Direct Answer: A limited liability partnership contract template is the written agreement between the partners (called “members” in the UK) of an LLP that sets out capital contributions, profit and loss sharing, management roles, admission and exit of partners, and dissolution, replacing the generic statutory default rules that apply automatically if no agreement exists. It differs from a limited partnership contract template, which must separate the unlimited liability of a “general partner” who manages the business from the passive, capped liability of “limited partners” who cannot take part in management without losing that protection. Below is the full clause-by-clause structure, a downloadable template outline, and the jurisdiction-specific points to check (UK, India, US) before two or more partners sign.

📅 June 8, 2026⏱ 19 min read✍️ GT Setu Editorial Team🔄 Updated regularly

15+

Standard Clauses In a Complete LLP Template

2

Minimum Partners Required to Form an LLP

2

Designated Members Required Under UK LLPA 2000

0%

GTsetu Broker Commission on Verified Partner Discovery

Searching for a “limited liability partnership contract template” usually means one of two things: you’re about to go into business with someone and need to document how that relationship will actually work, or you’ve found a generic template online and aren’t sure whether it covers what you need. Both situations carry the same risk, an LLP agreement that looks complete on the surface but is silent on the one issue that eventually causes a dispute: how profits get split when contributions are unequal, what happens when a partner wants out, or who actually has the authority to sign a contract on the partnership’s behalf.

This guide breaks the limited liability partnership contract template down clause by clause, explains exactly how it differs from a limited partnership contract template (a related but legally distinct structure), and covers what a partnership contract template UK users need looks like under the Limited Liability Partnerships Act 2000, alongside the equivalent requirements in India and the US. If you’re forming a partnership specifically to collaborate with a manufacturing, distribution, or technology partner rather than a professional services firm, see our companion guides on the business partnership contract and contract between manufacturer and distributor for commercially-specific clause guidance.

⚖️ Who Is This Guide For?

This guide is written for founders, professional partners (accountants, consultants, architects), and small business owners who are forming or restructuring as an LLP or limited partnership and need to understand what their contract template should contain before they sign. It is educational in nature, it explains the standard structure and clauses found across publicly available LLP agreement templates and statutory frameworks, but it is not a substitute for jurisdiction-specific legal advice. For partnerships formed around a specific commercial relationship, joint ventures, distribution, or technology partnerships, see our guides on technology partnerships and cross-border business partnerships.

SECTION 1

1 What Is a Limited Liability Partnership Contract Template?

🎯 The Core Definition

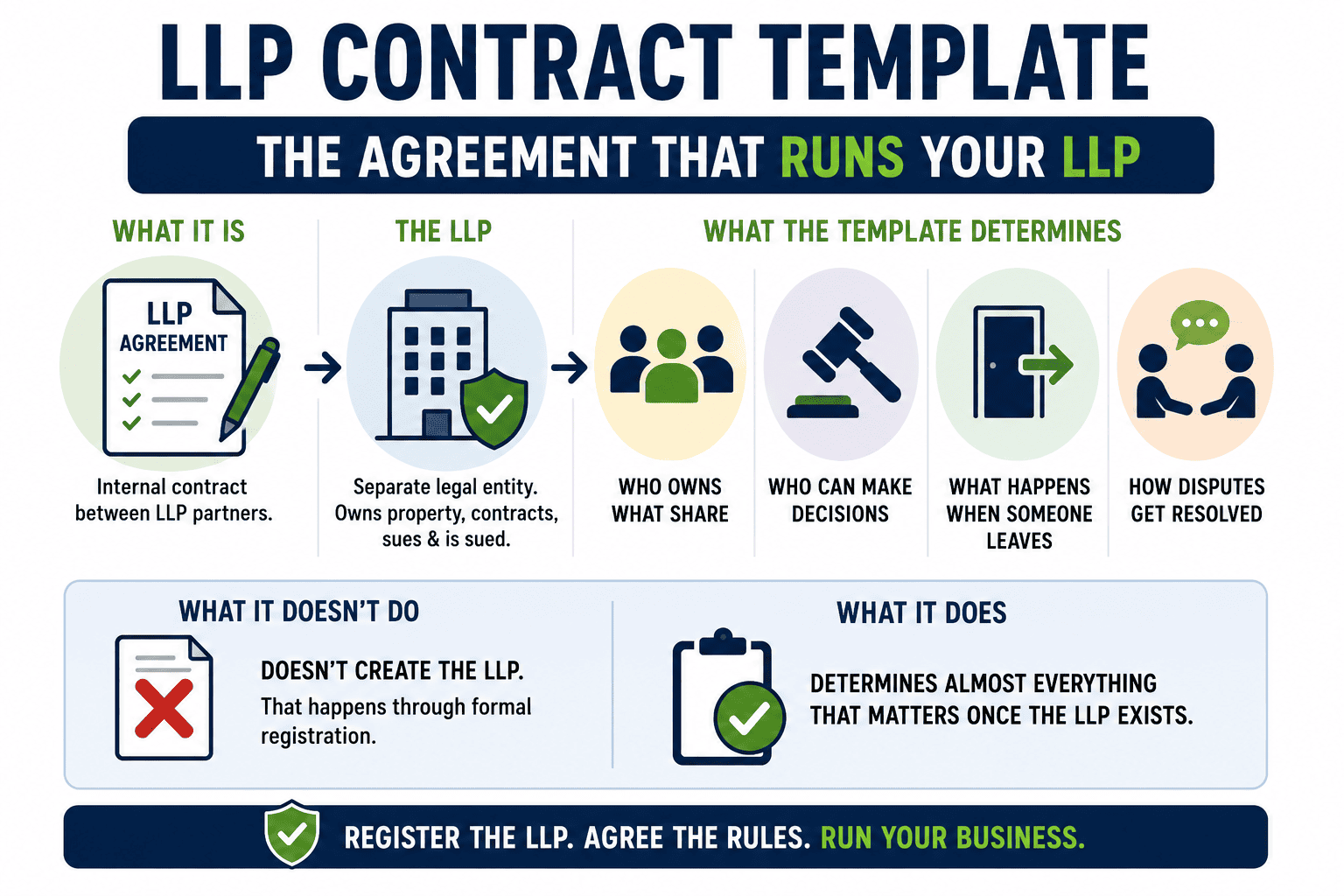

A limited liability partnership contract template, also called an LLP agreement or, in the UK, a members’ agreement, is the internal contract between the partners of an LLP that governs how the business actually runs. An LLP itself is typically a separate legal entity (distinct from its partners) that can own property, enter contracts, and sue or be sued in its own name. The contract template doesn’t create the LLP, that happens through formal registration with the relevant company or partnership registrar, but it determines almost everything that matters once the LLP exists: who owns what share, who can make decisions, what happens when someone leaves, and how disputes get resolved.

🏢

Separate Legal Entity

Unlike a general partnership, an LLP usually has “unlimited capacity”, it can do almost anything a natural person could do, including holding property and entering contracts in its own name. The contract template governs the internal relationship; it doesn’t need to be filed publicly in most jurisdictions.

🛡️

Limited Liability for All Partners

Every partner’s personal liability is normally capped at the amount they’ve agreed to contribute, a meaningful structural difference from a general partnership, where every partner is personally exposed for the firm’s debts and the misconduct of other partners.

📝

Not Always Legally Required

In most jurisdictions, partners are not legally obliged to have a written agreement to incorporate an LLP. But without one, generic default statutory rules apply automatically, and they are rarely what real partners would have chosen if asked.

🔄

Tax-Transparent Structure

In most jurisdictions, an LLP itself doesn’t pay tax on its profits. Profits flow through to each partner, who is taxed individually, much like a traditional partnership, even though the liability protection resembles that of a company.

👥

Minimum Two Partners

An LLP needs at least two partners to exist. If membership drops to one for an extended period in some jurisdictions, this can put the LLP’s continued existence at risk, a structural point worth flagging in the agreement’s withdrawal provisions.

🖋️

Internal Flexibility, External Formality

While the LLP itself must be formally incorporated with a registrar, the internal contract between partners is largely a private matter, giving partners significant flexibility to structure profit sharing, decision rights, and exit terms however suits their actual business arrangement.

SECTION 2

2 LLP vs. Limited Partnership Contract Template: Key Differences

“Limited liability partnership” and “limited partnership” sound similar and are frequently confused, but they are legally distinct structures with materially different contract templates. Getting this wrong at the drafting stage can mean a partner unknowingly takes on personal liability they thought they were protected from.

Allocate management rights and profit shares between equals

Draw a hard line between management/liability and passive capital

Annual accounts / filing burden

Similar to a company in most jurisdictions

Lighter, often no accounts or agreement filing required

⚠️ The Single Biggest Drafting Risk

In a limited partnership, a limited partner who takes any active role in managing the business, making binding decisions, directing operations, signing on the partnership’s behalf, can lose their limited liability protection automatically and become exposed as if they were a general partner. A limited partnership contract template must define the boundary between “investing capital” and “managing the business” with precision, because the law does not give partners a second chance to fix this after the fact. If your structure involves investors who want to remain passive, see our guide on risk allocation in cross-border deals for how liability boundaries are typically documented.

SECTION 3

3 Why You Need a Written Agreement (Even If It’s Not Mandatory)

Across most jurisdictions, there is no strict legal requirement for partners to sign a written LLP agreement before incorporating. Many partners, particularly first-time founders, assume that because incorporation is the “official” step, the internal agreement is optional paperwork they can skip or handle informally. This is the single most common and most expensive mistake in LLP formation.

⚖️

Default Rules Apply Automatically, And They’re Generic

In the UK, the Limited Liability Partnerships Regulations 2001 set out default provisions that apply whenever no agreement exists, or where the agreement is silent on a particular point. The defaults include rules such as all partners sharing equally in capital and profits, regardless of how much each partner actually contributed, and no power to expel a member, even for serious misconduct.

Statutory Risk

💰

Equal Profit Shares Rarely Match Reality

If one partner contributes 80% of the capital and another contributes 20%, default equal-sharing rules mean both walk away with the same share of profit, a mismatch that becomes a serious point of conflict the moment the business starts generating real money.

Financial Risk

🚪

No Expulsion Mechanism Without an Express Clause

Without an explicit expulsion clause, a partner cannot be forced to leave the LLP under most default frameworks, even where there’s been a serious breach of duty, fraud, or conduct that’s actively damaging the business. This single gap can leave the remaining partners with no practical exit short of dissolving the entire entity.

Governance Risk

🤝

No Fiduciary Duty Unless You Write One In

Courts in some jurisdictions have held that LLP members do not automatically owe each other a fiduciary duty of good faith unless that duty is expressly stated in the agreement, a meaningful gap compared with traditional partnership law, where such duties are typically assumed.

Legal Risk

📊

Drawings vs. Profit Misalignment

A recurring real-world problem: partners agree informally on monthly “drawings” (cash withdrawals) that don’t actually line up with the LLP’s working capital needs or its real profit performance, leading to cash shortfalls that a properly drafted distribution clause would have anticipated and prevented.

Cash Flow Risk

💡 The Practical Takeaway

Treat any limited liability partnership contract template you find online as a structured checklist, not a finished document. The value of a template is that it shows you which clauses exist and roughly how they’re worded, not that the specific numbers, percentages, or default language inside it match your actual arrangement. Walk through every clause and ask: “does this reflect what we’ve actually agreed, or is this just boilerplate?”

SECTION 4

4 Clause-by-Clause: What Every LLP Contract Template Must Cover

Below is the standard clause structure found across LLP agreement templates and statutory drafting guides. Not every clause applies to every partnership, a two-person consulting LLP needs less than a multi-partner professional firm, but each should at least be considered and deliberately included or excluded, rather than silently omitted.

🏷️Foundational

Name, Registered Office & Business Purpose

The LLP’s legal name (subject to registrar approval), the registered office address, and a clear description of the business the LLP will carry on. Most templates also state where the LLP is permitted to operate and whether it covers regulated activities, relevant for professional services firms.

Sets the legal identity and operating scope

💵Capital

Capital Contributions

Each partner’s initial capital contribution, in cash or in kind (property, equipment, services), and the rules for additional capital calls: when they can be required, whether interest applies, and what happens if a partner can’t or won’t pay an additional call.

Defines who put in what, and what happens if more is needed

📊Most Disputed

Profit & Loss Sharing

The ratio in which profits and losses are shared, which does not have to mirror the capital contribution ratio. Many agreements use a different formula for profit (rewarding effort or revenue generation) versus loss (tied to capital at risk). Specify distribution timing: end of financial year, quarterly, or another agreed cadence.

The clause most likely to cause conflict if left as a generic default

🧭Governance

Management, Roles & Decision-Making

Who manages day-to-day operations, what decisions require unanimous consent versus a majority vote, and (in the UK) which partners are “designated members” responsible for statutory filings and compliance. If no designated members are chosen, all partners are deemed designated by default, removing any distinction in responsibility.

Prevents deadlock and clarifies who can bind the LLP

🗓️Operational

Meetings & Voting Procedures

Minimum frequency of partner meetings (commonly quarterly), notice periods, quorum requirements, and how voting works, whether by headcount or weighted by profit-sharing ratio. Specify what happens when partners can’t reach consensus on a non-routine decision.

Provides a clear escalation path before disputes become deadlocks

➕Growth

Admission of New Partners

The process for bringing in a new partner: consent threshold required from existing partners, how the new partner’s capital contribution and profit share are determined, and any conditions (e.g. minimum tenure before admission, restrictive covenant sign-on).

Controls who can join and on what terms

🚶Critical

Resignation, Retirement & Expulsion

Notice period for voluntary resignation; retirement age or conditions if applicable; and, crucially, an express expulsion mechanism for cause (misconduct, breach of agreement, conduct detrimental to the LLP). Without this clause, a partner generally cannot be forced out under default rules, regardless of behaviour.

The clause most often missing from free generic templates

💸Exit Mechanics

Valuation & Payout on Departure

How a departing partner’s interest is valued (net asset value, a multiple of profits, or an independent expert valuation), whether goodwill is included, and the payment structure, lump sum or instalments, with or without interest and security.

Avoids costly post-exit valuation disputes

🔒Protective

Restrictive Covenants

Reasonable non-compete, non-solicitation of clients and staff, and confidentiality obligations, tailored to the specific sector and geography, since overly broad restrictive covenants risk being unenforceable. See our guide on force majeure provisions for how protective clauses are typically scoped in commercial agreements more broadly.

Protects the remaining business after a partner departs

🛡️Risk Allocation

Indemnity Provisions

Each partner typically indemnifies the LLP and other partners for losses caused by their own negligence, breach of duty, or misconduct, while the LLP in turn often indemnifies partners for liabilities incurred in the ordinary and proper conduct of its business.

Defines who bears the cost when something goes wrong

🏛️Wind-Down

Dissolution & Asset Distribution

The process for voluntary dissolution (typically by partner consent or under statute), and the priority order for distributing assets on wind-down: first settling LLP liabilities, then returning capital contributions, then distributing any remaining surplus per the profit-sharing ratio.

Sets the end-state rules before anyone needs them

⚔️Resolution

Dispute Resolution & Governing Law

A staged dispute resolution process, typically requiring good-faith negotiation first, then mediation or arbitration before litigation, plus the governing law and exclusive jurisdiction for any dispute that does reach court. See our guide on risk allocation in cross-border deals for how this is handled when partners are based in different countries.

Below is a representative outline of how a limited liability partnership contract template is typically structured, based on common drafting conventions across publicly available templates. Treat the bracketed text as fields to be completed and reviewed, not as legal advice for your specific situation.

RECITALS, This Limited Liability Partnership Agreement (“Agreement”) is made on [date] by and between [Partner 1 Name], residing at [Address] (“First Partner”), and [Partner 2 Name], residing at [Address] (“Second Partner”), collectively the “Partners,” who wish to form a Limited Liability Partnership for the purpose of carrying on the business described below.

1. NAME, The name of the LLP shall be [LLP Name], subject to approval from the relevant Registrar.

2. REGISTERED OFFICE, Located at [Registered Office Address], or such other place as the Partners may agree.

3. BUSINESS, The LLP shall carry on the business of [Nature of Business] and any other business mutually agreed, subject to applicable law.

4. COMMENCEMENT, The LLP’s business and this Agreement take effect upon issue of the Certificate of Incorporation.

5. CONTRIBUTIONS, Initial capital: First Partner [Amount]; Second Partner [Amount]. Additional contributions, if required, shall be made in proportion to each Partner’s existing contribution unless otherwise agreed. No interest on capital unless mutually agreed.

6. PROFIT & LOSS SHARING, Profits and losses shared: First Partner [%]; Second Partner [%]. Distributed at the end of each financial year or as the Partners agree.

7. RIGHTS & DUTIES, Each Partner shall act in the LLP’s best interest, avoid competing activity, and provide truthful accounts of all related transactions. Significant decisions require mutual consent.

8. MEETINGS & DECISIONS, Partners meet at least [quarterly], with [7] days’ notice. Decisions by mutual agreement, falling back to a majority vote weighted by profit share if consensus fails.

9. ADMISSION OF NEW PARTNERS, By mutual consent of existing Partners, with capital contribution and profit share agreed in writing at the time of admission.

10. RESIGNATION, RETIREMENT & EXPULSION, Resignation: [X] days’ written notice. Retirement: at age [X] or by mutual consent. Expulsion: for just cause (misconduct, breach, conduct detrimental to the LLP), decided by mutual consent of remaining Partners.

11. DISSOLUTION, By mutual consent or under applicable law. On dissolution, proceeds applied in order: (i) LLP liabilities, (ii) return of capital, (iii) remaining surplus per profit-sharing ratio.

12. INDEMNITY, Each Partner indemnifies the LLP and other Partners against losses caused by their own negligence, breach of duty, or misconduct.

13. DISPUTE RESOLUTION, Good-faith negotiation first; unresolved disputes after [30] days referred to arbitration under [applicable arbitration law].

14. GOVERNING LAW, This Agreement is governed by the laws of [Jurisdiction]; courts of [City] have exclusive jurisdiction.

15. AMENDMENTS, This Agreement may be amended only by written consent of [all / a specified majority of] Partners.

💡 Adapting This Structure to a Limited Partnership

If you’re drafting a limited partnership contract template instead, the same numbered structure largely applies, but Clause 7 (Rights & Duties) and Clause 8 (Decision-Making) must be rewritten to give management authority exclusively to the General Partner(s), with Limited Partners explicitly restricted from binding decisions or day-to-day operations. Clause 6 (Profit Sharing) commonly adds a priority order, the General Partner often receives a management fee deducted from income before remaining profits are distributed to Limited Partners.

SECTION 6

6 Partnership Contract Template UK: Specific Requirements

A partnership contract template UK businesses use must work within the framework of the Limited Liability Partnerships Act 2000 (LLPA 2000) and the Limited Liability Partnerships Regulations 2001 (LLPR 2001). The UK terminology and several structural points differ from generic international templates, so a template drafted for another jurisdiction should not be used unmodified.

01

“Members,” Not “Partners”, Though Both Terms Are Used in Practice

The LLPA 2000 formally refers to the owners of a UK LLP as “members,” even though they are commonly called “partners” in everyday business language. A precise template should use “member” in the formal defined terms while noting that “partner” may be used interchangeably for convenience, avoiding ambiguity about which legal framework applies.

02

Two Designated Members Are Mandatory

A UK LLP must have at least two “designated members” who carry specific statutory responsibilities, including filing annual accounts and confirmation statements with Companies House. If the members do not actively designate specific individuals in the agreement, UK law deems all members to be designated members by default, with no distinction in responsibility between them. A well-drafted template should name designated members explicitly if a distinction is intended.

03

Mandatory Incorporation at Companies House

Unlike a general partnership, a UK LLP does not exist as a legal entity until incorporation documents are filed, the fee is paid, and Companies House issues a certificate of incorporation. Members of a general partnership can inadvertently expose themselves to unlimited personal liability by trading before formalities are complete, LLP members do not get limited liability protection until incorporation is confirmed.

04

People with Significant Control (PSC) Regime

UK LLPs fall within the Persons of Significant Control regime, meaning the LLP must identify and file details of anyone with significant control over it, broadly, someone holding more than 25% of the rights to surplus assets or voting rights, or who otherwise has significant influence. This is a public filing obligation separate from the LLP agreement itself, but the agreement should be drafted with PSC disclosure obligations in mind.

05

Economic Crime and Corporate Transparency Act 2023 (ECCTA) Reforms

Recent UK reforms under ECCTA introduce identity verification requirements for LLPs, alongside related changes affecting limited partnerships under the Limited Partnerships Act 1907. A current partnership contract template UK businesses use should reflect these updated identity verification and transparency obligations rather than relying on pre-reform drafting.

06

UK GDPR & Data Protection Clause

If the LLP handles client data, which is common for professional services firms, the agreement should reference compliance with UK GDPR and the Data Protection Act 2018, and most LLPs should maintain a clear, published privacy policy as a matter of good governance even where not directly mandated by the agreement itself.

⚖️ UK Limited Partnership Distinction

If you are instead forming a UK limited partnership (LP) rather than an LLP, note that this is governed by an entirely different statute, the Limited Partnerships Act 1907, as amended by ECCTA 2023, and registered separately with Companies House. English and Welsh limited partnerships are not separate legal entities (Scottish limited partnerships are an exception), meaning the LP itself cannot hold property or sign contracts directly, only the General Partner can, acting on the LP’s behalf. A limited partnership contract template for the UK market must reflect this entity-status difference clearly, since it affects how the partnership holds and transfers assets.

SECTION 7

7 LLP Agreement Requirements by Jurisdiction

While the core clause structure of a limited liability partnership contract template is broadly similar worldwide, the underlying statutory framework, terminology, and filing obligations differ meaningfully by country. Always confirm which framework applies before adapting a generic template.

🇬🇧 United Kingdom

Governed by the LLPA 2000 and LLPR 2001. Owners are called “members.” Minimum two designated members required. Incorporation at Companies House is mandatory before the LLP exists. PSC regime and ECCTA 2023 identity verification apply.

Default rules: equal profit/capital shares; no expulsion power without an express clause

🇮🇳 India

Governed by the Limited Liability Partnership Act, 2008. The LLP Agreement must typically be filed with the Registrar of LLPs within 30 days of incorporation (Form 3), unlike the UK, where the agreement is private. Owners are called “partners.”

Disputes commonly referred to arbitration under the Arbitration and Conciliation Act, 1996

🇺🇸 United States

LLP law is set at the state level, not federally, and historically LLPs were often restricted to licensed professional service businesses (law, accounting, architecture, medicine) in many states, though this has broadened over time. Filing requirements and naming conventions vary significantly by state.

Federal tax treatment: Form 1065 partnership return plus a Schedule K-1 per partner

🌍 Cross-Border Partnerships

Where partners are based in different countries, the agreement should specify governing law and jurisdiction explicitly rather than leaving it ambiguous, and should address currency, tax residency, and cross-border enforcement of restrictive covenants. See our guide on cross-border business partnerships for the broader structuring considerations.

Always confirm enforceability of arbitration clauses in each partner’s home jurisdiction

SECTION 8

8 Common Mistakes in Free Templates & How to Avoid Them

⚖️

Equal Split by Default, Not by Design

Many free templates pre-fill 50/50 or equal-share clauses simply because that’s the simplest example to show. If your actual contributions, time commitment, or risk exposure are unequal, copying this default without adjusting it bakes in unfairness from day one.

🚪

Missing or Vague Expulsion Clause

A generic template may include a resignation clause but omit expulsion entirely, or describe it so vaguely (“for cause”) that it offers no real protection. Define specific trigger events and the exact decision-making threshold required to expel a partner.

💸

No Real Valuation Methodology

“The departing partner’s share will be valued fairly” is not a valuation clause, it’s an invitation to dispute. Specify net asset value, a profit multiple, or a named independent valuer mechanism, and state clearly whether goodwill is included.

🌍

Wrong Jurisdiction’s Statutory References

A template drafted for US state law referencing “Articles of Organization” or citing the wrong arbitration statute for your country is a clear sign it wasn’t built for your jurisdiction, even if the general clause structure looks reasonable.

🔏

No Restrictive Covenants, or Covenants Too Broad to Enforce

Templates either omit non-compete and confidentiality clauses entirely, or include sweeping worldwide, indefinite restrictions that courts are likely to strike down as unenforceable. Tailor scope, geography, and duration to what’s actually reasonable for your sector.

📑

Treating the Template as Final, Not a Draft

The most common mistake of all: filling in the blanks of a free template and signing it without review, rather than using it as a structured starting point for a conversation about what the partners actually want, then having it checked by a lawyer in the relevant jurisdiction.

SECTION 9

9 Exit, Valuation & Dispute Resolution Clauses

Most disputes that end up in court were entirely foreseeable at the drafting stage, they just weren’t addressed clearly enough in the original agreement. The exit and dispute resolution clauses deserve the most careful attention precisely because they only get tested when the relationship between partners has already become strained.

Exit Scenario

What the Clause Should Specify

Why It Matters

Voluntary resignation

Required notice period; whether resignation can be blocked or delayed; effect on ongoing client/customer relationships the partner managed

Prevents a sudden departure from disrupting the business with no transition runway

Retirement

Retirement age or trigger conditions (if used); whether retirement terms differ from ordinary resignation (e.g. more favourable payout)

Distinguishes planned succession from disputed exits

Expulsion for cause

Specific trigger events; voting threshold required among remaining partners; right of the expelled partner to respond before a final decision

The only mechanism that allows partners to remove someone who is actively harming the business

Valuation of departing interest

Valuation method (net asset value / profit multiple / independent expert); whether goodwill is included; date used for valuation

Removes the single most common source of post-exit litigation

Payment terms on exit

Lump sum vs. instalments; interest on deferred payment; security for payment; right of set-off against amounts owed to the LLP

Protects the LLP’s cash flow while ensuring the departing partner is actually paid

Clawback for undisclosed liabilities

Mechanism to adjust a departing partner’s payout if liabilities they were responsible for surface after they’ve left

Prevents a partner from leaving just before a problem they caused becomes visible

Dispute resolution

Staged process: good-faith negotiation, then mediation, then arbitration before litigation; named arbitration body and rules

Faster, cheaper, and more private than going straight to court

💡 Mediation Before Arbitration, Arbitration Before Court

A well-drafted dispute resolution clause typically requires partners to attempt direct negotiation first, escalate to mediation if that fails, and only proceed to binding arbitration (or litigation, in jurisdictions where that’s preferred) as a last resort. This staged approach is faster and cheaper than going straight to court, and it preserves the working relationship in cases where the partnership ultimately continues. For commercial partnerships specifically, as opposed to professional LLPs, see our guide on risk allocation in cross-border deals for how dispute clauses are adapted when partners operate in different legal systems.

SECTION 10

10 When to Use an LLP vs. Other Partnership Structures

Before drafting any contract template, confirm that the LLP structure actually fits your situation. The three most common partnership structures, general partnership, limited partnership, and LLP, serve different purposes, and choosing the wrong one means re-papering the entire relationship later.

Structure

Best Suited For

Liability Profile

Formation Complexity

General Partnership

Simple, low-risk ventures between trusted parties; no formal registration in many jurisdictions

Unlimited personal liability for all partners, joint and several

Very low, often no filing required, though a written agreement is still strongly advisable

Limited Partnership (LP)

Investment funds, joint ventures with passive investors, structures where some parties want capital exposure only

General partner(s): unlimited. Limited partner(s): capped at investment, provided they stay passive

Moderate, registration required; lighter accounts/filing burden than an LLP in many jurisdictions

Limited Liability Partnership (LLP)

Professional services firms, founder teams wanting flexible profit-sharing with liability protection, trading businesses with multiple active partners

All partners limited, typically capped at their agreed contribution

Higher, formal incorporation, ongoing filing obligations similar to a company in many jurisdictions

If your structure instead involves a manufacturing relationship, a distribution agreement, or a technology licensing arrangement rather than co-ownership of a single business, a partnership contract template may not be the right starting point at all, you likely need a commercial agreement instead. See our guides on OEM vs. ODM vs. EMS, white-label vs. private label manufacturing, and contract between manufacturer and distributor to identify the right framework for a commercial (rather than ownership) relationship.

SECTION 11

11 Verifying a Prospective Partner Before You Sign

A contract template, however carefully drafted, only protects you from the risks you can anticipate on paper. It does nothing to verify that the person or company you’re about to sign with is who they claim to be, has the financial standing they represent, or doesn’t have an undisclosed conflicting business relationship. This verification step matters just as much as the clauses themselves, particularly where the prospective partner is based in a different city, state, or country.

Confirm business registration status independently, don’t rely solely on documents the prospective partner provides you

Verify tax registration and any required professional licences for regulated activities

Check for existing competing business interests or conflicting partnership commitments

Request financial references appropriate to the scale of capital contribution being discussed

Use a mutual non-disclosure agreement before sharing sensitive business plans, client lists, or financial details

If the partnership spans borders, confirm how disputes would actually be enforced in each partner’s home jurisdiction

⚖️ Why This Matters More for Commercial Partnerships

If the “partnership” you’re forming is really a vehicle for a broader commercial relationship, say, a joint venture to manufacture or distribute a product internationally, the verification burden is significantly higher than it is for, say, two local consultants forming a professional LLP. Cross-border commercial partnerships carry currency, regulatory, and enforcement complexity that a domestic professional LLP simply doesn’t face. See our guides on partnership evaluation criteria and international wholesale distributors for the due diligence framework typically used in these situations.

SECTION 12

12 How GTsetu Helps Partners Verify Each Other First

🤝 GTsetu, Verified B2B Partner Discovery, Before the Contract

Find and Verify a Business Partner Before You Ever Draft an Agreement

Most disputes traced back to a flawed limited liability partnership contract template actually started earlier, with two parties who didn’t properly verify each other before agreeing to partner in the first place. GTsetu addresses that earlier step: a compliance-verified B2B platform where every company has been checked through business registration, tax ID, licensing, and industry certification before they ever appear in the network. Whether you’re forming an LLP with a domestic co-founder or structuring a cross-border manufacturing or distribution partnership, GTsetu lets you discover and qualify a prospective partner anonymously, execute an NDA before sharing sensitive details, and only then move to drafting the formal agreement, with zero broker commissions on whatever partnership you ultimately form.

🏛️

Pre-Verified Business Identity

Every company on GTsetu has been checked against business registration, tax ID, and licensing records before appearing in the network, reducing the due diligence burden before you draft anything.

🕵️

Anonymous Discovery

Evaluate a prospective partner’s profile and credentials without revealing your own identity or intentions until you choose to engage directly.

📄

Built-In NDA Workflow

A digital mutual NDA with timestamped signatures is in place before any sensitive business or financial information is exchanged, ahead of any partnership agreement drafting.

🔐

Encrypted Document Workspace

Share financial references, business plans, and early draft terms through an AES-256 encrypted workspace rather than unprotected email.

🚫

Zero Broker Commission

GTsetu charges no commission on any partnership formed through the platform, the commercial terms stay strictly between you and your partner.

🌏

Cross-Border Ready

For partnerships spanning multiple countries, GTsetu’s verified network and our B2B matchmaking tool help surface and qualify candidates before commercial or legal terms are negotiated.

QWhat is a limited liability partnership contract template?

A limited liability partnership contract template is a structured document, also called an LLP agreement or, in the UK, a members’ agreement, that records how the partners of a limited liability partnership will run the business together. It typically covers capital contributions, profit and loss sharing, management and decision-making, admission of new partners, retirement and expulsion, and dissolution. While most jurisdictions do not legally require a written LLP agreement, without one default statutory rules apply automatically, and those defaults are usually generic and rarely match what real partners actually intend, such as assuming all partners share profits equally regardless of their actual capital contribution.

QWhat is the difference between a limited liability partnership contract and a limited partnership contract template?

A limited liability partnership (LLP) gives every partner limited liability and is usually a separate legal entity that can hold property and sign contracts in its own name. A limited partnership (LP), by contrast, requires at least one “general partner” with unlimited personal liability who manages the business, and one or more “limited partners” who contribute capital but cannot take part in day-to-day management without losing that protection. The contract templates differ accordingly: an LLP contract template treats all partners similarly subject to agreed rights and responsibilities, while a limited partnership contract template must clearly separate the general partner’s management powers and unlimited liability from the limited partner’s passive, capped-liability investor status, and define precisely what activity would cause a limited partner to lose that protection.

QIs a limited liability partnership contract template legally required?

In most jurisdictions, including the UK under the Limited Liability Partnerships Act 2000 and India under the LLP Act 2008, there is no strict legal requirement to have a written LLP agreement before incorporating the entity itself. However, incorporation (filing with the relevant registrar) is mandatory, and in the absence of a written agreement, generic default statutory provisions automatically govern the partners’ relationship. In the UK, these are the Limited Liability Partnerships Regulations 2001 defaults, for example, equal profit shares regardless of actual contribution, and no power to expel a member without an express clause. This is precisely why a tailored limited liability partnership contract template is considered essential good practice rather than a mere legal formality, even where it isn’t strictly mandatory. Note that India differs procedurally: the LLP Agreement is typically required to be filed with the Registrar of LLPs within a set period after incorporation, unlike the UK where the agreement remains a private document between partners.

QWhat clauses must a limited liability partnership contract template include?

A complete limited liability partnership contract template should include: the name and registered office of the LLP; the nature and scope of the business; capital contributions of each partner and rules for additional contributions; profit and loss sharing ratios; rights, duties, and management roles of partners, including designated members under UK law; decision-making and voting procedures, including meeting frequency and quorum; admission of new partners; provisions for resignation, retirement, and expulsion, including how a departing partner’s interest is valued and paid out; restrictive covenants such as non-compete, non-solicitation, and confidentiality obligations; indemnity provisions covering negligence and misconduct; dissolution and the priority order for asset distribution; a staged dispute resolution mechanism (negotiation, then mediation, then arbitration); and the governing law and exclusive jurisdiction clause. Cross-border partnerships should also address currency, tax residency, and cross-border enforceability explicitly.

QCan I use a free limited liability partnership contract template, or do I need a lawyer?

A free limited liability partnership contract template is a reasonable starting point for understanding the standard structure and clauses, and can save significant time compared to drafting from a blank page. However, it should be treated as a checklist and a conversation-starter rather than a final, sign-ready document. Generic templates often default to equal profit-sharing regardless of actual contribution, use vague exit-valuation language (“a fair value will be determined”), and may reference the wrong jurisdiction’s statutory framework entirely. For anything beyond the simplest two-person arrangement with negligible assets, particularly where unequal capital contributions, professional regulatory requirements, significant assets, or cross-border elements are involved, having a qualified lawyer in the relevant jurisdiction review or tailor the template before signing is strongly advisable. The cost of legal review is almost always smaller than the cost of resolving a dispute caused by a gap the template left unaddressed.

QWhat does a partnership contract template UK businesses use need to address that international templates might miss?

A partnership contract template UK businesses use should reflect several jurisdiction-specific points that generic international templates often miss: (1) UK LLP law uses “members” as the formal legal term, even though “partners” is common in everyday usage, precise drafting should clarify this. (2) A UK LLP must have at least two “designated members” responsible for statutory filings; without explicit designation, all members are deemed designated by default. (3) The LLP does not legally exist until Companies House issues a certificate of incorporation, earlier informal trading risks exposing the founders to unlimited liability as an unintended general partnership. (4) UK LLPs fall within the People with Significant Control (PSC) regime, a public disclosure obligation distinct from the agreement itself. (5) Recent reforms under the Economic Crime and Corporate Transparency Act 2023 introduce identity verification requirements that older templates won’t reflect. (6) If client data is handled, the agreement should reference UK GDPR and Data Protection Act 2018 compliance. A template built for a different jurisdiction’s statutes, even one with similar clause headings, will not correctly address these UK-specific obligations.

Verify a prospective business partner, domestic or cross-border, through GTsetu’s compliance-verified network before you draft a single clause. Anonymous discovery, built-in NDA workflow, and zero broker commissions.

They represents the product, and research team behind GTsetu, a global B2B collaboration platform built to help companies explore cross-border partnerships with clarity and trust. The team focuses on simplifying early-stage international business discovery by combining structured company profiles, verification-led access, and controlled collaboration workflows.

With a strong emphasis on trust, and disciplined engagement, Team GTsetu shares insights on global trade, partnerships, and cross-border collaboration, helping businesses make informed decisions before entering deeper commercial discussions.