How to Expand Your Manufacturing & Industrial Automation Business to Vietnam

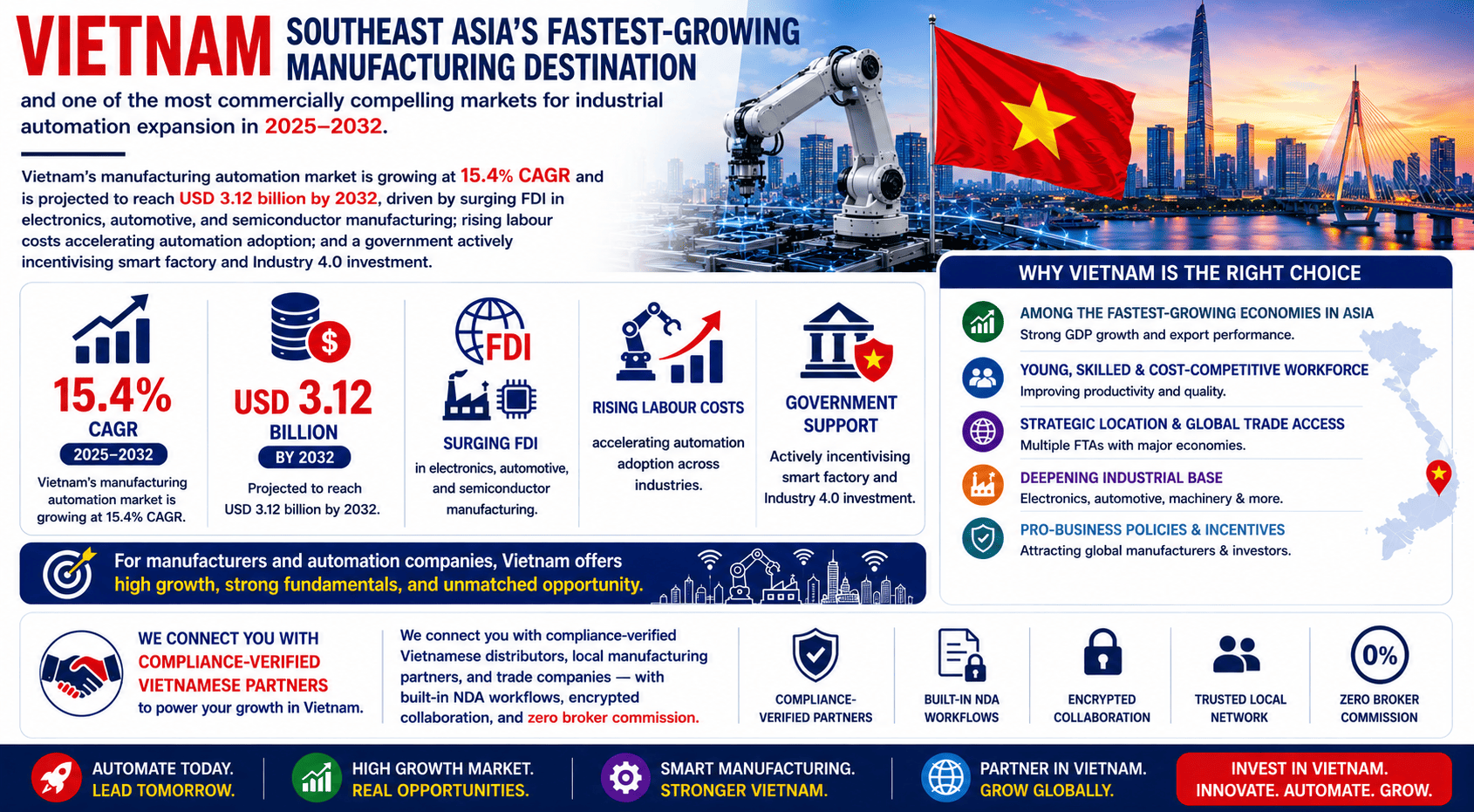

Direct Answer: Vietnam is Southeast Asia’s fastest-growing manufacturing destination and one of the most commercially compelling markets for industrial automation expansion in 2025–2032. The country’s manufacturing automation market is growing at a 15.4% CAGR and is projected to reach USD 3.12 billion by 2032, driven by surging FDI in electronics, automotive, and semiconductor manufacturing; rising labour costs accelerating automation adoption; and a government actively incentivising smart factory and Industry 4.0 investment. For manufacturers and automation companies, GTsetu connects you with compliance-verified Vietnamese distributors, local manufacturing partners, and trade companies, with built-in NDA workflows, encrypted collaboration, and zero broker commission.

📅 June 2026⏱ 18 min read✍️ GT Setu Editorial Team🔄 Updated regularly

Vietnam’s rise as a global manufacturing powerhouse is one of the defining industrial stories of this decade. Samsung, Intel, LG, Foxconn, and hundreds of Tier-1 global manufacturers have established or significantly expanded operations in the country, drawn by a combination of competitive costs, favourable trade agreements, and a government that treats manufacturing FDI as a strategic priority. For industrial automation companies and manufacturers seeking to supply, partner in, or establish operations in Vietnam, the window of commercial opportunity is wide open, and the evidence for acting now, rather than in three years, is compelling.

This guide covers everything required to make an informed Vietnam expansion decision: the market size and growth trajectory, the industry sectors driving automation demand, the key industrial zones, the regulatory landscape, the market entry modes available, and the practical steps to establishing your presence. It also explains how GTsetu helps manufacturers and automation companies find and engage compliance-verified Vietnamese partners, distributors, local manufacturers, and technology integrators, without the fraud and verification risk of unverified outreach.

🇻🇳 Vietnam at a Glance

Population: ~100 million. GDP growth: 6–7% annually. Manufacturing share of GDP: ~25%. Key manufacturing categories: electronics and semiconductors (65%+ of FDI inflows), textiles and footwear, automotive components, food processing, chemicals. Major trade partners: USA, China, EU, South Korea, Japan. Vietnam is a signatory to 17 free trade agreements including CPTPP, EVFTA, RCEP, VKFTA, and VJEPA.

SECTION 1

1 Why Vietnam for Manufacturing & Industrial Automation?

Vietnam has emerged as the leading China+1 manufacturing destination globally, not because it is simply cheaper than China, but because it has systematically built the infrastructure, regulatory environment, and trade relationships required to support sophisticated, high-value manufacturing operations. For industrial automation companies specifically, Vietnam represents both a deployment market (manufacturers adopting automation to stay competitive) and a production base (establishing manufacturing or assembly operations in the country).

$36B+

FDI attracted in 2023, nearly 30% increase year-on-year

10.3%

Industrial production growth in Q2 2025

18%

Export value growth in Q2 2025 to ~USD 117 billion

The Five Strategic Drivers

Driver

What It Means for Manufacturers & Automation Companies

Commercial Implication

China+1 Diversification

Global manufacturers are relocating or duplicating production lines from China to Vietnam to reduce geopolitical supply chain risk

New factories entering Vietnam adopt automation from the outset, immediate demand for PLCs, robotics, SCADA systems, and IIoT platforms

17 Free Trade Agreements

Vietnam’s FTA network gives manufacturers in Vietnam preferential tariff access to the EU (EVFTA), UK, ASEAN, Japan, South Korea, and CPTPP signatories

Manufacturing in or through Vietnam provides tariff advantages for accessing major global markets, a pull factor for multinational production investment

Rising Labour Costs

Vietnamese manufacturing wages have grown 7–10% annually, making automation increasingly cost-justified for labour-intensive operations

Existing manufacturers upgrading production efficiency are actively evaluating IIoT, robotics, and predictive maintenance solutions

Industry 4.0 Government Policy

Vietnam’s Resolution 52/NQ-TW and National Strategy on Industry 4.0 provide direct incentives for smart manufacturing adoption including tax holidays and preferential land rates in hi-tech parks

Government-backed demand accelerates automation adoption across both FDI and domestic manufacturers

Growing Industrial Infrastructure

Vietnam has over 400 operational industrial zones, a rapidly expanding logistics infrastructure, and improving power grid reliability

Industrial infrastructure supports scalable manufacturing operations; reducing the operational barriers that previously limited high-tech production

💡 The Automation Pull Factor

New factories entering Vietnam, particularly in electronics and semiconductor manufacturing, are adopting automation technologies from day one rather than starting with manual processes. Electronics and high-tech sectors alone accounted for more than 65% of new FDI inflows into Vietnam, and these are precisely the sectors with the highest automation intensity. Industrial automation companies entering Vietnam now are entering a market where their primary customers are actively and urgently investing. See also: technology partnership models for industrial sector expansion.

Vietnam’s industrial automation market is one of the fastest-growing in Southeast Asia, driven by the intersection of surging FDI in manufacturing, government digitisation mandates, rising labour costs, and the global push toward Industry 4.0 and smart factory deployment.

Market Metric

Value

Source / Period

Manufacturing Automation Market Size

USD 1.15 billion

2025 estimate (Market Research Outlook)

Manufacturing Automation CAGR

15.4%

2026–2032 forecast period

Manufacturing Automation Market by 2032

USD 3.12 billion

2032 projection

Industrial Automation Market (broader)

USD 917.6 million

2024 (IMARC Group)

Industrial Automation CAGR

8.55%

2025–2033 (IMARC Group)

Industrial Automation Market by 2033

USD 1.92 billion

2033 projection (IMARC)

Top sensor segment share

Over 30% of automation hardware demand

IoT-enabled industrial sensors

Smart sensor adoption

70%+ of newly commissioned industrial equipment includes smart sensors

2023 baseline (market data)

SCADA installation growth

28% year-on-year

Manufacturing and utilities sector

Key Growth Drivers in Detail

📈

Surging FDI in High-Tech Manufacturing

Vietnam attracted over USD 36 billion in FDI in 2023, with electronics and high-tech sectors accounting for more than 65% of new investment inflows. New factories entering the country, particularly in semiconductors, electronics assembly, and automotive components, deploy automation infrastructure from setup, creating immediate demand for robotics, PLCs, industrial sensors, MES systems, and IIoT platforms. This FDI wave is the primary accelerant of the automation market.

Primary Driver

🤖

Rising Labour Costs Justify Automation ROI

Vietnamese manufacturing wages have grown consistently at 7–10% annually. For labour-intensive operations, electronics assembly, garment and textile manufacturing, food processing, the ROI case for automation is crossing the threshold of viability for a growing number of domestic manufacturers. This is converting legacy manual operations into active buyers of robotic systems, automated material handling, and vision inspection technology.

Economic Driver

🏛️

Government Industry 4.0 Strategy

Vietnam’s Resolution 52/NQ-TW on Industry 4.0 mandates smart manufacturing adoption across key industries by 2030. The government’s National Digital Transformation Programme and hi-tech park incentive frameworks provide tax holidays, preferential land rates, and import duty exemptions on automation equipment for qualifying investments. This policy framework is directly accelerating the timeline of automation adoption across both domestic and FDI manufacturers.

Policy Driver

🔗

SME Automation Adoption

Despite strong enthusiasm, a core challenge lies in the scarcity of skilled automation professionals. Many Vietnamese manufacturers lack staff with hands-on experience in PLC programming, IIoT system deployment, and predictive-maintenance analytics. This skills gap, while a challenge, creates the commercial opportunity for automation companies offering not just technology but training, integration services, and managed automation solutions, a higher-margin product that SMEs specifically need.

SME Opportunity

SECTION 3

3 Top Industry Sectors: Where Automation Demand Is Highest

Automation demand in Vietnam is not uniform across sectors. The following eight sectors represent the highest-opportunity targets for industrial automation companies entering the Vietnamese market, combining current adoption velocity, near-term investment pipeline, and structural demand drivers.

💻

Electronics & Semiconductors

Largest automation demand segment, 65%+ of new FDI

Vietnam is now a global hub for electronics manufacturing, Samsung alone accounts for a third of national exports. Foxconn, Intel, LG, and dozens of Tier-1 electronics OEMs have established or expanded operations. New fab and assembly lines deploy SMT automation, PCB inspection, pick-and-place robotics, automated testing, and cleanroom automation from day one.

Vietnam’s automotive sector, Thaco, VinFast, Toyota, Honda, Hyundai, is shifting from assembly to component manufacturing with significant government support. VinFast’s EV production is catalysing a new wave of precision manufacturing investment requiring robotic welding, automated body-in-white assembly, and battery module production automation.

Welding RobotsBody AssemblyEV Battery AutomationQuality Control Systems

🌾

Food & Beverage Processing

High SME adoption potential; significant upgrade cycle

Vietnam is the world’s largest cashew exporter, second-largest coffee producer, and a major seafood exporter. The food processing sector is undergoing rapid modernisation driven by export market quality requirements (EU, Japan, USA). Automation of cleaning, sorting, packaging, and cold-chain logistics is the priority investment for food manufacturers upgrading to international standards.

Vietnam’s pharmaceutical market is growing at ~15% annually, with domestic production increasingly targeting export markets. GMP compliance requirements from WHO, EU-GMP, and US FDA are driving pharmaceutical manufacturers to upgrade from manual to automated production and quality control systems, creating structured demand for filling automation, serialisation, and environmental monitoring systems.

Largest existing manufacturing sector; automation lag opportunity

Vietnam is the world’s third-largest garment exporter. The sector employs over 2.5 million workers, making labour cost sensitivity extremely high. Automation adoption has lagged due to the complexity of flexible material handling, but rapid wage growth is now crossing the ROI threshold for automated cutting, spreading, sewing assistance, and quality inspection systems, particularly among larger export-focused factories.

Vietnam’s rapid industrialisation has created acute energy demand pressure. The government is investing heavily in renewable energy, Vietnam has one of the world’s largest installed solar capacities, and in grid modernisation. SCADA systems, smart grid monitoring, energy management systems, and substation automation are experiencing significant demand growth as the power infrastructure scales to support industrial expansion.

Vietnam’s logistics sector is transforming rapidly, supported by booming e-commerce and export growth. Warehouse automation, automated storage and retrieval systems (AS/RS), conveyor systems, autonomous mobile robots (AMRs), and WMS integration, is being adopted by both 3PL operators and large manufacturers building internal logistics infrastructure to support export operations.

AMRs / AGVsAS/RS SystemsWMS IntegrationConveyor Systems

🏗️

Construction & Building Materials

Infrastructure boom driving process automation

Vietnam’s construction sector is expanding at 8–10% annually, driven by industrial zone development, residential demand, and major infrastructure projects. Building materials manufacturing, cement, steel, ceramics, glass, represents a significant process automation opportunity, with many existing plants operating with outdated control systems ready for modernisation with DCS, PLC upgrades, and process optimisation solutions.

Vietnam operates over 400 industrial zones, economic processing zones, and hi-tech parks, but location selection significantly affects tax incentives, logistics access, labour availability, and operational costs. The most commercially relevant clusters for manufacturing and automation companies are grouped by geographic region.

🔵

Northern Cluster, Hanoi, Bac Ninh, Bac Giang, Hai Phong

Best for: Electronics, semiconductors, high-tech manufacturing, automotive components. This is Vietnam’s most established manufacturing cluster and the primary destination for global electronics investment, Samsung’s major production facilities, LG Electronics, and numerous Korean and Taiwanese suppliers are concentrated here. Bac Ninh and Bac Giang have become known as Vietnam’s “Silicon Valley” for electronics. Hai Phong’s deep-water port provides critical logistics access for export-oriented manufacturing. Key zones include: VSIP Bac Ninh, Quang Chau Industrial Zone (Bac Giang), and DEEP C Industrial Zone (Hai Phong). Corporate tax: 10% for 15 years in hi-tech parks vs. standard 20%.

Electronics Hub

🔵

Hanoi Hi-Tech Park (HHTP)

Best for: R&D, software, precision manufacturing, automation technology companies. Hanoi Hi-Tech Park is Vietnam’s premier designated hi-tech zone, home to Canon, Panasonic, and leading domestic technology companies. Foreign investors in HHTP receive a 10% CIT rate for the first 15 years (4-year exemption + 9-year 50% reduction), import duty exemption on fixed assets, and priority infrastructure access. Automation and technology companies with R&D functions are particularly well-suited to this zone.

R&D & Tech

🟢

Central Vietnam, Da Nang Hi-Tech Park, Chu Lai Open Economic Zone

Best for: Precision manufacturing, automotive, aerospace components, technology services. Da Nang is Vietnam’s third-largest city and a growing manufacturing hub. The Da Nang Hi-Tech Park focuses on electronics, precision engineering, and information technology, with additional incentives mirroring national hi-tech park policy. Chu Lai Open Economic Zone (Quang Nam) is home to Thaco Truong Hai, Vietnam’s largest automotive manufacturer, and is expanding its automotive components ecosystem.

Precision & Auto

🟡

Southern Cluster, Ho Chi Minh City, Binh Duong, Dong Nai, Long An

Best for: Consumer goods, food processing, FMCG, chemicals, light manufacturing, logistics. The southern industrial cluster is Vietnam’s largest manufacturing region by output, with over 70 operational industrial zones across HCMC, Binh Duong, and Dong Nai. Binh Duong, home to VSIP 1 & 2, is the country’s most mature manufacturing province for foreign investors. Dong Nai hosts major food processing operations and chemical manufacturing. Long An is the fastest-growing logistics and light manufacturing destination due to its proximity to HCMC and strategic position at the gateway to the Mekong Delta.

FMCG & Logistics

🟡

Saigon Hi-Tech Park (SHTP), Ho Chi Minh City

Best for: Semiconductor, electronics, medical devices, biotech, advanced manufacturing. SHTP is Vietnam’s leading southern hi-tech zone, Intel’s semiconductor assembly plant, Nidec, Jabil Circuit, and Sanofi operate here. The park offers the same 10%/15-year CIT package as northern hi-tech parks plus import duty exemption on production inputs. Its location in HCMC provides the best access to Vietnam’s talent pool for engineering and technology roles.

Semiconductors

✅ Industrial Zone Selection Criteria

Location selection in Vietnam should assess: proximity to relevant customer base or supply chain; port and logistics access (northern vs southern); labour availability and wages (significantly lower in central and rural zones); power supply reliability (critical for precision manufacturing); available industrial land rates and lease terms; and tax incentive eligibility (hi-tech park vs. standard industrial zone vs. economic processing zone). Engage a Vietnam-registered investment advisory firm for site evaluation before committing to any zone.

SECTION 5

5 Market Entry Modes for Manufacturers & Automation Companies

The right market entry mode for Vietnam depends on your investment size, product category, regulatory requirements, speed-to-market priority, and appetite for operational control. These are the five principal modes available to foreign manufacturers and industrial automation companies.

🏭

Wholly Foreign-Owned Enterprise (WFOE)

Full ownership and operational control. Most common for large-scale manufacturing FDI. Requires Investment Registration Certificate (IRC) and Enterprise Registration Certificate (ERC). Can operate in industrial zones or hi-tech parks with associated incentives. Best for manufacturers committing significant capital to Vietnam operations with a long-term market development strategy.

High Control / Capital Intensive

🤝

Joint Venture with Vietnamese Partner

Partnership with a local entity, sharing ownership and operations. Useful for navigating relationships with government bodies, customers, and suppliers; accessing local market knowledge; and managing some regulatory requirements. Some restricted manufacturing sectors (printing, publishing, certain pharmaceuticals) require local partnership. See: joint venture vs strategic alliance.

Shared Control / Local Knowledge

🏢

Representative Office

Limited to market research, relationship building, and liaison activities, no commercial production or sales permitted. Lowest cost entry mode; useful for market assessment before committing to full investment. Often used by automation companies in the initial 12–24 months of market exploration. Cannot generate revenue in Vietnam.

Low Cost / No Revenue

📋

Contract Manufacturing / Toll Manufacturing

Engage a Vietnamese manufacturer to produce goods to your specification without establishing a legal entity in Vietnam. Lower capital requirement; faster market access; useful for testing market demand before committing to direct investment. IP and quality control require careful contractual management. See: contract manufacturing and toll manufacturing.

Fast Entry / Lower Capital

🚚

Distribution Partnership

Appoint a verified Vietnamese distributor or trading company to sell your automation products in Vietnam without direct establishment. Zero capital investment; fastest route to market; suitable for automation equipment and solution companies who want commercial presence without operational commitment. Requires careful distributor selection and a well-structured distribution agreement. GTsetu provides pre-verified Vietnamese distributors for this route.

Fastest / Zero Capital

🔬

Technology Licensing

License your manufacturing process, automation technology, or IP to a Vietnamese partner who manufactures and sells using your technology. Revenue through royalties; minimal operational burden; suitable where your competitive advantage is technology rather than manufacturing capability. Requires robust technology transfer agreement and strong IP protection. See: licensing vs distribution agreements.

IP-Based Entry

⚡ Fastest Route to Vietnamese Market Revenue

For industrial automation companies that want to generate Vietnamese market revenue within 3–6 months without establishing a legal entity, the Distribution Partnership route, appointing a verified, technically capable local distributor, is the commercially optimal starting point. GTsetu pre-verifies Vietnamese distributors against business registration, trade licences, and relevant technical certifications, giving automation companies confidence that their partner can actually represent their products correctly in market. See also: market entry partnership structures for a full comparison.

SECTION 6

6 Regulatory Framework: Setting Up & Operating in Vietnam

Vietnam’s investment regulatory framework has improved significantly over the past decade, the 2020 Investment Law and 2020 Enterprise Law streamlined foreign investment procedures and reduced the bureaucratic burden for new entrants. However, the process still requires careful navigation and local advisory support.

Regulatory Requirement

Description

Timeline

Key Consideration

Investment Registration Certificate (IRC)

Required for all foreign investment projects above USD 300,000. Obtained from the provincial Department of Planning and Investment (DPI) or Management Authority of Industrial Zones

15–45 days for standard applications

Projects in conditional sectors (pharmaceuticals, chemicals, media) require additional ministry approval, significantly extending the timeline

Enterprise Registration Certificate (ERC)

Establishes the legal entity (limited liability company is most common for foreign investors). Obtained from the DPI following IRC approval

3–5 working days after IRC

Company charter, legal representative designation, and minimum charter capital documentation required

Tax Registration

Register with the General Department of Taxation for corporate income tax (20% standard; 10% in hi-tech parks), VAT (10% standard), and withholding tax purposes

Concurrent with ERC

Hi-tech park CIT incentives (10% for 15 years) require formal hi-tech enterprise certification from the Ministry of Science and Technology

Import/Export Licence

Required for trading companies; manufacturing companies can self-import production inputs. Certain regulated products (chemicals, medical devices, electrical equipment) require product-specific import licences

15–30 days

Automation equipment import duties are generally 0–5% for production inputs; verify HS code classification before finalising

Industrial Zone / Hi-Tech Park Approval

For investments in designated zones, approval from the zone management authority is required separately and precedes DPI application

15–30 days

Zone authorities have different requirements and approval timelines; earlier engagement significantly speeds the overall process

Environmental Impact Assessment (EIA)

Required for manufacturing projects in regulated sectors (chemicals, food processing, certain electronics). Filed with provincial or national Department of Natural Resources and Environment

60–180 days

EIA is the single longest regulatory step for manufacturing investments. Starting EIA process concurrently with IRC application significantly reduces overall timeline

Labour Regulations

Vietnam’s Labour Code governs employment contracts, working hours (48-hour standard week), overtime (200 hours/year standard, 300 with labour authority approval), termination procedures, and social insurance obligations

Ongoing compliance

Foreign workers in technical/management roles require work permits unless exempt. Engage local HR and legal counsel for compliant employment structuring

🇻🇳 Vietnam Investment Incentives for High-Tech & Automation

Manufacturing and automation companies investing in designated Hi-Tech Parks (Hanoi, Ho Chi Minh City, Da Nang, and others) receive: 10% Corporate Income Tax for 15 years (vs. 20% standard); 4-year full CIT exemption + 9-year 50% reduction; import duty exemption on fixed assets, raw materials, and components for high-tech production; preferential land lease rates. To qualify, the enterprise must obtain “high-tech enterprise” status from Vietnam’s Ministry of Science and Technology (MOST), which requires meeting criteria on R&D spend, revenue from high-tech products, and skilled workforce ratios.

SECTION 7

7 Challenges & How to Mitigate Them

Vietnam’s manufacturing and automation opportunity is real and significant, but so are the operational challenges that foreign companies encounter. Understanding these in advance and building mitigation strategies into your market entry plan is essential for a successful expansion.

Challenge

Specifics for Automation Companies

Mitigation Strategy

Skilled Workforce Shortage

Many Vietnamese manufacturers lack staff with hands-on experience in PLC programming, IIoT system deployment, and predictive-maintenance analytics. This affects both end-user adoption capability and the availability of local integration and support talent

Partner with Vietnamese universities (HUST, VNU, RMIT Vietnam) for talent pipeline; offer training and certification programmes as part of your product/service offering; engage local technical colleges for vocational training partnerships

Complex Legacy System Integration

Many existing Vietnamese factories operate older, heterogeneous control systems with poor documentation and no digital twin capability, making automation overlay and integration technically demanding

Build modular, protocol-agnostic integration capability into your offering; develop reference integration cases with major Vietnamese industrial categories; partner with local system integrators who have legacy environment experience. See: co-development partnerships

High Initial Capital Sensitivity

Vietnamese SME manufacturers, a major automation target segment, are highly cost-sensitive. High upfront system costs are the primary barrier to automation adoption in the SME sector

Develop leasing, pay-per-use, or outcome-based pricing models; leverage government SME digitalisation grant programmes; structure pilots with measurable ROI demonstrations before full deployment. See: pricing structures

Regulatory Complexity for Certain Products

Medical devices, certain chemicals, and specific electrical equipment require product registration with Vietnamese regulatory bodies (MOIT, MOH) before sale, adding 6–12 months to market entry timeline in regulated categories

Begin regulatory registration in Vietnam concurrently with other market entry steps; engage a regulatory affairs consultant with Vietnam-specific experience; prioritise product variants already compliant with IEC or CE standards (reduces local testing requirements)

Intellectual Property Protection

Vietnam has improved its IP legal framework significantly but enforcement remains inconsistent. Technology IP shared with local partners without robust contractual protection is at risk of misappropriation

Execute robust mutual NDAs before any technical information is shared; register trademarks and patents with Vietnam’s Intellectual Property Office (NOIP) before market entry; use GTsetu’s built-in NDA workflow and encrypted document exchange for pre-contract IP protection. See: IP ownership

Unverified Partner Risk

Cold outreach to potential Vietnamese distributors or manufacturing partners exposes companies to identity fraud, credential misrepresentation, and information leakage to competitors

Use GTsetu’s compliance-verified partner network, every Vietnamese company on the platform has been vetted against official registries, trade licences, and certifications before engagement. Anonymous discovery protects your market entry strategy during evaluation

SECTION 8

8 Step-by-Step Expansion Process

Expanding a manufacturing or industrial automation business into Vietnam follows a structured sequence. The steps below apply whether you are establishing a direct legal entity, entering through a distribution partnership, or pursuing contract manufacturing, though the specific requirements differ by route.

01

Market Assessment & Sector Targeting

Before any legal steps, conduct a structured market assessment: which Vietnamese industry segments represent the highest demand for your specific products or services? Who are the current market incumbents (Siemens, ABB, Schneider Electric, Mitsubishi Electric, Rockwell, all active in Vietnam)? What is the realistic total addressable market for your offering within 3 years? What partnerships, distribution channels, or customer relationships already exist that you could leverage? This assessment determines your entry mode, zone selection, and resource requirement. Related: global expansion analysis.

02

Entry Mode Selection

Based on your market assessment, select your entry mode: distribution partnership (fastest, lowest capital, appropriate for most automation equipment suppliers), representative office (for market exploration without revenue commitment), contract manufacturing (for products needing local production), or direct legal entity establishment (for long-term, large-scale manufacturing commitment). Most automation companies benefit from starting with a verified distribution partnership and expanding to direct operations as market knowledge and revenue scale. See our market entry partnerships guide for the full decision framework.

03

Verified Partner Discovery

Identify and verify your Vietnamese partners, distributors, manufacturing partners, or technology integrators, before any commercial engagement. Use GTsetu’s compliance-verified platform to browse pre-vetted Vietnamese companies by sector and capability. Anonymous discovery protects your market entry strategy during evaluation. Execute a mutual NDA before sharing any pricing, product specifications, or commercial terms. Verify business registration, import licences, technical capability, and financial standing before committing to any partnership. See: business verification and partnership evaluation criteria.

04

Legal Entity Establishment (If Direct Investment)

For direct investment routes: engage a Vietnam-registered legal firm to prepare investment registration documentation; obtain Industrial Zone or Hi-Tech Park approval if applicable; submit Investment Registration Certificate (IRC) application to the provincial DPI; obtain Enterprise Registration Certificate (ERC); complete tax, social insurance, and banking registrations. Timeline: 3–6 months for standard manufacturing investments; longer for regulated sectors or hi-tech park applications requiring MOST certification. Engage local advisory from day one, navigating the IRC/ERC process without experienced local counsel significantly increases timeline and error risk.

05

Product Regulatory Compliance

Register your products with relevant Vietnamese regulatory bodies: electrical equipment with MOIT (Ministry of Industry and Trade); medical devices with MOH (Ministry of Health); food contact materials with MARD or MOH; hazardous chemicals with MOIT. Engage a Vietnam-registered regulatory consultant to manage the registration process concurrently with other setup steps. Products covered by EVFTA or ASEAN harmonised standards may benefit from recognition, but Vietnam often requires local conformity assessment regardless of CE or other international certifications.

06

Commercial Agreement Execution

With your Vietnamese partner or distribution structure confirmed, execute the commercial agreements: distribution agreement with territory, pricing, and volume commitment terms; exclusivity provisions if applicable; termination clauses; and IP protection provisions. Have agreements reviewed by legal counsel in both your home jurisdiction and Vietnam. Ensure dispute resolution mechanism and governing law are explicitly specified, for Vietnam agreements, Singapore or Hong Kong arbitration is widely used for enforceability. Consider Incoterms selection for logistics risk allocation.

07

Go-to-Market & Relationship Development

Launch commercial operations: participate in Vietnam industry events (Vietnam Manufacturing Expo, Metalex Vietnam, Auto Expo, Vietnam ETE); register on relevant Vietnamese B2B platforms and government supplier registries; develop Vietnamese-language product documentation and application case studies; build relationships with government bodies and state-owned enterprises relevant to your sector. For the automation sector specifically, connecting with Vietnam Automation Society (VAUS) and engaging with Industry 4.0 government working groups provides significant relationship and market intelligence value. See: top places to find B2B leads.

08

Operational Localisation & Scale

As your Vietnamese market operation matures: hire local technical and commercial talent; develop local technical support and service capability (automation customers require post-sale support, and response time matters); adapt pricing and product configuration for Vietnamese market requirements; explore opportunities for local content, assembly, kitting, or component localisation, to qualify for additional government incentives or local procurement requirements from SOE customers. Review your supply chain partner network annually and expand or adjust your distribution network as the market develops.

SECTION 9

9 How GTsetu Connects You with Verified Vietnamese Partners

The most commercially productive route to the Vietnamese market for manufacturers and industrial automation companies is through verified local partners, distributors with active trade relationships, manufacturing partners with proven capability, and technology integrators with relevant technical credentials. GTsetu pre-verifies every Vietnamese company on the platform against official business registries, trade licences, and relevant certifications, so your commercial engagement starts from a position of verified confidence, not optimistic assumption.

🏛️

Compliance Verification

Every Vietnamese company verified against business registration, trade licences, and relevant certifications before they can engage, eliminating identity fraud and credential misrepresentation risk.

🕵️

Anonymous Discovery

Browse Vietnamese partner profiles by sector and capability without revealing your market entry strategy, protecting competitive intelligence during evaluation.

📄

Built-In NDA Workflow

Mutual NDA with digital signatures and full audit trail, executed before any pricing, product data, or IP is shared with a Vietnamese partner candidate.

🔐

Encrypted Document Exchange

Technical specifications, product data sheets, and commercial proposals shared in AES-256 encrypted workspace, no unprotected email attachments.

🌏

100+ Countries Including Vietnam

Active network of verified manufacturers, distributors, and suppliers in Vietnam and across 100+ countries, supporting your global partner strategy.

🚫

Zero Commission

GTsetu takes no success fee on any partnership formed. Your deal economics with your Vietnamese partner stay entirely between you.

GTsetu is particularly valuable for the Distribution Partnership entry route, the fastest and most capital-efficient first step into the Vietnamese market for most automation companies. Rather than relying on trade directory listings (self-reported, unverified) or cold outreach (no identity verification, no NDA infrastructure), GTsetu delivers pre-verified Vietnamese distributors with confirmed trade licences and sector capabilities. Your market entry starts with verified partners, not hopeful introductions. See: B2B secure collaboration and supplier collaboration platforms.

🌏 Explore Other Manufacturing & Automation Expansion Destinations

Q Why is Vietnam a top destination for manufacturing expansion?

Vietnam is a top manufacturing expansion destination because of its strategic position as the leading China+1 alternative in Southeast Asia, a young and rapidly growing industrial workforce, competitive labour costs, a network of 17 free trade agreements providing preferential market access to the EU, UK, ASEAN, Japan, and South Korea, and a government actively incentivising foreign investment in high-tech manufacturing and automation. Vietnam attracted over USD 36 billion in FDI in 2023, marking nearly a 30% increase from the previous year, with electronics and high-tech sectors accounting for more than 65% of new investment inflows. The combination of FTA-backed market access, competitive production costs, and government Industry 4.0 incentives makes Vietnam uniquely attractive for both manufacturing establishment and automation solution deployment.

Q How large is Vietnam’s industrial automation market?

The Vietnam Manufacturing Automation Market was estimated at USD 1.15 billion in 2025 and is expected to grow at a CAGR of around 15.4% during 2026–2032, reaching over USD 3.12 billion by 2032. The broader industrial automation market (including all industrial control systems) reached USD 917.6 million in 2024 with projections to USD 1.92 billion by 2033. Key demand segments include electronics and semiconductor manufacturing (the largest by volume), automotive production, food and beverage processing, pharmaceutical manufacturing, and logistics automation. Sensors represent the top segment, accounting for over 30% of automation hardware demand across sectors.

Q What are the main market entry modes for Vietnam?

The main market entry modes for manufacturing and automation expansion into Vietnam are: (1) Wholly Foreign-Owned Enterprise (WFOE), full ownership with maximum control, most common for large-scale manufacturing FDI; (2) Joint Venture, partnership with a Vietnamese entity, useful for restricted sectors and local market navigation; (3) Representative Office, limited to non-commercial activities, no production or sales; (4) Contract Manufacturing or Toll Manufacturing, engaging a local manufacturer to produce under your specification without establishing a legal entity; (5) Distribution Partnership, appointing a verified Vietnamese distributor to sell your products without direct establishment; and (6) Technology Licensing, earning royalties from a Vietnamese partner using your technology. Most industrial automation companies begin with a Distribution Partnership to generate early market revenue while evaluating the opportunity for deeper investment.

Q What tax incentives are available for manufacturing investment in Vietnam?

Manufacturing and automation companies investing in designated Hi-Tech Parks receive: 10% Corporate Income Tax rate for 15 years (vs. 20% standard rate); 4-year full CIT exemption followed by 9 years at 50% reduction; import duty exemption on fixed assets and production inputs for high-tech activities; and preferential industrial land lease rates. To qualify for hi-tech incentives, the enterprise must obtain “high-tech enterprise” certification from Vietnam’s Ministry of Science and Technology, meeting criteria on R&D expenditure as a percentage of revenue, revenue share from high-tech products, and skilled workforce ratios. Standard industrial zone investments typically receive 2-year CIT exemption and 4-year 50% reduction.

Q Which Vietnamese industrial zones are best for automation and electronics?

For electronics and semiconductor automation: Northern Vietnam is the primary destination, Bac Ninh, Bac Giang, and Hai Phong provinces host Samsung, LG, Foxconn, and hundreds of supplier companies; Hanoi Hi-Tech Park focuses on precision manufacturing and R&D. For southern Vietnam: Saigon Hi-Tech Park (SHTP) hosts Intel, Jabil, and Nidec, with strong semiconductor and precision electronics presence. For automotive automation: Da Nang Hi-Tech Park and Chu Lai Open Economic Zone in Central Vietnam serve the growing automotive cluster. For FMCG and food processing automation: Binh Duong and Dong Nai provinces in Southern Vietnam have the highest concentration of food and consumer goods manufacturers.

Q What are the biggest challenges for industrial automation companies in Vietnam?

The primary challenges are: a shortage of skilled automation professionals (PLC programmers, IIoT specialists, predictive maintenance engineers); price sensitivity among SME customers who need ROI justification for automation investment; complexity of integrating with legacy production systems in existing Vietnamese factories; product regulatory compliance requirements (electrical equipment, medical devices, chemicals require local registration); IP protection (Vietnam’s legal framework has improved but enforcement is inconsistent); and the verification risk of unverified distributor and partner outreach (identity fraud and credential misrepresentation are common in cold outreach contexts). GTsetu addresses the verification and IP protection challenges by providing compliance-verified partner discovery with built-in NDA workflows and encrypted document exchange.

Q How does GTsetu help manufacturers expand into Vietnam?

GTsetu connects manufacturers and industrial automation companies with compliance-verified Vietnamese distributors, local manufacturing partners, and trading companies. Every Vietnamese company on GTsetu has been verified against official business registries, import/export licences, and relevant certifications before they can engage on the platform, eliminating the identity fraud and misrepresentation risk inherent in unverified outreach. Anonymous discovery protects your market entry strategy while you evaluate potential partners. Built-in NDA workflows ensure your pricing, product specifications, and commercial terms are protected before any information is shared. All document exchange happens in an encrypted workspace with full audit trail. And unlike broker-mediated introductions, GTsetu charges zero commission on any partnership formed.

Find Verified Vietnamese Manufacturing & Distribution Partners on GTsetu

Join 500+ verified manufacturers, distributors, and automation companies building international trade partnerships on GTsetu, with compliance-verified Vietnamese partner profiles, built-in NDA workflows, encrypted document exchange, and zero broker commission.

They represents the product, and research team behind GTsetu, a global B2B collaboration platform built to help companies explore cross-border partnerships with clarity and trust. The team focuses on simplifying early-stage international business discovery by combining structured company profiles, verification-led access, and controlled collaboration workflows.

With a strong emphasis on trust, and disciplined engagement, Team GTsetu shares insights on global trade, partnerships, and cross-border collaboration, helping businesses make informed decisions before entering deeper commercial discussions.