How to Expand Your Manufacturing & Industrial Automation Business to Australia

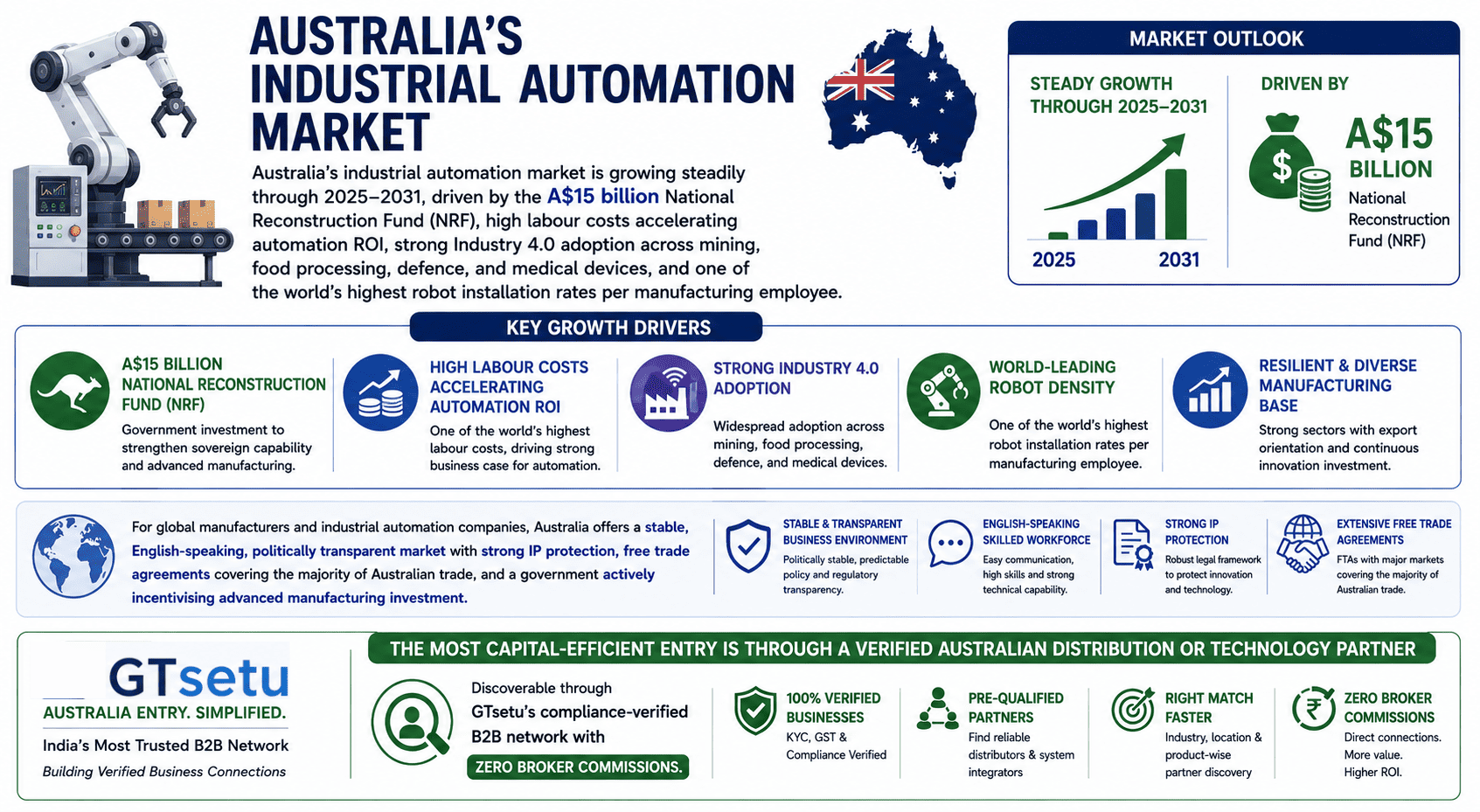

Direct Answer: Australia’s industrial automation market is growing steadily through 2025–2031, driven by the A$15 billion National Reconstruction Fund (NRF), high labour costs accelerating automation ROI, strong Industry 4.0 adoption across mining, food processing, defence, and medical devices, and one of the world’s highest robot installation rates per manufacturing employee. For global manufacturers and industrial automation companies, Australia offers a stable, English-speaking, politically transparent market with strong IP protection, free trade agreements covering the majority of Australian trade, and a government actively incentivising advanced manufacturing investment. The most capital-efficient entry is through a verified Australian distribution or technology partner, discoverable through GTsetu‘s compliance-verified B2B network with zero broker commissions.

📅 April 5, 2026⏱ 21 min read✍️ GT Setu Editorial Team🔄 Updated regularly

A$15B

National Reconstruction Fund

7

NRF Priority Sectors for Advanced Mfg

2031

6WResearch Forecast Horizon

0%

GTsetu Broker Commission

Australia occupies a unique position in the global manufacturing and industrial automation landscape. It is simultaneously a high-income, English-speaking, politically stable developed market with world-class regulatory frameworks, and a country in the midst of a deliberate, government-backed reindustrialisation effort. After decades of declining manufacturing share of GDP, Australia is now investing at national scale to rebuild industrial capability across seven priority sectors, backed by the A$15 billion National Reconstruction Fund and a federal advanced manufacturing strategy that positions automation and robotics as the cornerstone of Australia’s industrial future.

For international manufacturers, industrial automation OEMs, robotics companies, sensor and control system providers, and technology integrators, Australia in 2026 represents a market entry opportunity defined by quality rather than volume, high average selling prices, technically sophisticated buyers, strong IP protection, and commercial relationships built on trust and long-term commitment. Australia’s geographic remoteness and relatively small population create specific distribution and service infrastructure requirements that require careful navigation, but companies that invest in building the right local partner network find a market that rewards quality and commitment with loyal, long-term customer relationships. This guide covers all of it, from market sizing and sector opportunity to regulatory requirements, partner qualification, and the commercial frameworks that govern successful Australia market entry. You can also explore our guides on advantages and disadvantages of global expansion and international business development consulting for broader strategic context.

🇦🇺 Who Is This Guide For?

This guide is written for international manufacturers, industrial automation OEMs, robotics and control system providers, technology integrators, and industrial equipment companies seeking to enter or expand in the Australian market, whether through a distributor partnership, technology licensing, joint venture, or direct establishment. It is equally relevant for companies already selling into Australia informally who want to formalise their market presence. If you are exploring other markets alongside Australia, see our country guides: India, Vietnam, Germany, United Kingdom, and UAE.

SECTION 1

1 Why Australia for Manufacturing & Industrial Automation?

🎯 The Strategic Case

Australia combines the commercial advantages of a mature, high-income developed market, English-language operations, transparent contracts, strong rule of law, world-class IP protection, with the growth dynamics of a market in active reindustrialisation. The government’s deliberate strategy to rebuild manufacturing capability, address supply chain vulnerability exposed by COVID-19, and transition to a net-zero economy is creating structural, multi-decade automation demand across seven priority sectors simultaneously. For industrial automation companies, Australia’s combination of high labour costs, remote geography, skills shortages, and government-backed investment provides a compelling, durable business case that is unlike any other APAC market.

A$15B

National Reconstruction Fund committed to advanced manufacturing and critical technology sectors, accessible to foreign companies incorporated in Australia

Top 5

Global ranking for industrial robot deployment per manufacturing employee, among the highest automation intensity economies globally

15+

Free Trade Agreements in force, covering the US, UK, EU, Japan, South Korea, China, ASEAN, and India, making Australian operations a natural APAC export platform

💼

Stable, Transparent Business Environment

Australia consistently ranks among the world’s top five countries for ease of doing business, rule of law, and contract enforceability. For international companies, this means predictable commercial relationships, effective IP protection, and regulatory frameworks that are understood and consistently applied, a stark contrast to many higher-growth emerging markets.

⚙️

High Labour Costs Drive Automation ROI

Australia has some of the world’s highest industrial labour costs, with average manufacturing wages well above comparable Asian markets. This compresses automation ROI timelines significantly, making the business case for robotic and automated solutions compelling even for mid-size manufacturers, and creating sustained demand across every industrial sector.

🏛️

National Reconstruction Fund Investment Wave

The A$15 billion NRF is the largest peacetime manufacturing investment programme in Australia’s history. Every company receiving NRF financing for production expansion is a potential buyer of your automation, control, robotics, or monitoring solutions, making NRF-aligned sectors the highest-priority prospecting targets for international automation companies.

🔋

Energy Transition & Critical Minerals Opportunity

Australia holds 30–50% of global reserves of several critical minerals required for EV batteries and renewable energy, lithium, cobalt, nickel, rare earths. The domestic processing and battery manufacturing value chain being built around these resources requires sophisticated process automation, materials handling, and quality inspection systems that international automation companies are uniquely positioned to supply.

🌏

APAC Gateway with FTA Coverage

Australia’s 15+ free trade agreements, covering Japan, South Korea, China, ASEAN, India, UK, and a finalised A-UK FTA, make Australian operations a natural platform for companies seeking APAC distribution and manufacturing presence. Products manufactured or value-added in Australia qualify for preferential tariff treatment across a significant portion of global trade.

🛡️

Defence & Sovereign Capability Investment

Australia’s defence spending has increased to 2% of GDP and is rising, with a focus on sovereign manufacturing capability, naval vessels, ammunition, radar, and advanced sensors. The AUKUS agreement and associated technology sharing are creating new domestic defence manufacturing requirements with significant automation content. See our global partner service frameworks for navigating defence market partnerships.

SECTION 2

2 Australia Industrial Automation Market: Size & Growth 2026

Australia’s industrial automation market is tracked by multiple research firms, with consistent directional agreement on steady growth through 2031 driven by PLCs, industrial robots, SCADA systems, and the emerging IIoT and AI-enabled automation layer being deployed across mining, food processing, defence, and medical device manufacturing.

Research Source

Market Scope

Current Value

Forecast Horizon

Key Finding

6W Research

Industrial Automation (PLCs, Robots, SCADA, Sensors, 3D Printing)

Reported 2024

2031

Steady growth driven by Industry 4.0, smart factory adoption, and government manufacturing investment programmes

Nexdigm / IMARC

Industrial Automation (broad including software, services)

Estimated USD 3–4B range (2024)

2032

Growth accelerating with NRF-funded manufacturing expansion in medical devices, defence, and clean energy sectors

IFR (International Federation of Robotics)

Industrial Robots

~4,000–5,000 units/year installed

2027

Food & beverage, metals, automotive and logistics driving new robot installations; collaborative robot (cobot) adoption accelerating

Automated Solutions Australia / Industry Reports

Factory Automation (Robotics, Vision, AGVs)

Strong growth trend 2024–2026

2028

Labour cost pressures, skills shortages, and NRF investment creating sustained multi-year demand across all manufacturing verticals

Government targeting significant increase in value-added manufacturing share through NRF and Future Made in Australia framework

Australia’s industrial automation market is smaller in absolute terms than major Asian or European markets, but commands significantly higher average selling prices, longer product lifecycles in harsh-environment applications (mining, offshore, agricultural), and a procurement culture that prioritises reliability and service over price, creating strong margins for international companies that establish genuine Australian presence. The mining and resources sector alone represents a disproportionate share of automation investment, with Australian mine sites deploying some of the world’s most advanced autonomous and semi-autonomous systems at massive scale.

Key Market Drivers for International Companies Entering Australia

🏛️

National Reconstruction Fund (NRF) Manufacturing Investment

The A$15 billion NRF, Australia’s largest ever peacetime manufacturing investment programme, is funding production expansion across seven priority sectors. Every NRF-approved investment in domestic manufacturing creates downstream demand for automation technology, process control systems, and smart factory integration. NRF disbursements began in 2024 and will drive investment through the end of the decade.

Policy Driver

💰

High Labour Cost & Skills Shortage Acceleration

Australia’s manufacturing labour costs are among the highest globally, with minimum wages, mandatory superannuation contributions (11.5%), and award wages creating powerful economic incentives for automation. Combined with a structural skilled trades shortage that leaves manufacturing positions unfilled for months, automation is increasingly the only viable path to production growth for Australian manufacturers.

Labour Driver

⛏️

Mining & Resources Autonomous Operations

Australia’s mining sector, iron ore, coal, gold, copper, lithium, is the world’s largest deployer of autonomous mining equipment. Rio Tinto, BHP, and Fortescue operate entire mine sites with autonomous haul trucks, drilling systems, and remote operations centres. This sector drives outsized demand for industrial automation, sensor systems, and remote monitoring technology with global reference value for any automation company.

Mining Driver

🔋

Clean Energy & Critical Minerals Processing Investment

Australia’s ambition to become a global renewable energy and critical minerals processing hub, lithium battery materials, green hydrogen, rare earth processing, is driving investment in new processing plants requiring advanced process automation, electrolyser assembly, and materials handling systems. The federal Future Made in Australia programme is accelerating this investment pipeline.

Energy Driver

🤖

AI-Driven Automation Adoption Wave

Australia’s manufacturing sector is accelerating AI integration into automation systems, predictive maintenance, computer vision quality inspection, AI-optimised process control, and generative AI for production planning. International companies offering AI-embedded automation solutions are finding strong early-adopter interest from Australian manufacturers seeking competitive differentiation in high-cost operating environments.

Technology Driver

🛡️

Defence & Sovereign Manufacturing Build-Out

Australia’s AUKUS commitments, increased defence budget, and sovereign manufacturing capability strategy are driving domestic production of defence materiel, naval systems, munitions, advanced electronics, all requiring specialist automated assembly, precision machining automation, and quality inspection systems. Defence is now among the fastest-growing automation investment sectors in Australia.

Defence Driver

🍎

Food & Agri-Tech Export Competitiveness

Australia is a major global food exporter, beef, wheat, dairy, wine, seafood, and food processors are under sustained pressure to automate to maintain cost competitiveness for export markets (particularly Japan, South Korea, China, and the Middle East) while meeting increasing food safety certification requirements. The NRF includes A$15 billion allocation to the food and beverage sector specifically.

Agri-Food Driver

SECTION 3

3 High-Demand Sectors for Industrial Automation in Australia

Industrial automation demand in Australia is concentrated in specific verticals where government investment, labour cost pressures, export competitiveness requirements, and safety compliance drivers are converging to create sustained, high-value automation investment. Understanding which sectors are generating the strongest demand enables international companies to prioritise their Australian go-to-market strategy.

⛏️Largest Segment

Mining & Resources

Australia’s mining sector is the world’s most advanced deployer of autonomous systems, haul trucks, drilling rigs, conveyor systems, ore processing plants, and remote operations centres. BHP, Rio Tinto, Fortescue, and Newmont operate globally-referenced autonomous mine sites that represent the highest concentration of industrial automation investment per facility anywhere in the world.

Australia’s food processing sector, one of the country’s largest manufacturing industries, is investing heavily in automation to address labour costs and export market food safety requirements. Primary processing (meat, dairy, seafood), secondary packaging, and cold chain logistics are all active automation investment areas. NRF funding specifically targets food and beverage manufacturing capability.

Australia is building domestic medical device and pharmaceutical manufacturing capability, accelerated by COVID-19 supply chain vulnerabilities. TGA (Therapeutic Goods Administration) compliance requirements are driving investment in automated filling lines, serialisation, quality inspection, and cleanroom automation. NRF allocates A$1B+ specifically to medical science manufacturing capability.

Australia’s AUKUS commitments and increased defence budget are creating new domestic defence manufacturing requirements, naval vessels, submarine systems, guided weapons, advanced electronics, and munitions. Sovereign manufacturing capability requirements mean these must be built in Australia, requiring specialist automated assembly, precision machining, and inspection systems with international technology content.

Australia’s ambition to process critical minerals domestically, rather than exporting raw ore, is driving investment in lithium processing, battery materials production, green hydrogen generation, and electrolyser manufacturing. Each new processing facility requires sophisticated process automation, materials handling, and quality analytics systems with high technical content.

While volume automotive assembly no longer exists in Australia, automotive component manufacturing, stamping, fabrication, electronics, continues, increasingly supplying global EV supply chains. Australia is also developing EV battery pack assembly capability around its domestic lithium and battery materials processing, creating new automation demand for battery module and pack assembly operations.

Key demand: EV battery pack assembly, stamping automation, weld inspection, traceability systems

🏗️Infrastructure Push

Construction Materials & Building Products

Australia’s massive infrastructure investment programme, roads, rail, housing, airports, is driving demand for automated production of construction materials: prefabricated structures, concrete panels, structural steel, and building products. Automation investment in this sector is supported by a sustained federal and state infrastructure pipeline that extends well into the 2030s.

Australia’s waste and recycling sector is transitioning rapidly, export bans on waste materials are forcing domestic processing investment in automated sorting, materials recovery, e-waste processing, and lithium battery recycling. Automated sorting systems, AI-powered material identification, and robotic disassembly are all active investment areas with strong government support through circular economy policy frameworks.

Key demand: robotic sorting, AI material identification, battery recycling automation, conveyors

SECTION 4

4 Key Industrial & Manufacturing Hubs Across Australia

Australia’s manufacturing and industrial geography is distributed across state-based clusters, each with distinct sector specialisations, infrastructure profiles, and government incentive structures. Understanding this geography is essential for designing an effective distribution and service network for the Australian market.

🏙️ Victoria (Melbourne), Advanced Mfg & Defence Core

Victoria is Australia’s largest manufacturing state by output. Melbourne hosts the highest concentration of advanced manufacturing, defence, medical devices, food processing, and automotive components, and is home to the Australian Manufacturing Workers Union (AMWU) and key defence primes (BAE Systems, Thales, Rheinmetall Australia). Victoria’s Advanced Manufacturing Innovation Precinct (AMIP) in Fishermans Bend is the country’s flagship advanced manufacturing hub.

Key clusters: Fishermans Bend Defence, Food Valley Shepparton, Dandenong Manufacturing, Geelong Advanced Mfg

🌊 New South Wales (Sydney), Tech & Life Sciences

NSW is Australia’s largest economy and the primary hub for pharmaceutical manufacturing, medical devices, electronics, and technology-intensive manufacturing. Western Sydney is undergoing a major transformation as the new Western Sydney Airport (Badgerys Creek) drives industrial and logistics investment. The NSW Government’s Advanced Manufacturing Research Facility (AMRF) supports technology adoption.

Key clusters: Western Sydney Industrial, Hunter Valley Mining Supply, Illawarra Steel & Engineering, Newcastle Advanced Mfg

⛏️ Queensland, Mining, Food & Aerospace

Queensland hosts the world’s largest coal export infrastructure and significant resource sector automation investment. Brisbane’s aerospace cluster (Boeing, Airbus, Northrop Grumman) is growing rapidly. The Sunshine Coast and Gold Coast host advanced manufacturing in medical devices and technology. Regional Queensland has extensive food processing and agricultural automation investment.

🪨 Western Australia (Perth), Mining Autonomy Global Leader

WA is Australia’s mining powerhouse, home to BHP, Rio Tinto, Fortescue, and hundreds of mining supply chain companies. Perth is the operational centre for the world’s most advanced autonomous mining systems, making it a global reference for mining automation technology. WA’s Critical Minerals Strategy is driving new lithium and rare earth processing investments requiring advanced process automation.

South Australia is Australia’s designated defence manufacturing hub, hosting the Future Submarine Programme (AUKUS), guided weapons (GWEO), and the Australian Space Agency. Adelaide’s Osborne Naval Shipyard is one of the most significant sovereign manufacturing investments in Australian history. The SA Government actively recruits advanced manufacturing and defence technology companies.

Tasmania hosts significant food processing (salmon, dairy, horticulture), forestry products, and a growing advanced manufacturing cluster around the University of Tasmania. Regional areas across all states have food processing, agricultural machinery maintenance, and mining services automation requirements that require distributor coverage beyond the major capital city clusters.

Key clusters: Devonport Food Processing, Hobart Advanced Mfg, NT Darwin Port Industrial, ACT Defence Technology

💡 Distribution Network Design for Australia

For most international industrial automation companies entering Australia, the optimal first distribution network requires offices in Melbourne (advanced manufacturing, defence), Sydney (life sciences, technology), and Perth (mining, resources). Brisbane and Adelaide should be covered in Year 2 as the market grows. Australia’s geography means that remote-area service capability, fly-in fly-out (FIFO) technical support for mine sites, regional food processors, is a competitive differentiator that many international entrants underestimate. Your Australian distributor’s service reach beyond capital cities often determines whether you win or lose major accounts. See our guide to building a distributor network for the structural framework.

SECTION 5

5 Market Entry Models: Choosing the Right Approach

Australia offers a straightforward regulatory environment for foreign business entry, 100% foreign ownership is permitted in most sectors, and the establishment process for an Australian company is fast and low-cost relative to many comparable markets. The right entry model depends on your product category, target sectors, capital availability, and long-term APAC strategy.

Entry Model

How It Works

Capital Required

Time to Revenue

Best For

Key Reference

Australian Distributor / Channel Partner

Appoint a verified Australian company to stock, sell, and support your products, assumes inventory and credit risk, operates in defined territories

Very Low

3–9 months

Industrial automation hardware, instruments, sensors, control systems, standardised products with established Australian applications

Incorporate an Australian Pty Ltd, 100% foreign ownership permitted, requires at least one Australian-resident director, no minimum share capital, registration via ASIC in 1–3 days

Low–Moderate

3–6 months (setup + first revenue)

Long-term strategic commitment; direct sales and service operations; NRF funding eligibility; defence and government procurement qualification

Co-invest in a jointly owned Australian Pty Ltd or partnership with an established Australian manufacturer, system integrator, or distribution group

Moderate–High (shared)

12–18 months (structure + setup)

Defence and government sectors where Australian sovereign capability requirements favour locally owned entities; complex technology requiring deep local integration

License software, process know-how, or manufacturing technology to an Australian partner, earn royalties without operational presence

Minimal

6–18 months (licensing negotiation)

Software platforms, proprietary control algorithms, specialised process technologies; where Australian manufacture is strategically important but direct establishment is premature

Commission an Australian EMS/OEM to manufacture or assemble your products in Australia, for local supply, defence qualification, or NRF-supported production

Low–Moderate

6–12 months (qualification)

Defence and government procurement requiring Australian content; NRF eligibility; reducing import tariffs on finished goods versus components

Partner with an Australian university (CSIRO, ANU, University of Melbourne, UQ), research centre, or Cooperative Research Centre (CRC) to co-develop Australia-adapted solutions

Shared

18–36 months (development cycle)

Adapting global platforms to Australian industry requirements; accessing Australian R&D tax incentives; building credibility with government and mining sector buyers

💡 Recommended Entry Sequence for Industrial Automation Companies

For most international industrial automation companies entering Australia: Year 1–2: Appoint a verified national distributor with sector-specific expertise (mining / food / defence / medical), targeting one or two of the highest-demand sectors for your product category. Attend AUSTECH and/or AIMEX for market visibility and partner assessment. Year 2–3: Evaluate establishing a Pty Ltd as a local entity for direct sales, government tender eligibility, and potential NRF financing access. Year 3+: Assess whether Australian contract manufacturing or co-development partnerships can enhance your positioning in defence or government markets requiring Australian sovereign content. Australian Pty Ltd registration takes 1–3 business days and has no minimum capital, one of the world’s simplest incorporation processes, but the operational costs (GST compliance, payroll tax, superannuation, workers compensation) require realistic financial modelling before committing.

SECTION 6

6 National Reconstruction Fund & Government Programmes: What Foreign Companies Must Know

🏛️ Policy Overview

The National Reconstruction Fund (NRF) is Australia’s flagship manufacturing investment vehicle, a A$15 billion fund providing concessional loans, equity investments, and guarantees to support manufacturing and industrial capability in seven priority sectors. Unlike India’s PLI scheme (which provides direct production incentives), the NRF operates as a financing facility, reducing the cost of capital for qualifying manufacturing investments rather than providing grants or tax credits. Foreign companies incorporated in Australia as Pty Ltd entities are eligible to apply for NRF financing. For automation technology companies, the NRF is the most important demand signal in the Australian market, every company receiving NRF financing for manufacturing expansion is a qualified buyer of automation, control, and monitoring solutions.

NRF Priority Sectors & Their Automation Technology Requirements

High, Industry 4.0 integration, digital twin platforms, IIoT systems, AI-driven manufacturing analytics

Cross-sector productivity enhancement, Industry 4.0 technology adoption, R&D commercialisation

Additional Government Support Programmes

Programme

Managing Body

Relevance to Automation Companies

Funding Mechanism

R&D Tax Incentive

ATO / Industry, Science & Resources

High, 43.5% refundable tax offset for eligible R&D expenditure (turnover <A$20M); 38.5% non-refundable for larger companies. Accessible to Australian Pty Ltd entities conducting qualifying R&D

Tax offset on eligible R&D expenditure, no grant application required; registered with AusIndustry

Critical Technologies Investment Programme

DISR

High, A$1B for enabling technologies including AI, robotics, advanced manufacturing, and IIoT systems. Foreign companies in Australian joint ventures can participate

Competitive grants and concessional financing for qualifying technology investments

Modern Manufacturing Initiative (MMI)

DISR

Medium–High, grants for manufacturers investing in capability, collaboration, and commercialisation in priority sectors. Many MMI recipients are automation technology buyers

Grants up to A$20M for qualifying manufacturing investments; co-investment required

State-Level Advanced Manufacturing Grants

State Government Economic Development Agencies

Medium, all major states (Victoria, NSW, Queensland, SA, WA) have dedicated advanced manufacturing support programmes with grants, land access, and co-investment for qualifying companies

Varies by state: grants A$50K–A$5M; concessional land; workforce training subsidies

Austrade Trade & Investment Support

Australian Trade and Investment Commission (Austrade)

High, Austrade provides free market entry facilitation, investor introduction services, and sector-specific intelligence for international companies establishing in Australia. First point of contact for serious market entrants

Free advisory services, introductions, and market intelligence; online at austrade.gov.au

🇦🇺 NRF Strategy for Automation Companies

Even if your automation company does not directly qualify for NRF financing (most automation technology providers do not, NRF targets manufacturers, not their suppliers), the NRF is your primary demand signal. Build your Australian sales strategy around NRF-approved manufacturers in your target sectors, every company receiving NRF concessional financing for production investment is expanding capacity and needs automation technology. Austrade can provide introductions to NRF-approved companies in your target sector, engage Austrade’s investment facilitation team early in your Australian market entry planning. Also note that Australia’s R&D Tax Incentive is available to any Pty Ltd conducting qualifying R&D in Australia, this is accessible without a competitive grant application and provides a direct 43.5% return on qualifying R&D expenditure for smaller companies. See our technology partnership frameworks for how to structure R&D partnerships that maximise this incentive.

SECTION 7

7 Regulatory & Compliance Requirements for Entry

Australia’s regulatory environment for foreign companies is among the most straightforward in the world, transparent, consistently applied, and with extensive government support available for navigating compliance requirements. The key compliance considerations for manufacturing and industrial automation companies are specific and manageable with appropriate planning.

01

Business Registration, ABN & ACN (ASIC)

Foreign companies establishing an Australian entity must register a Proprietary Limited Company (Pty Ltd) with the Australian Securities and Investments Commission (ASIC), one of the world’s fastest and simplest incorporation processes, achievable online in 1–3 business days. The Pty Ltd requires at least one Australian-resident director (this can be a service director engaged through a corporate services provider). Upon incorporation, the company receives an ACN (Australian Company Number). A separate ABN (Australian Business Number) is required for tax purposes and is obtained from the ATO. GST registration is mandatory for entities with A$75,000+ annual turnover. No minimum share capital requirement exists, a single $1 share is sufficient at incorporation, though practical considerations usually dictate a more substantial initial capitalisation.

02

RCM Mark (Regulatory Compliance Mark), Electrical & Electronic Equipment

The RCM mark (Regulatory Compliance Mark) is Australia and New Zealand’s mandatory product compliance mark for electrical, electronic, and telecommunication equipment, replacing the former C-Tick and A-Tick marks. RCM certification demonstrates compliance with the relevant Australian Standards (AS/NZS) for electromagnetic compatibility (EMC) and electrical safety. For industrial automation products including PLCs, drives, HMIs, sensors, and control systems, RCM mark is mandatory before commercial sale in Australia. RCM requires testing against applicable AS/NZS standards, self-declaration of conformity, registration in the ERAC (Electrical Regulatory Authorities Council) database, and annual renewal. RCM compliance lead times are typically 2–6 months, initiate this process well before your planned Australian market launch. Note that some products that already hold CE marking may require additional Australian-specific testing rather than direct acceptance of CE test reports.

03

Work Health & Safety (WHS) Compliance

Australia’s Work Health and Safety framework, based on the harmonised WHS Act across most states and territories, imposes significant obligations on manufacturers and suppliers of industrial equipment. Manufacturers of plant (machinery and equipment) that could pose a risk to workers must conduct risk assessments and may need to register plant designs and individual items of plant with the relevant state WHS regulator before first commissioning in Australia. For imported industrial automation equipment, the Australian importer/distributor is typically the legal duty holder under WHS, but international suppliers must provide adequate information, instructions, and technical documentation to enable compliance. Ensuring your Australian distributor understands and accepts WHS duty-holder responsibilities is a contractual requirement that must be addressed in your distribution agreement.

The Foreign Investment Review Board (FIRB) reviews certain foreign investments in Australia for national interest implications. For most manufacturing and industrial automation market entry models, establishing a Pty Ltd, appointing a distributor, or licensing technology, FIRB approval is not required. FIRB review is triggered primarily by acquisitions of established Australian businesses above A$310M threshold (lower thresholds apply for investments from certain countries, for sensitive sectors including defence and critical infrastructure, and for agricultural land). If you are planning to acquire an existing Australian automation distributor or manufacturer, assess FIRB requirements with Australian legal counsel before initiating negotiations. The NRF financing process involves its own Australian government approval requirements separate from FIRB.

05

Australian Privacy Act & Australian Privacy Principles

The Australian Privacy Act 1988 and its 13 Australian Privacy Principles (APPs) govern the collection, use, storage, and disclosure of personal information by entities with A$3M+ annual turnover. For industrial automation companies deploying connected systems in Australian facilities, IIoT sensors, condition monitoring, production tracking, data handling involving employee information or operational data that can be linked to individuals must comply with the APPs. Cross-border data transfer provisions require either consent or confirmation that the overseas recipient is subject to comparable privacy obligations. Ensure your cloud-connected automation architecture documents its Australian privacy law compliance position, Australian industrial buyers in regulated sectors (health, defence, financial services) will audit this. See our B2B secure collaboration guide for relevant frameworks.

06

GST, Income Tax & Transfer Pricing

Australia’s Goods and Services Tax (GST) applies at 10% on most commercial transactions. GST registration is mandatory for entities above A$75,000 annual turnover and is straightforward through the ATO. Australian company income tax rate is 30% (25% for base rate entities with turnover below A$50M). Transfer pricing rules apply to related-party transactions between an Australian Pty Ltd and its overseas parent, arm’s-length pricing documentation is required for intra-group supply arrangements above materiality thresholds. For companies supplying goods from overseas to an Australian distributor, the Pty Ltd structure creates a clean tax boundary; for branch offices, the tax treatment is more complex. Engage an Australian tax adviser experienced in international business before finalising your operational structure.

07

IP Protection in Australia

Australia has a robust and well-enforced IP protection framework. Register trademarks through IP Australia (trademark registration valid for 10 years, renewable), processing takes 7–13 months for straightforward applications. Patent protection through IP Australia provides 20-year protection for inventions meeting patentability requirements; Australia is a PCT national phase jurisdiction. Trade mark and patent applications can be filed through Australian patent attorneys with experience in international IP portfolio management. For software-embedded automation systems, copyright protection is automatic in Australia (no registration required) and is generally effective. See our guides on IP ownership in manufacturing partnerships and mutual NDA frameworks before entering Australian partner arrangements.

SECTION 8

8 Finding a Verified Australian Distribution or Technology Partner

For international manufacturing and industrial automation companies entering Australia, finding the right Australian partner is the most important single decision in the market entry process. Australia’s market is relationship-driven, industrial buyers value long-term supplier partnerships and make significant switching costs before changing automation suppliers. The right Australian partner brings not just commercial channel access but sector credibility, remote-area service capability, and the government and procurement relationships that are essential for winning in mining, defence, and medical device manufacturing.

What to Look for in an Australian Industrial Automation Distributor or Partner

✅

Verified Business Identity

ACN (ASIC registration), ABN, GST registration, relevant industry certifications (ISO 9001, AS 4801 for OHS management, DISP for defence), and authority letter confirmation. Non-negotiable foundation, see business verification requirements.

🔧

Technical Engineering Capability

Australian industrial buyers demand technical pre-sales and commissioning support, not just order processing. Does the partner have qualified engineers (mechanical, electrical, software) capable of application engineering, site demonstration, and first-line technical support? Critical for mining, defence, and pharmaceutical sector accounts where technical credibility is table stakes.

🗺️

Geographic Reach & FIFO Capability

Australia’s size means geographic reach matters enormously. A distributor covering Melbourne and Sydney but with no presence in Perth (mining), Adelaide (defence), or regional Queensland (food processing) cannot serve your target markets. Critically, do they have the capability and willingness to provide fly-in fly-out (FIFO) technical service to remote mine sites? Many major mining accounts are 4–12 hours from capital cities.

🏗️

Sector Specialisation & Existing Customer Base

Does the partner have genuine customer relationships in your target sectors, mining, food processing, defence, medical devices? A distributor covering 30 unrelated product categories without sector depth will be unable to position complex automation solutions competitively with technically demanding Australian industrial buyers. See partnership evaluation criteria.

🛡️

Defence Industry Security Programme (DISP) Membership

For companies targeting Australian defence manufacturing accounts, your distributor should hold active DISP (Defence Industry Security Programme) membership, the security framework required to supply defence prime contractors and government defence projects. DISP membership involves background checks, security clearances, and ongoing compliance, confirm this status before committing to a defence market partnership.

⚡

RCM & Standards Compliance Capability

Can the partner support RCM mark compliance obligations, managing product registration, coordinating testing, and ensuring ongoing mark maintenance? The Australian importer of record has WHS and product compliance obligations; your distribution agreement must clearly define who bears responsibility for RCM registration and maintenance, and the allocation of compliance costs.

💰

Financial Capacity & Inventory Financing

Australian automation distributors typically need significant inventory investment, particularly for mining and food processing accounts that demand fast spare parts availability. Does the partner have the financial capacity to maintain adequate stock, fund demonstration equipment, and carry the working capital of 60–90 day Australian payment cycles? See our payment terms guide.

🔐

Cybersecurity & Data Handling Practices

Australian Privacy Act and sector-specific cybersecurity requirements (particularly in defence and critical infrastructure) mean your partner must have demonstrable data security practices. Require execution of a mutual NDA governed by Australian law before any sensitive data exchange. Use encrypted channels, see B2B secure collaboration.

Channels for Finding Verified Australian Partners

💻

GTsetu Verified B2B Platform

GTsetu provides access to verified Australian manufacturers, distributors, system integrators, and technology partners, with anonymous discovery, built-in NDA workflow, and encrypted collaboration at zero broker commission. The most efficient and secure channel for verified Australian partner discovery. See how GTsetu compares to alternatives to Alibaba and open B2B directories for a full picture of available channels.

Best for Verified Discovery

🎪

AUSTECH, AIMEX & Sector Trade Shows

AUSTECH (biennial, Sydney/Melbourne, precision engineering and advanced manufacturing), AIMEX (Sydney, mining equipment), Fine Food Australia (Sydney, food processing), and AuManufacturing Forum are the key sector-specific events for meeting potential Australian partners. Hannover Messe Australia (associated events) and Pacific 2025 (naval defence) are also significant. See our top B2B networking places for manufacturers.

In-Person Channel

🏛️

Austrade International Trade Facilitation

Australia’s official trade and investment promotion agency, Austrade, provides free introductions, market intelligence, and sector-specific facilitation for international companies entering Australia. Austrade offices in 80+ countries provide on-the-ground support for initial Australian partner search and NRF-aligned opportunity identification. First point of contact for any serious Australian market entry.

Government Channel

⚙️

Ai Group & Sector Associations

The Australian Industry Group (Ai Group) is the primary national manufacturing industry association, with 60,000+ member businesses. Sector-specific associations include AMTIL (Australian Manufacturing Technology Institute), AMCA (Advanced Manufacturing Cooperative Research Association), DIAA (Defence Industry Association), FAAA (Food & Agribusiness Alliance), and state-based advanced manufacturing associations that maintain active member directories. See our B2B business network guide.

Association Channel

🔬

CSIRO, CRCs & University Research Partnerships

CSIRO (Commonwealth Scientific and Industrial Research Organisation) is Australia’s national science agency with 5,000+ researchers across manufacturing, materials, and digital technology. Cooperative Research Centres (CRCs) bring together universities, industry, and government around specific technology challenges. Partnering with a CSIRO research team or relevant CRC provides research credibility, government connections, and R&D Tax Incentive access. See our technology partnership guide.

Research Channel

SECTION 9

9 Step-by-Step Australia Market Entry Roadmap

01

Market Prioritisation, Validate Sector Fit

Before committing resources to Australia, validate which specific sectors and applications have the strongest unmet demand for your automation solutions. Is your product most relevant to mining automation, food processing, defence, medical devices, or clean energy? Australian buyers in each sector have distinct procurement processes, technical standards, and supplier relationship expectations. Use GTsetu’s platform to anonymously assess potential Australian partners and identify sector-specific demand signals before revealing your market entry plans. A targeted 4–6 week validation programme including GTsetu discovery, Austrade briefings, and AUSTECH attendance will provide better market intelligence than any desk research.

02

RCM Compliance Programme, Start Early

Initiate your RCM (Regulatory Compliance Mark) certification programme in parallel with market validation, not after partner selection. RCM timelines of 2–6 months mean delays here delay your entire Australian commercial launch. Engage an Australian or New Zealand-based RCM compliance consultant for a gap assessment of your products against applicable AS/NZS standards. For products already CE-marked, assess whether Australian-specific testing is required in addition to European test reports. Register your company in the ERAC database before committing to first commercial sales. If your products are categorised as industrial plant under WHS regulations, identify which states require plant design registration and build this into your compliance timeline.

03

Ideal Partner Profile, Be Specific

Define precisely what you need in an Australian partner: sector specialisation (mining / food / defence / medical / clean energy), geographic coverage (which capital cities and remote regions), engineering team depth and qualifications, DISP membership if defence is a target sector, and existing customer base profile. The more specific your ideal partner profile, the faster GTsetu’s verified network surfaces relevant Australian candidates. For mining sector partners specifically, also assess their existing supplier relationships with the major mining companies (BHP, Rio Tinto, Fortescue, Newmont), a distributor already approved as a supplier to these companies has an enormous advantage over one requiring new vendor qualification from scratch. See our international wholesale distributors guide for qualification frameworks.

04

Partner Discovery & Verification

Discover candidates through GTsetu’s verified platform, targeted trade show engagement, Austrade introductions, and Ai Group member outreach. For every candidate, verify: ASIC registration (at abr.business.gov.au), ABN status, relevant certifications, and trade references from existing principals. GTsetu performs compliance verification for all companies on its platform, eliminating this due diligence burden. See business verification requirements for the complete Australian checklist.

05

NDA Execution & Secure Technical Exchange

Execute a mutual NDA governed by Australian law before sharing any technical data. Australian commercial culture is straightforward about NDAs, most serious partners expect and welcome them as evidence of commercial professionalism. GTsetu’s platform has the NDA workflow built in, activated before the encrypted workspace unlocks. For defence-adjacent technology, be especially cautious about information sharing before verifying a partner’s DISP status and security clearance level, some of your technology may be subject to Australian export control (Defence Export Controls) or ITAR/EAR restrictions that limit sharing with Australian entities without appropriate licencing.

06

Commercial Negotiation, Australian Market Specifics

Negotiate all commercial terms with Australian market specifics in mind. Key Australia-specific considerations: AUD pricing and exchange rate risk allocation; exclusivity structure (national vs. sector-specific vs. state-based); payment terms (standard Australian commercial terms: 30 days EOM, sometimes 60 days for major manufacturers); GST treatment on all transactions; RCM compliance responsibility allocation; WHS duty-holder provisions; remote-area service coverage commitments; and annual volume commitments calibrated to realistic Australian market development timelines.

07

Agreement Execution with Australian Legal Review

Execute the manufacturer-distributor contract with review by Australian-qualified legal counsel. Australian contract law (based on English common law principles) is generally business-friendly with few mandatory provisions that override contractual terms, but Australian Consumer Law (ACL) guarantees for business goods and the WHS duty-holder provisions require specific contractual treatment. Address dispute resolution explicitly, most international supplier-distributor agreements with Australian parties specify Australian courts or ACICA (Australian Centre for International Commercial Arbitration) arbitration as the dispute resolution mechanism. Review termination clauses and non-compete provisions carefully, Australian courts generally enforce reasonable restraint of trade clauses.

08

Market Launch & Partner Enablement

A successful Australian launch requires specific enablement investment: joint technical seminars at target customer facilities (mining sites, food processing plants, defence primes); co-development of Australian reference case studies from first installations; AUSTECH and sector show co-presence for market visibility; Australian-specific product documentation addressing local standards (AS/NZS, WHS, RCM); and a clearly defined remote-area service commitment. The first 12 months in Australia require sustained investment in your distributor’s technical capability, under-invest here and the relationship stalls before meaningful momentum builds. Australian industrial buyers are patient evaluators but become extremely loyal to suppliers who demonstrate genuine technical commitment to the Australian market.

SECTION 10

10 Key Commercial Terms for Australia Partnerships

Australia-specific commercial dynamics require important adjustments to standard international distribution agreement terms. Australian commercial law, procurement culture, and the unique geographic and sector characteristics of the market shape what effective Australian partnership agreements must contain.

Commercial Term

Australia-Specific Consideration

Reference Guide

AUD Pricing & Exchange Rate Risk

Australia pricing is in AUD. For non-AUD suppliers, AUD/home-currency fluctuations (AUD can move 10–15% against USD/EUR in a 12-month period) significantly affect supply cost economics. Structure annual price review mechanisms, typically tied to AUD/USD rate bands, to address exchange rate movements systematically rather than creating ad-hoc disputes mid-year.

Australian GST (10%) applies to most commercial transactions. If your overseas entity is the legal seller (without an Australian Pty Ltd), GST may not be applicable on export supplies, but once an Australian entity exists, all domestic sales attract GST. Structure invoicing and distributor pricing to reflect GST economics correctly from day one, GST compliance errors with the ATO are costly and time-consuming to unwind.

Standard Australian commercial payment terms are 30 days EOM (end of month), sometimes 60 days for large industrial manufacturers. For a new relationship, start with advance payment or letter of credit for first 2–3 orders before establishing open account credit with a defined credit limit. Australian company credit checks are straightforward through commercial credit bureaus (Illion, Equifax Australia).

Clearly specify in your distribution agreement who is responsible for RCM registration, maintenance, and renewal costs, the overseas manufacturer or the Australian distributor (as importer of record). WHS duty-holder responsibilities for industrial plant must also be clearly allocated. Ambiguity here creates significant liability exposure on both sides.

Given Australia’s geographic size and sector complexity, consider structuring exclusivity by sector (mining / food / defence / medical) rather than pure geography for first partnerships. A distributor with deep mining sector relationships but no food processing presence cannot effectively cover national exclusivity across all sectors. Performance-linked exclusivity provisions (extending exclusivity rights tied to annual revenue milestones) are standard Australian commercial practice.

Australian Consumer Law provides automatic statutory guarantees for goods supplied to consumers and certain small businesses, including that goods are of acceptable quality and fit for purpose. For commercial B2B sales, ACL guarantees can be contractually modified or excluded in some circumstances, but cannot be excluded for consumer sales. Define your warranty policy clearly, including the treatment of field failures in remote mine sites where service costs can be disproportionate to product value.

Servicing automation equipment at remote Australian mine sites involves significant FIFO travel costs, flights, accommodation, per diem, that can easily exceed product value for minor repairs. Define clearly in your agreement and end-customer warranty policy how remote area service costs are allocated: between you and your distributor, and between your distributor and the end customer. Failure to address this creates recurring commercial disputes once the first remote site service call occurs.

Australian industrial sales cycles for new suppliers can be 12–24 months for major mining or defence accounts, vendor qualification processes at BHP or Thales Australia are thorough and time-consuming. First-year minimum purchase commitments must reflect these realities. Calibrate minimums to achievable market development targets with ratchet provisions in years 2–3 as qualifications are completed and the pipeline matures.

Australia is the world’s largest island continent, and major industrial facilities can be thousands of kilometres from service centres. A mine site in the Pilbara (WA) is 1,500km from Perth; a food processing plant in Queensland’s Atherton Tablelands is hours from Brisbane. Service capability for remote locations is not optional for serious market entry, it is a prerequisite for winning major accounts.

🏆

Long Vendor Qualification Processes in Mining

Major Australian mining companies (BHP, Rio Tinto, Fortescue) have rigorous vendor qualification processes, technical evaluation, financial assessment, safety audits, and often site trials, that can take 12–24 months for a new supplier. Build this timeline into your revenue projections and partner performance expectations. The reward for completing qualification is sustained, high-volume purchasing relationships, but the patience to complete qualification is essential.

💱

AUD Exchange Rate Volatility

The Australian dollar is a commodity-linked currency that can experience significant volatility, 10–20% swings against USD and EUR over 12–18 month periods are not uncommon. This directly affects the economics of AUD-priced, foreign-currency-sourced automation products. Build exchange rate risk management into your pricing strategy from day one, and ensure your distribution agreement has clearly defined price review mechanisms.

📋

RCM & WHS Compliance Complexity

Australia’s RCM mark and state-based WHS plant registration requirements are not as straightforward as they initially appear, particularly for complex industrial automation systems that incorporate multiple sub-assemblies each potentially requiring separate compliance treatment. Engage a specialist Australian compliance consultant before your first product shipment and budget realistically for compliance costs in your Australian pricing model.

💰

High Operational Costs

Australia has high labour costs, compulsory superannuation contributions (11.5% of gross salary), mandatory workers’ compensation insurance, payroll tax (state-based), and GST compliance costs that add 30–40% to base labour costs compared to many other markets. If establishing a Pty Ltd with Australian employees, model these costs realistically in your Australian P&L before committing to the structure. Distributor partnerships avoid these costs entirely for the international company.

🔒

Defence Security & Export Control Requirements

Australia’s defence market requires careful navigation of security frameworks, DISP membership for suppliers, personnel security clearances for certain project roles, and Australian export control laws (Defence Export Controls, governed by the Defence Trade Controls Act) that restrict certain dual-use technologies. If your automation technology has any defence or dual-use application, obtain Australian export control legal advice before engaging any Australian partners or providing technical data.

SECTION 12

12 How GTsetu Connects You with Verified Australian Partners

🇦🇺 GTsetu, Verified B2B Platform for Australia Market Entry

Discover Verified Australian Manufacturers & Distributors, No Broker Commission

GTsetu provides international manufacturing and industrial automation companies with direct access to compliance-verified Australian manufacturers, distributors, system integrators, and technology partners, across every industrial sector and all major Australian manufacturing regions. Every company in GTsetu’s Australia network has been verified through ASIC registration, ABN documentation, relevant industry certifications (ISO, DISP, sector-specific), and authority letter confirmation before appearing in the platform. You discover, qualify, and engage with verified Australian partners, without broker intermediaries taking a cut of your commercial economics.

🏛️

Multi-Layer Compliance Verification

Every Australian partner on GTsetu has been verified: ASIC registration, ABN, certifications, sector credentials, by GTsetu’s compliance team. Eliminates fraud risk and due diligence workload.

🕵️

Anonymous Discovery

Browse verified Australian partner profiles without revealing your identity. Protect your Australia market entry strategy until you choose to engage.

📄

Built-In NDA Workflow

Digital mutual NDA with timestamped signatures activated before sensitive technical or commercial data can be exchanged. Governed by Australian or mutually agreed law.

🔐

Encrypted Document Workspace

AES-256 encryption at rest, TLS in transit. Role-based access controls. Full audit trail. Australian Privacy Act-compliant data handling. Exchange product specs and pricing securely.

🚫

Zero Broker Commission

GTsetu charges zero commission on any partnership formed between international manufacturers and Australian distributors or partners. All commercial economics stay between you and your partner.

🌏

100+ Countries Including Australia

GTsetu’s verified network covers all major Australian industrial regions as well as global markets, supporting your Australia entry today and expansion into India, Germany, and beyond tomorrow.

QWhy should I expand my manufacturing or industrial automation business to Australia?

Australia offers a compelling combination of market quality, government support, and structural demand that is unique among APAC markets. It is a stable, English-speaking, high-income developed market with transparent regulations, strong IP protection, and one of the world’s most favourable business environments for foreign companies, incorporating a Pty Ltd takes 1–3 business days with no minimum capital. The A$15 billion National Reconstruction Fund is driving manufacturing investment across seven priority sectors, and Australia’s high labour costs create powerful automation ROI economics that make the business case for automation solutions compelling at every scale of manufacturer. Australia also has one of the world’s highest industrial robot deployment rates, the most advanced autonomous mining operations globally, and 15+ free trade agreements making Australian operations a natural APAC export platform. See the broader context in our company global expansion guide.

QWhat are the best entry models for expanding an automation business to Australia?

For most first-time Australia entrants in industrial automation, the recommended entry sequence is: (1) Appoint a verified Australian national distributor or sector-specialist channel partner, fastest market access (3–9 months to first revenue) with minimal capital. (2) After 2–3 years of validated Australian market presence and revenue, evaluate establishing a Pty Ltd for greater market control and direct customer relationships. (3) For defence and government market access, a Pty Ltd and DISP-registered partner network are typically required for qualifying opportunities. Australian Pty Ltd incorporation is one of the world’s fastest and simplest, 1–3 business days through ASIC, but ongoing operational costs (superannuation, payroll tax, workers compensation, GST compliance) require realistic financial modelling. Technology licensing to an Australian partner is appropriate where local manufacturing capability is strategically important. See our full comparison in market entry partnerships and licensing vs. distribution agreements.

QWhat is the National Reconstruction Fund and how does it benefit foreign manufacturers?

Australia’s National Reconstruction Fund (NRF) is a A$15 billion government investment facility providing concessional loans, equity investments, and guarantees to support manufacturing capability in seven priority sectors: resources technology and critical minerals processing, food and beverage, medical science, clean energy, defence, transport, and enabling capabilities including advanced manufacturing and industrial automation. Foreign companies incorporated as Australian Pty Ltd entities can apply for NRF financing for qualifying investments that create Australian manufacturing capability. Unlike India’s PLI scheme (direct production incentives), the NRF operates as a concessional financing vehicle, reducing the cost of capital for qualifying investments. For automation technology companies, the NRF is primarily a demand signal: every NRF-approved manufacturer expanding production is a qualified buyer of automation, control, and monitoring solutions. Austrade provides free facilitation for companies seeking NRF introductions and qualified investment opportunities.

QWhat RCM and regulatory compliance is required to sell industrial automation products in Australia?

The key compliance requirements for selling industrial automation products in Australia are: (1) RCM mark (Regulatory Compliance Mark), mandatory for electrical, electronic, and telecommunications equipment; replaces the former C-Tick and A-Tick marks. Requires testing against applicable AS/NZS standards, self-declaration of conformity, and registration in the ERAC database. Allow 2–6 months and budget for testing costs. (2) WHS (Work Health and Safety) compliance, Australian importers of industrial plant (machinery and equipment) are legal duty-holders under WHS legislation; plant design registration may be required with state WHS regulators for certain equipment categories. (3) Australian Consumer Law (ACL), automatic statutory guarantees apply to goods supplied in trade or commerce; warranty policies must address ACL guarantees. (4) Australian Privacy Act, for connected automation systems processing personal data of Australian individuals. (5) For defence-related products, Defence Export Controls and DISP requirements. Engage an Australian compliance specialist for a gap assessment against your specific product range before committing to a market launch timeline.

QHow do I find a verified distributor for industrial automation products in Australia?

The most efficient and secure route to finding a verified Australian industrial automation distributor is through GTsetu’s compliance-verified B2B platform, where every company has been verified through ASIC registration, ABN, and industry certifications before appearing in the network, with anonymous discovery, built-in NDA workflow, and encrypted collaboration at zero broker commission. Supplement with targeted trade show engagement at AUSTECH (precision engineering and advanced manufacturing) and AIMEX (mining equipment). Engage Austrade for facilitated introductions and market intelligence, free for international companies entering Australia. Contact Ai Group for Ai Group member introductions in your target sector. Always verify candidates independently, ASIC registration at asic.gov.au, ABN at abr.business.gov.au, before sharing product specifications or pricing. Review our guides on finding international distributors and distributors and manufacturers frameworks.

QWhich sectors in Australia have the highest industrial automation investment demand?

The sectors with the highest industrial automation investment demand in Australia in 2026 are: (1) Mining and resources, the world’s most advanced autonomous mining operations (BHP, Rio Tinto, Fortescue) drive outsized automation demand; Pilbara iron ore operations and Goldfields mining have the highest automation investment per facility globally. (2) Food and beverage processing, NRF-funded expansion in meat, dairy, seafood, and grain processing is driving packaging and quality inspection automation investment. (3) Defence manufacturing, AUKUS submarine, guided weapons, and sovereign capability investment is driving demand for precision assembly automation, NDT systems, and electronics manufacturing. (4) Medical devices and pharmaceuticals, post-COVID domestic capability investment is driving TGA-compliant filling, serialisation, and cleanroom automation. (5) Clean energy and critical minerals, lithium processing, green hydrogen, and battery materials production require advanced process automation. Victoria (Melbourne, defence, advanced manufacturing), Western Australia (Perth, mining), New South Wales (Sydney, life sciences), and South Australia (Adelaide, defence, naval) are the highest-priority geographic clusters for most automation companies.

QWhat commercial terms should I negotiate carefully in an Australia distribution agreement?

Australia-specific commercial terms requiring careful negotiation: (1) AUD pricing and exchange rate risk allocation, AUD can move 10–15% against USD/EUR annually; define price review mechanisms explicitly. (2) GST treatment on all transaction types, ensure invoicing and pricing structures are GST-compliant from day one. (3) RCM compliance responsibility, specify who bears RCM registration costs, maintenance, and renewal; and who is the legal importer of record with WHS duty-holder responsibility. (4) Payment terms, standard Australian commercial terms are 30 days EOM; start with advance payment or LC for first transactions before establishing open account credit. (5) Remote area service coverage, define FIFO service commitment, cost allocation, and response time SLAs for remote industrial sites. (6) Exclusivity structure, consider sector-specific rather than national exclusivity for first partnerships. (7) Annual volume commitments calibrated to Australian market development timelines (12–24 months for major mining or defence account qualification). (8) Termination and exit provisions, specify buyback obligations, transition assistance, and notice periods explicitly. See our complete guides on exclusivity clauses, termination clauses, and manufacturer-distributor contracts.

Ready to Expand Your Manufacturing Business to Australia?

Connect with verified Australian manufacturers, distributors, and technology partners on GTsetu, with compliance-backed verification, anonymous discovery, built-in NDA workflows, and zero broker commissions on every Australia market partnership you form.

They represents the product, and research team behind GTsetu, a global B2B collaboration platform built to help companies explore cross-border partnerships with clarity and trust. The team focuses on simplifying early-stage international business discovery by combining structured company profiles, verification-led access, and controlled collaboration workflows.

With a strong emphasis on trust, and disciplined engagement, Team GTsetu shares insights on global trade, partnerships, and cross-border collaboration, helping businesses make informed decisions before entering deeper commercial discussions.