How to Expand Your Manufacturing & Industrial Automation Business to Czech Republic

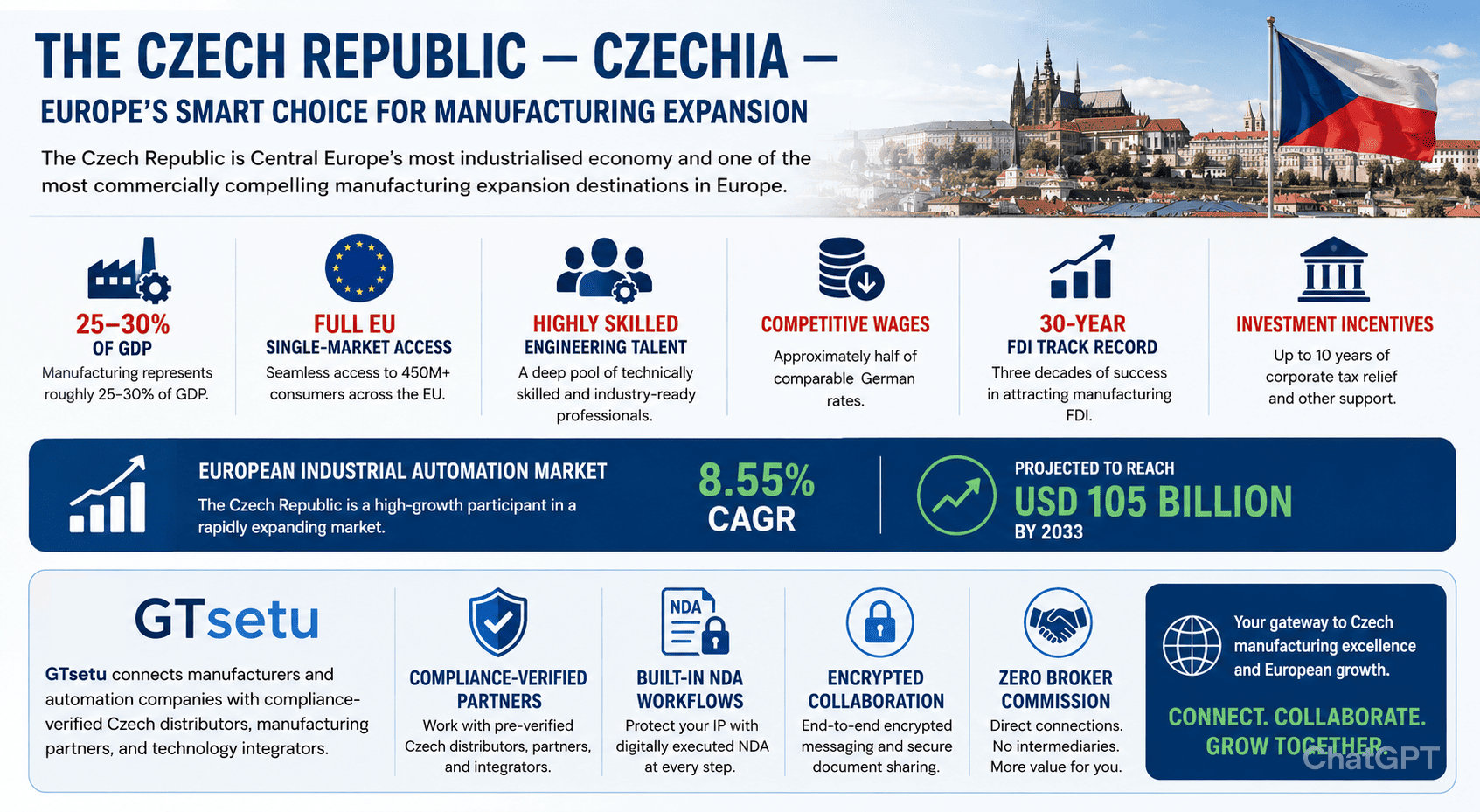

Direct Answer: The Czech Republic, Czechia, is Central Europe’s most industrialised economy and one of the most commercially compelling manufacturing expansion destinations in Europe. Manufacturing represents roughly 25–30% of GDP. The country offers full EU single-market access, highly skilled engineering talent, competitive wages (approximately half of comparable German rates), a 30-year track record of attracting manufacturing FDI, and government investment incentives including up to 10 years of corporate tax relief. The European industrial automation market, of which the Czech Republic is a high-growth participant, is growing at an 8.55% CAGR, projected to reach USD 105 billion by 2033. GTsetu connects manufacturers and automation companies with compliance-verified Czech distributors, manufacturing partners, and technology integrators, with built-in NDA workflows, encrypted collaboration, and zero broker commission.

📅 June 2026⏱ 17 min read✍️ GT Setu Editorial Team🔄 Updated regularly

25–30%

Manufacturing / GDP

8.55%

EU Automation CAGR

~50%

Wages vs Germany

EU27

Single Market Access

🌍 Also Explore: Expand to Other Global Manufacturing Markets

The Czech Republic sits at the geographical and commercial heart of Europe. Landlocked between Germany, Austria, Slovakia, and Poland, it is one of the most strategically positioned manufacturing locations in the world, within a day’s drive of 80% of EU industrial consumers, with full EU single-market access, and a 30-year track record of successfully integrating into Europe’s most demanding supply chains. Škoda Auto, Toyota, Hyundai, Bosch, Siemens, Honeywell, and hundreds of Tier-1 automotive and electronics suppliers have built their Central European operations here, drawn by a combination of engineering culture, cost competitiveness, and institutional stability that no other Central European economy fully replicates.

For manufacturers and industrial automation companies specifically, Czechia offers both a deployment market, where existing manufacturers are upgrading to Industry 4.0 and smart factory systems, and a production base, where establishing operations gives access to EU market advantages, lower production costs than Western Europe, and an internationally respected engineering workforce. This guide covers everything required to make an informed Czech expansion decision and the practical steps to executing it.

🇨🇿 Czech Republic at a Glance

Official name: Czechia / Czech Republic. Population: approx. 10.9 million. Capital: Prague. EU member since 2004. Currency: Czech Koruna (CZK), not yet in the Eurozone. GDP: approx. USD 340 billion (2024). Manufacturing share of GDP: 25–30%. Unemployment: 2.7% (February 2025, second lowest in the EU). Major industries: automotive, machinery and equipment, electronics, chemicals, pharmaceuticals. Primary trading partners: Germany, Slovakia, Poland, France, Austria, Netherlands.

SECTION 1

1 Why Czech Republic for Manufacturing & Automation?

The Czech Republic has maintained its position as one of Europe’s most competitive manufacturing FDI destinations for more than three decades. Its attraction is not a single factor but a convergence: central European location, EU membership, an engineering culture dating to the Austro-Hungarian industrial era, cost advantages over Western Europe, and a government that treats industrial FDI as a national strategic priority.

#1

FDI per capita in Central and Eastern Europe (KPMG, 2024)

2.7%

Unemployment rate, 2nd lowest in the EU (Feb 2025)

27.5%

Max investment incentive as % of total investment for strategic projects

The Six Strategic Drivers

Driver

What It Means for Manufacturers & Automation Companies

Commercial Implication

EU Single Market Access

Full access to the EU27 market with no tariff barriers, harmonised regulatory standards, and freedom of goods movement across 450+ million consumers

Products manufactured in Czechia benefit from EU CE marking recognition and EVFTA / EU trade agreement advantages when exported globally

Geographic Centrality

Within 500km of Vienna, Munich, Berlin, Warsaw, and Bratislava, access to the densest concentration of manufacturing industry in Europe

Logistics costs for intra-European supply chain integration are among the lowest in CEE; just-in-time delivery to major German automotive OEMs is commercially viable

Engineering Workforce Quality

Czech Republic has one of Europe’s highest ratios of engineering graduates per capita, with a 200-year industrial tradition dating to the Austro-Hungarian era

Skilled workforce for advanced manufacturing, automation integration, and R&D at wages approximately half of comparable German roles, the most commercially compelling cost-quality ratio in Europe

Nearshoring Wave

Geopolitical disruption and supply chain risk from Asia are driving European manufacturers to bring production back to Europe; countries like Czechia are primary beneficiaries

New factories established through nearshoring adopt automation from the outset, accelerating demand for robotics, PLCs, IIoT, MES, and smart factory systems

EV & Semiconductor Investment Surge

Czech Republic is a primary beneficiary of the EU Chips Act and the EV transition, ONSEMI’s SiC semiconductor expansion (government incentives of up to 27.5%) and multiple EV battery investments since 2025

New high-tech manufacturing facilities in semiconductors, EV batteries, and clean energy represent the highest-automation-intensity manufacturing investments entering Europe

Government Industry 4.0 Policy

Czechia’s National Industry 4.0 Initiative and Investment Incentives Act (2019, amended) provide structured incentives for smart manufacturing, R&D investment, and workforce digitalisation

Government funding through EU Structural Funds and national programmes directly subsidises automation adoption by domestic manufacturers, expanding the addressable market for automation solution providers

💡 The Nearshoring Automation Multiplier

According to market data, countries like Poland and Czechia are witnessing surges in FDI specifically targeted at reshoring production from Asia. To make this economically viable against lower-cost Asian competitors, reshored plants must leverage high degrees of automation. Automated lines allow reshored plants to operate with minimal staff while achieving output qualities that justify premium pricing. This creates a structural, policy-backed demand multiplier for industrial automation in the Czech market that extends well beyond the current investment cycle. See also: technology partnerships as a market entry vehicle for automation solution providers.

SECTION 2

2 Market Overview: Size, Growth & Industrial Position

The Czech Republic participates in the European industrial automation market, one of the world’s largest and most sophisticated, as both a consumer of automation technology (installing solutions in its own manufacturing base) and increasingly as a production location for automation components and systems destined for the broader EU market.

Market Metric

Value

Period / Source

Europe Industrial Automation Market

USD 50.17 billion

2024 (Market Data Forecast)

Europe Industrial Automation CAGR

8.55%

2025–2033

Europe Industrial Automation by 2033

USD 105 billion

2033 projection

Europe Factory Automation Market

USD 64.10 billion

2025 (Market Data Forecast)

Europe Factory Automation CAGR

8.13%

2026–2034

Europe Smart Manufacturing Market

USD 63.09 billion

2025, growing at 12.52% CAGR to USD 161B by 2033

Industrial Software CAGR (Europe)

13.8%

2025–2033, fastest-growing automation sub-segment

PLC Market Share

27.98% of factory automation revenue

2025 (Mordor Intelligence)

Czech ICT Market

USD 22.5 billion (2025) → USD 32.4 billion (2030)

7.6% CAGR (Mordor Intelligence)

Czech Republic’s Specific Position in European Automation

🏆

Highest FDI per Capita in CEE

The Czech Republic receives more FDI per capita than any other Central and Eastern European economy, a 30-year track record that reflects both the country’s business environment quality and the depth of its integration into European supply chains. This FDI concentration directly translates into automation demand: high-tech factories investing in Czechia deploy advanced automation from day one.

#1 CEE FDI

⚡

EV & Semiconductor Investment Surge (2025+)

Since 2025, the Czech Republic has witnessed a surge of foreign manufacturing investments in high-tech sectors, EV batteries, SiC semiconductors (ONSEMI expansion with 27.5% government incentive), and advanced electronics. Taiwan’s CTi Cable is building a new plant; multiple EV battery gigafactories are in planning or construction. These are the highest-automation-intensity manufacturing categories, creating structured near-term demand.

EV & Semicon

🤖

Industry 4.0 Transformation Mandates

The Czech government’s National Industry 4.0 Initiative, backed by EU Structural Fund allocation, is systematically driving the digitalisation of Czech manufacturing. SME digitalisation grants, smart factory demonstration projects, and university-industry partnerships are creating structured demand for IIoT, digital twin, MES, and predictive maintenance solutions beyond the large FDI project pipeline.

Industry 4.0

🔧

Deep Automotive Supplier Ecosystem

The Czech Republic’s automotive industry, anchored by Škoda Auto (Volkswagen Group), Toyota Peugeot Citroën Automobile Czech (TPCA), and Hyundai’s Nošovice plant, creates an exceptionally deep Tier 1, 2, and 3 supplier ecosystem. Automotive applications account for approximately 24% of European factory automation demand. In Czechia, the automotive share is higher, creating disproportionate demand for welding robotics, body-in-white automation, and EV battery assembly systems.

Automotive Hub

SECTION 3

3 Top Sectors: Where Automation Demand Is Highest

Automation demand in the Czech Republic is concentrated in eight sectors that together represent the core of the country’s industrial base. Each presents distinct opportunities for automation companies and manufacturers entering the market.

🚗

Automotive & EV Manufacturing

Largest automation demand sector, 24%+ of European factory automation

The Czech Republic is one of Europe’s most concentrated automotive manufacturing nations per capita. Škoda Auto (VW Group) in Mladá Boleslav and Kvasiny, Toyota-Peugeot in Kolín, and Hyundai in Nošovice are surrounded by over 200 automotive Tier 1 and Tier 2 suppliers. The EV transition is driving massive investment in new battery assembly lines, SiC power module production, and EV drivetrain component manufacturing, all requiring new automation infrastructure.

Electronics and semiconductor manufacturing is the fastest-growing FDI category in Czechia in 2025–2026. ONSEMI’s SiC semiconductor expansion, Taiwan’s CTi Cable, and multiple PCB assembly and electronic components manufacturers are establishing or expanding operations. New semiconductor fabs and electronics assembly lines are among the highest-automation-intensity investments in any manufacturing category.

SMT AutomationCleanroom SystemsAOI & X-raySiC Production

⚙️

General Engineering & Machinery

Traditional strength; significant upgrade cycle underway

Czech engineering and machinery manufacturing, turbines, pumps, compressors, machine tools, has a 200-year tradition. Companies like Doosan Škoda Power, ČKD, Motorpal, and hundreds of mid-market engineering firms are undergoing significant Industry 4.0 upgrades, replacing legacy PLCs, adding SCADA and MES layers, and deploying IIoT condition monitoring to compete with German and Austrian manufacturers on quality rather than cost alone.

Government-incentivised; growing defence manufacturing base

The Czech Republic has a growing aerospace manufacturing sector, Honeywell Aerospace Technologies in Brno (avionics), MESIT in Uherské Hradiště, and a network of precision component manufacturers supply global OEMs. Czech aerospace exports grew significantly in 2024–2025 driven by defence investment. Precision CNC machining automation, quality control systems, and AS9100 compliant MES are key demand areas.

Government-incentivised technology sector; EU GMP compliance driver

Pharmaceuticals are an explicitly incentivised sector under Czechia’s Investment Incentives Act. Czech pharma companies, Zentiva, TEVA Czech, and numerous generic manufacturers, are investing in EU GMP-compliant automation to access European and US export markets. Filling line automation, serialisation/traceability systems, and environmental monitoring are priority investment areas for Czech pharmaceutical producers.

Large domestic industry; export-driven quality upgrade cycle

The Czech Republic has a well-established food and beverage manufacturing sector, brewing (Czech beer is a cultural and export staple), dairy, confectionery, and meat processing. Increasing export focus on EU markets and retail consolidation is driving quality standardisation and automation investment: automated filling and packaging, HACCP monitoring systems, and CIP (Clean-in-Place) automation are priority areas.

Major government strategic programme, CZK 100B+ investment 2025–2033

The Czech government approved a strategic investment programme in late 2024 committing CZK 100 billion (EUR 4+ billion) to clean technology manufacturing 2025–2033, covering batteries, solar panels, wind turbines, heat pumps, and electrolysers. This programme explicitly supports automation investment in clean energy manufacturing and creates significant demand for process control, assembly automation, and quality systems in new and expanding clean tech factories.

Battery ManufacturingSolar Panel AutomationHeat Pump AssemblyProcess Control

🔬

Nanotechnology & Advanced Materials

University-industry ecosystem; Czech global strength in nano

The Czech Republic has a globally recognised strength in nanotechnology, with TU Liberec developing Nanospider technology (world’s first industrial nanofibre production machine) and a cluster of university spinouts in advanced materials, nano-electronics, and photonics. The Investment Incentives Act specifically identifies nanotechnology and advanced materials as incentivised sectors, creating opportunity for automation companies serving precision manufacturing environments.

Czech manufacturing is regionally concentrated, with distinct clusters for different industry categories. Understanding the regional structure is essential for location selection, customer proximity, and talent access.

🏙️

Prague & Central Bohemia, Technology, R&D, Electronics

Best for: Technology companies, R&D operations, electronics, ICT, and professional services. Prague is the Czech Republic’s commercial and technology capital, home to multinational regional headquarters, technology research centres, and a thriving startup ecosystem. Central Bohemia’s industrial zones host precision manufacturing and electronics assembly. Proximity to the German border (via D5/E50) makes it an efficient Western European logistics hub. Key industrial zones include Příbram Industrial Zone, Kladno Science and Technology Park, and multiple Prague logistics parks.

Technology Hub

🎓

South Moravia / Brno, Automotive, Electronics, IT

Best for: Automotive components, electronics, IT, aerospace, and high-tech manufacturing. Brno is the Czech Republic’s second city and its “Silicon Valley”, home to Honeywell Aerospace Technologies, IBM, Red Hat, and a cluster of automotive Tier 1 suppliers. Brno University of Technology (VUT) provides a continuous pipeline of engineering talent. The South Moravian Innovation Centre supports university-industry technology transfer. Key zones include Brno-Černovice Industrial Zone, Brno Science and Technology Park, and Pohořelice Industrial Zone.

Czech Silicon Valley

🚗

Mladá Boleslav / Central Bohemia, Automotive (Škoda Hub)

Best for: Automotive suppliers, Tier 1, 2, 3 component manufacturers. Mladá Boleslav is Škoda Auto’s headquarters and principal production site, the anchor of one of Central Europe’s most concentrated automotive supplier clusters. The city and surrounding region host over 200 automotive component manufacturers serving Škoda directly. Automation companies providing welding, stamping, assembly, and paint shop automation have a concentrated, accessible customer base in this cluster. Kvasiny (Škoda’s SUV plant) and Vrchlabí (transmission production) extend the geographic footprint.

Škoda Automotive

🏭

Moravian-Silesian Region / Ostrava, Heavy Industry, Hyundai

Best for: Heavy engineering, automotive (Hyundai), metallurgy, energy equipment. Ostrava and the Moravian-Silesian region have the most significant incentive support of any Czech region (highest unemployment zones = lowest investment thresholds for incentives). Hyundai’s manufacturing plant in Nošovice and a large metallurgical and engineering sector provide a concentrated B2B market for heavy industrial automation, DCS, process control, metallurgical automation, and automotive body-shop robotics.

Heavy Industry

🔧

Pilsen / Plzeň, Engineering, Defence, Doosan Škoda Power

Best for: Heavy engineering, power generation equipment, defence, aerospace components. Plzeň is home to Doosan Škoda Power (steam turbines, generators), ŠKODA Transportation (rail vehicles), and a cluster of precision engineering manufacturers serving the global energy and defence sectors. The Pilsen region has a strong apprenticeship and vocational training system producing high-quality engineering technicians. Location on the D5 motorway provides direct logistics access to Munich (150km) and Western European markets.

Power & Defence

🧵

Liberec & Ústí nad Labem, Textiles, Glass, Automotive

Best for: Textiles (nanofibre technology), glass manufacturing, automotive components, chemicals. North Bohemia hosts globally distinctive industries: TU Liberec’s Nanospider technology makes the region a world leader in nanofibre production; Liberec is a centre for technical textiles; Ústí nad Labem and surroundings have glass, chemicals, and automotive component manufacturing. Higher incentive levels (above-average unemployment in some sub-regions) reduce the investment threshold for qualifying projects.

Nano & Glass

🇨🇿 CzechInvest, Your Gateway to Czech Industrial Zones

CzechInvest (Czech Business and Investment Development Agency) is the official government agency supporting foreign investors entering the Czech Republic. They provide free advisory services including site selection across Czech industrial zones, investment incentive navigation, regulatory guidance, and connection to the Czech supplier network. Engaging CzechInvest from the beginning of your market entry process significantly accelerates the regulatory and location selection steps. Contact: czechinvest.gov.cz

SECTION 5

5 Investment Incentives & Government Support

The Czech Republic’s investment incentive framework, established by the 2019 Investment Incentives Act (Amendment to Act No. 72/2000 Coll.), is among the most structured and generous in Central Europe for high-tech manufacturing. Incentives are funded from national budget and EU Structural Funds, and administered through CzechInvest.

Incentive Type

Details

Eligibility Condition

Corporate Income Tax Relief

Full or partial CIT exemption for up to 10 years on qualifying manufacturing investments

Minimum investment CZK 200 million (≈EUR 8M) for manufacturing; reduced to CZK 150M or CZK 100M in high-unemployment regions

Job Creation Cash Grant

Up to CZK 300,000 (≈USD 13,800) per new job created in qualifying sectors

Jobs must be in high-value sectors; applicant must maintain employment for minimum period

Training & Skills Cash Grant

Up to 70% of eligible training costs subsidised for workforce upskilling

Training in advanced manufacturing technologies, Industry 4.0, automation and digital skills

Fixed Asset Purchase Grant

Up to 20% of eligible fixed asset costs (machinery, equipment, automation systems)

Assets must include high-tech machinery from the approved government list; 50% rule for high-tech content

Strategic Project Incentive

Up to 27.5% of total investment for designated strategic projects (e.g., ONSEMI SiC)

Minimum investment EUR 110 million; notification and EU state aid approval required

Clean Technology Programme (2025–2033)

CZK 100 billion total programme for batteries, solar, wind, heat pumps, electrolysers manufacturing

Minimum project CZK 2.8 billion; applications via Ministry of Industry and Trade SIRS framework

R&D Tax Credits

100% deduction of R&D costs from tax base; additional 110% deduction for incremental R&D spend

Qualifying R&D activities in automation, AI, advanced materials, nanotechnology, ICT

EU Structural Funds

Operational Programme Technology and Applications for Competitiveness (OTAC), grants for SME digitalisation, automation, and energy efficiency

SME and mid-cap manufacturers in qualifying regions; various programme-specific thresholds

✅ Qualifying Sectors for Maximum Incentives

The 2019 Investment Incentives Act specifically eliminates incentives for low-skilled labour investments and reserves maximum incentive levels for: aerospace, ICT, life sciences, nanotechnology, and advanced automotive manufacturing. Industrial automation investments supporting these sectors qualify at the highest incentive tier. Investments in standard manufacturing sectors also qualify provided at least 50% of the production line value comprises high-tech machinery from the government-approved list, making automation equipment itself a qualifying investment cost.

SECTION 6

6 Market Entry Modes

The Czech Republic’s EU membership and open investment climate provide foreign manufacturers and automation companies with a full range of entry structures. The right choice depends on investment scale, product category, regulatory requirements, and the strategic role of the Czech operation within a broader European or global structure.

🏭

Wholly-Owned Subsidiary (s.r.o. or a.s.)

The most common structure for manufacturing FDI in Czechia. s.r.o. (společnost s ručením omezeným, limited liability company) requires minimum share capital of CZK 1 (approx. EUR 0.04) since 2014 reforms. Provides full operational control, access to investment incentives, and ability to employ local staff. Can operate in industrial zones and hi-tech parks with associated benefits.

Full Control / Full Investment

🤝

Joint Venture with Czech Partner

Partnership with a Czech company, sharing ownership and operations. Useful for sectors where local market relationships are critical (government procurement, state-owned enterprise supply chains), where local brand recognition provides commercial value, or where a Czech partner’s existing customer base provides rapid market access. Requires careful joint venture structuring including IP allocation and exit provisions.

Local Knowledge / Shared Risk

🏢

Branch Office or Representative Office

A branch office can conduct limited commercial activities as an extension of the foreign parent. A representative office is restricted to market research, liaison, and promotion, no commercial operations. Both are lower-cost initial options for market testing and relationship building before committing to full subsidiary establishment. Not eligible for Czech investment incentives.

Low Cost / Market Testing

📋

Contract Manufacturing

Engage a Czech contract manufacturer to produce your products to specification without establishing a legal entity. Particularly relevant for manufacturers wanting Czech production for EU market access (CE marking, EU content for FTA purposes) without direct factory investment. IP and quality control require robust contractual management. See: contract manufacturing.

No Entity / Czech Production

🚚

Distribution Partnership

For automation equipment and solution companies: appoint a verified Czech distributor or systems integrator to sell your products without direct establishment. Fastest route to revenue; lowest capital commitment; requires a well-structured distribution agreement with territory rights and technical support obligations. GTsetu provides pre-verified Czech distributors for this route.

Fastest Revenue / Zero Capex

🔬

Technology Licensing or Transfer

License your manufacturing process or automation technology to a Czech partner under a formal technology transfer agreement. Revenue through royalties; suitable where your competitive advantage is the technology rather than the manufacturing capability. Czech R&D tax credits make this structure additionally attractive for technology-intensive arrangements. See: licensing vs distribution.

IP-Based Revenue

SECTION 7

7 Regulatory Framework: Setting Up in Czechia

Czechia’s regulatory framework for business establishment is governed by EU directives and Czech commercial law, and has been significantly streamlined in recent years. The Czech Republic consistently ranks among the easier Central European markets for business formation.

Regulatory Requirement

Description

Timeline

Key Consideration

Company Formation (s.r.o.)

Register a limited liability company (s.r.o.) with the Commercial Register (Obchodní rejstřík) at the Regional Court. Minimum share capital CZK 1. Notarised memorandum of association required

5–15 working days (expedited registration available)

Foreign-owned companies must designate a local director or executive, can be a Czech resident or a non-resident EU citizen without restriction

Trade Licence (Živnostenský list)

For manufacturing and trading activities, a trade licence (živnostenský list) must be obtained from the Trade Licensing Office before commercial operations commence

5 working days

Regulated trades (pharmaceuticals, construction, certain foods) require professional qualifications evidence; standard manufacturing is a “free trade” category

Tax Registration

Register with the Czech Financial Administration for Corporate Income Tax (standard 21%; or 19% from 2024 for small companies), VAT (standard rate 21%), and withholding tax

Concurrent with company registration

VAT registration mandatory if annual turnover exceeds CZK 2 million (approx. EUR 80,000). Czech tax year is the calendar year

Social Insurance & Health Insurance Registration

Employers must register with the Czech Social Security Administration (ČSSZ) and health insurance companies. Social contributions: employer 33.8% of gross wage; employee 11%

Before first employee

Czech Republic has one of the EU’s most comprehensive social insurance systems; employer contribution costs are significant and must be factored into employment cost planning

Investment Incentive Application

Investment incentive applications submitted to CzechInvest before project implementation begins. Pre-application consultation with CzechInvest advisors is strongly recommended

3–6 months for full approval

Incentive applications must be submitted before investment commences, retrospective applications are not accepted. Engage CzechInvest in the planning phase, not after site selection

Building & Environmental Permits

Construction of new manufacturing facilities requires building permits from municipal authorities and, for regulated activities, environmental impact assessment (EIA)

3–12 months depending on project scale and location

Industrial zone sites with pre-approved zoning and infrastructure significantly reduce permitting timelines; greenfield sites on unzoned land add considerable time

CE Marking & Product Compliance

Products manufactured in or sold into the EU Czech market must comply with applicable EU directives (Machinery, Low Voltage, EMC, ATEX for relevant categories) and bear CE marking

Prior to sale

CE marking from a notified body in any EU member state is valid across all EU27, manufacturing in Czechia for EU export does not require separate national certification

SECTION 8

8 Challenges & How to Mitigate Them

The Czech Republic is a mature, well-governed market, but it presents specific operational challenges for foreign manufacturers and automation companies that should be anticipated in the market entry plan.

Challenge

Specifics

Mitigation Strategy

Near-Full Employment

Czech unemployment at 2.7% (2nd lowest in EU) means recruitment for manufacturing roles is highly competitive. Labour shortages are acute in engineering, tooling, and skilled trade roles

Locate in regions with higher unemployment (Moravian-Silesian, Northwest Bohemia) where incentive levels are also higher; engage Czech technical schools and universities directly; offer above-average wages and apprenticeship programmes; use Training Grant incentives (up to 70% of costs) to upskill available labour

Rising Wage Costs

Czech wages have grown 7.2% nominally in 2024 and real wage growth of 4.6%, narrowing the cost gap with Western Europe over time

Build automation intensity into your Czech operation from day one, the combination of EU market access and automation-enabled competitiveness sustains margin even as wages rise. See: pricing structures

CZK Currency Risk

Czechia is not in the Eurozone, invoicing, costs, and financial reporting are in Czech Koruna (CZK), creating currency exposure for companies pricing in EUR or USD

Hedge CZK exposure through forward contracts; structure Euro-denominated customer contracts where possible (Czech B2B customers in export sectors often accept EUR invoicing); model CZK/EUR sensitivity in financial planning

IP Protection

Czech Republic is an EU member with strong IP law (aligned with EU IPR Enforcement Directive), but enforcement for complex technology IP disputes requires engagement of specialist IP legal counsel

Register trademarks and patents with the Czech Industrial Property Office (IPO) and at EU level (EUIPO) for pan-European protection; execute robust NDAs before any technology sharing; use GTsetu’s encrypted document exchange for all sensitive pre-commercial exchanges

Bureaucratic Investment Approval Timelines

Investment incentive approvals, building permits, and environmental assessments can create 3–12 month timelines before operations commence, particularly for complex manufacturing projects

Engage CzechInvest in the planning phase; select pre-zoned industrial zone sites to reduce permitting timelines; begin incentive applications before site selection is finalised; use established industrial park operators who have pre-approved infrastructure

Unverified Partner Risk

Cold outreach to Czech distributors or manufacturing partners carries identity and credential risks, particularly for technical partner claims and financial standing assertions

Use GTsetu’s compliance-verified Czech partner network; execute NDA before sharing any product specifications, pricing, or commercial strategy; verify business registration and trade credentials against official Czech registries before commercial engagement

SECTION 9

9 Step-by-Step Expansion Process

Whether entering through a distribution partnership, establishing a subsidiary, or pursuing contract manufacturing, the Czech expansion process follows a structured sequence. The steps below are oriented toward the most commercially efficient initial entry for most manufacturers and automation companies.

01

Market Assessment & Sector Targeting

Identify the specific Czech manufacturing segments that represent the strongest near-term demand for your products or services. The automotive and EV cluster, electronics and semiconductor manufacturing, the clean technology programme investments, and the Industry 4.0 upgrade cycle in general engineering are the four highest-value pipelines. Determine: who are your target customers, where are they located, who are the incumbents (Siemens, ABB, Rockwell, Schneider Electric all have Czech operations), and what is a realistic 3-year addressable revenue? Related: global expansion analysis and company global expansion guide.

02

Entry Mode Selection

For most automation equipment and solution companies, the optimal starting point is a distribution partnership with a verified Czech technical distributor or systems integrator, generating revenue without entity establishment, while building the market knowledge to evaluate a direct investment. For manufacturers establishing production, a wholly-owned s.r.o. in an industrial zone with CzechInvest-supported incentives is the standard structure. Evaluate whether the scale of the Czech opportunity justifies entity costs (approximately EUR 15,000–25,000 all-in for s.r.o. formation) vs. the distribution partnership route. See: market entry partnerships.

03

Verified Partner Discovery & Engagement

Find and verify your Czech partners, distributors, technical resellers, systems integrators, or manufacturing partners, before any commercial engagement. Use GTsetu’s compliance-verified platform to browse pre-vetted Czech companies by sector and capability. Anonymous discovery protects your market entry strategy during evaluation. Execute a mutual NDA before sharing any pricing, product specifications, or commercial terms. Verify business registration (Obchodní rejstřík), trade licences, and technical capability before progressing. See: business verification and partnership evaluation criteria.

04

CzechInvest Engagement (for Direct Investment)

If pursuing direct investment (subsidiary, manufacturing facility), contact CzechInvest at the project concept stage, before any site selection or investment commitment. CzechInvest provides free advisory services including industrial zone shortlisting, investment incentive eligibility assessment, regulatory pathway navigation, and connection to Czech suppliers and universities. Critically, investment incentive applications must be submitted before investment begins, engaging CzechInvest in the planning phase, not after the fact, is the single most important process recommendation for direct investment routes.

05

Legal Entity Formation

Instruct a Czech-registered law firm to prepare the s.r.o. memorandum of association, notarisation, and Commercial Register filing. Simultaneously obtain the trade licence from the Trade Licensing Office. Register for corporate income tax, VAT, and social insurance. If investing in an industrial zone, obtain industrial zone allocation from the zone management authority or SIRS. Total timeline: 3–8 weeks for standard s.r.o. establishment; longer if investment incentive application is running in parallel. Engage legal counsel with specific Czech manufacturing FDI experience, generic EU corporate law firms may lack Czech-specific procedural knowledge.

06

Commercial Agreement Execution

Execute formal commercial agreements with Czech partners: distribution agreement or business partnership contract with clearly defined territory, pricing, volume commitments, IP provisions, and termination clauses. Ensure dispute resolution specifies Czech courts or ICC/VIAC arbitration (Vienna is the most common neutral venue for Czech international commercial disputes). Document IP provisions explicitly, Czech law is EU-harmonised but specific IP ownership provisions in any joint development context must be contractually defined.

07

Go-to-Market & Relationship Building

Establish commercial presence: participate in Czech and Central European trade events (Brno International Engineering Fair, MSV, the largest industrial fair in Central Europe; Amper (electrical engineering and automation); FOR ARCH (construction technology)); register in Czech B2B supplier databases; develop Czech-language product documentation; build relationships with Czech technical universities (CTU Prague, VUT Brno, VŠB Ostrava) for talent pipeline and R&D collaboration. For the B2B lead generation strategy, see: top places to find B2B leads and industrial business collaboration.

08

Scale & Regional Expansion

As your Czech operation matures, evaluate expansion across the broader CEE region from your Czech base. The Czech Republic’s central location and EU membership make it a natural regional headquarters for Central European operations, with Slovakia, Poland, Hungary, and Austria all within a day’s logistics reach. Consider how your Czech investment interacts with operations in neighbouring markets: our country guides for Germany, Romania, and India cover the adjacent strategic expansion opportunities for European-headquartered manufacturers.

SECTION 10

10 How GTsetu Connects You with Verified Czech Partners

For manufacturers and industrial automation companies entering the Czech market, the fastest and most capital-efficient first step is a verified local partnership, a Czech technical distributor, systems integrator, or manufacturing partner who can represent your products credibly to Czech OEMs and industrial buyers. GTsetu pre-verifies every Czech company on the platform against official business registries, trade licences, and relevant certifications. Anonymous discovery, built-in NDA workflows, and encrypted document exchange protect your IP and commercial strategy throughout the evaluation process.

🏛️

Czech Business Registry Verification

Every Czech company verified against the Obchodní rejstřík (Commercial Register) and trade licensing records, confirming legal identity before any engagement.

🕵️

Anonymous Discovery

Browse verified Czech partner profiles by sector and capability without revealing your market entry strategy until you are ready to engage.

📄

Built-In NDA Workflow

Mutual NDA with digital signatures and audit trail, executed before any pricing, technical specifications, or IP is shared with a Czech partner candidate.

🔐

Encrypted Document Exchange

Product data sheets, pricing schedules, and technical documentation shared in AES-256 encrypted workspace, not via unprotected email.

🌍

EU & Global Coverage

Verified manufacturers and distributors across the Czech Republic and 100+ countries, supporting your global partner and cross-border partnership strategy.

🚫

Zero Commission

GTsetu takes no success fee on any partnership formed. Your deal economics with your Czech partner stay entirely between you, unlike broker-mediated introductions.

Q Why is the Czech Republic a top destination for manufacturing expansion?

The Czech Republic is Central Europe’s most industrialised economy, with manufacturing representing roughly 25–30% of GDP. It offers full EU single-market access for goods produced there, a highly skilled engineering workforce (one of Europe’s highest ratios of engineering graduates per capita), competitive wages approximately half of comparable German rates, the highest FDI per capita in Central and Eastern Europe, and a government Investment Incentives Act providing up to 10 years of corporate tax relief. The country’s central location, within 500km of Vienna, Munich, Berlin, and Warsaw, makes it the optimal production base for serving the densest concentration of European manufacturing industry. Since 2025, a surge of EV, semiconductor, and clean technology investment has made Czechia an even more compelling destination for high-tech manufacturing FDI.

Q What investment incentives does the Czech Republic offer for manufacturers?

The Czech Republic’s 2019 Investment Incentives Act provides: corporate income tax relief for up to 10 years; cash grants for job creation up to CZK 300,000 per new position; training grants up to 70% of eligible costs; fixed asset purchase grants up to 20% of costs; and investment incentives of up to 27.5% of total investment for designated strategic projects. Incentive thresholds are reduced in high-unemployment regions (CZK 150M or CZK 100M vs. standard CZK 200M), making those regions proportionally more attractive for smaller investments. A separate CZK 100 billion programme (2025–2033) supports clean technology manufacturing. R&D tax credits allow 100–110% deduction of qualifying R&D expenditure from the tax base.

Q What are the biggest manufacturing sectors in the Czech Republic?

The Czech Republic’s leading manufacturing sectors by output and employment are: automotive (Škoda Auto / VW Group, Toyota, Hyundai, with one of Europe’s highest automotive output-per-capita ratios); general engineering and machinery (turbines, pumps, compressors, machine tools); electronics and electrical equipment (growing semiconductor manufacturing base); pharmaceuticals (Zentiva, TEVA Czech); chemicals and plastics; food and beverage (beer, dairy, confectionery); and aerospace components (Honeywell Aerospace, MESIT). Newer high-growth categories include SiC semiconductor manufacturing, EV batteries, clean technology manufacturing (solar, wind, heat pumps), and nanotechnology-based advanced materials.

Q Is the Czech Republic in the Eurozone?

No. The Czech Republic is an EU member but retains its own currency, the Czech Koruna (CZK). Eurozone accession has been repeatedly deferred and has no fixed timeline as of 2026. For manufacturers and automation companies operating in Czechia, this creates CZK/EUR currency exposure that must be managed through forward hedging, Euro-denominated customer contracts (acceptable in Czech B2B contexts), or natural hedging (CZK revenues against CZK costs). The CZK is generally a stable currency closely correlated with the Euro, with the Czech National Bank maintaining a managed float policy. Currency risk is manageable but must be budgeted for in financial planning.

Q How does GTsetu help manufacturers expand into Czech Republic?

GTsetu connects manufacturers and industrial automation companies with compliance-verified Czech distributors, manufacturing partners, and technology integrators, without the identity fraud and credential misrepresentation risks of cold outreach or unverified directory listings. Every Czech company on GTsetu has been verified against official business registries and trade licences before engagement. Anonymous discovery protects your market entry strategy during the evaluation phase. Built-in NDA workflows ensure pricing, product specifications, and commercial strategy are protected before any information is shared. Encrypted document exchange and a complete audit trail support both IP protection and compliance documentation. And unlike broker-mediated introductions, GTsetu charges zero commission on any partnership formed.

Q What is the fastest way to enter the Czech market for an automation company?

For most industrial automation equipment and solution companies, the fastest route to Czech market revenue is a distribution partnership with a verified Czech technical distributor or systems integrator, a partner who has existing relationships with Czech industrial buyers (automotive OEMs, engineering manufacturers, electronics factories) and the technical capability to represent your products credibly. This approach generates revenue without entity establishment costs or timelines, and provides the market knowledge needed to evaluate whether direct investment is warranted. GTsetu provides pre-verified Czech distributors and technical partners for this route. If direct entity establishment is required, a straightforward s.r.o. registration in Czechia takes 5–15 working days, among the fastest in Central Europe.

Find Verified Czech Manufacturing & Distribution Partners on GTsetu

Join 500+ verified manufacturers, distributors, and automation companies building international trade partnerships on GTsetu, with compliance-verified Czech partner profiles, built-in NDA workflows, encrypted document exchange, and zero broker commission.

They represents the product, and research team behind GTsetu, a global B2B collaboration platform built to help companies explore cross-border partnerships with clarity and trust. The team focuses on simplifying early-stage international business discovery by combining structured company profiles, verification-led access, and controlled collaboration workflows.

With a strong emphasis on trust, and disciplined engagement, Team GTsetu shares insights on global trade, partnerships, and cross-border collaboration, helping businesses make informed decisions before entering deeper commercial discussions.