How to Expand Your Manufacturing & Industrial Automation Business to Poland

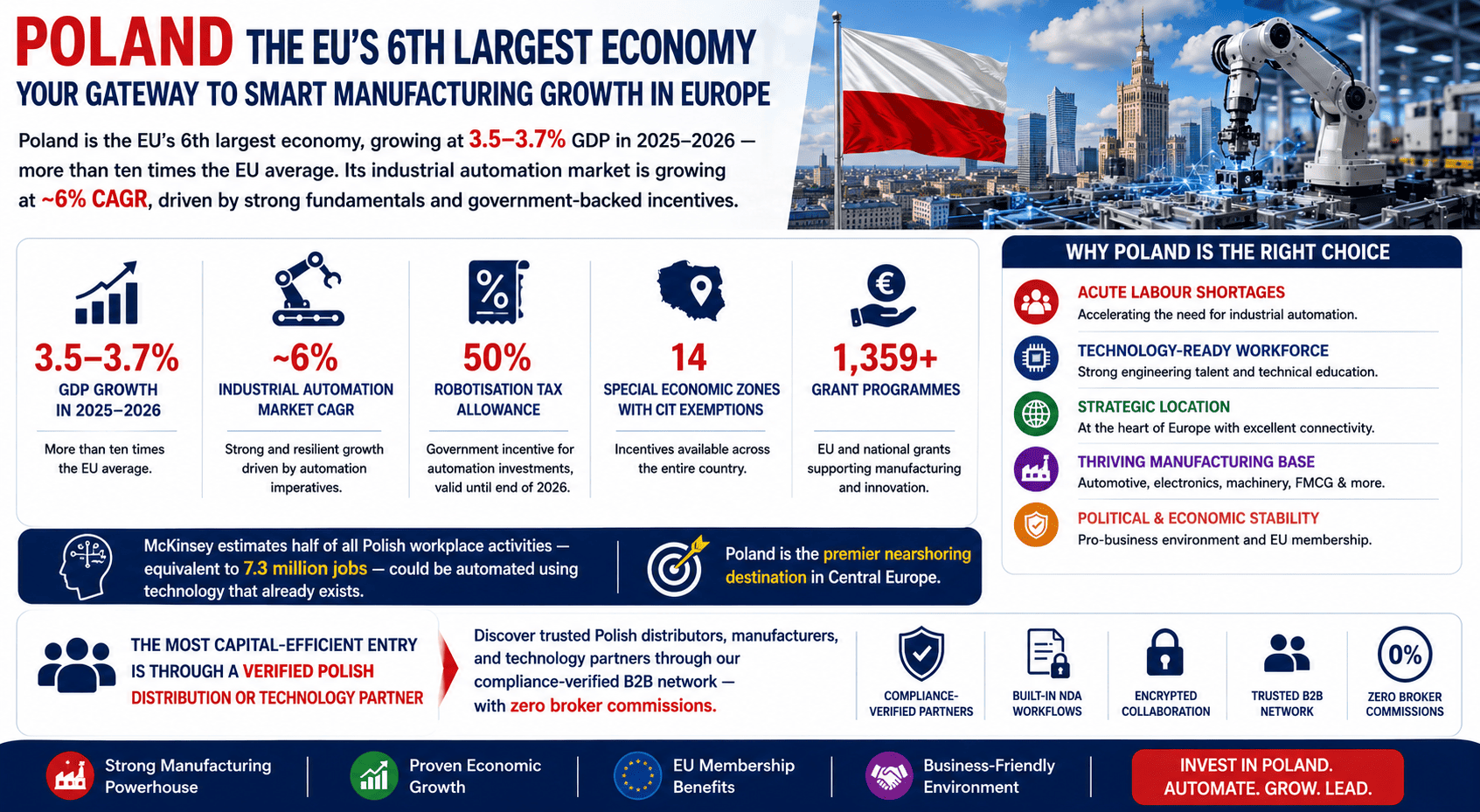

Direct Answer: Poland is the EU’s 6th largest economy, growing at 3.5–3.7% GDP in 2025–2026, more than ten times the EU average. Its industrial automation market is growing at ~6% CAGR, driven by acute labour shortages, a government 50% robotisation tax allowance (valid until end of 2026), 14 Special Economic Zones with CIT exemptions covering the entire country, and over 1,359 EU and national grant programmes for manufacturing businesses. McKinsey estimates half of all Polish workplace activities, equivalent to 7.3 million jobs, could be automated using technology that already exists. For international manufacturers and automation companies, Poland is the premier nearshoring destination in Central Europe, and the most capital-efficient entry is through a verified Polish distribution or technology partner, discoverable through GTsetu‘s compliance-verified B2B network with zero broker commissions.

📅 June 2, 2026⏱ 22 min read✍️ GT Setu Editorial Team🔄 Updated regularly

6th

Largest Economy in the EU

~6%

Industrial Automation CAGR 2025–2032

14

Special Economic Zones (SEZ / PIZ)

0%

GTsetu Broker Commission

Poland has undergone one of the most remarkable economic transformations in modern European history. In three decades, it has grown from a centrally planned economy to the EU’s 6th largest, with GDP expanding at 3.5–3.7% in 2025–2026, more than ten times the EU average of 0.3%. Manufacturing contributes 20–25% of national GDP and employs approximately 2.8 million people across automotive, food processing, aerospace, electronics, machinery, chemicals, and pharmaceuticals sectors that are deeply integrated into European and global supply chains.

For international manufacturers and industrial automation companies, Poland in 2026 represents a confluence of structural demand drivers that rarely appear simultaneously: acute labour shortages and rising wages creating the economic case for automation; a government-backed 50% robotisation tax allowance accelerating adoption; 14 Special Economic Zones covering the entire national territory with CIT exemptions; over 1,359 EU and national grant programmes specifically targeting manufacturing modernisation; and a McKinsey-quantified automation potential of 7.3 million jobs, half of all Polish workplace activities. This guide covers the complete picture, from market sizing and sector-by-sector opportunity, to incentive frameworks, regulatory navigation, partner discovery, and the commercial terms that govern successful Poland market entry. Explore our guides on the advantages and disadvantages of global expansion and international business development consulting for broader strategic context.

🇵🇱 Who Is This Guide For?

This guide is written for international manufacturers, industrial automation OEMs, robotics and control system providers, technology integrators, and industrial equipment companies seeking to enter or expand in the Polish market, whether through a distributor partnership, technology licensing, contract manufacturing, joint venture, SEZ-based production, or direct subsidiary establishment. It is also relevant for companies currently selling into Poland via informal channels who want to formalise their market presence. If you are exploring other European markets alongside Poland, see our country guides for Germany, Romania, United Kingdom, and Egypt.

SECTION 1

1 Why Poland for Manufacturing & Industrial Automation?

🎯 The Strategic Case

Poland is Central Europe’s dominant manufacturing and nearshoring hub, fully integrated into EU single market supply chains, home to 2.8 million manufacturing workers, and experiencing a structural automation inflection point driven by rising wages, acute labour shortages, demographic decline, and government incentives specifically designed to accelerate industrial robot adoption. For international automation companies, Poland offers a rare combination: a large, modernising industrial base actively seeking technology; EU-level regulatory alignment that removes product compliance barriers; and a government incentive framework, robotisation allowance, SEZ tax exemptions, and €76B+ in EU cohesion funds, that materially improves the economics of every automation purchase for every Polish manufacturer.

3.7%

Poland GDP growth (Q3 2025) vs. EU average of 0.3%, the strongest performance in three years

50%

Robotisation tax allowance, 50% deduction of qualifying robot investment costs from tax base; valid until end of 2026

7.3M

Jobs automatable by 2030 using existing technology, half of all Polish workplace activities (McKinsey report)

🇪🇺

EU Single Market Access

Poland’s EU membership provides full single market access, CE marking accepted across 27 countries, tariff-free exports to all EU member states, and EU regulatory alignment that removes the compliance burden that non-EU markets impose on industrial product companies.

📈

Fastest-Growing EU Economy

Poland’s GDP growth of 3.5–3.7% in 2025–2026 is dramatically outpacing the EU average. The 20th largest economy globally and 6th in Europe, Poland is still growing, unlike the stagnating Western European economies many automation companies are already saturating.

👷

Acute Labour Shortage Driving Automation

Poland’s minimum wage rose by more than 50% in five years (€489 in 2019 to €782 in 2023 and beyond). Demographic decline will shrink the working-age population by one-third by 2070. Universal Robots data shows industrial robot installations jumped 56% in 2021 alone as manufacturers responded to structural labour scarcity.

🤖

Government Robotisation Incentive

Poland’s robotisation tax allowance, 50% deduction of qualifying robot investment costs from tax base, covering hardware, related machinery, implementation, and training, directly reduces the net cost of automation for every Polish manufacturer. Valid until end of 2026, it is the most direct government push for industrial automation adoption in any EU market.

🏭

Deep Nearshoring Hub for Western Europe

Poland is the premier nearshoring destination for German, Dutch, French, and UK manufacturers, with more than 100 German companies having established production facilities in Poland. Mercedes-Benz is constructing a $1.45 billion EV cargo vehicle factory, and LG Energy Solution operates one of the world’s largest EV battery plants in southern Poland.

💰

EU Cohesion Funds, Largest EU Recipient

Poland has been the EU’s largest cohesion fund recipient since 2007, with over €76B in EU funds allocated for the 2021–2027 programming period. These funds support manufacturing modernisation, Industry 4.0 adoption, R&D infrastructure, and green manufacturing, creating government-backed demand for automation solutions across Polish SMEs and large enterprises alike.

Poland’s industrial automation market is experiencing a structural inflection, the combination of acute labour shortages, wage inflation, demographic pressures, government robotisation incentives, and deep integration into EU automotive and electronics supply chains is creating multi-year demand expansion that is structural rather than cyclical. Multiple research firms track the Polish automation market, with consistent signals of sustained 5–6% CAGR growth through 2032.

Research Source

Base Year Value

Forecast Horizon

Projected Value

CAGR

Data Bridge Market Research

USD 477.50 million (2024)

2032

USD 730.90 million

5.98%

Universal Robots / IFR Data

56% rise in robot installations (2021); 13% correction (2022)

2030

Half of all Polish workplace activities automatable by 2030

McKinsey: structural automation potential for 7.3M jobs

GrantBite / EU Grants Database

1,359+ active grant programmes for manufacturing businesses in Poland

Ongoing

EU cohesion funds €76B+ (2021–2027); 5B TRY-equivalent national grants for automation

Sustained public-sector demand stimulus

U.S. Trade.gov (ITA Poland)

Industry 4.0 adoption growing fastest in automotive and aviation

2028

Mercedes-Benz $1.45B EV factory; LG Energy Solution gigaplant; 213,000+ automotive workers

Strong demand pull from OEM investment wave

Grand View Research (Europe IPA)

Europe Industrial Process Automation: USD 23.87 billion (2024)

2030

USD 31.22 billion

4.57% (Europe total); Poland growing above regional average

Poland’s automation market sits at the intersection of two powerful forces: demand pull from manufacturers facing structural labour constraints, and supply push from government incentives reducing the net cost of every automation investment. This combination produces a market dynamic that is more durable than pure market-rate demand, and more accessible than markets without government subsidy support.

Key Market Drivers for International Automation Companies

👷

Structural Labour Shortage & Demographic Decline

Poland’s unemployment rate stands at just 3.2% (Eurostat), functionally full employment, while the population is projected to decline 20% by 2070 and the working-age population to shrink by one-third. This structural labour constraint is not solvable through immigration alone; automation is the only durable solution, creating a decades-long demand expansion that no cyclical downturn can fully reverse.

Structural Driver

💰

Rapid Minimum Wage Inflation Compressing Labour Advantage

Poland’s minimum wage rose more than 50% in five years, from €489 per month in 2019 to over €782 in 2023 and continuing upward, dramatically improving the ROI economics of automation versus manual labour for every Polish manufacturer. The payback period on cobot and robot investments has compressed to under 2 years for many Polish food, metal, and automotive applications.

Economic Driver

🏛️

Government Robotisation Allowance (50% Tax Deduction)

Poland’s robotisation tax allowance allows manufacturers to deduct 50% of qualifying robot investment costs, covering new industrial robots, related machinery, implementation costs, and employee training, from their tax base. Valid until end of 2026, this government incentive directly subsidises every automation sale to a Polish manufacturer. Companies selling automation equipment should ensure Polish customers are aware of and using this allowance in their investment business cases.

Policy Driver

🚗

EV Manufacturing Investment Wave

Poland is becoming a major European EV manufacturing hub, with LG Energy Solution operating one of the world’s largest EV battery plants in Wrocław, Mercedes-Benz building a $1.45 billion EV cargo vehicle factory, and established OEMs (Stellantis, Volkswagen) expanding Polish capacity. Each new EV facility requires significantly more automation than an equivalent ICE production line, creating concentrated, high-value automation demand.

Sector Driver

🛡️

NATO Defence Spending & Aerospace Investment

Poland leads NATO in defence spending relative to GDP, projected at 4.8% of GDP in 2025, creating significant demand for defence manufacturing automation in the Aviation Valley and Silesian Aviation Cluster (170+ aerospace companies, 35,000+ employees, including Sikorsky, Pratt & Whitney, and Airbus). Industry 4.0 adoption in aviation and defence is identified by the U.S. ITA as Poland’s highest-priority automation growth sector.

Defence Driver

🇪🇺

EU Cohesion Funds & 1,359+ Grant Programmes

Poland’s position as the EU’s largest cohesion fund recipient since 2007 creates an extraordinary secondary demand stimulus, over 1,359 active grant programmes for manufacturing businesses covering automation, digitisation, energy efficiency, and Industry 4.0 implementation. Polish manufacturers accessing these grants become funded buyers of automation equipment, expanding the addressable market well beyond what pure market economics would support.

EU Stimulus Driver

SECTION 3

3 High-Demand Sectors for Industrial Automation in Poland

Industrial automation demand in Poland is concentrated in the sectors that constitute the backbone of Polish manufacturing. The handling operations dominate at 52% of all cobot applications in Poland, followed by welding at 17% of new installations (the fastest growing application due to the national welder shortage). Understanding sector-by-sector automation demand enables international companies to target their distribution, positioning, and partner selection precisely.

🚗Largest Segment

Automotive & EV Manufacturing

Automotive manufacturing is Poland’s premier industrial automation sector, employing 213,000+ workers at OEMs including Stellantis, Volkswagen, Toyota, and Fiat, plus an extensive Tier 1 and Tier 2 supplier base. EV transition investment from Mercedes-Benz ($1.45B factory) and the LG Energy Solution gigaplant is creating intense new demand for battery assembly automation, robotic welding, AGVs, and precision inspection systems.

Key demand: robotic welding, EV battery assembly, AGVs, vision quality inspection, MES

🍔Largest by Revenue

Food & Beverage Processing

Poland’s food sector is its largest industrial segment, generating PLN 344.1 billion across 4,478 companies with strong year-on-year growth. The sector faces acute labour shortages particularly in meat processing, dairy, and bakery operations, making it the highest-urgency automation investment area. Export-oriented food manufacturers also face growing EU food safety and traceability compliance requirements driving MES and packaging automation.

Poland’s Aviation Valley (Podkarpacie region) and Silesian Aviation Cluster together host 170+ aerospace companies including Sikorsky, Pratt & Whitney, Airbus, and GE Aviation, producing components found in nearly every commercial aircraft globally. With defence spending at 4.8% of GDP, Poland is Europe’s most active defence manufacturing investor. U.S. ITA identifies aviation and defence as the top Industry 4.0 priority sectors in Poland.

Poland is a major European electronics and appliance producer, with LG Electronics, Philips, Miele, and BSH (Bosch/Siemens) operating major manufacturing facilities. Electronics manufacturing employs significant numbers across PCB assembly, appliance final assembly, and consumer electronics production. Rising labour costs are driving rapid investment in SMT automation, vision-guided assembly, and end-of-line testing systems.

Key demand: SMT assembly, AOI, end-of-line testing, conveyor systems, SCADA for process monitoring

🔩Welder Shortage Driver

Metal Processing & Machinery

Metal fabrication, stamping, machining, and mechanical engineering constitute a large portion of Polish manufacturing, and face the sharpest labour gap: welders have been in shortage in all Polish regions since at least 2016. Welding automation accounts for 17% of all new cobot installations and is the fastest-growing automation application in Poland. Machine builders serving German and EU OEM customers also drive strong demand for servo drives, PLCs, and safety systems.

Key demand: welding cobots and robots, CNC automation, press tending, grinding, conveyor systems

💊Growing Sector

Pharmaceuticals & Medical Devices

Poland has a growing pharmaceuticals and medical devices manufacturing base, with 1,756 pharma companies operating and EU GMP and FDA compliance requirements driving investment in process automation, serialisation systems, cleanroom monitoring, and packaging line automation. Poland ranks 4th in Europe for labour cost competitiveness, making it an increasingly attractive pharma manufacturing location for EU-market-serving producers.

Key demand: serialisation, cleanroom automation, process control, packaging, MES for GMP compliance

🧴Large Base

Chemicals, Plastics & Rubber

Poland has a well-developed chemicals and plastics industry serving automotive, electronics, and construction sectors. The rubber and plastic products sector is one of the most robotised in Poland, high-volume, repetitive production processes and tight dimensional tolerances make it a natural automation candidate. Injection moulding automation, quality inspection, and materials handling are high-priority investment areas.

Poland is one of Europe’s largest furniture exporters, with companies like IKEA sourcing significantly from Polish suppliers. The sector is experiencing rapid automation investment driven by export quality requirements, labour cost pressure, and the need for consistent product quality at scale. CNC routing automation, finishing line robotics, and packaging automation are the key demand areas in this underserved niche for many automation suppliers.

4 Key Industrial & Manufacturing Hubs Across Poland

Poland’s industrial geography is distributed across five major clusters, each with distinct sectoral specialisations and SEZ infrastructure. Understanding this geography is essential for designing distributor networks, service coverage, and sales operation positioning.

🏙️ Mazovia (Warsaw), Business & Advanced Tech

Warsaw and the Mazovia voivodeship host Poland’s largest concentration of multinational headquarters, shared service centres, and advanced manufacturing R&D operations. Strong in electronics, ICT, chemicals, and food processing. The Warsaw SEZ sub-zone provides incentives for high-tech manufacturing investment.

Key clusters: Masovian Technology Park, Warsaw Industrial Park, Płock Petrochemical Complex

⚙️ Silesia (Katowice), Automotive & Heavy Industry

Silesia is Poland’s traditional industrial heartland, now transformed into a major automotive and advanced manufacturing hub. Home to major Stellantis, Fiat, and Opel operations, plus the Silesian Aviation Cluster and an extensive automotive supply chain. The Katowice SEZ is Poland’s most established and largest by area.

Key clusters: Katowice SEZ, Silesian Science and Technology Centre, Gliwice Auto Zone

🔬 Lower Silesia (Wrocław), Electronics & EV Batteries

Wrocław and Lower Silesia host LG Energy Solution’s gigaplant, LG Electronics, Volvo, and major electronics manufacturers, making it Poland’s fastest-growing automation demand cluster. The WSSE (Wrocław SEZ) and Wałbrzych Special Economic Zone provide investment incentives across the region.

Key clusters: LG Energy Wrocław, Wałbrzych SEZ, Wrocław Technology Park, Legnica Copper Belt

✈️ Podkarpacie, Aviation Valley

The Aviation Valley cluster in south-eastern Poland (Rzeszów, Mielec, Stalowa Wola) is Poland’s premier aerospace and defence manufacturing zone, 170+ companies including Sikorsky, Pratt & Whitney, and Airbus, generating 90% of Poland’s aerospace output. The Euro-Park Mielec (Poland’s first SEZ, established 1995) and Rzeszów industrial parks anchor the zone.

Key clusters: Aviation Valley, Euro-Park Mielec SEZ, Rzeszów Industrial Park, WSK Rzeszów

🍔 Greater Poland & Kujawy, Agri-Food Processing

Poznań, Bydgoszcz, and the surrounding Greater Poland and Kujawy-Pomerania regions are Poland’s agri-food processing heartland, home to major food manufacturers, dairy processors, and meat processing operations. The Poznań Fair (Międzynarodowe Targi Poznańskie) hosts Poland’s major industrial trade events including ITM Poland and TAROPAK.

For most industrial automation companies entering Poland, a national distributor headquartered in Warsaw with regional engineers or sub-distributors in Katowice (automotive and heavy industry), Wrocław (electronics and EV), and Rzeszów (aerospace and defence) provides the optimal coverage for the first 2–3 years. The automotive corridor (Silesia) and the food processing belt (Greater Poland) represent the two highest-volume automation demand clusters for most product categories. See our guide to building a distributor network and our guide on international wholesale distributors for the qualification framework.

SECTION 5

5 Market Entry Models: Choosing the Right Approach

The right entry model for your manufacturing or industrial automation business in Poland depends on your product category, capital availability, long-term Poland and EU strategy, and whether your primary objective is serving the Polish domestic market, using Poland as a Central European hub, or establishing EU production capacity. Poland’s EU membership means that entry models optimised for Poland also optimise for EU market access.

Entry Model

How It Works

Capital Required

Time to Revenue

Best For

Key Reference

Polish Distributor / Channel Partner

Appoint a verified Polish company to stock, sell, and support your products in a defined territory

Very Low

3–9 months

Industrial automation hardware, sensors, PLCs, drives, cobots, standardised products with established Polish industry applications

Form a jointly owned Polish company with an established Polish manufacturer or integrator, shared equity, governance, and P&L

Moderate (shared)

12–24 months (setup)

Complex technology integration requiring local engineering depth; access to Polish partner’s existing customer relationships; shared capital risk for SEZ manufacturing

Establish manufacturing operations within a Special Economic Zone or Polish Investment Zone, accessing CIT exemptions, real estate tax exemption, and prepared industrial land

High

18–36 months (site + build + ramp)

Large-scale EU production for multiple market supply; companies qualifying for CIT exemption over 12–15 years; European supply chain anchor strategy

💡 Recommended Entry Sequence for Industrial Automation Companies

For most international industrial automation companies entering Poland for the first time, the optimal sequence is: Year 1–2: Appoint 1–2 verified national distributors with sector-specific expertise (automotive/Silesia first for hardware-intensive products; national coverage for standard catalogue items). Year 2–3: Evaluate establishing a Polish Sp. z o.o. for direct market presence, EU Central European hub operations, or access to Polish Investment Zone CIT exemptions. Year 3+: If production volume justifies, assess SEZ-based assembly or manufacturing for EU market supply. Always ensure your Polish distributor is actively helping customers access the 50% robotisation tax allowance, it is the most powerful sales enabler in the Polish automation market and many smaller manufacturers are not aware of or fully utilising it.

SECTION 6

6 SEZ, Polish Investment Zone & EU Grants: What Foreign Manufacturers Must Know

🏛️ Incentive Framework Overview

Poland’s investment incentive framework operates on three parallel tracks: the Polish Investment Zone (PIZ) / Special Economic Zone (SEZ) system providing CIT and real estate tax exemptions; government cash grants (MASP) for large strategic investments; and EU cohesion funds and Horizon Europe grants covering automation, digitisation, R&D, and green manufacturing. Foreign companies incorporated in Poland are fully eligible for all incentive programmes on equal terms with domestic investors. The combination of these three tracks creates a layered incentive structure that can materially improve the economics of manufacturing establishment and automation investment across Poland.

Poland’s Investment Incentive Framework: The Key Programmes

Incentive Programme

Key Benefits

Relevance to Automation Companies

Eligibility

Robotisation Tax Allowance

50% deduction of qualifying robot investment costs from tax base; covers industrial robots, related machinery and equipment, implementation costs, employee training costs

Very High, every automation sale to a Polish manufacturer is subsidised by 50% deduction; reduces effective customer acquisition cost and improves ROI for automation buyers; valid until end of 2026

All Polish taxpayers (CIT/PIT) investing in new industrial robots; no minimum investment threshold; available alongside other incentives

Polish Investment Zone (PIZ), CIT/PIT Exemption

Income tax (CIT or PIT) exemption for qualifying new investments, available across the entire territory of Poland on both public and private sites; exemption period 12–15 years depending on location history

High, for automation companies establishing Polish manufacturing or assembly operations; exemption amount tied to qualifying investment value and job creation; significantly improves economics of SEZ-based production vs. Western European alternatives

Investments meeting minimum expenditure thresholds (lower in less-developed regions); qualifying sectors (manufacturing, modern services, R&D); decision on support issued by SEZ manager

Special Economic Zones (14 SEZs)

CIT exemption (via PIZ); real estate tax (RETAX) exemption; prepared industrial land with roads, utilities, and infrastructure; scientific and research facility access; existing permits valid until end of 2026

Very High, OIZ-equivalent zones covering Poland’s major industrial clusters; ready-built infrastructure significantly reduces greenfield establishment costs; existing supplier and logistics ecosystems within zones

Investment within SEZ boundaries; qualifying activities (manufacturing, high-tech services, R&D, renewable energy); minimum investment threshold varies by SEZ and unemployment rate in the area

Government Cash Grants (MASP, Minister of Economy)

Direct cash grants from the Minister responsible for the economy; grant agreement concluded directly between Minister and investor; maximum grant amount up to 20% higher for eastern Poland voivodeships (Lubelskie, Podkarpackie, Podlaskie, Świętokrzyskie, Warmińsko-Mazurskie)

Medium-High, for large strategic automation-related investments; grants available for qualifying manufacturing investments meeting employment and investment thresholds; not available on standard rolling basis, assessed case-by-case

Large-scale investments meeting strategic significance thresholds; no standing calls for applications; assessed by Ministry of Economic Development

R&D Tax Relief

100% additional deduction of R&D expenditure from tax base (effectively 200% total); 150% for R&D centres; covers salaries, materials, equipment, external services, IP acquisition

Medium-High, for automation companies with Polish R&D or software development operations; especially relevant for IIoT, MES, and Industry 4.0 software platform companies with Polish engineering teams

Qualifying R&D activities under Polish tax law; R&D centre designation requires separate MEIT application; all Polish CIT/PIT taxpayers eligible for standard 100% relief

EU Cohesion Funds, 1,359+ Grant Programmes

Grants for manufacturing automation, Industry 4.0, energy efficiency, R&D, digitalisation, from €50K to €15M+ per project; national and regional programmes through Polish Agency for Enterprise Development (PARP) and regional Marshal Offices

Very High, grants effectively fund automation purchases by Polish manufacturers, making them qualified buyers; your Polish distributor working with grant-funded customers can significantly expand addressable market; your own R&D activities in Poland may qualify directly

Polish companies (or foreign companies with Polish subsidiaries) meeting programme criteria; 1,359+ programmes available; application windows vary by programme, monitor PARP and regional portals

Real Estate Tax Exemption (Municipal)

Exemption from local property and land taxes for qualifying investments in municipalities; available as local state aid; duration and amount set by individual municipality

Medium, for automation companies establishing Polish manufacturing facilities; reduces ongoing operating costs; combined with SEZ/PIZ income tax exemptions creates strong cost case for Poland vs. Western Europe

Qualifying investments in participating municipalities; coordinated with SEZ manager or local government investment office

🇵🇱 How the 50% Robotisation Allowance Changes Your Sales Strategy

The Polish robotisation tax allowance is the most powerful tool in your Polish automation sales strategy, and most international companies are not leveraging it effectively. Every Polish manufacturer that is a CIT/PIT taxpayer can deduct 50% of qualifying robot investment costs from their tax base. This means a PLN 500,000 robot installation has an effective net cost of PLN 250,000 after the tax benefit, a 50% immediate return on investment before the robot has produced a single part. Train your Polish distributor to lead with the robotisation allowance in every customer conversation, quantify the tax benefit in every proposal, and include it in ROI calculations alongside labour cost savings. This allowance has been one of the most powerful demand accelerators in any European automation market, use it explicitly.

SECTION 7

7 Regulatory & Compliance Requirements for Entry

Poland’s regulatory environment is fully aligned with EU standards, a major advantage for international companies that already meet EU compliance requirements. CE marking, GDPR, REACH, and all EU product safety directives apply in Poland exactly as they do across the EU27. This significantly reduces the additional compliance burden compared to non-EU emerging markets while providing access to the world’s largest single market.

01

Business Entity Registration, KRS (National Court Register)

The standard structure for foreign-owned commercial operations in Poland is the Spółka z ograniczoną odpowiedzialnością (Sp. z o.o.), limited liability company. Registration is with the National Court Register (Krajowy Rejestr Sądowy / KRS). Requirements: minimum share capital of PLN 5,000; at least one shareholder (individual or corporate); at least one director; registered Polish address. Online registration via the S24 portal is available for standard articles. A branch of a foreign company (Oddział) can be established for limited commercial activities without full subsidiary incorporation, appropriate for market assessment phases. Sole trader operations are available for EU citizens. Representative offices are not permitted to conduct commercial activities. Registration typically takes 3–7 business days online.

02

Tax Registration, CIT, VAT, and Withholding Tax

Polish corporate income tax (CIT) is set at 19% standard rate, with a reduced 9% rate for small taxpayers (annual revenue below €2 million equivalent). Extensive CIT reductions and exemptions are available under PIZ/SEZ investment decisions (see Section 6). VAT registration is required before commercial invoicing; the standard Polish VAT rate is 23%, with reduced rates of 8% and 5% for specific goods. EU VAT rules apply, Polish VAT is recoverable on inputs through the standard EU VAT credit mechanism. Withholding tax applies to cross-border dividends, interest, and royalties, rates reduced under Poland’s extensive double tax treaty network (80+ treaties). Mandatory Polish tax filing includes monthly/quarterly VAT returns and annual CIT declarations.

03

CE Marking & EU Product Compliance

Poland applies all EU product safety directives in full, CE marking is mandatory for industrial machinery (Machinery Directive 2006/42/EC), electrical equipment (Low Voltage Directive), electromagnetic compatibility (EMC Directive), pressure equipment (PED), and all other relevant EU product safety frameworks. For European manufacturers whose products are already CE marked, this creates no additional compliance burden. For non-European manufacturers, CE marking obtained for the EU market provides immediate access to Poland. RoHS 2 (restriction of hazardous substances in electrical and electronic equipment) and REACH (chemical substance registration) apply in Poland as EU member state obligations. There are no Poland-specific product certification requirements equivalent to India’s BIS or Turkey’s TSE for most industrial automation products.

04

GDPR & Data Protection

Poland applies the EU General Data Protection Regulation (GDPR) in full. For industrial automation companies deploying cloud-connected IIoT platforms, MES systems, or remote monitoring solutions that process personal data of Polish personnel, GDPR compliance obligations apply, including data processing agreements, privacy notices, and, where applicable, Data Protection Impact Assessments (DPIAs). The Polish data protection authority (UODO) enforces GDPR with fines up to 4% of global annual turnover for major violations. Polish-specific nuance: the Polish Labour Code has additional restrictions on employee monitoring beyond standard GDPR, obtain local legal advice on the interaction between GDPR and Polish labour law for any shop-floor monitoring or biometric system deployment.

05

Employment Law & ZUS (Social Insurance)

Polish Labour Code applies to all employees working in Poland under Polish employment contracts. Key requirements: written employment contracts (in Polish); minimum wage compliance (updated annually); social insurance (ZUS) registration and contributions, employer contributions total approximately 20–21% of gross salary on top of the employee salary cost; occupational health and safety (BHP) training mandatory for all employees; statutory notice periods of 2 weeks to 3 months depending on tenure. Poland ranks 4th in Europe for labour cost competitiveness, annual employee compensation averaging €34,405, well below Germany (€48,000+) and UK (€42,000+). For employers in SEZs, social security premium support may be available under the investment decision terms, reducing effective labour costs further.

06

Intellectual Property Protection

Poland is a signatory to all major international IP conventions (Paris Convention, PCT, TRIPS) and the European Patent Convention. EU trademark (EUTM) and EU design registrations registered via the EUIPO are automatically valid in Poland. Patent registration in Poland is via the Polish Patent Office (Urząd Patentowy RP) or the European Patent Office (EPO) for European Patents. Software copyright is protected automatically under Polish copyright law (aligned with EU Software Directive). Key considerations for automation companies: understand IP ownership in contract manufacturing agreements before engaging Polish OEM partners; specify tooling and mould ownership explicitly; and ensure NDA agreements are governed by Polish law with enforceable jurisdiction clauses (GDPR-compliant digital NDAs, as used on GTsetu’s platform, satisfy this requirement).

SECTION 8

8 Finding a Verified Polish Distribution or Technology Partner

For the majority of international manufacturing and industrial automation companies entering Poland, finding the right Polish partner, a distributor, system integrator, technology licensor, OEM partner, or joint venture candidate, is the most consequential single decision in the market entry process. The right Polish automation distributor brings sector-specific engineering expertise, established customer relationships with Polish OEMs and industrial manufacturers, local SEZ and grant programme knowledge that enables customers to fund automation purchases, and the technical service infrastructure required by Polish industrial buyers.

What to Look for in a Polish Industrial Automation Distributor or Partner

✅

Verified Business Identity

KRS (National Court Register) number, NIP (tax identification number), REGON (statistical number), import licence, relevant certifications (ISO 9001, industry-specific). Confirm the authorised signatory for commercial agreements. GTsetu pre-verifies all of this before any company appears in its network, see our business verification requirements guide.

🏭

Sector & Application Expertise

Does the partner have genuine application knowledge in your target sector, automotive (Silesia), food processing (Greater Poland), aerospace (Aviation Valley), electronics (Lower Silesia)? Handling operations and welding account for 69% of all Polish cobot applications, a distributor without welding automation expertise will miss Poland’s fastest-growing application segment.

💰

Grant Programme Expertise

Does the partner actively help customers access the 50% robotisation allowance, EU cohesion fund grants, and PARP digitalisation grants? A Polish distributor who can navigate the grant application process for their customers significantly accelerates the buying decision and differentiates their service offering from price-only competitors.

🗺️

Regional Coverage & Service Infrastructure

Does the partner have genuine presence in your target industrial regions, Silesia, Lower Silesia, Mazovia, Greater Poland, Podkarpacie? A Warsaw-headquartered distributor without regional service engineers may struggle to provide the application support and response times required by Silesian automotive Tier 1 suppliers.

⚡

Technical & Pre-Sales Engineering Depth

Polish industrial customers expect technical pre-sales application support, demo system capability, integration assistance, and post-commissioning training. For welding automation, robotics, and complex control systems, assess the partner’s technical team depth, how many application engineers, what certifications, what languages (Polish, German, English) can they support?

📊

Financial Standing & Inventory Capacity

Polish automation distributors must fund inventory for fast-moving products, maintain demonstration systems, and often bridge the timing gap between customer grant fund receipt and purchase order placement. Assess financial standing and credit capacity relative to the working capital requirements of distributing your product range. See our partnership evaluation criteria guide.

🇩🇪

German-Market Integration

Many Polish industrial companies are deeply integrated with German supply chains, their automation technology requirements often align with German OEM specifications. A Polish distributor with German-language capability, familiarity with German OEM approval processes, and relationships with German-owned Polish manufacturing facilities provides access to the most automation-intensive customer segment in Poland.

🔐

Data Security & NDA Practices

Industrial automation partnerships involve sharing technically sensitive information. Require execution of a mutual NDA governed by Polish law before any sensitive technical or commercial data exchange. All technical data exchange should occur through encrypted channels, see our guide to B2B secure collaboration. GTsetu’s built-in NDA workflow and encrypted workspace satisfy all GDPR requirements for cross-border data protection.

Channels for Finding Verified Polish Partners

💻

GTsetu Verified B2B Platform

GTsetu provides access to compliance-verified Polish manufacturers, distributors, and technology partners across all industrial sectors, with anonymous discovery, built-in NDA workflow, and encrypted collaboration. Zero broker commissions on every partnership formed. The most efficient and secure channel for verified Polish partner discovery. Compare with our guide to supplier collaboration platforms for alternatives assessment.

Best for Verified Discovery

🎪

Polish Industrial Trade Shows

AUTOMATICON (automation, Warsaw), ITM Poland (Poznań, industrial technology fair), TAROPAK (packaging, Poznań), PLASTPOL (plastics, Kielce), Metal Show & Forum, and the MSV Brno partner events are the primary venues for meeting qualified Polish industrial automation partners. See our guide on top B2B networking places.

In-Person Channel

🏛️

Bilateral Chambers of Commerce

Polish-German Chamber of Industry and Commerce (AHK Polen, the largest bilateral chamber in Poland), Polish-British Chamber of Commerce, AmCham Poland, and the French-Polish Chamber of Commerce provide member directories of Polish companies actively seeking international principal relationships. AHK Polen in particular surfaces German-supply-chain-integrated Polish manufacturers.

Community Channel

🏢

PAIH, Lewiatan & Industry Associations

The Polish Investment and Trade Agency (PAIH) maintains databases of Polish companies by sector and provides investor facilitation services. Lewiatan (Polish business confederation), PZPM (automotive industry association), and PSME (machine builders association) provide member directories and sector-specific networking events. The B2B business network guide covers association-based discovery in depth.

Association Channel

🌐

SEZ Managers & Polish Investment Zone Operators

The 14 Polish SEZ managers (including Katowice SEZ, Wałbrzych SEZ, Euro-Park Mielec, Poznań SEZ) maintain networks of investors operating within their zones and can facilitate introductions to qualified industrial companies within their ecosystem, including potential distributors, OEM partners, and technology integration firms actively seeking international automation principals.

Zone Channel

SECTION 9

9 Step-by-Step Poland Market Entry Roadmap

01

Market Prioritisation, Validate Before Committing

Before investing in Poland entry, validate the market opportunity for your specific product category. Which Polish industrial sectors have the highest automation investment urgency for your product type, welding (nationwide shortage), food processing (largest sector, acute labour gap), automotive (EV investment wave), or aerospace (Aviation Valley)? What is the competitive landscape, which global automation brands are already established in Polish distribution? Use GTsetu’s platform to anonymously assess potential Polish partners before revealing your market entry plans. Explore our guide on cross-border business partnerships for the validation framework.

02

Robotisation Allowance Strategy, Build Into Every Proposal

Before approaching your first Polish customer or partner, fully understand Poland’s 50% robotisation tax allowance. Build a standard ROI model that includes the tax benefit alongside labour cost savings. Train your Polish distributor candidates on this tool, the ability to clearly quantify the robotisation allowance benefit in customer proposals is a competitive differentiator that separates serious automation partners from catalogue sellers. This step should happen before you’ve chosen your distributor, because it is a selection criterion for the distributor itself. Review the pricing structures guide for how to present ROI in a market with government subsidy support.

03

Entry Model Selection & CE Certification Confirmation

Select your entry model based on validated market intelligence. Confirm CE marking status for all products you intend to sell in Poland, for EU-registered companies this is typically already in place; for non-EU companies, CE marking for a single EU market access applies to all 27. Assess whether the SEZ/PIZ incentive structure creates a case for local assembly from day one for large-volume products. Review the full entry model trade-offs in our market entry partnerships guide.

04

Ideal Partner Profile Definition

Define precisely what you need in a Polish partner: geographic focus (Silesia automotive, Greater Poland food, Aviation Valley aerospace, Lower Silesia electronics), sector expertise, grant programme navigation capability, technical engineering depth (application engineers, commissioning support), inventory financing capacity, and German-language capability where relevant. The more specific your ideal partner profile, the faster GTsetu’s verified network surfaces relevant candidates. See our guide on distributors and manufacturers relationships for the profile framework.

05

Partner Discovery & Verification

Discover candidates through GTsetu’s verified platform, AUTOMATICON trade show attendance, AHK Polen chamber engagement, and PAIH facilitation. For every candidate, complete formal verification: KRS number, NIP, import licence, ISO certifications. GTsetu pre-verifies all companies in its network, eliminating this burden. See our business verification requirements checklist for independent verification steps.

06

NDA Execution & Secure Technical Exchange

Execute a mutual NDA governed by Polish law before sharing any technical data. Ensure your NDA is GDPR-compliant for EU data protection requirements. All technical data exchange should occur through encrypted channels. GTsetu’s platform enforces NDA execution before the encrypted workspace unlocks, satisfying both contractual protection and GDPR cross-border transfer requirements. Include explicit non-circumvention provisions in your NDA where relevant.

Execute the manufacturer-distributor contract with review by Polish legal counsel. Polish contract law (Civil Code) has specific requirements for enforceability of non-compete provisions (maximum 3 years, proportionate geographic scope), exclusivity clauses, and IP assignment. Address dispute resolution explicitly, specify Polish arbitration (SA in Warsaw) or international arbitration (ICC, VIAC) and whether Polish court jurisdiction applies as fallback. Include force majeure provisions and risk allocation mechanisms.

SECTION 10

10 Key Commercial Terms for Poland Partnerships

Commercial Term

Poland-Specific Consideration

Reference Guide

Pricing Currency

Poland uses the PLN (Polish złoty), not the euro. EUR-denominated supply pricing with PLN resale pricing exposes the Polish distributor to currency risk, particularly for project-based sales with long quotation-to-order cycles. Options: EUR-denominated pricing for large projects (accepted by Polish OEM customers for capital equipment), PLN pricing with annual EUR/PLN review windows, or automatic adjustment bands for moves beyond ±5% from a reference rate.

Polish customers accessing EU cohesion grants or national automation grants may experience delays of 3–9 months between project approval and fund disbursement. Structure distributor payment terms to accommodate grant-funded customer purchase cycles, where possible, consider payment milestones that align with grant disbursement timing rather than standard net-30 terms that may be commercially unrealistic for grant-funded buyers.

Your distributor’s customers benefit from the 50% robotisation allowance on the full purchase price. Ensure the invoicing and documentation for robot-related purchases clearly identifies qualifying components (robot, related machinery, implementation services) to facilitate customer tax deduction claims. Some international principals provide supplementary documentation packages for Polish distributor use specifically for robotisation allowance claims, this is a commercial differentiator worth investing in.

Poland is a large country with distinct regional market dynamics. Consider structuring exclusivity by region (Silesia automotive vs. Greater Poland food vs. Podkarpacie aerospace) or sector rather than nationally for first-time partnerships. National exclusivity should be earned through year 1–2 performance rather than granted upfront. See our exclusivity clauses guide.

Polish automotive Tier 1 suppliers (serving German OEM JIT chains) have very short delivery requirements. Polish food processing companies during peak season (harvest) have emergency purchasing needs. Define maximum acceptable lead times, minimum stock requirements for fast-moving products, and emergency delivery protocols in the distribution agreement. Short lead times are a key competitive differentiator vs. Asian brands in the Polish market.

Polish industrial customers, particularly SMEs outside Warsaw, strongly prefer Polish-language product documentation, operating manuals, safety data sheets, and technical support. Stipulate in the distribution agreement that the Polish distributor is responsible for providing Polish-language translation of key documentation; clarify who funds this (usually shared) and who approves final translations for technical accuracy.

First-year volume commitments in Poland should reflect the 6–12 month market development phase before ratcheting in years 2–3. For automation hardware, the grant funding cycle creates lumpy purchase patterns, avoid annual commitments that penalise distributors for grant-timing delays outside their control. Denominate in units or EUR value rather than PLN to avoid inflation-related commitment distortion. See our volume commitments guide.

Polish distribution agreements should specify notice periods (3–6 months), post-termination inventory buyback at distributor cost plus agreed margin, non-competition restrictions (maximum 2 years, proportionate territory and activity scope under Polish Civil Code), customer transition assistance, and treatment of pending grant-funded orders at the point of termination. See our termination clauses guide.

EU and national grant programmes in Poland have complex application requirements, long processing timelines (3–9 months), and competitive allocation processes. Polish SMEs often lack the internal capacity to navigate applications alone. Your Polish distributor’s ability to support customers through grant applications, or to partner with specialist grant consultants, can be a decisive sales enabler. Build grant navigation capability into your distributor selection criteria.

💱

PLN/EUR Currency Volatility

The PLN/EUR exchange rate can move 5–10% over 12-month periods, affecting distributor economics on EUR-priced imports. Structure price review mechanisms, EUR project pricing for large capital equipment, and automatic adjustment clauses into your distribution agreement from the start. Poland is not a high-inflation environment like some emerging markets, but currency management still requires explicit commercial structure.

🤝

German-Brand Preference Among Polish OEM Customers

Polish automotive and aerospace suppliers serving German OEM customers often have strong preferences for German-brand automation equipment due to OEM specification requirements, German-speaking service support, and established supply chain familiarity. Position against German incumbents (Siemens, Festo, KUKA) on total cost of ownership, application engineering support, and robotisation allowance ROI, and ensure your Polish distributor understands your differentiation versus German competitors explicitly.

📚

Polish-Language Documentation Gap

Polish industrial SMEs, particularly in food processing and metal fabrication outside major cities, operate primarily in Polish. Missing Polish-language operating manuals, safety data sheets, and technical support create real barriers to sale and post-sale satisfaction. Budget for Polish translation of key technical documentation as part of your market entry investment rather than treating it as the distributor’s sole responsibility.

🏭

Distributor Multi-Brand Portfolio Fragmentation

Many Polish industrial automation distributors carry 15–30 brands across multiple categories. Securing genuine mindshare and application engineering commitment from a multi-brand distributor requires ongoing investment: joint customer visits, technical training, co-funded demo equipment, and regular performance reviews. Absent this investment, your product line risks becoming a passive catalogue entry behind more actively managed competitor brands.

🔄

Post-2026 Incentive Landscape Uncertainty

Poland’s robotisation tax allowance and existing SEZ permits are both scheduled to transition at the end of 2026, the PIZ system fully replaces old SEZ permit structures, and the robotisation allowance’s extension beyond 2026 is subject to legislative renewal. Monitor the legislative calendar and plan your Polish distributor’s customer pipeline to maximise purchases under the current robotisation allowance before any change in programme terms.

SECTION 12

12 How GTsetu Connects You with Verified Polish Partners

🇵🇱 GTsetu, Verified B2B Platform for Poland Market Entry

Discover Verified Polish Manufacturers & Distributors, No Broker Commission

GTsetu provides international manufacturing and industrial automation companies with direct access to compliance-verified Polish manufacturers, distributors, system integrators, and technology partners, across every industrial sector and all major manufacturing regions. Every company in GTsetu’s Poland network has been verified through KRS registration, NIP tax ID, import licences, industry certifications, and authority letter confirmation before appearing in the platform. You discover, qualify, and engage, without broker intermediaries taking a cut of your commercial economics. Explore how GTsetu compares with open marketplaces via our guides on alternatives to Alibaba and global collaboration examples.

🏛️

Multi-Layer Compliance Verification

Every Polish partner on GTsetu has been verified: KRS, NIP, REGON, import licences, ISO certifications, by GTsetu’s compliance team before they appear in the network.

🕵️

Anonymous Discovery

Browse verified Polish partner profiles without revealing your identity. Protect your Poland market entry strategy until you choose to engage.

📄

GDPR-Compliant NDA Workflow

Digital mutual NDA with timestamped signatures activated before sensitive data exchange. Governed by Polish law. GDPR-compliant for EU cross-border data transfers.

🔐

Encrypted Document Workspace

AES-256 encryption at rest, TLS in transit. Role-based access controls. Full audit trail. Exchange product specs, pricing, and technical proposals securely.

🚫

Zero Broker Commission

GTsetu charges zero commission on any partnership formed. All commercial economics stay between you and your Polish partner.

🌏

100+ Countries Including Poland

GTsetu covers all major Polish industrial regions plus Germany, India, China, and 100+ countries for your multi-market expansion strategy.

QWhy should I expand my manufacturing or industrial automation business to Poland?

Poland offers one of the most structurally compelling market entry cases in Europe for manufacturing and industrial automation companies. It is the EU’s 6th largest economy, growing at 3.5–3.7% GDP in 2025–2026, more than ten times the EU average of 0.3%. Manufacturing contributes 20–25% of GDP across automotive, food processing, aerospace, electronics, machinery, chemicals, and pharmaceuticals sectors deeply integrated into EU supply chains. Acute labour shortages (unemployment at just 3.2%), minimum wage inflation of 50%+ in five years, and demographic decline projecting a 20% population reduction by 2070 are creating structural automation demand that cannot be resolved through any alternative to technology. The government provides a 50% robotisation tax allowance (valid until end of 2026), 14 Special Economic Zones with CIT exemptions covering the entire country, and over 1,359 EU and national grant programmes for manufacturing businesses. McKinsey estimates half of all Polish workplace activities, 7.3 million jobs, could be automated by 2030 using currently available technology, providing a decades-long demand expansion runway.

QWhat is Poland’s 50% robotisation tax allowance and how does it affect my sales strategy?

Poland’s robotisation tax allowance permits Polish manufacturers to deduct 50% of qualifying robot investment costs from their taxable income, in addition to standard depreciation deductions. Qualifying costs include new industrial robots, machinery and equipment functionally related to robots, leasing fees, implementation costs, and employee training. The allowance is valid until the end of 2026 for all Polish CIT and PIT taxpayers. For your sales strategy: a PLN 500,000 robot system has an effective net cost of PLN 250,000 after the tax benefit, a 50% immediate return before the robot produces a single part. Every proposal to a Polish manufacturer should include a robotisation allowance calculation alongside labour cost savings and productivity ROI. Train your Polish distributors to lead with this calculation, it compresses sales cycles, reduces price objections, and positions automation as a financially compelling decision even for cost-constrained manufacturers. This allowance is the most powerful demand accelerator in any EU automation market and should be central to your entire Polish go-to-market approach.

QWhat are the best entry models for expanding a manufacturing or automation business to Poland?

For most first-time Poland entrants in industrial automation and manufacturing technology, the recommended entry sequence is: (1) Appoint a verified Polish national distributor or regional channel partners, lowest capital, fastest market access (3–9 months to first revenue). Focus the first distributor selection on sector expertise in your primary target vertical (automotive/Silesia, food/Greater Poland, aerospace/Podkarpacie, electronics/Lower Silesia) rather than national geographic coverage alone. (2) After 2–3 years of validated market presence, evaluate establishing a Polish Sp. z o.o. (limited liability company) for greater commercial control, direct customer engagement, and access to Polish Investment Zone CIT exemptions. (3) If local production is commercially justified, for EU supply chain nearshoring or SEZ incentive access, pursue OEZ-based assembly or contract manufacturing via a qualified Polish EMS partner. Technology licensing to a Polish partner is appropriate where Polish-language adaptation and local production matter for customer acceptance but direct establishment is premature. Joint ventures are most suitable when access to an established Polish customer base is the primary value driver and shared capital risk of OIZ/SEZ manufacturing is the strategic goal.

QHow do I find a verified distributor for industrial automation products in Poland?

The most efficient and secure route to finding a verified Polish industrial automation distributor is through GTsetu’s compliance-verified B2B platform, where every Polish company has been verified through KRS registration, NIP tax ID, import licences, and industry certifications before appearing in the network. GTsetu enables anonymous discovery of verified Polish partner profiles, digital GDPR-compliant NDA execution before sharing technical data, and secure encrypted workspace collaboration, all with zero broker commissions. Supplement with targeted trade show attendance (AUTOMATICON Warsaw, ITM Poland Poznań), bilateral chamber engagement (AHK Polen, the Polish-German Chamber), and PAIH facilitation for sector-specific introductions. Always verify candidates independently, or use a platform where pre-verification is already complete, before sharing product specifications or pricing. See our guide on how to find international distributors for the complete methodology, and our guide on industrial business collaboration for structuring the partnership once found.

QWhat are the key regulations for manufacturing companies entering Poland?

Key regulatory requirements for manufacturing companies entering Poland: (1) Business entity registration, Sp. z o.o. (limited liability company) via the KRS online portal; minimum PLN 5,000 share capital; typically completed in 3–7 business days. (2) EU single market compliance, Poland is a full EU member state; CE marking (mandatory for machinery, electrical equipment, and most industrial products), REACH, RoHS, and all EU product safety directives apply. For EU-registered companies, no additional Polish-specific product certification is required for most automation products. (3) Tax registration, CIT at 9% (small taxpayers) or 19% standard; VAT at 23%; extensive CIT exemptions under PIZ/SEZ investment decisions. (4) GDPR, applies in full; Polish data protection authority (UODO) enforces; critical for IIoT and cloud-connected automation deployments. (5) Employment law, Polish Labour Code; ZUS social insurance registration mandatory for all employees. (6) SEZ/PIZ permit, for operations within Special Economic Zones; applied through SEZ manager with qualifying investment thresholds. Poland’s EU membership means there is no special import licensing regime for most industrial automation products, standard EU customs procedures apply for non-EU origin goods.

QWhich industrial sectors in Poland have the highest automation investment demand?

The sectors with the highest industrial automation investment demand in Poland in 2026 are: (1) Automotive and EV manufacturing, the largest automation demand segment, concentrated in Silesia (Katowice, Gliwice, Tychy); EV investment wave from Mercedes-Benz, LG Energy Solution, and existing OEM capacity expansion driving battery assembly, robotic welding, and precision inspection demand. (2) Food and beverage processing, Poland’s largest industrial sector by revenue (PLN 344.1 billion), with acute labour shortages in meat, dairy, and bakery creating urgent automation demand; handling operations (52% of all cobot applications) are concentrated here. (3) Metal processing, nationwide welder shortage since at least 2016; welding automation is the fastest-growing application in Poland (17% of new installations). (4) Aerospace and defence, Aviation Valley (Podkarpacie) and Silesian Aviation Cluster; 4.8% of GDP defence spending driving advanced manufacturing automation for precision components. (5) Electronics and white goods, Lower Silesia (Wrocław, Wałbrzych); LG, Philips, Miele, BSH driving SMT, assembly, and test automation. (6) Pharmaceuticals, growing GMP compliance requirements driving serialisation, packaging, and process automation investment. The Silesia region (automotive/heavy industry) holds the largest installed automation base; Lower Silesia (EV batteries/electronics) is the fastest-growing cluster.

QHow does the Polish Investment Zone (PIZ) differ from the old Special Economic Zones?

The Polish Investment Zone (PIZ) was introduced by the Act of 10 May 2018 and represents a major expansion of the original Special Economic Zone (SEZ) concept. The critical difference: under the old SEZ system, CIT exemptions were only available within the defined SEZ boundaries (approximately 0.08% of Polish territory). Under the PIZ, income tax exemption (CIT or PIT) is available across the entire territory of Poland, on both public and privately owned properties, for companies implementing qualifying new investments. This means you no longer need to locate within a specific SEZ parcel to access tax exemption benefits. The 14 existing SEZs continue to operate as zone managers and facilitation infrastructure under the PIZ umbrella, but their geographic restriction has been removed. Existing SEZ permits granted before the 2018 reform remain valid until the end of 2026 under the old rules. New investment decisions under PIZ are issued with 12–15 year exemption periods depending on location history. For foreign manufacturers, this means CIT exemption is available for virtually any Polish location, removing the site selection constraint that the old SEZ system imposed while retaining the infrastructure and ecosystem benefits that SEZ managers provide.

Ready to Expand Your Manufacturing Business to Poland?

Connect with verified Polish manufacturers, distributors, and technology partners on GTsetu, with compliance-backed verification, anonymous discovery, GDPR-compliant NDA workflows, and zero broker commissions on every Poland market partnership you form.

They represents the product, and research team behind GTsetu, a global B2B collaboration platform built to help companies explore cross-border partnerships with clarity and trust. The team focuses on simplifying early-stage international business discovery by combining structured company profiles, verification-led access, and controlled collaboration workflows.

With a strong emphasis on trust, and disciplined engagement, Team GTsetu shares insights on global trade, partnerships, and cross-border collaboration, helping businesses make informed decisions before entering deeper commercial discussions.