How to Expand Your Manufacturing & Industrial Automation Business to India

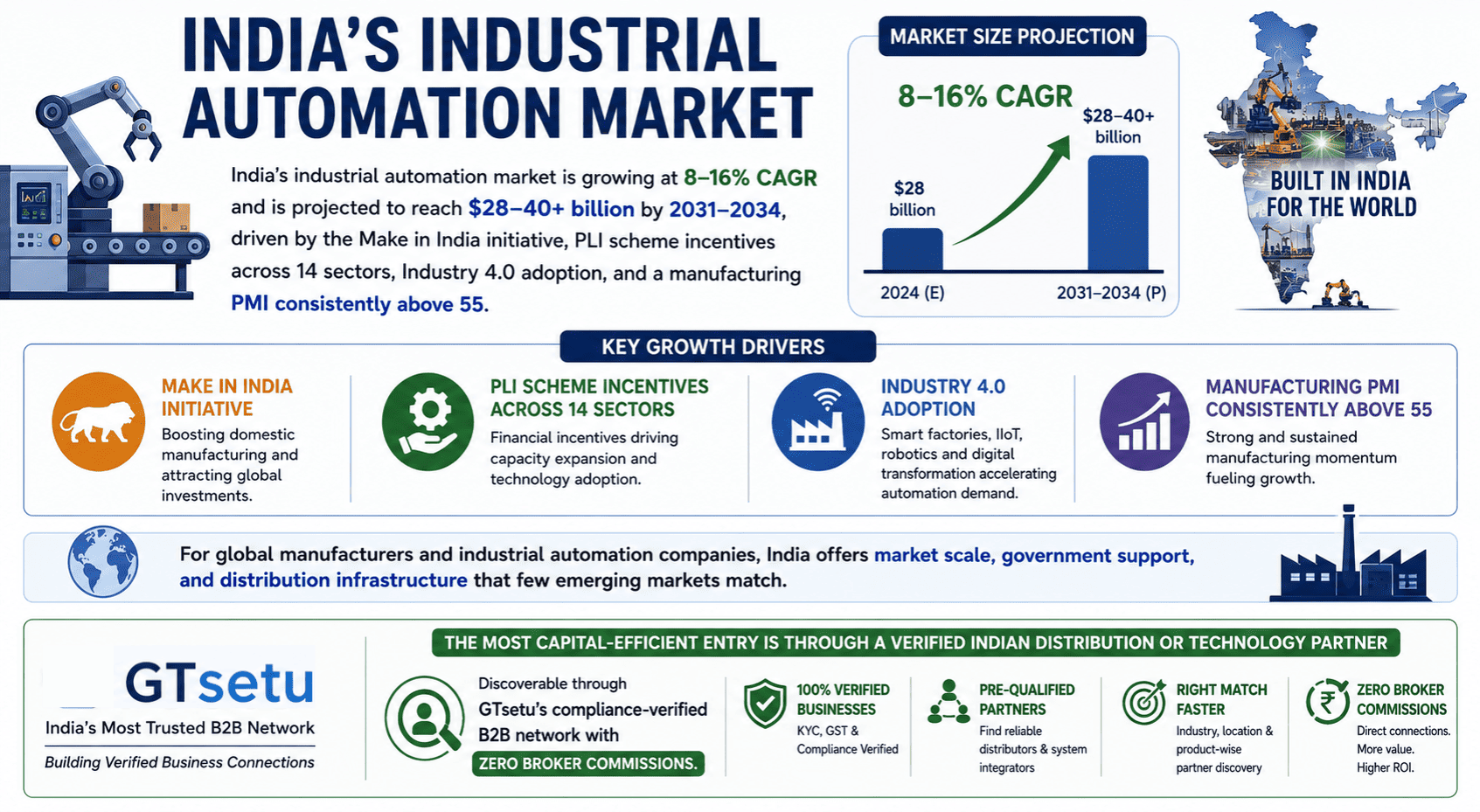

Direct Answer: India’s industrial automation market is growing at 8–16% CAGR and is projected to reach $28–40+ billion by 2031–2034, driven by the Make in India initiative, PLI scheme incentives across 14 sectors, Industry 4.0 adoption, and a manufacturing PMI consistently above 55. For global manufacturers and industrial automation companies, India offers market scale, government support, and distribution infrastructure that few emerging markets match. The most capital-efficient entry is through a verified Indian distribution or technology partner, discoverable through GTsetu‘s compliance-verified B2B network with zero broker commissions.

📅 April 5, 2026⏱ 21 min read✍️ GT Setu Editorial Team🔄 Updated regularly

$28B+

India Automation Market by 2031

8–16%

CAGR 2026–2031

14

PLI Scheme Sectors

0%

GTsetu Broker Commission

India has crossed a strategic inflection point in its manufacturing and industrial automation journey. No longer simply a low-cost assembly hub, India is actively positioning itself as a global manufacturing powerhouse, with a manufacturing PMI of 59.2 in late 2025, the largest young workforce on the planet, a government committing over $24 billion in production-linked incentives, and an industrial automation market expanding at 8–16% annually depending on segment.

For international manufacturers, industrial automation OEMs, technology integrators, robotics companies, and sensor and control system providers, India in 2026 represents one of the highest-potential market entry opportunities globally. But the path from intent to revenue requires navigating a specific set of regulatory, commercial, and partner qualification challenges that are unique to the Indian market. This guide covers all of it, from market sizing and sector-by-sector opportunity, to entry model selection, PLI scheme eligibility, partner discovery, and the commercial frameworks that govern successful India market entry. You can also explore our guides on advantages and disadvantages of global expansion and international business development consulting for broader strategic context.

🇮🇳 Who Is This Guide For?

This guide is written for international manufacturers, industrial automation OEMs, robotics and control system providers, technology integrators, and industrial equipment companies seeking to enter or expand in the Indian market, whether through a distributor partnership, technology licensing, contract manufacturing, joint venture, or direct establishment. It is also relevant for companies currently selling into India via informal channels who want to formalise their market presence. If you are planning expansion into other markets as well, see our country expansion guides below.

SECTION 1

1 Why India for Manufacturing & Industrial Automation?

🎯 The Strategic Case

India is simultaneously the world’s most populous country, the fifth-largest economy, the fastest-growing major manufacturing base, and the government most aggressively incentivising industrial investment among all major emerging markets. For industrial automation companies, the convergence of rising labour costs, a government mandate for smart manufacturing, a massive installed base of legacy industrial equipment due for modernisation, and 14-sector PLI scheme incentives creates a demand environment that is structurally different, and more durable, than cyclical commodity-driven growth in comparable markets.

59.2

India Manufacturing PMI (Oct 2025), strong order growth, faster output, sustained job gains

$24B

PLI scheme allocation across 14 manufacturing sectors, accessible to foreign companies incorporated in India

~20%

operational cost reduction reported by manufacturers adopting smart technologies, Nexdigm / India Automation Market analysis

📈

Fastest-Growing Major Economy

India’s GDP growth consistently outpaces other major economies, creating domestic demand for industrial goods and automation solutions across every manufacturing vertical.

🏭

Make in India Mandate

The government’s Make in India initiative, backed by PLI schemes and industrial policy, is driving a fundamental shift from import-dependent manufacturing to domestic production, creating sustained demand for automation technology.

🤖

Industry 4.0 Adoption Wave

India’s manufacturers are adopting IIoT, AI, robotics, and MES platforms at accelerating rates. Sensor prices have fallen significantly; 5G rollout is expanding; government Industry 4.0 demonstration centres are reducing SME adoption barriers.

🔄

Massive Legacy Modernisation Pipeline

Decades of capacity investment in textiles, pharmaceuticals, chemicals, and food processing have created a large installed base of legacy equipment that is now at the economic threshold for automation retrofit, creating a recurring upgrade demand cycle.

💼

China+1 Supply Chain Diversification

Global manufacturers actively diversifying production away from China are selecting India as a primary alternative, bringing their automation technology suppliers and integrators with them, creating both direct and indirect demand.

🌍

Export Platform for South & Southeast Asia

A manufacturing or distribution presence in India provides a natural platform for serving regional and global export markets through India’s trade infrastructure, port connectivity, and bilateral trade agreements, particularly into the Middle East, Africa, Europe, and Asia-Pacific where GTsetu maintains verified partner networks.

SECTION 2

2 India Industrial Automation Market: Size & Growth 2026

India’s industrial automation market is one of the most actively researched and hotly forecast segments in Asian manufacturing. Multiple research firms track this market with slightly different scope definitions, but all converge on the same directional conclusion: strong, sustained double-digit growth driven by the same structural forces.

Research Source

2025 Market Value

Forecast Horizon

Projected Value

CAGR

Mordor Intelligence

USD 17.28 billion

2031

USD 28.73 billion

8.41%

IMARC Group

USD 8.22 billion

2034

USD 16.67 billion

8.17%

Verified Market Research

USD 16.5 billion (2024)

2032

USD 41.56 billion

14.11%

BlueWeave Consulting

USD 15.1 billion (2024)

2031

USD 40.8 billion

16.2%

Renub Research

USD 3.64 billion

2034

USD 13.65 billion

15.82%

Variance in market sizing across research firms reflects different scope definitions, some include only factory automation hardware, others include software, services, and industrial IoT. The consistent signal: India’s industrial automation market is growing at 8–16% CAGR depending on segment, and every credible forecast points to a multi-decade demand expansion driven by structural manufacturing transformation rather than a cyclical investment spike.

Key Market Drivers for International Companies

🏛️

Government Production-Linked Incentive (PLI) Disbursements

PLI investments have crossed ₹3.2 lakh crore ($38B) with production already exceeding ₹7.5 lakh crore ($90B) by March 2025, driving factory capacity investment that pulls through automation technology demand in every incentivised sector.

Policy Driver

💡

Sharp Fall in Sensor and Component Prices

The cost of PLCs, HMIs, sensors, and edge computing modules has fallen significantly, compressing automation ROI timelines to under two years for many discrete manufacturing retrofit projects, dramatically expanding the addressable market beyond large enterprises to mid-market manufacturers.

Cost Driver

📊

Rising Labour Costs in Industrial Centres

Labour cost inflation in industrial states, Maharashtra, Gujarat, Tamil Nadu, Karnataka, is improving the economics of automation investment for manufacturers previously reliant on low-cost manual assembly. This trend is structural, not cyclical.

Economic Driver

🌐

5G Rollout and Industrial IoT Expansion

India’s 5G network expansion is enabling Industrial IoT deployments at scale, real-time machine monitoring, predictive maintenance, connected factory infrastructure, creating demand for the wireless sensors, edge gateways, and connectivity infrastructure that IoT-enabled automation requires.

Technology Driver

♻️

Carbon Compliance and ESG Requirements

Carbon-credit compliance deadlines are pushing energy-intensive Indian manufacturers, steel, cement, chemicals, glass, toward automated energy monitoring and process optimisation systems. ESG reporting requirements from export markets are reinforcing this investment driver.

Compliance Driver

🔬

Localisation of Automation Value Chains

India is actively encouraging domestic manufacturing of drives, sensors, robots, and automation components, with PLI incentives for electronics manufacturing and government investments in semiconductor fabrication. This creates both market demand and local manufacturing partnership opportunities for international automation companies.

Localisation Driver

SECTION 3

3 High-Demand Sectors for Industrial Automation in India

Industrial automation demand in India is not uniformly distributed, it is concentrated in specific verticals where government incentives, export competitiveness pressure, and productivity imperatives are converging simultaneously. Understanding which sectors are generating the highest automation investment demand enables international companies to prioritise their sales, distribution, and partnership strategies accordingly.

🚗Largest Segment

Automotive & EV Manufacturing

India’s automotive sector, the world’s third-largest by volume, is undergoing rapid EV transition, driving investment in battery assembly automation, robotic welding, precision machining, and quality inspection systems. OEMs and Tier 1–2 suppliers are all expanding automation depth.

Key demand: robotic welding, EV battery assembly, vision systems, AGVs

💊PLI Priority Sector

Pharmaceuticals & Medical Devices

India is the world’s largest generic drug manufacturer and a major exporter of medical devices. FDA and WHO-GMP compliance requirements are driving investment in process automation, packaging line automation, data integrity systems, and cleanroom monitoring.

Key demand: serialisation systems, process automation, cleanroom HVAC control, MES

📱PLI Priority Sector

Electronics & Semiconductor Manufacturing

PLI incentives for mobile phones, IT hardware, and semiconductors are attracting global electronics manufacturers, Apple suppliers, Samsung, Foxconn, all building automated facilities in India. Demand for SMT assembly, AOI systems, and cleanroom automation is growing rapidly.

India’s food processing sector is expanding rapidly, with export-oriented manufacturers demanding automation to meet international food safety standards (FSSC, BRC). Primary and secondary packaging automation, CIP systems, and process control are high-priority investment areas.

India’s chemicals sector, one of Asia’s largest, is investing in DCS/SCADA upgrades, safety instrumented systems (SIS), and process optimisation platforms as it modernises legacy plants to meet export market and ESG compliance requirements.

Key demand: DCS/SCADA, SIS, process analytics, energy management systems

🏗️Infrastructure Push

Steel, Cement & Heavy Industry

India’s massive infrastructure programme, roads, railways, ports, urban development, is driving capacity expansion and modernisation in steel and cement, with automation investment focused on energy efficiency, quality control, and predictive maintenance systems.

Key demand: predictive maintenance, energy monitoring, conveyor automation, quality analytics

🧵PLI Sector

Textiles & Apparel

PLI incentives for MMF (man-made fibre) and technical textiles are driving automation investment in yarn processing, fabric production, and cut-make-trim operations, particularly among export-oriented manufacturers competing with automated South Asian and Southeast Asian peers.

India’s 500GW renewable energy target by 2030 is creating demand for solar panel manufacturing automation, wind turbine component automation, grid management systems, and battery storage production lines, all requiring specialist automation technology.

Key demand: solar cell line automation, battery assembly, SCADA for grid management

SECTION 4

4 Key Industrial & Manufacturing Hubs Across India

India’s industrial geography is highly concentrated, the majority of manufacturing capacity, automation demand, and distribution infrastructure is clustered in specific industrial corridors and clusters. Understanding this geography is essential for positioning distributor networks, service centres, and sales operations.

🏙️ West India, 38.7% Regional Share

The dominant region for industrial automation investment. Maharashtra (Pune, Mumbai, Nashik, Aurangabad) and Gujarat (Ahmedabad, Surat, Vadodara, Rajkot) house the highest concentration of automotive, chemicals, pharmaceuticals, and engineering manufacturing.

Key clusters: Auto Valley Pune, GIFT City Gujarat, Dahej Chemical Zone, MIDC corridors

🌟 South India, 28.5% Highest Growth

Tamil Nadu (Chennai, Coimbatore, Hosur), Karnataka (Bengaluru, Hubli, Tumkur), and Telangana (Hyderabad) lead electronics, aerospace, semiconductor, and defence manufacturing investment, the highest-growth automation region.

Key clusters: Chennai Auto Corridor, Bengaluru Aerospace SEZ, ITIR Hyderabad

🏭 North India, Industrial Heartland

Haryana-Delhi-UP industrial corridor, Gurgaon, Faridabad, Noida, Lucknow, houses automotive, electronics assembly, and FMCG manufacturing. Rajasthan (Neemrana, Bhiwadi) is a rising Japanese and Korean manufacturing hub.

Key clusters: Manesar Auto Hub, Noida Electronics, Neemrana Japanese Zone, Yamuna Expressway Corridor

🌊 East India, 10.4% Untapped Opportunity

West Bengal (Kolkata), Odisha, and Jharkhand offer port-led manufacturing growth and metals sector modernisation, the largest untapped automation opportunity. Durgapur-Asansol industrial belt is expanding with steel and engineering manufacturing.

For most industrial automation companies entering India, a national distributor headquartered in Mumbai or Delhi with sub-distributors in Chennai, Bengaluru, Pune, and Ahmedabad provides the optimal coverage-to-cost ratio in the first 2–3 years. The automotive corridor (Pune–Chennai–Bengaluru) and the pharma belt (Hyderabad–Mumbai–Ahmedabad) are the two highest-priority coverage clusters for technology companies. See our guide to building a distributor network for the structural framework.

SECTION 5

5 Market Entry Models: Choosing the Right Approach

The right entry model for your manufacturing or industrial automation business depends on your product category, capital availability, long-term India strategy, and regulatory requirements. Here is the complete menu of entry models, with the trade-offs for industrial automation companies specifically.

Entry Model

How It Works

Capital Required

Time to Revenue

Best For

Key Reference

Indian Distributor / Channel Partner

Appoint a verified Indian company to stock, sell, and support your products in a defined territory

Very Low

3–9 months

Industrial automation hardware, instruments, sensors, control systems, standardised products with established applications

💡 Recommended Entry Sequence for Industrial Automation Companies

For most international industrial automation companies, particularly those entering India for the first time, the optimal sequence is: (1) Year 1–2: Appoint 1–2 verified national or regional distributors to validate market demand, build reference installations, and generate initial revenue with minimal capital exposure. (2) Year 2–3: Evaluate whether to establish a liaison office or India-incorporated entity based on validated revenue and strategic importance. (3) Year 3–5: If volume justifies, move to a wholly owned subsidiary or JV for greater market control, PLI eligibility, and local assembly capability. This staged approach manages risk while building the market knowledge required to make high-capital decisions correctly.

SECTION 6

6 Make in India & PLI Scheme: What Foreign Manufacturers Must Know

🏛️ Policy Overview

The Production Linked Incentive (PLI) scheme is India’s flagship manufacturing incentive programme, allocating over ₹1.97 lakh crore (~$24 billion) across 14 manufacturing sectors to incentivise both domestic and foreign manufacturers to establish or expand production in India. Foreign companies incorporated in India are fully eligible for PLI incentives provided they meet sector-specific investment thresholds and incremental sales targets. The scheme provides 4–6% incentives on incremental sales above a base year, paid over 5 years, functioning as a direct return on production investment that significantly improves the economics of establishing manufacturing in India.

PLI-Eligible Sectors Relevant to Manufacturing & Industrial Automation

PLI Sector

Allocated Budget

Relevance to Automation Companies

Incentive Rate

Electronics / Mobile Manufacturing

₹40,995 crore

High, electronics OEMs and EMS companies building PLI-eligible plants need automation solutions

4–6% on incremental sales

Pharmaceuticals & API

₹15,000 crore

High, pharmaceutical manufacturers expanding for PLI are major buyers of process automation and packaging line solutions

10% (bulk drugs), 5% (formulations)

Medical Devices

₹3,420 crore

Medium-High, expanding medical device manufacturing requires assembly automation and quality inspection systems

5% on incremental sales

Automotive & Auto Components

₹25,938 crore

Very High, EV transition investment is the largest single driver of new automation technology demand in India

13–18% (EV segment)

Telecom Networking Products

₹12,195 crore

Medium, telecom hardware manufacturing drives demand for PCB assembly automation and testing systems

6% on incremental sales

Food Processing

₹10,900 crore

Medium, food manufacturers expanding under PLI are investing in processing and packaging automation

10% (innovative food products)

Textile (MMF & Technical)

₹10,683 crore

Medium, textile PLI is driving spinning and weaving automation investment

15% on incremental sales (Year 1)

Advanced Chemistry Cell (Battery)

₹18,100 crore

High, battery Gigafactory construction will require significant cell assembly and formation automation

Up to ₹20/kWh incentive

Drones & Components

₹120 crore

Medium, drone manufacturing requires precision assembly automation and inspection systems

20% on value addition

🇮🇳 PLI Strategy for Automation Companies

Even if your automation company does not directly qualify for PLI incentives (most automation technology providers do not, as PLI is for goods manufacturers), the PLI scheme is your primary demand signal. Every company receiving PLI incentives for production expansion is a potential buyer of your automation, control, robotics, or monitoring solutions. Building your Indian sales and distribution strategy around PLI-active sectors, and identifying which specific companies in your target sectors have received PLI approval, provides a qualified prospect list that no generic market research can match.

SECTION 7

7 Regulatory & Compliance Requirements for Entry

India’s regulatory environment for foreign manufacturers and technology companies has improved significantly since 2014, but it retains complexity that requires careful navigation. Understanding the key regulatory requirements before committing to an entry model prevents the costly surprises that derail market entry timelines.

01

FDI Route & Business Entity Registration

Most manufacturing and industrial automation sectors in India allow 100% Foreign Direct Investment (FDI) under the Automatic Route, meaning no government approval is required, only post-fact reporting to the Reserve Bank of India (RBI). The preferred business structure for foreign-owned commercial operations is a Private Limited Company (Pvt Ltd), incorporated under the Companies Act 2013, requiring a minimum of two directors (one Indian resident), two shareholders, and a registered Indian address. Liaison offices (market research only) and branch offices (limited commercial activities) are also available but with significant operational restrictions. Defence, print media, and a small number of other sectors require government approval, verify your specific sector before assuming automatic route eligibility.

02

GST Registration & Indirect Tax Compliance

Goods and Services Tax (GST) applies to all commercial transactions in India above ₹20 lakh turnover (₹10 lakh in special category states). GST registration is mandatory before issuing invoices or importing goods for sale. Industrial automation products are typically classified at 12–18% GST depending on product category, confirm the correct HSN code and applicable rate for your specific products before pricing the Indian market. Input tax credits are available for GST paid on imports and purchases, which can significantly reduce the effective tax cost of establishing supply chain operations in India.

03

Import Licensing & Customs Tariffs

Most industrial automation products can be imported into India without specific import licences, but are subject to Basic Customs Duty (BCD), IGST, and in some cases Social Welfare Surcharge. Effective landed cost including all duties typically adds 18–32% to ex-works cost for industrial electronics and automation equipment, a significant factor in India pricing strategy. Some products, particularly those with defence dual-use potential, wireless transmission capability above certain frequencies, or items on India’s negative import list, require advance import licences or DGFT approvals. BIS (Bureau of Indian Standards) certification is mandatory for an expanding list of electronic and electrical products sold in India.

04

BIS Certification & Product Standards

The Bureau of Indian Standards (BIS) mandates certification for an increasing number of product categories sold in India, including many electronic, electrical, and industrial safety products. BIS certification requires product testing at a BIS-recognised laboratory, factory inspection (for BIS Licence scheme products), and ongoing compliance maintenance. Lead times for BIS certification range from 3–9 months. International automation companies entering India through a distributor route should confirm BIS requirements for their specific product range before finalising the market entry timeline, a missed BIS requirement discovered post-launch can halt sales entirely.

05

Intellectual Property Protection

India’s IP framework has improved significantly, the Indian Patent Office has reduced examination timelines, and trademark registration is now achievable within 12–18 months. However, effective IP protection in India requires proactive registration before market entry, not reactive filing after an infringement. File trademarks (class-appropriate), register designs for industrial products, and for software-embedded automation platforms, consider whether patent protection is commercially justified. Understand IP ownership in contract manufacturing agreements before engaging Indian EMS or OEM partners, and ensure your NDA agreements are governed by Indian law with enforceable jurisdiction clauses.

06

Data Localisation & Digital Personal Data Protection (DPDPA)

India’s Digital Personal Data Protection Act (DPDPA 2023) imposes obligations on entities processing personal data of Indian residents, including data collected through industrial IoT sensors in connected factories where operator personal data is involved. Cross-border data transfer restrictions are still being finalised in implementing rules, but companies deploying cloud-connected industrial automation in India should assess DPDPA compliance requirements as part of their product architecture and commercial terms. Encryption and access controls on all data exchange, as provided by GTsetu’s platform, satisfy the security baseline required under DPDPA and comparable frameworks.

SECTION 8

8 Finding a Verified Indian Distribution or Technology Partner

For the majority of international manufacturing and industrial automation companies entering India, finding the right Indian partner, a distributor, system integrator, technology licensor, or joint venture candidate, is the most consequential single decision in the market entry process. The wrong partner costs years and market credibility. The right one provides instant channel access, local application knowledge, service infrastructure, and customer relationships that would take a decade to build independently.

What to Look for in an Indian Industrial Automation Distributor or Partner

✅

Verified Business Identity

Company registration, GST registration, import licence, relevant industry certifications (ISO, BIS), and an authority letter from the person authorised to sign commercial agreements. This is the non-negotiable foundation, see business verification requirements.

🏭

Sector & Application Expertise

Does the partner have genuine application knowledge in your target industrial vertical, automotive, pharma, food processing, chemicals? A distributor selling across 20 unrelated product categories may lack the technical depth to position complex automation solutions effectively in competitive sales situations.

🗺️

Geographic Coverage & Service Infrastructure

Does their coverage match your target industrial hubs? Can they provide after-sales service and application support within acceptable response times across the territories they commit to covering? A distributor covering Mumbai but not Pune or Chennai is geographically incomplete for most automation companies.

🤝

Existing Customer Relationships

The highest-value asset a distributor brings is their existing customer relationships with procurement and engineering decision-makers at target accounts. Request a territory-specific account list (non-disclosure protected) and assess whether their existing customers overlap significantly with your target end-users.

⚡

Technical & Pre-Sales Capability

Industrial automation products typically require technical pre-sales support, application consulting, demo units, proof-of-concept projects, and commissioning support. Does the partner have engineers who can perform these functions credibly? Evaluate their technical team depth before committing.

📊

Financial Standing & Inventory Capacity

Can the partner fund the inventory required to maintain stock availability and provide demonstration equipment? Request financial references and assess their credit capacity relative to the working capital requirements of distributing your product range at target volumes. See our guide on partnership evaluation criteria.

🚫

Competitive Product Portfolio Check

Does the partner already distribute a directly competing product line? Many Indian distributors carry multiple competing brands to avoid overdependence on a single principal, assess whether their existing portfolio creates conflicts that compromise their commitment to your products.

🔐

Data Security & Confidentiality Practices

Industrial automation partnerships involve sharing technically sensitive information, product roadmaps, pricing strategies, key account data. Assess how the partner handles confidential information; require execution of a mutual NDA before any sensitive technical or commercial data exchange occurs. Use encrypted channels for all sensitive sharing, see B2B secure collaboration.

Channels for Finding Verified Indian Partners

💻

GTsetu Verified B2B Platform

GTsetu provides access to 500+ compliance-verified Indian manufacturers, distributors, and technology partners across all industrial sectors, with anonymous discovery, built-in NDA workflow, and encrypted collaboration. Zero broker commissions. The most efficient and secure channel for verified Indian partner discovery. Compare with alternatives to IndiaMart and alternatives to TradeIndia for open marketplace comparisons.

Best for Verified Discovery

🏛️

Bilateral Chambers of Commerce

Indo-German Chamber (IGCC), India-Japan Chamber (IJCCI), UK India Business Council (UKIBC), India-US Business Council (IUSBC), and similar bilateral chambers maintain verified member directories of Indian companies actively seeking international principal relationships. Strong for community-building and warm introductions.

Community Channel

🎪

India Trade Shows & Exhibitions

Automation Expo (Mumbai), IMTEX (Bengaluru), India Manufacturing Show, Chemtech, Pharmatech, and Packplus are the primary industry-specific trade events for meeting potential Indian partners face-to-face. See our guide on top B2B networking places for manufacturers and distributors.

In-Person Channel

🏢

CII, FICCI & Industry Associations

Confederation of Indian Industry (CII), Federation of Indian Chambers of Commerce (FICCI), and sector-specific bodies (ACMA for automotive, IDMA for pharma) provide member directories and networking events that surface qualified Indian industrial companies actively seeking international partnerships.

Association Channel

🌐

Invest India & Government Entry Support

India’s Invest India portal (Government of India) provides sector-specific market entry information, FDI facilitation, and introductions to state-level investment agencies. State governments, particularly Gujarat, Maharashtra, and Tamil Nadu, operate dedicated investor facilitation desks for priority sectors.

Government Channel

SECTION 9

9 Step-by-Step India Market Entry Roadmap

01

Market Prioritisation, Validate Before Committing

Before spending a rupee on India entry, validate the market opportunity for your specific product category. Which industrial verticals have the highest automation investment intensity? Which states are investing most heavily in your target sectors? What is the competitive landscape, which global automation brands already have established Indian distribution, and what are the gaps? A 4–6 week desk research and India visit programme, structured around conversations with potential Indian distributors and end-users, will reveal more than any market research report. Use GTsetu’s platform to identify and anonymously assess potential Indian partners before revealing your market entry plans.

02

Entry Model Selection, Match to Your Situation

Select your entry model based on validated market intelligence, not assumption. For most first-time India entrants in industrial automation, a verified national or regional distribution partnership is the right first step. Confirm whether PLI sector alignment creates a case for local manufacturing from day one. Assess BIS certification requirements early, they affect your go-to-market timeline regardless of entry model. Review the full trade-offs in our market entry partnerships guide before deciding.

03

Ideal Partner Profile Definition

Define precisely what you need in an Indian partner: geography coverage (national vs. regional; specific state clusters), sector specialisation (automotive / pharma / food / chemicals), existing customer base, technical capability (engineering staff for application support), inventory financing capacity, and complementary product portfolio. A specific ideal partner profile makes every discovery interaction productive. The more specific your brief, the faster GTsetu’s verified network surfaces relevant candidates.

04

Partner Discovery & Verification

Discover candidates through GTsetu’s verified platform, trade show attendance, bilateral chamber engagement, and referral from existing supply chain contacts. For every candidate, complete formal verification before engagement: company registration (MCA portal), GST registration, import licences, and any sector-specific certifications. GTsetu performs this verification for all companies on its platform, eliminating the due diligence burden from your discovery process. See business verification requirements for the complete checklist.

05

NDA Execution & Secure Technical Exchange

Execute a mutual NDA governed by Indian law before sharing any technical data, product specifications, pricing, application notes, or market strategy. All technical data exchange should occur through encrypted channels. On GTsetu, the NDA workflow is built in and activated before the encrypted workspace unlocks. For technical evaluation by a potential distributor, share product documentation in stages, public information first, then confidential technical specifications only after NDA is signed and trust has been established through initial meetings.

Execute the manufacturer-distributor contract with review by Indian legal counsel, not just your home country lawyer. Indian contract law has specific requirements for enforceability, particularly around non-compete provisions, non-circumvention clauses, and IP ownership. Address dispute resolution mechanisms explicitly, specify whether India-based arbitration (DIAC, Mumbai Centre for International Arbitration) or international arbitration (ICC, SIAC) applies, and whether Indian courts have exclusive jurisdiction. See also risk allocation in cross-border deals and force majeure provisions.

08

Market Launch & Partner Enablement

A successful India launch requires more than shipping the first container. Invest in: distributor technical training (product application, competitive positioning, troubleshooting); co-development of Indian-market commercial and technical collateral; joint visit programme to key target accounts in the first 90 days; first reference installation supported by your own technical resources; and a shared marketing activation plan covering India-specific trade publications, digital channels, and sector events. The first 6 months in any new India partnership are critical, under-invest in enablement and the relationship stalls before momentum builds.

SECTION 10

10 Key Commercial Terms for India Partnerships

India-specific commercial dynamics require adjustments to standard international distribution agreement terms. Here are the most important commercial considerations unique to the Indian market.

Commercial Term

India-Specific Consideration

Reference Guide

Pricing & Currency

India pricing is typically set in INR. USD-denominated supply prices with INR resale pricing exposes the distributor to currency risk, address this explicitly: who bears INR/USD fluctuation risk and through what mechanism (hedging, price adjustment bands, annual repricing windows)?

Custom duty rates on industrial goods change with every annual Union Budget. Specify in the agreement whether changes in Indian import duty rates trigger automatic price adjustment or require renegotiation, and the mechanism for each direction of duty change.

Indian distributors typically request 30–60 day credit terms. For a new relationship, start with advance payment or LC for the first 2–3 orders, then move to open account with defined credit limit once payment track record is established. Never extend Indian distributor credit beyond your risk appetite without credit insurance.

India is a large, heterogeneous market, consider structuring exclusivity by state cluster rather than nationally for first-time partnerships. National exclusivity granted before market validation creates a long-term problem if the partner underperforms in regions outside their core territory.

Indian customers expect local warranty service, not “return to manufacturer” warranties that require international shipping. Define clearly which warranty repair functions the Indian distributor performs, what the response time SLAs are, and how warranty costs are shared.

Annual minimum purchase commitments must be calibrated to Indian market reality, not your global distribution expectations. First-year minimums should reflect market development phase realities; ratchet clauses can increase commitments in years 2–3 as the market matures.

For partnerships involving Indian contract manufacturing, specify clearly who owns tooling, dies, and moulds manufactured in India, and what happens to them on termination. Indian courts are not uniformly supportive of foreign-owned tooling recovery claims without explicit contractual provisions.

Indian distribution agreements should specify notice periods (typically 3–6 months), post-termination inventory buyback obligations, and transition assistance requirements. Vague termination clauses in India create costly disputes, define every exit scenario explicitly.

Indian industrial procurement cycles are long, capital equipment decisions in process industries can take 12–24 months from initial specification to purchase order. Plan your India revenue projections and distributor performance expectations against realistic sales cycle timelines, not the shorter cycles of your home market.

💬

Price Sensitivity & Chinese Competition

Chinese automation brands, Delta, Hikvision, INVT, Inovance, compete aggressively on price in India at margins that European and American brands typically cannot match. Position on application support, service depth, PLI-related quality requirements, and total cost of ownership rather than on price. Many PLI recipients specifically require international-standard automation for export-oriented manufacturing, your quality positioning is commercially valid.

📋

BIS & Regulatory Certification Timelines

BIS certification delays of 6–9 months can stall market entry for electronics-intensive automation products. Begin BIS certification applications as early as possible in your India entry programme, ideally 12 months before target commercial launch, and budget for the testing and inspection costs involved.

🔁

Distributor Multitasking & Commitment

Many Indian industrial distributors carry 20–40 brands across multiple categories. Securing genuine mindshare and sales team commitment from a multi-brand distributor requires ongoing investment: joint account visits, technical training, co-funded marketing, and regular performance reviews. Absent this investment, your product line risks becoming a passive catalogue item.

💱

Currency Volatility

The INR/USD exchange rate has been broadly stable but can move 5–8% in either direction over a 12-month period, significantly affecting INR-priced distributor economics on USD-invoiced imports. Structure price review mechanisms in your distribution agreement to address this systematically rather than reactively.

🏙️

Geographic Heterogeneity

India is not one market, industrial demand profiles, buying behaviours, language preferences, and competitive dynamics vary significantly between Maharashtra, Tamil Nadu, Gujarat, and the North. A distribution network that covers Mumbai well but has no presence in the Chennai automotive corridor or the Ahmedabad pharma cluster is not a national India coverage. Design your partner network with deliberate geographic logic.

SECTION 12

12 How GTsetu Connects You with Verified Indian Partners

🇮🇳 GTsetu, Verified B2B Platform for India Market Entry

Discover Verified Indian Manufacturers & Distributors, No Broker Commission

GTsetu provides international manufacturing and industrial automation companies with direct access to compliance-verified Indian manufacturers, distributors, system integrators, and technology partners, across every industrial sector and all major manufacturing regions. Every company in GTsetu’s India network has been verified through business registration, GST documentation, import/export licences, industry certifications, and authority letter confirmation before appearing in the platform. You discover, qualify, and engage, without broker intermediaries taking a cut of your commercial economics.

🏛️

Multi-Layer Compliance Verification

Every Indian partner on GTsetu has been verified: company registration (MCA), GST, import licences, certifications, by GTsetu’s compliance team. Eliminates fraud risk and due diligence workload.

🕵️

Anonymous Discovery

Browse verified Indian partner profiles without revealing your identity. Protect your India market entry strategy until you choose to engage. Not possible via trade directories or open marketplaces.

📄

Built-In NDA Workflow

Digital mutual NDA with timestamped signatures activated before sensitive technical or commercial data can be exchanged. Governed by Indian or mutually agreed law.

🔐

Encrypted Document Workspace

AES-256 encryption at rest, TLS in transit. Role-based access controls. Full audit trail. Exchange product specs, pricing, and technical proposals securely, never through unprotected email.

🚫

Zero Broker Commission

GTsetu charges zero commission on any partnership formed between international manufacturers and Indian distributors or partners. All commercial economics stay between you and your partner.

🌏

100+ Countries Including India

GTsetu’s verified network covers all major Indian industrial regions and global markets, supporting your India entry today and expansion into China, the UAE, and Germany tomorrow. See all country expansion guides.

QWhy should I expand my manufacturing or industrial automation business to India?

India offers one of the most compelling market entry cases for manufacturing and industrial automation companies globally. The Indian industrial automation market is projected to grow from approximately $15–17 billion in 2025 to $28–40+ billion by 2031–2034 at 8–16% CAGR, driven by Make in India policy, PLI scheme investments across 14 sectors, Industry 4.0 adoption, rising labour costs in industrial centres, and a manufacturing PMI consistently above 55. India has the world’s largest young technical workforce, improving infrastructure, and a government more actively incentivising industrial investment than any comparable emerging market. For industrial automation companies, the combination of a massive installed base of legacy equipment due for modernisation, strong EV transition investment, and pharmaceutical and electronics export growth creates durable demand that is structural rather than cyclical.

QWhat are the best entry models for expanding a manufacturing or automation business to India?

For most first-time India entrants in industrial automation and manufacturing technology, the recommended entry sequence is: (1) Appoint a verified Indian national distributor or regional channel partners, lowest capital, fastest market access (3–9 months to first revenue). (2) After 2–3 years of validated market presence, evaluate establishing a wholly owned subsidiary (Private Limited Company) for greater market control and PLI eligibility. (3) If local production is commercially justified, pursue contract manufacturing via an Indian EMS/OEM partner or establish local assembly operations. Technology licensing to an Indian partner is appropriate where local production is strategically important but direct establishment is premature. Joint ventures are most suitable for sectors requiring local ownership advantages or for sharing the significant capital and risk of new manufacturing investment. See the full comparison in market entry partnerships.

QWhat is the PLI scheme and how does it benefit foreign manufacturers?

India’s Production Linked Incentive (PLI) scheme allocates over ₹1.97 lakh crore (~$24 billion) across 14 manufacturing sectors to incentivise domestic and foreign manufacturers to establish or expand production in India. Foreign companies incorporated as Indian entities are fully eligible. The scheme provides 4–6% incentives on incremental sales above a base year, paid over five years, functioning as a direct performance bonus on production growth. PLI recipients also typically receive state-level complementary incentives: land at industrial rates, power subsidies, and stamp duty exemptions. Even if your automation company does not directly qualify for PLI incentives (most technology providers don’t), the PLI scheme is your primary demand signal, every PLI-approved manufacturer expanding production is a qualified buyer of automation, control, and monitoring solutions.

QHow do I find a verified distributor for industrial automation products in India?

The most efficient and secure route to finding a verified Indian industrial automation distributor is through GTsetu’s compliance-verified B2B platform, where every Indian company has been verified through business registration (MCA), GST, import licences, and industry certifications before appearing in the network. You can browse verified Indian partner profiles anonymously, execute digital NDAs before sharing technical data, and engage through an encrypted workspace, with zero broker commissions on any partnership formed. Supplement with targeted trade show attendance (Automation Expo Mumbai, IMTEX Bengaluru), bilateral chamber engagement (IGCC, UKIBC), and CII/FICCI member introductions. Always verify candidates independently, or use a platform where pre-verification is already complete, before sharing product specifications or pricing. See our guide on how to find international distributors.

QWhat are the key regulations for manufacturing companies entering India?

Key regulatory requirements for manufacturing companies entering India: (1) Business entity registration, Private Limited Company (Pvt Ltd) for foreign-owned commercial operations under the Companies Act 2013. (2) FDI route, most manufacturing sectors allow 100% FDI under the Automatic Route; RBI post-fact reporting required. (3) GST registration, mandatory for commercial operations above ₹20 lakh turnover. (4) BIS certification, mandatory for an expanding list of electronic, electrical, and industrial safety products sold in India; allow 6–9 months for certification. (5) Import licences and customs duty, most industrial automation products can be imported without specific licences but are subject to BCD + IGST (effective landed cost typically +18–32%). (6) IP registration, trademark and patent registration before market entry, not after. (7) DPDPA compliance, for cloud-connected industrial IoT deployments collecting personal data. Engage Indian legal counsel for jurisdiction-specific advice before committing to an entry structure.

QWhich industrial sectors in India have the highest automation investment demand?

The sectors with the highest industrial automation investment demand in India in 2026 are: (1) Automotive and EV manufacturing, the largest automation demand segment, driven by EV transition investment in battery assembly, robotic welding, and precision machining. (2) Pharmaceuticals and medical devices, FDA/WHO-GMP compliance driving process automation, serialisation, and MES investment. (3) Electronics and semiconductor manufacturing, PLI-driven expansion of mobile phone, IT hardware, and semiconductor facilities creating demand for SMT assembly automation and cleanroom systems. (4) Food and beverage processing, export-oriented manufacturers automating for FSSC/BRC compliance. (5) Chemicals and petrochemicals, DCS/SCADA modernisation and SIS upgrades in large-scale process plants. (6) Battery and renewable energy manufacturing, new Gigafactory investments requiring cell assembly and formation automation. South India (Tamil Nadu, Karnataka, Telangana) is the highest-growth region at 28.5% share; West India (Maharashtra, Gujarat) holds the largest existing installed base at 38.7%.

QWhat commercial terms should I negotiate carefully in an India distribution agreement?

India-specific commercial terms requiring careful negotiation: (1) Currency risk allocation, who bears INR/USD fluctuation risk and through what mechanism. (2) Import duty passthrough, mechanism for handling changes in Indian customs duty rates that affect landed cost. (3) Payment terms, start with advance payment or LC for first transactions; move to open account with defined credit limits after establishing payment track record. (4) Exclusivity structure, consider state-cluster exclusivity rather than national for first partnership; tie extended exclusivity to performance thresholds. (5) Warranty and after-sales service obligations, define which warranty functions the Indian distributor performs and response time SLAs. (6) Annual volume commitments calibrated to Indian market development phase, avoid over-aggressive first-year minimums. (7) IP ownership and tooling provisions for any manufacturing involvement. (8) Termination and exit conditions, specify buyback obligations, transition assistance requirements, and notice periods explicitly. See our complete guides on exclusivity clauses, termination clauses, and manufacturer-distributor contracts.

Ready to Expand Your Manufacturing Business to India?

Connect with verified Indian manufacturers, distributors, and technology partners on GTsetu, with compliance-backed verification, anonymous discovery, built-in NDA workflows, and zero broker commissions on every India market partnership you form.

They represents the product, and research team behind GTsetu, a global B2B collaboration platform built to help companies explore cross-border partnerships with clarity and trust. The team focuses on simplifying early-stage international business discovery by combining structured company profiles, verification-led access, and controlled collaboration workflows.

With a strong emphasis on trust, and disciplined engagement, Team GTsetu shares insights on global trade, partnerships, and cross-border collaboration, helping businesses make informed decisions before entering deeper commercial discussions.