preferred destination for technology companies including UiPath (a Romanian unicorn). This talent base makes Romania an excellent location for automation technology co-development and system integration operations.

💶

€28.5B PNRR, Biggest EU Stimulus Per Capita

Romania’s National Recovery and Resilience Plan allocates €28.5 billion through 2026, with over 21% earmarked for digital transition including SME digitalisation grants, Industry 4.0 adoption support, and manufacturing automation. This government-backed demand stimulus is directly funding automation purchases by Romanian manufacturers who would not otherwise have the investment capital.

SECTION 2

2 Romania Industrial Automation Market: Size & Growth 2026

Romania’s industrial automation market is at an early but accelerating stage of development, making it a high-opportunity entry window for international automation companies establishing distributor networks and brand presence before the market matures. Multiple data sources converge on a consistent growth trajectory, driven by nearshoring manufacturing investment, Industry 4.0 adoption mandates from Western European OEM customers, and government PNRR funding actively subsidising automation purchases.

Research Source

Market Indicator

Forecast Horizon

Projected Value / Signal

CAGR

GlobalTenders Industrial Automation Data

Romania industrial automation market

2030

USD ~2.7 billion

~6.1% (PLCs, SCADA, robotics, IIoT)

6W Research, Machine Tools

Romania Machine Tools Market

2031

Significant growth trajectory

5.5% CAGR (2025–2031)

EY Attractiveness Survey Romania 2025

FDI projects in manufacturing (2024)

2024 actual

94 FDI projects (+57%), manufacturing = 41%

Best FDI performance since 2019

ING Economics, Nearshoring Forecast

Manufacturing investment pipeline

2034

Romania GDP projected to exceed €700B; manufacturing major driver

Romania positioned as premier Western nearshoring hub

BrainSource Labour Market Data 2026

Expansion vs. replacement hiring ratio

2026 live data

70.7% of 26,303 expansion jobs are newly created roles (not replacements)

Structural growth, not cyclical, manufacturing & logistics top expansion sectors

Romania’s automation market has historically been underpenetrated relative to its manufacturing scale, particularly in SME segments outside the large automotive and electronics OEMs. The PNRR SME Digitalisation Programme and EU cohesion fund support are now addressing this gap systematically, creating demand in market segments that previously lacked investment capital for automation. For international automation companies, this means the total addressable market is expanding faster than the headline numbers suggest.

Key Market Drivers for International Automation Companies

🏭

Nearshoring Manufacturing Investment Wave

Global supply chain reconfiguration, accelerated by the Russia-Ukraine war, Red Sea disruptions, and post-COVID resilience strategies, is systematically redirecting production to Romania. Aranca analysis confirms Romania outperforms Greece and Bulgaria in securing FDI projects, with 25–50% lower labour costs vs. Western Europe making the economics compelling. Each new nearshored facility requires full automation fit-out, creating concentrated capital equipment demand.

Structural Driver

💶

PNRR €28.5B, SME Digitalisation & Industry 4.0 Grants

Romania’s National Recovery and Resilience Plan allocates over 21% of its €28.5 billion to digital transition, including a dedicated PNRR SME Digitalisation Programme providing grants for automation and Industry 4.0 projects. These grants fund automation purchases by Romanian manufacturers who would not otherwise have the investment capital, directly expanding the automation addressable market to previously under-served SME segments.

EU Stimulus Driver

🚗

Automotive EV Supply Chain Expansion

Romania is the largest producer of motor vehicles in Eastern Europe, with Dacia (Groupe Renault), Ford (Craiova), and an extensive Tier 1 and Tier 2 supply chain base. EV transition investment, including Nokian Tyres’ zero-CO2 tire factory in Oradea and Gestamp’s automotive parts expansion, is driving demand for battery production automation, robotic welding, precision inspection, and advanced quality control systems across the automotive supply chain.

Sector Driver

🔗

OEM Industry 4.0 Compliance Requirements

Romanian Tier 1 and Tier 2 automotive, aerospace, and electronics suppliers are being required by their Western European OEM customers to implement Industry 4.0 capabilities, real-time production data, MES integration, quality traceability, and predictive maintenance, as conditions of supply contract retention. This OEM-imposed compliance mandate creates automation investment demand that is not discretionary but contractually required, compressing the decision timeline significantly.

Compliance Driver

💻

AI & Digital Transformation Acceleration

Romania’s AI and automation transformation is accelerating across both manufacturing and services sectors, documented in the GenGraphic AI Automation Transformation report. The combination of UiPath-ecosystem talent, strong ICT graduate output (~10,000 annually), and PNRR-funded digitalisation projects is creating an ecosystem where AI-powered automation, IIoT, and smart factory implementation are gaining rapid adoption beyond the traditional large-OEM manufacturing base.

Technology Driver

📦

Logistics & Warehouse Automation Expansion

Romania is transitioning from a peripheral logistics node into a central CEE distribution corridor, driving concentrated investment in warehouse automation, AGVs, sortation systems, and logistics management software. BrainSource 2026 data identifies logistics as the highest expansion-hiring sector in Romania by job creation ratio, confirming the scale of capital investment behind the logistics automation wave.

Logistics Driver

SECTION 3

3 High-Demand Sectors for Industrial Automation in Romania

Romania’s automation demand is concentrated in the sectors that form its manufacturing backbone, automotive and components, furniture and wood processing, food and beverage, electronics, aerospace, and chemicals. Understanding sector-by-sector automation demand enables international companies to target their distribution positioning and partner selection with precision.

🚗Largest Segment

Automotive & EV Components

Romania is Eastern Europe’s largest motor vehicle producer, with Dacia (Mioveni), Ford (Craiova), and an extensive Tier 1 and Tier 2 supply chain including Gestamp (Argeș), Nokian Tyres (Oradea), and Volkswagen supplier network expansion. EV transition investment is driving battery component manufacturing, robotic welding, precision machining, and advanced inspection system demand. German companies including Bosch and Siemens have established engineering centres specifically to serve Romania’s automotive automation market.

Key demand: robotic welding, EV component assembly, AGVs, vision inspection, SCADA, MES

🪑EU Top Exporter

Furniture & Wood Processing

Romania is among Europe’s top furniture exporters, with over 3,000 furniture companies serving German, Italian, and UK markets. The sector faces acute labour shortages and European supply chain compliance requirements driving automation in CNC routing, finishing lines, panel processing, and packaging operations. Italian companies Biesse Group and Fiedia have specifically expanded Romanian distribution for CNC woodworking and mould-making automation, validating the market scale.

Food processing is Romania’s largest industrial sector by number of companies and employment. Export-oriented manufacturers serving EU markets face growing food safety compliance requirements (FSSC 22000, BRC) driving processing line automation, filling and packaging systems, CIP automation, and traceability systems. PNRR and EU cohesion grants are specifically funding food processing modernisation across Romanian SMEs who cannot self-fund automation investment.

Key demand: filling and packaging lines, CIP systems, cold chain monitoring, traceability, MES

📱Nearshoring Growth

Electronics & Electrical Equipment

Electric machinery and equipment is Romania’s top export category, with major electronics manufacturers including Flextronics, Celestica, and Honeywell operating Romanian facilities. The sector’s EU export orientation and Western OEM Industry 4.0 compliance requirements drive SMT assembly automation, AOI inspection, PCB testing, and quality management system investment. Electronics manufacturing in Romania is identified as a priority nearshoring sector by ING Economics forecasts.

Romania has a significant aerospace manufacturing history, with companies including IAR (helicopters), Romaero (aircraft maintenance), and a growing supply chain for Western European aerospace OEMs. GE Aviation has partnered with Romanian aerospace firms to produce aircraft engine components. US ITA investment advisors identify aerospace as one of Romania’s highest-growth industrial sectors for advanced automation and additive manufacturing technology adoption.

Key demand: CNC precision machining, composite fabrication, NDT inspection, digital quality systems

🧴Growing Segment

Chemicals, Plastics & Rubber

Romania has a well-established chemicals and plastics sector serving automotive, construction, and consumer goods industries. Petroleum refining (Petrotel-Lukoil, Petrobrazi), plastics injection moulding (servicing automotive Tier 1 suppliers), and specialty chemicals are key automation investment areas, particularly for DCS/SCADA upgrades, safety instrumented systems, and process optimisation platforms required by EU export market compliance standards.

Romania’s PNRR-funded infrastructure programme, including 700km of expressways, hospital construction, and urban development, is driving one of the largest construction sector expansions in EU history (sector employment reached a record 462,000 in July 2025). Building materials automation, prefabricated elements production, and construction material handling represent a significant and growing automation demand pool largely untapped by international automation suppliers.

Key demand: precast concrete automation, material handling robots, batch mixing control, quality systems

📦Fastest Expanding

Logistics & Warehouse Automation

Logistics is identified as Romania’s highest expansion-intensity hiring sector in 2026, with the country transitioning into a major CEE distribution hub for EU internal trade and Black Sea-connected routes. E-commerce penetration growth across Eastern Europe, combined with nearshoring supply chain infrastructure build-out, is generating concentrated investment in warehouse management systems, AGVs, sortation automation, and conveyor infrastructure across Romania’s growing logistics cluster.

4 Key Industrial & Manufacturing Hubs Across Romania

Romania’s industrial geography is distributed across five major development clusters, each with distinct sectoral specialisations and infrastructure quality. Understanding this geography is essential for designing distributor coverage, service networks, and sales operation positioning.

🏙️ Bucharest-Ilfov, Capital & Tech Hub

Romania’s capital region is its largest economic cluster, housing multinational headquarters, logistics centres, food processing facilities, and electronics manufacturing. Bucharest hosts the highest concentration of automation system integrators, industrial distributors, and technology companies. The PNRR government digitalisation procurement is concentrated here.

The South region (Argeș, Pitești, Craiova) is Romania’s automotive heartland, Dacia factory in Mioveni, Ford in Craiova, and Gestamp automotive parts in Argeș. The highest concentration of industrial automation demand in Romania is in this corridor, robotic welding, assembly automation, and precision machining for EU automotive supply chains.

Key clusters: Dacia Mioveni, Ford Craiova, Gestamp Argeș, South Automotive Supply Chain

Transylvania’s three major cities host Romania’s highest concentration of technology companies, engineering talent, and aerospace manufacturing. Siemens has its Romanian technology hub in Cluj-Napoca, Bosch operates an engineering centre, and Continental and ZF Friedrichshafen have significant automotive technology operations. The region is Romania’s highest-growth automation technology cluster.

Key clusters: Siemens Cluj, Bosch Engineering Sibiu, Romavia Brașov, Transylvania IT Park

🪑 West (Timișoara, Arad, Oradea), Furniture & Nearshoring

Western Romania bordering Hungary and Serbia is the premier furniture manufacturing region and a key nearshoring gateway for Western European supply chains. Nokian Tyres’ zero-CO2 factory operates in Oradea, and the region hosts major German and Austrian nearshoring investments. The proximity to the Hungarian border and Schengen Zone makes it a logistics and manufacturing sweet spot.

Key clusters: Timișoara Industrial Park, Arad Free Zone, Oradea Industrial Parks, Nokian Tyres

🌊 East & Moldova (Iași, Bacău, Galați), Emerging

Eastern Romania and the Moldova region represent the country’s highest-growth investment destination due to the lowest operational costs, PNRR infrastructure investment, and proximity to Ukraine reconstruction opportunities. Iași is a growing IT and technology hub; Galați hosts Romania’s largest steel producer (Liberty Galați); and the region is attracting nearshoring investment from companies seeking maximum Romania cost advantage.

Key clusters: Iași IT Hub, Liberty Steel Galați, Bacău Industrial Park, Suceava Woodworking

💡 Distribution Network Design for Romania

For most industrial automation companies entering Romania, a national distributor headquartered in Bucharest with regional engineers in Cluj-Napoca (Transylvania technology cluster) and Pitești-Craiova (automotive corridor) provides the optimal coverage for the first 2–3 years. The automotive corridor (Argeș-Craiova) and the technology cluster (Transylvania) represent the two highest-value automation demand concentrations. See our guide to building a distributor network and our guide on international wholesale distributors for the qualification framework.

SECTION 5

5 Market Entry Models: Choosing the Right Approach

The right entry model for your manufacturing or industrial automation business in Romania depends on your product category, capital availability, long-term Romania and EU strategy, and whether your primary objective is serving the Romanian domestic market, using Romania as a CEE nearshoring production base, or both.

Entry Model

How It Works

Capital Required

Time to Revenue

Best For

Key Reference

Romanian Distributor / Channel Partner

Appoint a verified Romanian company to stock, sell, and support your products in a defined territory

Very Low

3–9 months

Industrial automation hardware, sensors, PLCs, drives, cobots, standardised products with established Romanian applications in automotive, food, furniture, and electronics

Form a jointly owned Romanian company with an established Romanian manufacturer or integrator

Moderate (shared)

12–24 months (setup)

Complex technology integration requiring local engineering depth; access to Romanian partner’s existing OEM customer relationships; shared capital risk for manufacturing establishment

Partner with a Romanian technology company, university, or IT firm to co-develop automation solutions using Romanian engineering talent

Shared

18–36 months (development)

Accessing Romania’s UiPath-ecosystem AI and automation engineering talent; EU Horizon Europe R&D grant eligibility; developing IIoT or Industry 4.0 platforms

💡 Recommended Entry Sequence for Industrial Automation Companies

For most international industrial automation companies entering Romania for the first time, the optimal sequence is: Year 1–2: Appoint 1–2 verified national distributors with sector-specific expertise (automotive/Argeș-Craiova for hardware-intensive products; IT-integrated partners in Cluj-Napoca for smart factory and IIoT solutions). Year 2–3: Evaluate establishing a Romanian SRL for direct market presence, PNRR grant programme eligibility, and CEE hub operations for neighbouring markets. Year 3+: If production volume justifies, assess contract manufacturing or greenfield production for EU market supply. Always ensure your Romanian distributor is actively positioning PNRR and EU cohesion fund grants to customers, these grants are the single most powerful demand accelerator in the Romanian automation market and many SME manufacturers are not yet aware of how to access them for automation purchases.

SECTION 6

6 PNRR, EU Funds & State Aid: What Foreign Manufacturers Must Know

🏛️ Incentive Framework Overview

Romania’s investment incentive framework operates on three parallel tracks: state aid schemes providing tax incentives, direct grants, and subsidised loans for qualifying investment projects; the PNRR (National Recovery and Resilience Plan) allocating €28.5 billion through 2026 with over 21% for digital transition including SME automation; and EU cohesion funds (2021–2027) providing approximately €50 billion for Romania across infrastructure, manufacturing modernisation, R&D, and green energy. Foreign companies incorporated in Romania are fully eligible for all incentive programmes on equal terms with domestic investors.

Profits reinvested in technological equipment, computers, and peripheral devices are exempt from the 16% corporate income tax; direct reduction of effective tax rate on equipment investment

Very High, every automation equipment sale benefiting from this exemption reduces the customer’s effective net cost; technology equipment broadly defined to include automation hardware; applicable to Romanian companies of all sizes

All Romanian corporate income tax payers; reinvestment must be in qualifying technological equipment; profit must be earned in the same fiscal year

State Aid, Direct Investment Grants

Cash grants and tax concessions for qualifying large investment projects meeting employment and investment thresholds; amount determined by project location and eligible investment costs; higher grants available for less-developed regions

High, for automation companies establishing Romanian manufacturing operations or large sales subsidiaries; available across manufacturing, services, and technology sectors; amount and conditions negotiated case-by-case with the Ministry of Economy

Minimum investment thresholds (typically €1M+ for grants, higher for large-scale projects); minimum job creation requirements; applications via the Ministry of Economy

PNRR SME Digitalisation Programme

Grants for SME digital transformation projects including Industry 4.0, automation, cloud migration, and digital skills; multiple tranches available under Romania’s NRRP through 2026; grant intensity typically 50–90% of eligible project costs for qualifying SMEs

Very High, your Romanian distributor’s SME customers can access these grants to fund automation purchases, making them qualified buyers who could not otherwise afford investment; integrating PNRR grant navigation into your distributor’s sales process is a powerful market expansion tool

Romanian SMEs meeting standard EU SME definition; project activities must qualify as digital transformation or Industry 4.0 adoption; applications through MIPE (Ministry of Investment and European Projects)

EU Cohesion Funds (2021–2027)

€50B+ for Romania across infrastructure (roads, railways, hospitals), manufacturing modernisation, R&D, green energy, and smart manufacturing; accessible via PNCDI R&D programme, Regional Operational Programmes, and sector-specific calls

Very High, multiple cohesion fund programmes specifically target manufacturing automation, Industry 4.0, energy efficiency, and smart factory implementation; Romanian subsidiaries of foreign companies are eligible for most programmes; track fund calls via MIPE portal

Romanian legal entities (including subsidiaries of foreign companies); programme-specific criteria vary; partnership with Romanian universities or research institutions strengthens R&D project applications

R&D Tax Deduction

50% additional deduction on R&D expenditure from the corporate tax base (effectively 150% total deduction); covers salaries, materials, equipment, and external services qualifying as R&D activities

Medium-High, for automation companies with Romanian software development, system integration R&D, or IIoT platform development operations; Romania’s UiPath-ecosystem engineering talent makes R&D centre establishment commercially attractive

Qualifying R&D activities as defined by Romanian tax legislation; R&D activities must be performed in Romania; documentation of qualifying expenditures required

Micro-Enterprise Tax Rate (1%)

1% corporate income tax rate for companies with annual revenue below €500,000 (standard rate is 16%); dramatically lower tax burden for early-stage Romanian subsidiaries below revenue threshold

Medium, highly relevant for companies establishing a Romanian sales subsidiary or representative presence in the first 2–3 years before revenue scales above the threshold; provides significant tax cost advantage during market development phase

Romanian legal entities (SRL) with annual revenue below €500,000; at least one full-time employee; not applicable to banking, insurance, or certain other regulated sectors

Free Trade Zones & Industrial Parks

Customs duty exemptions, VAT exemptions on imports, reduced utility costs, prepared industrial land with infrastructure; multiple free zones and industrial parks across Romania offering various local tax incentive combinations

Medium, for companies establishing Romanian manufacturing or logistics operations; Arad Free Zone (western Romania), Curtici-Curtici logistics hub, and Bucharest-area industrial parks provide EU customs-efficient manufacturing locations; combined with state aid and PNRR grants can be very compelling

Manufacturing or logistics operations meeting free zone activity criteria; operator licence from Ministry of Finance; export-oriented operations favoured in free zones

🇷🇴 How PNRR Grants Change Your Sales Strategy in Romania

The PNRR SME Digitalisation Programme is the most powerful demand accelerator in the Romanian automation market, and most international companies entering Romania are not leveraging it systematically. Romanian SMEs that previously could not afford automation investment are now receiving 50–90% grant funding for qualifying Industry 4.0 and digitalisation projects. Your Romanian distributor’s ability to identify grant-eligible customers, help them navigate the application process (or connect them with grant consultants), and time sales proposals to align with grant approval and disbursement cycles is a critical competitive differentiator. Build PNRR grant navigation capability into your Romanian distributor selection criteria, it directly expands your addressable market from large OEMs only to the entire Romanian manufacturing SME base.

SECTION 7

7 Regulatory & Compliance Requirements for Entry

Romania’s regulatory environment is fully aligned with EU standards, a major structural advantage for international companies that already meet EU compliance requirements. All EU product safety directives, CE marking requirements, GDPR, REACH, and RoHS apply in Romania exactly as across the EU27. This means there are no Romania-specific product certification requirements for most industrial automation products beyond standard EU compliance.

01

Business Entity Registration, ONRC (National Trade Register Office)

The standard structure for foreign-owned commercial operations in Romania is the Societate cu Răspundere Limitată (SRL), limited liability company. Registration is via the National Trade Register Office (Oficiul Național al Registrului Comerțului / ONRC). Requirements: minimum share capital of RON 200 (approximately €40, effectively no minimum); at least one shareholder; at least one administrator (director); a registered Romanian address. Online registration is available via the ONRC portal. Registration typically takes 3–7 business days. A Branch (Sucursală) of a foreign company can be established for limited commercial activities without full SRL incorporation, appropriate for initial market assessment phases. For most commercial operations, the SRL is the recommended structure for simplicity, cost, and full eligibility for Romanian and EU incentive programmes.

02

Tax Registration, CIT, VAT, and Micro-Enterprise Status

Romanian corporate income tax (CIT) is set at 16% standard rate, with a dramatically reduced 1% rate for micro-enterprises (annual revenue below €500,000, at least one full-time employee). The micro-enterprise rate is one of the lowest in the EU and provides a significant tax advantage during market development phases. A notable incentive: profits reinvested in qualifying technological equipment are exempt from CIT, directly reducing the net cost of automation equipment purchases. VAT registration is required before commercial invoicing; the standard Romanian VAT rate is 19%, with reduced rates of 9% and 5% for specific goods. EU VAT rules apply. Withholding tax applies to cross-border dividends (5%), interest (16%), and royalties (16%), reduced under Romania’s double tax treaty network (90+ treaties).

03

CE Marking & EU Product Compliance

Romania applies all EU product safety directives in full, CE marking is mandatory for industrial machinery (Machinery Directive 2006/42/EC), electrical equipment (LVD), EMC, and all other relevant EU frameworks. For EU-registered companies whose products are already CE marked, there is no additional Romanian product certification requirement. For non-EU manufacturers, CE marking obtained for any EU market provides immediate access to Romania. RoHS 2 and REACH apply in full. Note that Romania applies these directives through national implementing legislation (transposing EU directives), in practice, CE marking and EU compliance documentation accepted in Germany, France, or the UK are accepted identically in Romania, significantly reducing the compliance burden compared to non-EU emerging markets.

04

GDPR & Data Protection (ANSPDCP)

Romania applies GDPR in full, enforced by the National Supervisory Authority for Personal Data Processing (Autoritatea Națională de Supraveghere a Prelucrării Datelor cu Caracter Personal / ANSPDCP). For industrial automation companies deploying cloud-connected IIoT platforms, MES systems, or remote monitoring solutions that collect personal data of Romanian plant personnel, GDPR compliance is mandatory, data processing agreements, privacy notices, and DPIAs where applicable. Romania’s PNRR digital transition programme specifically funds GDPR-compliant digital infrastructure across SMEs, aligning compliance investment with EU grant eligibility. ANSPDCP enforcement has been active, ensure GDPR compliance is addressed in product architecture and commercial terms from market entry, not retrospectively.

05

Employment Law & Labour Compliance

Romanian Labour Code applies to all employees working in Romania under Romanian employment contracts. Key requirements: written employment contracts registered with REVISAL (General Register of Employees); minimum wage compliance (updated annually); social insurance contributions registration with the National Agency for Fiscal Administration (ANAF) and Labour Inspectorate (ITM); mandatory health and safety training. Romania’s average monthly net salary of approximately €1,069 (November 2025) represents significant cost competitiveness versus Western Europe, but note that public sector wage freezes in 2025–2026 are creating real wage erosion and some talent retention pressure in more specialised engineering roles. For automation technology companies, Romanian engineering talent (software, mechatronics, automation systems) remains available and cost-competitive but requires competitive compensation packages relative to the IT sector benchmark.

06

Intellectual Property Protection

Romania is a full member of the international IP system, EU trademark (EUTM) and EU design registrations via EUIPO are automatically valid in Romania. European Patent Office (EPO) patents cover Romania. Domestic trademark and patent registration is via OSIM (State Office for Inventions and Trademarks). Software copyright is automatically protected under Romanian copyright law (aligned with EU Software Directive). Key considerations: understand IP ownership in contract manufacturing agreements before engaging Romanian OEM partners; specify tooling and mould ownership explicitly in any manufacturing arrangement; ensure NDA agreements are governed by Romanian law with GDPR-compliant digital signature. The PNRR digital transformation programme includes IP digitalisation initiatives, relevant for any automation company applying for PNRR grants for technology development activities in Romania.

SECTION 8

8 Finding a Verified Romanian Distribution or Technology Partner

For the majority of international manufacturing and industrial automation companies entering Romania, finding the right Romanian partner, a distributor, system integrator, technology licensor, OEM partner, or joint venture candidate, is the most consequential decision in the market entry process. As MIA Partner Research documents, the most successful market entries, from German, Italian, and US companies, have been structured around Romanian partners with deep sector expertise, established OEM customer relationships, and the technical engineering capability to integrate complex automation systems into Romanian manufacturing environments.

What to Look for in a Romanian Industrial Automation Distributor or Partner

✅

Verified Business Identity

Romanian Trade Registry number (CUI/CIF), NRC registration, import licence, sector certifications (ISO 9001, industry-specific). Confirm the authorised signatory for commercial agreements. GTsetu pre-verifies all of this before any company appears in its network, see our business verification requirements guide.

🏭

Sector & Application Expertise

Does the partner have genuine application knowledge in your target sector, automotive (Argeș-Craiova), furniture (Transylvania-West), food processing (nationwide), electronics (Bucharest-Transylvania), aerospace (Brașov)? Romanian industrial sectors have distinct technical requirements and buying behaviours driven by their Western European OEM customer compliance obligations.

💶

PNRR & EU Grant Navigation

Does the partner actively help customers access PNRR SME digitalisation grants and EU cohesion fund programmes? A Romanian distributor who can guide SME customers through the grant application process, or who works with specialist grant consultants, dramatically expands the addressable customer base beyond self-funded buyers to the entire grant-eligible SME manufacturing base.

🗺️

Geographic Coverage & Service Depth

Does the partner have genuine presence across your target regions, Bucharest, Transylvania, and the automotive south? A Bucharest-headquartered distributor without service engineers in Cluj-Napoca or Pitești may lack the response time and local presence required by automotive Tier 1 suppliers with European OEM just-in-time requirements.

⚡

Technical & Integration Engineering Depth

Romanian industrial customers, particularly those in the automotive supply chain, expect technical pre-sales application support, system integration capability, commissioning, and ongoing service. Evaluate the partner’s engineering team depth: how many automation engineers, what software and PLC programming capabilities, what language support (Romanian, German, Italian, English)?

🇩🇪

German-Market Integration Capability

Many Romanian automotive and electronics manufacturers are deeply integrated with German supply chains, their automation requirements often align with German OEM specifications. A Romanian distributor with German-language capability, familiarity with Siemens/Bosch ecosystem requirements, and existing relationships with German-invested Romanian manufacturers provides access to the most automation-intensive customer segment.

📊

Financial Standing & Inventory Capacity

Romanian distributors must fund inventory, maintain demonstration systems, and often bridge the timing gap between grant disbursement and customer purchase order. Assess financial standing and credit capacity relative to working capital requirements. See our partnership evaluation criteria guide.

🔐

Data Security & GDPR-Compliant NDA

Industrial automation partnerships involve sharing technically sensitive information. Require execution of a mutual NDA governed by Romanian law before any sensitive technical or commercial data exchange. Ensure the NDA is GDPR-compliant for EU cross-border data transfers. Use encrypted channels, see our guide to B2B secure collaboration.

Channels for Finding Verified Romanian Partners

💻

GTsetu Verified B2B Platform

GTsetu provides access to compliance-verified Romanian manufacturers, distributors, and technology partners across all industrial sectors, with anonymous discovery, built-in GDPR-compliant NDA workflow, and encrypted collaboration. Zero broker commissions. The most efficient and secure channel for verified Romanian partner discovery. Compare with open marketplace alternatives via our guide to supplier collaboration platforms.

Best for Verified Discovery

🎪

Romanian Industrial Trade Shows

TIB – Bucharest International Fair (October, Romexpo), Romanian Automotive Supply Fair (RASF), Metal Show Romania, Indagra (food processing), and Romexpo industry-specific exhibitions are the primary venues for meeting qualified Romanian industrial partners. See our guide on top B2B networking places.

In-Person Channel

🏛️

Bilateral Chambers of Commerce

AHK Romania (German-Romanian Chamber of Commerce and Industry), the most active bilateral chamber with the deepest roster of German-Romanian industrial companies. Camera di Commercio Italiana per la Romania (CCIR), AmCham Romania, and the Bucharest Chamber of Commerce maintain member directories of Romanian companies actively seeking international principal relationships.

InvestRomania (the government investment promotion agency) provides sector-specific market entry support, state aid eligibility guidance, and introductions to Romanian industrial clusters and industrial parks. ARIO and CONAF (National Confederation of Romanian Employers) maintain networks of Romanian manufacturers actively seeking international technology and distribution partnerships. Our B2B business network guide covers association-based discovery in depth.

Government Channel

🔬

Technology Parks & University Research Clusters

Romania’s technology parks, IT Transylvania Cluster (Cluj-Napoca), Software Industry Cluster of North-West Romania, Iași IT Hub, provide access to Romanian technology companies, system integrators, and R&D partners with automation software and IIoT development capability. For automation companies with software components or co-development ambitions, these clusters surface qualified technology partners with Horizon Europe grant eligibility.

Tech Cluster Channel

SECTION 9

9 Step-by-Step Romania Market Entry Roadmap

01

Market Prioritisation, Validate Before Committing

Validate the market opportunity for your specific product category before investing in Romania entry. Which Romanian sectors have the highest automation urgency, automotive (Argeș-Craiova corridor), furniture (Transylvania), food processing (nationwide), or electronics (Bucharest-Transylvania)? Which Western European companies are expanding Romanian production capacity, and are they your current customers who could specify your automation technology for their Romanian facilities? Use GTsetu’s platform to anonymously assess potential Romanian partners before revealing your market entry plans. Explore our guide on cross-border business partnerships for the validation framework.

02

PNRR Grant Landscape Mapping, Build Into Your Strategy

Before approaching your first Romanian customer or distributor candidate, fully understand the PNRR SME Digitalisation Programme and active EU cohesion fund calls for manufacturing automation in Romania. Build a standard customer ROI model that includes applicable grant rates (50–90% of eligible project costs for qualifying SMEs) alongside automation ROI calculations. This positions your Romanian distributor candidates as facilitators of government-funded automation adoption, a compelling sales proposition that separates expert partners from catalogue sellers. The pricing structures guide covers how to structure proposals in markets with significant public subsidy support.

03

Entry Model Selection & CE Compliance Confirmation

Select your entry model based on validated market intelligence. Confirm CE marking status for all products, for EU-registered companies this is typically already in place; for non-EU companies, CE marking for any EU market covers Romania. Assess whether the reinvested profit tax exemption or other state aid creates a case for Romanian subsidiary establishment from day one for large-volume products. Review the full entry model trade-offs in our market entry partnerships guide. If white-label or private label production is part of the strategy, see our white-label vs. private label manufacturing guide.

04

Ideal Partner Profile Definition

Define precisely what you need in a Romanian partner: geographic focus (automotive south, Transylvania technology, Western Romania nearshoring), sector expertise, PNRR grant navigation capability, technical engineering depth (PLC programming, system integration, MES implementation), German and Italian language support where relevant, and financial capacity. The more specific your ideal partner profile, the faster GTsetu’s verified network surfaces relevant candidates. See our guide on distributors and manufacturers relationships for the profiling framework.

05

Partner Discovery & Verification

Discover candidates through GTsetu’s verified platform, TIB Bucharest trade fair attendance, AHK Romania chamber engagement, and InvestRomania facilitation. For every candidate, confirm: ONRC registration (CUI/CIF), VAT registration, import licence, ISO certifications. GTsetu pre-verifies all companies in its network, eliminating this burden. See our business verification requirements checklist for independent verification steps.

Execute a mutual NDA governed by Romanian law before sharing any technical data. Ensure the NDA is GDPR-compliant for EU cross-border data transfers. GTsetu’s platform enforces NDA execution before the encrypted workspace unlocks, satisfying both contractual protection and GDPR requirements. Include explicit non-circumvention provisions where relevant, and ensure IP ownership in any co-development or co-branding aspects is clearly defined.

Execute the manufacturer-distributor contract with review by Romanian legal counsel. Romanian contract law (Civil Code) has specific enforceability requirements for non-compete and exclusivity clauses. Address dispute resolution, specify Romanian arbitration (Bucharest Court of International Commercial Arbitration / CACIR) or international arbitration (ICC, Vienna International Arbitral Centre). Include force majeure provisions and risk allocation mechanisms. Review the business partnership contract guide for the full framework.

SECTION 10

10 Key Commercial Terms for Romania Partnerships

Commercial Term

Romania-Specific Consideration

Reference Guide

Currency & RON Risk

Romania uses the RON (Romanian leu), not the euro. EUR-denominated supply pricing with RON resale pricing exposes the Romanian distributor to currency risk. Options: EUR pricing for large capital equipment projects (accepted by automotive OEM customers), RON pricing with annual EUR/RON review windows, or automatic adjustment bands for exchange rate moves beyond ±5% of a reference rate. Note: Romania is on a path toward euro adoption, the timing remains uncertain but the direction removes long-term currency risk as a structural concern.

Romanian customers accessing PNRR SME digitalisation grants experience delays of 3–9 months between project approval and fund disbursement. Structure distributor payment terms to accommodate grant-funded purchase cycles, avoid standard net-30 terms that may be commercially unrealistic for grant-funded buyers. Consider milestone-based payment terms aligned with grant disbursement phases. This is a critical commercial adaptation that separates Romania-experienced automation suppliers from generic European distribution approaches.

Romania’s geographic and sectoral diversity supports regional or sector-specific exclusivity rather than national exclusivity for first-time partnerships. Consider structuring exclusivity by region (Bucharest vs. Transylvania vs. automotive south) or sector (automotive vs. food vs. furniture) for first-time partnerships. National exclusivity should be earned through year 1–2 performance rather than granted upfront. See our exclusivity clauses guide.

Romanian SMEs, particularly food processors, furniture manufacturers, and fabrication shops outside Bucharest, operate primarily in Romanian. Technical manuals, safety data sheets, and training materials in Romanian are often required for regulatory compliance and practical usability. Define in the distribution agreement who funds Romanian-language translation of key documentation and who approves technical accuracy of translations.

Romanian automotive Tier 1 suppliers (serving German OEM JIT supply chains) have very demanding delivery requirements. Define maximum acceptable lead times, minimum stock requirements for fast-moving products, and emergency delivery protocols. Short lead times are a significant competitive differentiator versus Asian brands in the Romanian automotive automation segment.

First-year volume commitments in Romania should reflect the 6–12 month market development phase and the lumpy purchasing pattern created by PNRR grant timing. Avoid annual commitments that penalise distributors for grant-timing delays outside their control. Denominate in units or EUR value rather than RON to avoid currency-inflation distortion of commitment measurement. See our volume commitments guide.

Romanian industrial customers expect local warranty and technical service, not return-to-manufacturer logistics that add weeks to downtime. Define which warranty functions the Romanian distributor performs, maximum response time SLAs by customer type (automotive OEM-supplier vs. SME food processor), and how warranty costs are shared. Romanian automotive Tier 1 customers may have OEM-mandated service SLA requirements that must be reflected in the distribution agreement.

Romanian distribution agreements should specify notice periods (3–6 months), post-termination inventory buyback obligations, and non-competition restrictions (proportionate scope and duration under Romanian Civil Code). Define explicitly how pending PNRR-funded customer projects at the time of termination are handled, this is a Romania-specific commercial complexity that generic distribution agreement templates do not address. See our termination clauses guide.

PNRR grant applications involve complex documentation requirements, competitive allocation processes, and long processing timelines (3–9 months from application to disbursement). Romanian SMEs often lack the internal capacity to navigate applications alone. Your distributor’s ability to support grant applications, or to partner with specialist grant consultants, is a critical market development capability. Build this into your distributor selection criteria from the start.

💱

RON/EUR Currency & Inflation

Romania’s HICP inflation averaged 6.8% in 2025, forecast at 7% in 2026, one of the highest in the EU. Combined with RON/EUR currency risk, this creates significant pricing complexity for EUR-invoiced automation equipment. Structure automatic price adjustment mechanisms and EUR project pricing into distribution agreements from day one. Monitor Romania’s euro adoption timeline, accession to the eurozone would eliminate this risk permanently.

📉

Fiscal Consolidation Impact on SME Investment

Romania’s government has implemented fiscal consolidation measures, tax increases and spending controls, that reduced household purchasing power and created caution in some SME investment decisions in 2025–2026. This creates a more selective purchasing environment for non-grant-funded automation investment. Position PNRR grants and reinvested profit tax exemptions as the bridge that enables automation investment despite fiscal headwinds, automation financed by government grants is not affected by SME budget constraints.

🤝

Relationship-Driven Sales Culture

Romanian industrial procurement, particularly in the automotive and furniture sectors, is highly relationship-driven. Buying decisions for capital equipment often depend on personal trust built through multiple interactions, plant visits, demonstration installations, and reference customer validation. Plan for longer relationship-building lead times than in more transactional markets, and ensure your Romanian distributor has genuine C-level access at target accounts.

💬

Multi-Language Complexity

Romanian industrial commerce involves multiple languages: Romanian for domestic SME interactions, German for automotive supply chain communications (Volkswagen, Bosch, Continental supplier requirements), Italian for furniture and machinery sector relationships, and English for multinationals. Assess your Romanian distributor’s language capabilities across all relevant stakeholder languages for your target sectors, this is a meaningful operational capability gap in many smaller distributors.

🏗️

Infrastructure Quality Variability

While Romania has invested heavily in infrastructure through PNRR and EU cohesion funds (700km of expressways under construction), road infrastructure quality still varies significantly between major industrial corridors (well-served) and less-developed eastern regions. Factor logistics costs and delivery reliability into pricing and service models for customers outside the major industrial hubs, particularly for heavy automation equipment requiring special transport.

SECTION 12

12 How GTsetu Connects You with Verified Romanian Partners

🇷🇴 GTsetu, Verified B2B Platform for Romania Market Entry

Discover Verified Romanian Manufacturers & Distributors, No Broker Commission

GTsetu provides international manufacturing and industrial automation companies with direct access to compliance-verified Romanian manufacturers, distributors, system integrators, and technology partners, across every industrial sector and all major Romanian manufacturing regions. Every company in GTsetu’s Romania network has been verified through ONRC registration, CUI/CIF tax ID, import licences, industry certifications, and authority letter confirmation before appearing in the platform. You discover, qualify, and engage, without broker intermediaries taking a cut of your commercial economics. Explore our global collaboration examples to understand what verified partnerships look like in practice, and compare with open marketplace alternatives via our guide to alternatives to Alibaba.

🏛️

Multi-Layer Compliance Verification

Every Romanian partner on GTsetu has been verified: ONRC registration, CUI, import licences, ISO certifications, by GTsetu’s compliance team before appearing in the network.

🕵️

Anonymous Discovery

Browse verified Romanian partner profiles without revealing your identity. Protect your Romania market entry strategy until you choose to engage.

📄

GDPR-Compliant NDA Workflow

Digital mutual NDA with timestamped signatures activated before sensitive data exchange. Governed by Romanian law. Fully GDPR-compliant for EU cross-border data transfers.

🔐

Encrypted Document Workspace

AES-256 encryption at rest, TLS in transit. Role-based access controls. Full audit trail. Exchange product specs, pricing, and technical proposals securely.

🚫

Zero Broker Commission

GTsetu charges zero commission on any partnership formed. All commercial economics stay between you and your Romanian partner.

🌏

100+ Countries Including Romania

GTsetu covers all major Romanian industrial regions plus Germany, Poland, India, and 100+ markets for your multi-country expansion.

QWhy should I expand my manufacturing or industrial automation business to Romania?

Romania has emerged as Europe’s fastest-rising nearshoring destination and one of the most structurally compelling automation markets in the EU. Key facts for 2026: Romania attracted 94 new FDI projects in 2024, a 57% surge and its best performance since 2019, with manufacturing accounting for 41% of all projects. Romania climbed from 17th to 13th in the European FDI attractiveness index and ranks 2nd in Central and Eastern Europe. Operational costs are 25–50% lower than Western Europe. Romania has EU single market access and full Schengen Zone membership. The industrial automation market is projected to reach approximately USD 2.7 billion by 2030 at ~6.1% CAGR. Romania’s €28.5 billion PNRR allocates over 21% to digital transition including SME automation grants. Germany, Italy, and the US are leading the manufacturing investment wave, Siemens (Cluj-Napoca factory automation hub), Bosch (automotive engineering centre), Comau (robotics expansion), Rockwell Automation, and Emerson all have expanding Romanian operations. The 70.7% expansion-driven hiring ratio across 26,303 new roles confirms that Romania’s growth is structural rather than cyclical, and manufacturing and logistics are the top two expansion-hiring sectors.

QWhat are the best entry models for expanding a manufacturing or automation business to Romania?

For most first-time Romania entrants in industrial automation and manufacturing technology, the recommended entry sequence is: (1) Appoint a verified Romanian national distributor or regional channel partners, lowest capital, fastest market access (3–9 months to first revenue). Focus initial distributor selection on sector expertise in your primary target vertical: automotive (Argeș-Craiova-Sibiu), furniture and wood processing (Transylvania-West), food processing (nationwide), or electronics (Bucharest-Transylvania). (2) After 2–3 years of validated market presence, evaluate establishing a Romanian SRL (limited liability company) for greater commercial control, direct customer engagement, access to PNRR grant programmes, and use as a CEE hub for neighbouring markets (Bulgaria, Serbia, Moldova). (3) If production volume justifies, for EU nearshoring strategy or state aid incentive access, pursue contract manufacturing via a qualified Romanian OEM, greenfield industrial park establishment, or co-development partnership using Romania’s engineering talent pool. Technology licensing to a Romanian partner is appropriate where Romanian-language adaptation and local production matter but direct establishment is premature. See the full trade-offs in our market entry partnerships guide.

QWhat incentives does Romania offer foreign manufacturers?

Romania’s investment incentive framework includes: (1) Reinvested profit tax exemption, profits reinvested in qualifying technological equipment are exempt from the 16% corporate income tax; one of the most directly automation-relevant tax incentives in any EU market. (2) PNRR SME Digitalisation Programme, grants covering 50–90% of eligible automation and Industry 4.0 project costs for qualifying Romanian SMEs; funded buyer programmes that expand the addressable market significantly. (3) State aid direct grants and tax concessions for large qualifying investments meeting employment and investment thresholds, negotiated case-by-case with the Ministry of Economy. (4) EU cohesion funds (2021–2027), approximately €50B for Romania across manufacturing modernisation, R&D, infrastructure, and green energy; accessible via multiple programme calls through MIPE. (5) R&D tax deduction, 50% additional deduction on qualifying R&D expenditure (effectively 150% total); relevant for automation software and IIoT development operations. (6) Micro-enterprise CIT rate of 1% for companies below €500,000 annual revenue, significantly reduces tax burden for early-stage Romanian subsidiaries. (7) Free Trade Zones, customs and VAT exemptions for export-oriented manufacturing operations. Foreign companies incorporated in Romania are eligible for all programmes on equal terms with domestic investors.

QHow do I find a verified distributor for industrial automation products in Romania?

The most efficient and secure route is through GTsetu’s compliance-verified B2B platform, where every Romanian company has been verified through ONRC registration, CUI/CIF tax ID, import licences, and industry certifications before appearing in the network. GTsetu enables anonymous discovery of verified Romanian partner profiles, GDPR-compliant digital NDA execution before sharing technical data, and secure encrypted workspace collaboration, all with zero broker commissions. Supplement with targeted trade show attendance (TIB Bucharest International Fair, Romanian Automotive Supply Fair, Metal Show Romania), bilateral chamber engagement (AHK Romania for German-supply-chain-integrated companies, AmCham Romania for US-owned operations), and InvestRomania agency facilitation. Always verify candidates independently, or use a platform where pre-verification is already complete, before sharing product specifications or pricing. See our guide on how to find international distributors and our guide on industrial business collaboration for structuring the partnership once found.

QWhat are the key regulations for manufacturing companies entering Romania?

Key regulatory requirements for manufacturing companies entering Romania: (1) Business entity registration, SRL (limited liability company) via the ONRC online portal; minimum RON 200 share capital (effectively no minimum); registration typically completed in 3–7 business days. (2) EU single market compliance, Romania is a full EU member state; CE marking (mandatory for machinery, electrical equipment, and most industrial products), REACH, RoHS, and all EU product safety directives apply. For EU-registered companies, no additional Romania-specific product certification is required for most automation products. (3) Tax registration, CIT at 1% (micro-enterprises below €500K) or 16% standard; VAT at 19%; reinvested profit tax exemption for qualifying technology equipment. (4) GDPR, applies in full; ANSPDCP enforces; critical for IIoT and cloud-connected automation product deployments. (5) Employment law, Romanian Labour Code; ANAF and ITM registration mandatory for all employees; minimum wage compliance. (6) State aid and PNRR grant eligibility, applications through Ministry of Economy or MIPE; legal entity must be registered in Romania. Romania’s EU membership means there is no special import licensing regime for most industrial automation products, standard EU customs procedures apply for non-EU origin goods.

QWhich industrial sectors in Romania have the highest automation investment demand?

The sectors with the highest industrial automation investment demand in Romania in 2026 are: (1) Automotive and EV components, the largest and most automation-intensive sector; concentrated in the Argeș-Craiova-Sibiu corridor with Dacia, Ford, Gestamp, and Volkswagen supply chain companies all investing in Industry 4.0 compliance; driving robotic welding, AGV, precision inspection, and MES demand. (2) Furniture and wood processing, Romania is an EU top exporter; over 3,000 companies; Italian companies (Biesse, Fiedia) have specifically expanded Romanian operations confirming market scale; CNC routing, finishing line robots, and packaging automation are the key demand areas. (3) Food and beverage processing, Romania’s largest industrial sector by company count; nationwide acute labour shortage driving handling and packaging automation; PNRR grants specifically funding food processing modernisation. (4) Electronics and electrical equipment, Romania’s top export category; Flextronics, Celestica, Honeywell operations driving SMT, AOI, and quality automation demand. (5) Logistics and warehouse automation, fastest expanding sector by job creation (BrainSource 2026); Romania’s transition to CEE distribution hub driving AGV, sortation, and WMS investment. (6) Aerospace, GE Aviation, Romaero, and growing supply chain driving high-precision CNC, NDT inspection, and composite fabrication automation demand in the Brașov-Bucharest aerospace cluster.

QHow do German, Italian, and US companies successfully expand into Romania’s industrial automation market?

According to MIA Partner Research’s analysis of successful market entries, the most effective Romania expansion models share several characteristics: (1) Establishing technology hubs rather than just distribution operations, Siemens chose Cluj-Napoca for a factory automation and IoT technology hub, not merely a sales office, creating a permanent market presence that builds Romanian ecosystem relationships. (2) Supporting the automotive supply chain relocation, Volkswagen’s Romanian supply chain expansion created demand pull for Bosch, Continental, and ZF automation technology; following your existing customers into Romania is the lowest-risk entry model. (3) Partnering with Romanian system integrators rather than only appointing catalogue distributors, Comau expanded its Romanian robotics presence through integration partnerships, not just hardware distribution. (4) Leveraging PNRR funding as a sales tool, the most successful automation companies entering Romania are treating PNRR SME grants as a funded buyer programme, helping Romanian manufacturers access grants to fund their technology purchases. (5) Building Romanian engineering team depth early, companies like Emerson and Rockwell Automation have established Romanian engineering teams who speak the language, understand the manufacturing context, and provide credible technical support to Romanian industrial customers. Apply these proven patterns to your own Romania entry strategy.

Ready to Expand Your Manufacturing Business to Romania?

Connect with verified Romanian manufacturers, distributors, and technology partners on GTsetu, with compliance-backed verification, anonymous discovery, GDPR-compliant NDA workflows, and zero broker commissions on every Romania market partnership you form.

They represents the product, and research team behind GTsetu, a global B2B collaboration platform built to help companies explore cross-border partnerships with clarity and trust. The team focuses on simplifying early-stage international business discovery by combining structured company profiles, verification-led access, and controlled collaboration workflows.

With a strong emphasis on trust, and disciplined engagement, Team GTsetu shares insights on global trade, partnerships, and cross-border collaboration, helping businesses make informed decisions before entering deeper commercial discussions.