How to Expand Your Manufacturing & Industrial Automation Business to Turkey

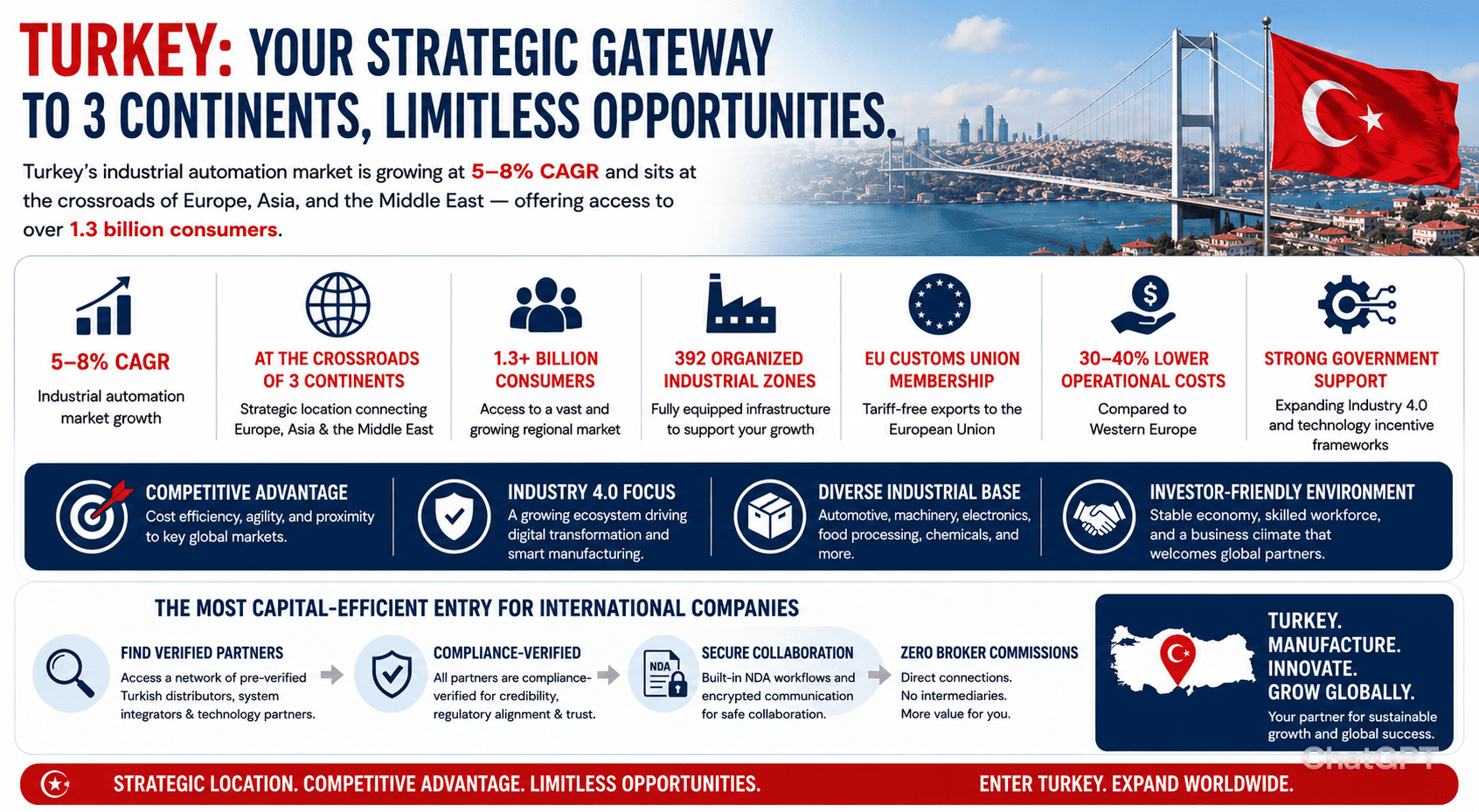

Direct Answer: Turkey’s industrial automation market is growing at 5–8% CAGR and sits at the crossroads of Europe, Asia, and the Middle East, offering access to over 1.3 billion consumers. With 392 Organized Industrial Zones (OIZs), EU Customs Union membership enabling tariff-free exports to Europe, operational costs 30–40% lower than Western Europe, and a government actively expanding its Industry 4.0 and technology incentive framework, Turkey is one of the most strategically compelling manufacturing destinations globally. For international manufacturers and automation companies, the most capital-efficient entry is through a verified Turkish distribution or technology partner, discoverable through GTsetu‘s compliance-verified B2B network with zero broker commissions.

📅 June 2, 2026⏱ 22 min read✍️ GT Setu Editorial Team🔄 Updated regularly

392

Organized Industrial Zones (OIZs)

5–8%

Automation Market CAGR 2025–2032

20+

Free Trade Agreements incl. EU Customs Union

0%

GTsetu Broker Commission

Turkey occupies a uniquely powerful position in the global manufacturing landscape. Physically bridging Europe and Asia, Turkey is simultaneously a major industrial producer for European supply chains, an emerging hub for China+1 production diversification, and a gateway to Middle Eastern, Central Asian, and North African markets. Turkish manufacturing’s share of GDP has grown to over 18%, with a stated government target of 21%, and Istanbul ranked alongside Pune, Bengaluru, and Chennai as one of the world’s top city hubs for industrial automation activity in a 2026 StartUs Insights global analysis.

For international manufacturers, industrial automation OEMs, robotics companies, and sensor and control system providers, Turkey in 2026 represents one of the most strategically versatile market entry opportunities outside of Asia. The country’s EU Customs Union membership removes tariff barriers for European distribution, its 20+ bilateral free trade agreements extend access further, and its government investment incentive framework, including Organized Industrial Zones (OIZs), Free Trade Zones (FTZs), and Technology Development Zones (Technoparks), provides a compelling cost structure for both market-serving and export-oriented manufacturing. This guide covers the complete picture, from market sizing and sector opportunity, to incentive frameworks, regulatory navigation, partner discovery, and the commercial terms that govern successful Turkey market entry. You can also explore our guides on the advantages and disadvantages of global expansion and international business development consulting for broader strategic context.

🇹🇷 Who Is This Guide For?

This guide is written for international manufacturers, industrial automation OEMs, robotics and control system providers, technology integrators, and industrial equipment companies seeking to enter or expand in the Turkish market, whether through a distributor partnership, technology licensing, contract manufacturing, joint venture, OIZ-based production, or direct subsidiary establishment. It is also relevant for companies currently selling into Turkey via informal channels who want to formalise their market presence. If you are exploring other European and Middle Eastern markets alongside Turkey, see our country guides for Germany, Poland, Romania, UAE, and Egypt.

SECTION 1

1 Why Turkey for Manufacturing & Industrial Automation?

🎯 The Strategic Case

Turkey sits at one of the world’s most strategically valuable geographic intersections, with land borders connecting Europe and Asia, sea access via the Bosphorus, and proximity to 1.3+ billion consumers across Europe, the Middle East, Central Asia, and North Africa. For industrial automation companies, Turkey’s combination of a large, modernising manufacturing base, rising EV and electronics investment, government Industry 4.0 mandates, EU Customs Union access, and operational costs 30–40% below Western Europe creates a demand environment that is both structurally strong and commercially attractive for market entry.

18%+

Manufacturing share of Turkey’s GDP, with government target of 21%; one of the highest ratios among G20 economies

67,000+

Companies operating in OIZs across 81 provinces, employing over 2 million people; ready-built industrial infrastructure available

30–40%

Lower operational costs vs. Western Europe, labour, energy, and logistics, per FDI analysis from the Turkish Investment Office

🌍

Unique Geographic Bridge

Turkey’s position between Europe, Asia, and the Middle East provides unparalleled access to multiple markets from a single manufacturing base. Bursa, Istanbul, and Kocaeli are within overnight truck distance of major European markets.

🇪🇺

EU Customs Union Advantage

Turkey’s EU Customs Union membership means goods manufactured in Turkey can be exported to EU member states without tariffs, a decisive advantage for international companies using Turkey as a European supply base.

🤖

Industry 4.0 Adoption Momentum

The Turkish government’s Industry 4.0 strategy, backed by KOSGEB grants and TÜBİTAK R&D incentives, is driving IIoT, robotics, and smart manufacturing adoption across automotive, textiles, chemicals, and food processing sectors.

🏭

Deep Industrial Manufacturing Base

Turkey has one of the most diversified manufacturing sectors in the EMEA region, automotive, textiles, chemicals, steel, food processing, defence, and electronics all operating at significant scale with a large legacy modernisation pipeline.

🚗

EV Transition Investment Wave

Chinese automaker Chery announced a $1 billion investment in a 200,000-vehicle-per-year EV facility in Samsun in 2025. Combined with existing OEM capacity from Ford, Toyota, and Stellantis, Turkey’s EV transition is generating major automation investment demand.

🔗

China+1 Supply Chain Diversification

Global manufacturers diversifying production away from China are actively evaluating Turkey as a European/EMEA production alternative, with its established logistics infrastructure, skilled workforce, and EU-compatible regulatory environment providing strong supply-chain credentials.

Istanbul ranks alongside Pune, Bengaluru, Chennai, and Hyderabad as one of the world’s leading city hubs for industrial automation activity, anchoring manufacturing automation, system integration, and industrial digitalisation for the wider EMEA region. Multiple research firms track Turkey’s industrial automation market, with consistent signals of sustained growth driven by the same structural forces reshaping manufacturing globally.

Istanbul ranked top 5 global automation hub city (2026)

—

Global market USD 325 billion by 2030 at 7.99% CAGR

Turkey as top 5 global hub

6W Research

Growing market; PLCs fastest growing segment at 6.80% CAGR

2032

Strong growth across industrial controls, HMI, drives, robotics

5–8% depending on segment

Note: Market sizing for Turkey’s automation sector varies significantly by scope, narrower definitions covering only factory automation hardware produce smaller numbers, while broader definitions including industrial IoT, software, services, and smart manufacturing infrastructure produce larger estimates. All credible sources agree on the same directional signal: Turkey’s industrial automation market is in sustained growth mode driven by structural manufacturing transformation, not a cyclical spending peak.

Key Market Drivers for International Automation Companies

🏛️

Government Industry 4.0 Strategy & Digital Transformation Mandates

The Turkish government has allocated 5 billion TRY towards grants and subsidies for automation projects under its Industry 4.0 strategy. KOSGEB (Small and Medium Enterprises Development Organization) provides accessible grants for SME automation adoption, dramatically expanding the addressable market beyond large enterprises to Turkey’s vast mid-market manufacturer base.

Policy Driver

🚗

EV Manufacturing & Automotive Transition Investment

Turkey’s automotive sector, the cornerstone of its manufacturing economy, is undergoing rapid electrification. New EV assembly facilities (including Chery’s $1B Samsun plant), battery component manufacturing, and EV drivetrain production lines are all driving significant demand for advanced assembly automation, robotic welding, and precision quality inspection systems.

Sector Driver

💰

Operational Efficiency Imperative & Labour Cost Inflation

Operational efficiency initiatives are projected to save Turkish manufacturers approximately 15 billion TRY annually, according to Ken Research analysis. Rising labour costs in Istanbul, Bursa, and Kocaeli industrial clusters are improving the economics of automation investment, compressing payback periods to under 2 years for many retrofit projects.

Economic Driver

📦

Export Quality Standards Compliance

Turkish manufacturers exporting to European markets face increasingly stringent quality, traceability, and ESG compliance requirements. Meeting CE marking standards, EU environmental directives, and customer-imposed Industry 4.0 reporting requirements is driving investment in automated quality control, production monitoring, and data collection systems across food, textiles, chemicals, and automotive supply chains.

Compliance Driver

🔬

Defence & Aerospace Technology Investment

Turkey’s rapidly growing domestic defence industry, driven by programmes including the Bayraktar TB2 drone, ASELSAN electronics, and TUSAŞ aerospace manufacturing, is driving high-precision automation demand for composite fabrication, avionics assembly, and defence electronics production at standards that require advanced international automation technology.

Defence Driver

🏗️

OIZ Infrastructure Expansion Creating New Automation Demand

Turkey is constructing 118 new Organized Industrial Zones across all 81 provinces, adding to the 274 already operational. Each new OIZ facility, representing a new manufacturing plant or expansion, generates fresh demand for production line automation, process control systems, and industrial connectivity infrastructure during both commissioning and ramp-up phases.

Infrastructure Driver

SECTION 3

3 High-Demand Sectors for Industrial Automation in Turkey

Industrial automation demand in Turkey is concentrated in specific verticals where export competitiveness pressure, government incentives, and productivity imperatives are converging. Turkey’s sector mix is distinct from other major emerging markets, the combination of European export orientation, a deep automotive OEM and Tier 1 base, and a world-scale textile industry creates demand profiles that differ significantly from Asia-Pacific markets.

🚗Largest Segment

Automotive & EV Manufacturing

Turkey’s automotive sector produces over 1.4 million vehicles annually for Ford, Toyota, Stellantis, Renault, and other OEMs, making it one of Europe’s top 5 automotive producers. The EV transition, accelerated by Chery’s $1B investment and the domestic TOGG EV brand, is driving investment in battery assembly automation, robotic welding, precision machining, and quality inspection systems across OEM and Tier 1 suppliers.

Key demand: robotic welding, EV battery assembly, AGVs, vision inspection systems

🧵World Top 5 Exporter

Textiles & Apparel

Turkey is among the world’s top 5 textile exporters, with a mature sector undergoing rapid modernisation to meet European fast-fashion supply chain requirements and ESG compliance standards. Automation investment is focused on spinning and weaving control, cut-make-trim robotics, quality inspection, RFID tracking, and ERP/MES integration for real-time production data.

Key demand: spinning/weaving automation, vision quality control, RFID, MES integration

⚙️5% Export Growth 2024

Machinery & Metal Processing

Turkey’s machinery sector achieved 5% export growth in 2024, with a target of 20% increase by 2025. Machine builders, including marble and granite processing, packaging machinery, and press equipment manufacturers, are driving demand for servo drives, PLCs, HMIs, and integrated control systems, particularly from companies serving European and Middle Eastern end-users who require CE-compliant, internationally supported automation platforms.

Turkey is one of Europe’s largest food exporters, with fruit, vegetables, processed foods, and snacks reaching EU, Middle Eastern, and US markets. Export-oriented manufacturers face FSSC 22000, BRC, and EU food safety compliance requirements, driving investment in processing line automation, filling and packaging systems, CIP (clean-in-place) automation, and cold chain monitoring.

Key demand: filling and packaging lines, CIP systems, temperature monitoring, serialisation

🧪Large Base

Chemicals & Petrochemicals

Turkey’s chemicals sector, one of the EMEA region’s largest, is investing in DCS/SCADA upgrades, safety instrumented systems (SIS), and process optimisation platforms as legacy plants in Izmit, Aliağa, and the Tüpraş refinery complex modernise to meet European export and ESG reporting requirements. The Dahej-style integrated chemical zones in Turkey’s western provinces represent significant recurring automation demand.

Key demand: DCS/SCADA, SIS, process analytics, energy management, emissions monitoring

🛡️High-Priority Sector

Defence & Aerospace

Turkey’s defence industry has undergone a transformation, with ASELSAN, Baykar, TUSAŞ, and Roketsan driving domestic production of drones, avionics, missiles, and aircraft components. High-precision manufacturing requirements for these sectors demand advanced automation: CNC machining, composite fabrication automation, cleanroom assembly, and automated testing and inspection systems that meet NATO and export market standards.

Turkey has strong domestic demand and significant export potential in consumer electronics and white goods, with Arçelik/Beko and Vestel among the world’s largest white goods producers by volume. Production automation investment in PCB assembly, appliance final assembly, and end-of-line testing is a consistent demand driver. Government incentives for high-tech electronics production are attracting further investment.

Turkey’s renewable energy expansion, targeting 50%+ renewables in power generation, is driving solar panel manufacturing, wind turbine component production, and grid management system investment. The steel sector, a major Turkish industry, is investing in energy management automation and predictive maintenance to meet carbon compliance and EU export requirements for green steel products.

Key demand: energy monitoring, predictive maintenance, solar manufacturing automation, SCADA

SECTION 4

4 Key Industrial & Manufacturing Hubs Across Turkey

Turkey’s industrial geography is concentrated along specific corridors, the Marmara region, the Aegean coast, and the central Anatolian heartland, with each region having distinct sectoral specialisations. Understanding this geography is essential for designing distributor networks, service coverage, and sales operation positioning.

🏙️ Marmara Region, Dominant Industrial Core

Istanbul, Bursa, Kocaeli (Izmit), Sakarya, and Gebze constitute Turkey’s largest industrial concentration, automotive (Ford, Toyota, Stellantis), chemicals, electronics, white goods, and logistics. The Bursa-Gebze automotive corridor is the country’s most automation-intensive manufacturing zone.

Key clusters: Bursa Auto OIZ, Gebze OSB, KOSBI Istanbul, Kocaeli Petkim Petrochemical Complex

🌊 Aegean Region, Export Manufacturing Hub

İzmir, Manisa, Denizli, and Afyonkarahisar anchor Turkey’s Aegean industrial base, textiles, food processing, chemicals, marble processing, and export-oriented light manufacturing. İzmir’s Aliağa free zone and ESBAS industrial zone are key entry points for international industrial companies.

Key clusters: Aliağa Free Zone, Manisa OSB, Denizli Textile OIZ, İzmir ESBAS

🏛️ Ankara & Central Anatolia, Defence & Tech

Ankara, Konya, and Eskişehir house Turkey’s defence technology, aerospace, and precision engineering base, ASELSAN, TUSAŞ, Roketsan, and the Turkish Aerospace Industries (TAI) cluster. Government-backed technology incentives and TÜBİTAK R&D centres make this region Turkey’s highest-growth automation investment area for high-precision sectors.

Key clusters: ASELSAN Ankara Campus, TUSAŞ Kazan, Konya Automobile OIZ, Eskişehir Tech Park

🌿 South & Southeast, Textiles & Agri-Processing

Gaziantep, Adana, Mersin, and Kahramanmaraş are Turkey’s textile, food processing, and agri-industrial hubs, with Gaziantep ranking among Europe’s largest carpet and textile manufacturing centres. Port access via Mersin provides direct export logistics for Middle Eastern and African markets.

Key clusters: Gaziantep OSB, Mersin Free Trade Zone, Adana OIZ, Kahramanmaraş Textile Zone

💡 Distribution Network Design for Turkey

For most industrial automation companies entering Turkey, a national distributor headquartered in Istanbul with sub-distributors or regional engineers in Bursa, İzmir, Ankara, and Gaziantep provides the optimal coverage-to-cost ratio in the first 2–3 years. The Bursa-Kocaeli automotive corridor and the Ankara defence-technology cluster are the two highest-priority territories for technology companies. See our guide to building a distributor network for the structural framework, and our guide on international wholesale distributors for qualification criteria.

SECTION 5

5 Market Entry Models: Choosing the Right Approach

The right entry model for your manufacturing or industrial automation business in Turkey depends on your product category, capital availability, long-term Turkey strategy, and whether you intend to serve the Turkish domestic market, use Turkey as an EMEA export platform, or both. Here is the complete menu of entry models with trade-offs specific to the Turkish context.

Entry Model

How It Works

Capital Required

Time to Revenue

Best For

Key Reference

Turkish Distributor / Channel Partner

Appoint a verified Turkish company to stock, sell, and support your products in a defined territory

Very Low

3–9 months

Industrial automation hardware, sensors, PLCs, drives, control systems, standardised products with established Turkish applications

Form a jointly owned Turkish company with an established Turkish manufacturer or distributor, shared equity, governance, and P&L

Moderate (shared)

12–24 months (setup)

Complex technology requiring local integration; defence sector (where Turkish partnership is operationally advantageous); shared capital risk for OIZ manufacturing

Establish production or warehousing in one of Turkey’s 19 Free Trade Zones, outside customs territory, with customs and tax exemptions for export-oriented operations

Moderate

9–15 months (FTZ licence + setup)

Export-oriented manufacturers; regional distribution hub for Middle East and North Africa; companies wanting customs exemptions on imported components

Acquire land and establish production within an Organized Industrial Zone, accessing VAT-free land, enhanced regional incentives, and ready infrastructure

High

18–36 months (land + construction + ramp)

Large-scale manufacturing for Turkish domestic market and EU export; companies qualifying for large-scale investment incentive certificates

💡 Recommended Entry Sequence for Industrial Automation Companies

For most international industrial automation companies entering Turkey for the first time, the optimal sequence is: Year 1–2: Appoint 1–2 verified national or regional distributors, focusing on the Marmara (Istanbul-Bursa-Kocaeli) automotive corridor first, then adding İzmir for the Aegean region and Ankara for defence and technology. Year 2–4: Evaluate establishing a Turkish limited company (Ltd. Şti.) if revenue warrants, enabling direct customer engagement, OIZ incentive access, and greater commercial control. Year 4+: If local production is commercially justified (via OIZ, FTZ, or contract manufacturing), move to the appropriate production model for EU export and Turkish market scale. This staged approach manages risk while building the market knowledge needed to make high-capital entry decisions correctly.

SECTION 6

6 OIZ, Free Zones & Investment Incentives: What Foreign Manufacturers Must Know

🏛️ Incentive Framework Overview

Turkey’s investment incentive framework is one of the most comprehensive in the EMEA region, operating on two parallel tracks: the Investment Incentive System (covering regional, large-scale, strategic, and priority investments) and the Project-Based Incentive System (for investments above 2 billion TRY in high-tech sectors). Foreign companies incorporated in Turkey are treated equally to domestic investors under the Turkish FDI Law (2003) and are fully eligible for all incentive programmes. The combination of OIZ location benefits, Free Trade Zone customs exemptions, Technopark tax incentives, and the Century of Türkiye Development Initiative creates a layered incentive structure that can materially improve the economics of manufacturing in Turkey.

Turkey’s Investment Incentive Tiers: The Six-Region Framework

Incentive Category

Key Benefits

Relevance to Automation Companies

Eligibility

General Investment Incentives

VAT exemption on machinery and equipment imports; customs duty exemption on imported machinery

High, directly reduces cost of importing automation hardware for Turkish production operations

All qualifying investments meeting minimum threshold (TRY 500K in Regions 3–6)

Regional Investment Incentives

Tax reduction (15–90% on corporate tax); social security premium support (2–10 years); land allocation; interest support

Very High, companies establishing production in less-developed regions (Regions 4–6) receive maximum incentive rates including long-term tax reductions

Region-specific qualifying investments; manufacturing, technology and strategic sectors prioritised

OIZ Location Bonus

Investments in OIZs qualify for one region higher incentive rate than geographic location; VAT-free land; 5-year property tax exemption; lower utility costs

Very High, a manufacturer in a Region 3 OIZ receives Region 4 incentive rates; OIZs provide ready infrastructure reducing capital expenditure on site development

Any investment within a qualifying OIZ; 392 OIZs across all 81 Turkish provinces

Large-Scale Investment Incentives

Tax reduction up to 90%; social security support up to 10 years; land allocation; VAT exemption

High, for automation companies establishing large manufacturing operations; automotive, electronics, chemicals, and machinery manufacturing qualify

Minimum investment thresholds vary by sector (automotive: TRY 1 billion+)

Free Trade Zone (FTZ) Operations

Customs duty exemption; income tax exemption on export earnings; no VAT; no currency restrictions; relaxed commercial regulations

High, for export-oriented automation component manufacturing and EMEA distribution hub operations; 19 FTZs across Turkey near major ports and airports

FTZ operating licence from Ministry of Trade; mandatory export orientation (at least 85% of production exported)

Technology Development Zone (Technopark / TDZ)

Corporate income tax and income tax exemption until 2028 for software and R&D income; customs duty exemption; social security premium support

Medium–High, for automation companies with embedded software or IIoT platform elements; 80+ technoparks hosting ~6,000 companies

Activities must qualify as software development or R&D; registration with Ministry of Industry and Technology

KOSGEB & TÜBİTAK Support

KOSGEB grants for SME automation adoption; TÜBİTAK R&D project grants (up to 75% of project costs); TEYDEB industrial R&D support

Medium, your Turkish distributor’s SME customers may access KOSGEB grants to fund automation purchases, expanding the addressable customer base; TÜBİTAK relevant for co-development

KOSGEB: Turkish SMEs; TÜBİTAK: joint R&D projects with Turkish universities or research institutions

🇹🇷 Incentive Strategy for International Automation Companies

Even if your automation company does not directly access investment incentives (most technology distributors don’t qualify for manufacturing incentive certificates), Turkey’s incentive framework is your primary demand signal and market intelligence tool. Every company receiving an Investment Incentive Certificate, publicly listed by the Ministry of Industry and Technology, is a potential buyer of automation, control, and monitoring solutions. The government’s 5 billion TRY allocation for automation grants means Turkish manufacturers who might not otherwise afford automation technology can now access subsidised funding, expanding your addressable market significantly. Align your Turkish distribution strategy with KOSGEB-registered distributors and integrators who can help customers access these grants as part of the sales process.

SECTION 7

7 Regulatory & Compliance Requirements for Entry

Turkey’s regulatory environment for foreign manufacturers and technology companies has a unique character, in many respects aligned with EU standards due to EU Customs Union membership, while retaining its own Turkish Commercial Code, tax framework, and sector-specific requirements. Understanding these requirements before committing to an entry model prevents costly delays.

01

Business Entity Registration & FDI Framework

Turkey’s FDI regime is governed by the Turkish FDI Law (2003), which mandates equal treatment of foreign and domestic investors, no prior approval is required for most sectors. The preferred structures for foreign-owned commercial operations are the Limited Liability Company (Ltd. Şti. / Anonim Şirket Ortaklığı), minimum 2 shareholders, no minimum capital for Ltd. Şti., or the Joint Stock Company (A.Ş.), minimum 50,000 TRY capital, for larger or publicly traded operations. A Turkish trade registry (Ticaret Sicili) registration is required before commercial activity begins. Registration requires Articles of Association, shareholder identification, and a registered Turkish address. YOIKK (Coordination Council for the Improvement of the Investment Environment) streamlines investor procedures and is the primary government body for FDI concern resolution.

02

Tax Registration & Corporate Tax Framework

Corporate tax in Turkey is set at 25% as of 2024, with extensive reductions available under investment incentive certificates (reductions of 15–90% depending on region and sector). VAT (KDV) is standard at 20%, with 10% applying to certain goods and 1% for basic necessities. VAT registration is required before commercial invoicing begins. Turkish tax law provides extensive input tax credit mechanisms, VAT paid on equipment imports and purchases is recoverable. Withholding tax applies to cross-border royalties, technical service fees, and interest, rates vary by double tax treaty (Turkey has treaties with 90+ countries including the US, UK, Germany, Japan, and all major trading partners). Tax residency rules for foreign-owned Turkish subsidiaries are straightforward, Turkey-incorporated entities are taxed on worldwide income.

03

CE Marking & Product Compliance

Due to EU Customs Union membership, Turkey has incorporated most EU product safety and market access directives into domestic law, meaning CE marking is required for most industrial electrical and electronic products sold in Turkey, just as it is for EU markets. This significantly reduces the additional compliance burden for European manufacturers (whose products are already CE marked) while providing a clear compliance pathway for non-European manufacturers who need CE marking for Turkey regardless. Additional Turkish-specific standards may apply for certain product categories, TSE (Turkish Standards Institution) mandatory certification is required for select product groups (electrical household appliances, safety equipment, certain industrial goods). Confirm TSE applicability for your specific product range before finalising go-to-market timelines.

04

Import Customs Duties & Common External Tariff

Turkey applies the EU Common External Tariff (CET) for most industrial goods under the EU Customs Union, meaning import duties for non-EU manufactured industrial automation products into Turkey are aligned with EU tariff rates. This creates a level playing field for European exporters (zero tariff) versus non-European exporters, but also means that products manufactured in Turkey can be exported to EU markets tariff-free. For products with significant Turkish import tariffs, establishing OIZ-based assembly or local production can eliminate this cost disadvantage, and the OIZ VAT and machinery duty exemptions make the economics of local assembly significantly more attractive than paying repeat import duties. Check the specific HS code classification and applicable tariff rate for your products against both EU CET rates and any Turkey-specific bindings that may differ.

05

Intellectual Property Protection

Turkey has a functional IP registration system, the Turkish Patent and Trademark Office (TÜRKPATENT) handles trademark, patent, and design registrations. Trademark registration takes approximately 12–18 months and should be filed before market entry to prevent third-party squatting. For software-embedded industrial automation platforms, confirm whether patent protection is commercially warranted, Turkey’s patent system broadly aligns with European Patent Convention (EPC) standards. Understand IP ownership in contract manufacturing agreements before engaging Turkish OEM or EMS partners, and ensure your NDA agreements are governed by Turkish law with enforceable jurisdiction clauses. See also our guide on who owns tooling and moulds in cross-border manufacturing arrangements.

06

Labour Law & Employment Compliance

Turkish Labour Law No. 4857 applies to all employees working in Turkey, whether for a Turkish subsidiary, representative office, or OIZ facility. Mandatory requirements include: Social Security Institution (SGK) registration for all employees within 30 days of employment commencement; minimum wage compliance (updated biannually); written employment contracts in Turkish; and adherence to termination notice and severance requirements (1 month’s salary per year of service for employees with over 1 year’s tenure). Turkey has a skilled manufacturing workforce, over 32 million people in the labour force, with competitive wage rates relative to Western European markets. Employers in OIZs may benefit from social security premium support under investment incentive programmes, reducing effective labour costs further.

SECTION 8

8 Finding a Verified Turkish Distribution or Technology Partner

For the majority of international manufacturing and industrial automation companies entering Turkey, finding the right Turkish partner, a distributor, system integrator, technology licensor, OEM partner, or joint venture candidate, is the most consequential single decision in the market entry process. As the Schneider Electric Alliance Master Industrial Automation Distributor case study of Botek Automation (Turkey) demonstrates, the right Turkish distributor brings application expertise, sector-specific customer relationships, local engineering support, and access to hard-to-reach industrial clusters that a foreign company cannot replicate independently in the first five years.

What to Look for in a Turkish Industrial Automation Distributor or Partner

✅

Verified Business Identity

Trade registry certificate (Ticaret Sicili Gazetesi), tax identification number, import licence, TSE registration where applicable, and authority letter from an authorised signatory. This is the non-negotiable foundation of any Turkish partnership, see our guide on business verification requirements.

🏭

Sector & Application Expertise

Does the partner have genuine application knowledge in your target sector, automotive, textiles, food processing, chemicals, defence? Turkey’s industrial sectors have distinct technical requirements and buyer behaviours. A distributor with deep automotive OEM relationships in Bursa may have limited relevance in Gaziantep’s textile cluster.

🗺️

Regional Coverage & Service Infrastructure

Does the partner have offices or service engineers in your target industrial regions, Istanbul, Bursa, İzmir, Ankara, Gaziantep? Botek Automation’s model (offices in 10 Turkish regions) represents the gold standard, but assess whether regional presence translates to genuine customer relationships and service capability.

⚡

Technical & Pre-Sales Engineering Capability

Turkish industrial customers, particularly automotive Tier 1 suppliers and defence prime contractors, expect distributors to provide application engineering, system integration support, commissioning assistance, and ongoing technical service. Evaluate the depth and qualification of the partner’s engineering team relative to your product complexity.

📊

Financial Standing & Inventory Capacity

Can the partner fund the inventory required for stock availability and demonstration equipment? Turkish distributors often manage significant inventory for multiple principals, assess their financial capacity and credit rating relative to the working capital requirements of distributing your product range. See our guide on partnership evaluation criteria.

🚫

Competitive Portfolio Check

Many Turkish industrial automation distributors carry competing brands, assess whether their existing portfolio creates conflicts with your product lines. The Turkish market has strong presence from Siemens, Schneider Electric, Rockwell, ABB, and Chinese brands (INVT, Delta). Understand where your offering fits relative to incumbents in the distributor’s current sales portfolio.

🌐

E-Commerce & Digital Capability

The Schneider Electric / Botek case study highlighted that Turkish machine builders value online ordering and rapid delivery visibility. Assess whether your potential Turkish distributor has digital ordering capability, this is increasingly a differentiating factor in competitive sales situations with Turkish OEM customers who require fast, transparent product fulfilment.

🔐

Data Security & NDA Practices

Industrial automation partnerships involve sharing technically sensitive information. Require execution of a mutual NDA governed by Turkish law before any sensitive technical or commercial data exchange. Use encrypted channels for all sensitive sharing, see our guide to B2B secure collaboration.

Channels for Finding Verified Turkish Partners

💻

GTsetu Verified B2B Platform

GTsetu provides access to compliance-verified Turkish manufacturers, distributors, and technology partners across all industrial sectors, with anonymous discovery, built-in NDA workflow, and encrypted collaboration. Zero broker commissions on every partnership formed. Compare with alternatives to Alibaba for open marketplace comparisons, and explore our supplier collaboration platforms guide for platform selection criteria.

Best for Verified Discovery

🎪

Turkish Industrial Trade Shows

WIN Eurasia (Automation & Robotics, Istanbul, held biannually), HANNOVER MESSE Turkey partner events, Metal Istanbul, Automechanika Istanbul, Eurasia Packaging, and MSPO defence fair are the primary venues for meeting potential Turkish industrial partners face-to-face. See our guide on top places to find B2B networking leads.

In-Person Channel

🏛️

Bilateral Chambers of Commerce

Turkish-German Chamber of Commerce (TD-IHK), American-Turkish Council (ATC), British-Turkish Chambers of Commerce, and Japan-Turkey Business Council provide verified member directories of Turkish companies actively seeking international principal relationships. Strong for warm introductions and community building in specific bilateral corridors.

Community Channel

🏢

TOBB, MÜSİAD & Industry Associations

The Union of Chambers and Commodity Exchanges of Turkey (TOBB), the Independent Industrialists and Businessmen’s Association (MÜSİAD), MESS (Turkish Metal Industrialists Association), OSD (Automotive Industry Association), and sector-specific bodies maintain member directories and host networking events that surface qualified Turkish industrial companies seeking international partnerships. See our B2B business network guide for more.

Association Channel

🌐

Turkish Investment Office (Presidency of the Republic)

Turkey’s Investment Office, operating under the Presidency of the Republic, provides sector-specific market entry support, Investment Incentive Certificate guidance, and introductions to qualified Turkish industrial partners and OIZ operators. The 2024–2028 Turkey International Direct Investment Strategy actively targets increasing FDI from 0.85% to 1.5% of global FDI inflows, with dedicated resources for incoming manufacturer facilitation.

Government Channel

SECTION 9

9 Step-by-Step Turkey Market Entry Roadmap

01

Market Prioritisation, Validate Before Committing

Before investing in Turkey entry, validate the market opportunity for your specific product category. Which Turkish industrial verticals have the highest automation investment intensity for your product type? What is the competitive landscape, which global automation brands already have established Turkish distribution, and where are the gaps? A 4–6 week desk research and Turkey visit programme, structured around conversations with potential Turkish distributors and end-users, will reveal more than any market research report. Use GTsetu’s platform to identify and anonymously assess potential Turkish partners before revealing your market entry plans. Explore our guide on cross-border business partnerships for the validation framework.

02

Entry Model Selection, Match to Your Situation

Select your entry model based on validated market intelligence and your strategic objectives. For most first-time Turkey entrants, a verified national distributor relationship is the right first step. Confirm whether OIZ or FTZ structures are relevant for your longer-term production strategy. Assess CE marking and TSE certification requirements early, they affect your go-to-market timeline regardless of entry model. Review the full trade-offs in our market entry partnerships guide before deciding. If considering white-label production for Turkish or export markets, see our white-label vs. private label manufacturing guide.

03

Ideal Partner Profile Definition

Define precisely what you need in a Turkish partner: geographic coverage (national vs. regional; Marmara vs. Aegean vs. Central Anatolia), sector specialisation (automotive / textiles / food / chemicals / defence), technical capability (engineering staff for application support), inventory financing capacity, and complementary product portfolio. The more specific your ideal partner profile, the faster GTsetu’s verified network surfaces relevant candidates. See our guide on distributors and manufacturers relationships for the profile framework.

04

Partner Discovery & Verification

Discover candidates through GTsetu’s verified platform, trade show attendance, bilateral chamber engagement, and referral from existing supply chain contacts. For every candidate, complete formal verification before engagement: trade registry certificate, tax ID, import licence, and relevant sector certifications. GTsetu performs this verification for all companies on its platform, eliminating the due diligence burden. See our complete business verification requirements checklist for independent verification steps.

05

NDA Execution & Secure Technical Exchange

Execute a mutual NDA governed by Turkish law before sharing any technical data, product specifications, pricing, application notes, or market strategy. All technical data exchange should occur through encrypted channels. On GTsetu, the NDA workflow is built in and activated before the encrypted workspace unlocks. Ensure your NDA addresses non-compete and non-circumvention provisions explicitly under Turkish contract law.

Execute the manufacturer-distributor contract with review by Turkish legal counsel, not just your home country lawyer. Turkish contract law (Turkish Code of Obligations) has specific enforceability requirements for exclusivity, IP assignment, and non-compete provisions. Address dispute resolution explicitly, specify whether Istanbul arbitration (ISTAC), ICC arbitration, or Turkish court jurisdiction applies. Include appropriate force majeure provisions and risk allocation mechanisms relevant to Turkey’s operating environment. Engage your Turkish lawyer to review the business partnership contract for local law compliance.

08

Market Launch & Partner Enablement

A successful Turkey launch requires more than shipping the first container. Invest in: distributor technical training (product application, competitive positioning, troubleshooting); co-development of Turkish-language commercial and technical materials; joint visits to key target accounts in the first 90 days; first reference installation supported by your own technical resources; and a shared marketing activation plan covering Turkey-specific trade publications, digital channels, and sector events. The first 6 months in any new Turkish partnership are critical, under-invest in enablement and the relationship stalls before momentum builds. Leverage the global partner service framework to structure your enablement programme.

SECTION 10

10 Key Commercial Terms for Turkey Partnerships

Turkey-specific commercial dynamics require important adjustments to standard international distribution agreement terms. Currency dynamics, inflation, and the OIZ incentive landscape create unique commercial considerations that must be addressed explicitly in partnership agreements.

Commercial Term

Turkey-Specific Consideration

Reference Guide

Currency & Inflation Risk

Turkey has experienced significant currency depreciation over extended periods. USD- or EUR-denominated supply pricing with TRY resale pricing creates substantial currency risk for Turkish distributors. Address this explicitly: annual TRY price adjustment mechanisms, USD/EUR denominated resale pricing for large projects, or automatic price revision bands tied to exchange rate movements. This is the most critical Turkey-specific commercial term.

Turkish distributors typically request 30–60 day credit terms. In a high-inflation environment, extended credit terms erode the real value of receivables, calibrate credit limits carefully and consider credit insurance for Turkish receivables. Start new relationships with advance payment or LC for the first 3–5 orders before extending open account terms. See our payment terms guide.

While Turkey applies EU CET rates for most goods, tariff rates can change, particularly for products where Turkey has additional protection or safeguard measures beyond the CET. Specify whether changes in Turkish import duty rates trigger automatic price adjustment or require renegotiation, and in which direction the adjustment applies.

Turkey’s geographic and sectoral diversity supports region-specific or sector-specific exclusivity rather than national exclusivity for first-time partnerships. Consider structuring exclusivity by OIZ cluster (Bursa automotive, Gaziantep textiles) rather than nationally for first partnership, with national exclusivity earned through performance. See our exclusivity clauses guide.

Turkish machine builders and OEM customers, particularly those serving European just-in-time supply chains, expect fast delivery. Distributors must maintain local stock for fast-moving products. Define minimum stock requirements and maximum acceptable lead times in the agreement. Short lead times are a competitive differentiator in the Turkish automation market.

Turkish industrial customers expect local warranty and after-sales service, not international return-to-manufacturer warranties. Define which warranty functions the Turkish distributor performs, response time SLAs by customer type (OEM vs. end-user), and how warranty costs are shared between principal and distributor.

Annual volume commitments must reflect Turkish market development realities, not home market expectations. First-year minimums should allow for the 6–12 month market development phase before ratcheting in years 2–3. Denominate commitments in units or USD value, not TRY, which is subject to inflation distortion. See our volume commitments guide.

Turkish distribution agreements should specify notice periods (3–6 months), post-termination inventory buyback obligations, and non-competition restrictions. Turkish courts have historically enforced reasonable non-compete provisions, ensure they are time-limited (max 2 years) and geographically scoped. Define every exit scenario explicitly. See our termination clauses guide.

Turkey has experienced significant TRY depreciation over extended periods, a reality that directly affects distributor profitability on USD- or EUR-priced imports. Structure price review mechanisms, USD-denominated project pricing for large deals, and TRY adjustment clauses into your distribution agreement from day one rather than handling currency pressure reactively.

🐢

Relationship-Driven Sales Cycles

Turkish industrial procurement is relationship-intensive, buying decisions for capital equipment are often made on the strength of personal trust built over multiple interactions, plant visits, and reference installations. Plan for longer relationship-building lead times than in more transactional European markets, and ensure your Turkish distributor has genuine C-level access at target accounts.

💬

Price Competition from Chinese Brands

Chinese automation brands, Delta, INVT, Inovance, Huawei, compete aggressively on price in the Turkish market. Position on application engineering support, CE compliance, supply chain reliability, European export compliance for Turkish manufacturers, and total cost of ownership. Turkish machine builders serving European OEM customers often specifically require international-pedigree automation for end-customer approval, your quality positioning is commercially valid.

🌍

Geographic and Sectoral Complexity

Turkey is a large, diverse market, automotive in Bursa/Kocaeli operates very differently from textiles in Gaziantep or defence in Ankara. A single national distributor may lack genuine depth across all regions and sectors. Consider a national distributor plus sector or region-specific sub-distributors or agents, particularly for the automotive corridor and the defence-technology cluster.

📋

Bureaucratic Complexity & Process Navigation

Despite significant improvements under YOIKK, Turkish regulatory processes, investment incentive certificate applications, OIZ allocation, trade registry changes, can involve bureaucratic complexity. Working with an experienced Turkish legal and regulatory advisor from the start significantly compresses timelines and reduces the cost of compliance errors.

🔒

IP Protection Vigilance

While Turkey’s formal IP framework is sound, vigilance is required in practice, particularly for technology that is embedded in machinery or software that a Turkish partner could theoretically replicate. Maintain version control on technical documentation shared with partners, use GTsetu’s encrypted workspace for all sensitive technical exchanges, and register trademarks and key patents before market entry rather than after.

SECTION 12

12 How GTsetu Connects You with Verified Turkish Partners

🇹🇷 GTsetu, Verified B2B Platform for Turkey Market Entry

Discover Verified Turkish Manufacturers & Distributors, No Broker Commission

GTsetu provides international manufacturing and industrial automation companies with direct access to compliance-verified Turkish manufacturers, distributors, system integrators, and technology partners, across every industrial sector and all major manufacturing regions. Every company in GTsetu’s Turkey network has been verified through trade registry documentation, tax ID, import/export licences, industry certifications, and authority letter confirmation before appearing in the platform. You discover, qualify, and engage, without broker intermediaries taking a cut of your commercial economics. Explore how GTsetu compares with our guides on alternatives to IndiaMart and alternatives to TradeIndia for open marketplace comparisons, and see our global collaboration examples to understand what verified partnerships look like in practice.

🏛️

Multi-Layer Compliance Verification

Every Turkish partner on GTsetu has been verified: trade registry, tax ID, import licences, industry certifications, by GTsetu’s compliance team. Eliminates fraud risk and due diligence workload.

🕵️

Anonymous Discovery

Browse verified Turkish partner profiles without revealing your identity. Protect your Turkey market entry strategy until you choose to engage. Not possible via open trade directories.

📄

Built-In NDA Workflow

Digital mutual NDA with timestamped signatures activated before sensitive technical or commercial data can be exchanged. Governed by Turkish or mutually agreed law.

🔐

Encrypted Document Workspace

AES-256 encryption at rest, TLS in transit. Role-based access controls. Full audit trail. Exchange product specs, pricing, and technical proposals securely, never through unprotected email.

🚫

Zero Broker Commission

GTsetu charges zero commission on any partnership formed. All commercial economics stay between you and your Turkish partner.

🌏

100+ Countries Including Turkey

GTsetu’s verified network covers all major Turkish industrial regions as well as India, China, Germany, and 100+ countries globally for your multi-market expansion.

QWhy should I expand my manufacturing or industrial automation business to Turkey?

Turkey offers one of the most strategically compelling market entry cases in the EMEA region for manufacturing and industrial automation companies. Turkey bridges Europe, Asia, and the Middle East, providing access to 1.3+ billion consumers from a single base. EU Customs Union membership enables tariff-free exports to EU markets. Operational costs are 30–40% below Western Europe. The industrial automation market is growing at 5–8% CAGR, driven by EV manufacturing investment (including Chery’s $1B Samsun facility), Industry 4.0 adoption, government automation grants, and a large installed base of legacy equipment in automotive, textiles, chemicals, food processing, and defence that is actively modernising. The government’s 392 Organized Industrial Zones provide ready infrastructure, VAT-free land, and enhanced investment incentives that make Turkey genuinely competitive for international manufacturing establishment. Istanbul ranks globally as a top 5 city hub for industrial automation activity alongside Pune, Bengaluru, Chennai, and Hyderabad.

QWhat are the best entry models for expanding a manufacturing or automation business to Turkey?

For most first-time Turkey entrants in industrial automation and manufacturing technology, the recommended entry sequence is: (1) Appoint a verified Turkish national distributor or regional channel partners, lowest capital, fastest market access (3–9 months to first revenue). Focus the first distributor appointment on the Marmara region (Istanbul-Bursa-Kocaeli automotive corridor) which represents the largest automation demand concentration. (2) After 2–3 years of validated market presence, evaluate establishing a Turkish Ltd. Şti. (limited liability company) for greater commercial control and direct access to OIZ investment incentives. (3) If local production is commercially justified, for EU export or large-scale Turkish market supply, pursue OIZ-based production, Free Trade Zone operations, or contract manufacturing via a qualified Turkish EMS partner. Technology licensing to a Turkish partner is appropriate where local production matters but direct establishment is premature. Joint ventures are most suitable for defence-related sectors or for sharing the capital risk of OIZ manufacturing establishment.

QWhat incentives does Turkey offer foreign manufacturers?

Turkey’s investment incentive framework is among the most comprehensive in the EMEA region. Key incentives for foreign manufacturers: (1) General investment incentives, VAT exemption and customs duty exemption on imported machinery and equipment for qualifying projects. (2) Regional investment incentives, corporate tax reduction of 15–90% depending on region and sector; social security premium support for 2–10 years; land allocation at below-market rates. (3) OIZ location bonus, investments in Organized Industrial Zones receive one-region-higher incentive rates; VAT-free land acquisition; 5-year property tax exemption; lower utility costs. There are 392 OIZs across all 81 Turkish provinces, with 274 currently operational. (4) Free Trade Zone benefits, customs duty exemption; income tax exemption on export earnings; no VAT; relaxed commercial regulations, for export-oriented manufacturers. (5) Technology Development Zone (Technopark) incentives, corporate income tax exemption until 2028 for software and R&D income. (6) KOSGEB grants, accessible government grants for SME automation adoption that can expand the addressable customer base for international automation companies. (7) TÜBİTAK R&D support, up to 75% of R&D project costs for qualifying joint development projects with Turkish research institutions.

QHow do I find a verified distributor for industrial automation products in Turkey?

The most efficient and secure route to finding a verified Turkish industrial automation distributor is through GTsetu’s compliance-verified B2B platform, where every Turkish company has been verified through trade registry documentation, tax ID, import licences, and industry certifications before appearing in the network. GTsetu enables anonymous discovery of verified Turkish partner profiles, digital NDA execution before sharing technical data, and secure encrypted workspace collaboration, all with zero broker commissions. Supplement with targeted trade show attendance (WIN Eurasia Automation, Metal Istanbul, Automechanika Istanbul), bilateral chamber engagement (TD-IHK German-Turkish Chamber, ATC American-Turkish Council), and TOBB/MÜSİAD member introductions. Always verify candidates independently, or use a platform where pre-verification is already complete, before sharing product specifications or pricing. See our guide on how to find international distributors for the complete methodology, and our guide on industrial business collaboration for structuring the partnership once found.

QWhat are the key regulations for manufacturing companies entering Turkey?

Key regulatory requirements for manufacturing companies entering Turkey: (1) Business entity registration, Limited Liability Company (Ltd. Şti.) is the standard structure for foreign-owned commercial operations; Joint Stock Company (A.Ş.) for larger operations. Registration is with the Turkish Trade Registry (Ticaret Sicili). (2) FDI framework, Turkish FDI Law (2003) mandates equal treatment of foreign and domestic investors; no prior approval required for most manufacturing sectors. (3) Tax registration, corporate tax at 25% (with extensive reductions under investment incentive certificates); VAT at 20% standard rate. (4) CE marking, required for most industrial and electrical products under EU Customs Union alignment; significantly reduces compliance burden for CE-certified European manufacturers. (5) TSE certification, Turkish Standards Institution mandatory certification for select product categories; confirm applicability for your specific products. (6) OIZ and FTZ licences, sector-specific; apply through Ministry of Industry and Technology with Turkish legal support. (7) Labour law compliance, Turkish Labour Law No. 4857; SGK (Social Security Institution) registration mandatory for all employees. Engage Turkish legal counsel for entity-specific advice before committing to an entry structure.

QWhich industrial sectors in Turkey have the highest automation investment demand?

The sectors with the highest industrial automation investment demand in Turkey in 2026 are: (1) Automotive and EV manufacturing, the largest automation demand segment, concentrated in Bursa, Kocaeli, and Samsun; EV transition investment (including Chery’s $1B facility and TOGG’s domestic EV programme) driving battery assembly, robotic welding, and precision inspection demand. (2) Textiles and apparel, Turkey is a top 5 global textile exporter; automation investment driven by European export compliance and fast-fashion supply chain requirements. (3) Machinery and metal processing, 5% export growth in 2024; machine builders serving European OEM customers drive PLCs, servo systems, and HMI demand. (4) Food and beverage processing, export-oriented manufacturers automating for FSSC 22000 and BRC compliance. (5) Defence and aerospace, ASELSAN, Baykar, TUSAŞ driving high-precision assembly automation, composite fabrication, and automated testing demand. (6) Electronics and white goods, Arçelik/Beko and Vestel driving PCB assembly, end-of-line testing, and appliance assembly automation. The Marmara region (Istanbul-Bursa-Kocaeli) accounts for the largest automation demand concentration; Central Anatolia (Ankara) is the fastest-growing for defence and technology sectors.

QHow do I handle currency risk when distributing through a Turkish partner?

Currency risk is the most important Turkey-specific commercial consideration in a distribution partnership. Turkey has experienced significant TRY depreciation over extended periods, meaning a Turkish distributor buying from you in USD or EUR and selling in TRY faces compounding margin erosion if currency risk is not managed structurally. The most effective approaches: (1) USD or EUR denominated resale pricing for large capital equipment projects, Turkish industrial buyers are accustomed to foreign currency pricing for capital goods. (2) Annual or semi-annual TRY list price revision mechanisms tied to a defined exchange rate benchmark. (3) Automatic price adjustment bands, if TRY/USD moves beyond a defined threshold (e.g. ±5%), prices adjust automatically without renegotiation. (4) Distributor FX hedging, encourage or support your Turkish distributor in using TRY/USD forward contracts for large, predictable order pipelines. Define the currency risk allocation mechanism explicitly in the distribution agreement, vague terms on this point create the most common disputes in Turkey partnerships. See our pricing structures guide for the full framework.

Ready to Expand Your Manufacturing Business to Turkey?

Connect with verified Turkish manufacturers, distributors, and technology partners on GTsetu, with compliance-backed verification, anonymous discovery, built-in NDA workflows, and zero broker commissions on every Turkey market partnership you form.

They represents the product, and research team behind GTsetu, a global B2B collaboration platform built to help companies explore cross-border partnerships with clarity and trust. The team focuses on simplifying early-stage international business discovery by combining structured company profiles, verification-led access, and controlled collaboration workflows.

With a strong emphasis on trust, and disciplined engagement, Team GTsetu shares insights on global trade, partnerships, and cross-border collaboration, helping businesses make informed decisions before entering deeper commercial discussions.