How to Expand Your Manufacturing & Industrial Automation Business to New Zealand

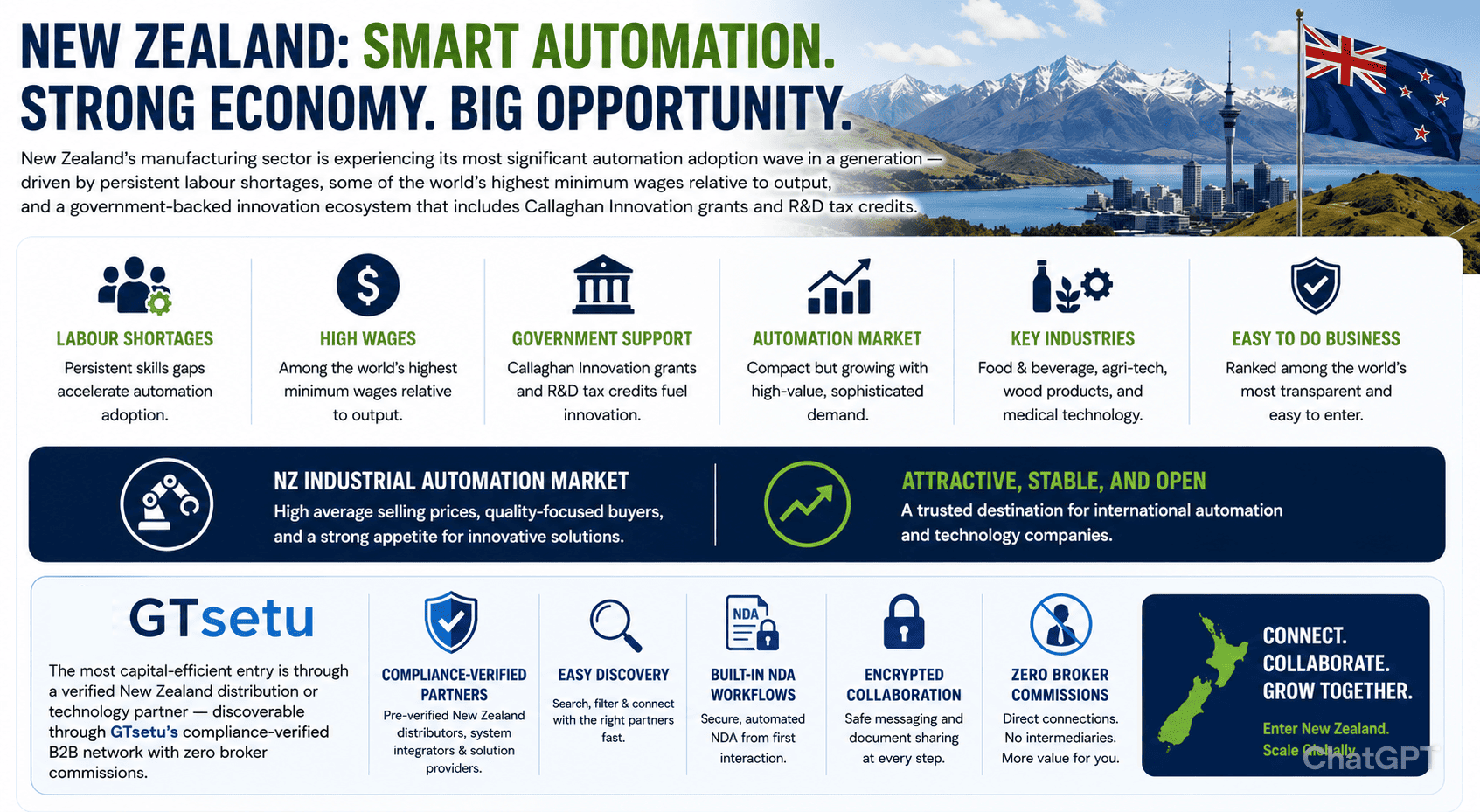

Direct Answer: New Zealand’s manufacturing sector is experiencing its most significant automation adoption wave in a generation, driven by persistent labour shortages, some of the world’s highest minimum wages relative to output, and a government-backed innovation ecosystem that includes Callaghan Innovation grants and R&D tax credits. The NZ industrial automation market, while compact by global standards, is characterised by high average selling prices, sophisticated buyers across food & beverage, agri-tech, wood products, and medical technology, and a business environment ranked among the world’s most transparent and easy to enter. The most capital-efficient entry is through a verified New Zealand distribution or technology partner, discoverable through GTsetu‘s compliance-verified B2B network with zero broker commissions.

📅 April 5, 2026⏱ 20 min read✍️ GT Setu Editorial Team🔄 Updated regularly

~12%

Manufacturing Share of NZ GDP

#1

World Bank Ease of Doing Business Ranking (Historically)

20%

Callaghan R&D Growth Grant on Eligible R&D Spend

0%

GTsetu Broker Commission

New Zealand punches far above its weight in manufacturing sophistication. A nation of five million people produces world-class dairy processing technology, globally respected wine and premium food products, sophisticated marine vessel components, and a rapidly maturing medical technology manufacturing sector, all while maintaining one of the world’s most transparent and business-friendly regulatory environments. For international manufacturers, industrial automation OEMs, robotics companies, and technology integrators, New Zealand in 2026 presents a market opportunity defined by quality, not quantity, high-value industrial buyers who make thoughtful technology investment decisions and become loyal, long-term supplier partners when they find the right fit.

New Zealand’s automation investment wave is being driven by a convergence of structural forces that have no short-term resolution: minimum wages that have increased by over 50% in a decade, a persistent skilled trades shortage that leaves manufacturing positions unfilled for months, a government actively supporting innovation through Callaghan Innovation grants, and increasing export market pressure from premium food and agri-product buyers in Japan, the US, and the EU who demand demonstrable quality assurance systems. This guide covers every dimension, from market sizing and sector opportunity to regulatory requirements, partner qualification, and the step-by-step roadmap for successful New Zealand market entry. You can also explore our guides on advantages and disadvantages of global expansion and international business development consulting for broader strategic context.

🇳🇿 Who Is This Guide For?

This guide is written for international manufacturers, industrial automation OEMs, robotics and control system providers, technology integrators, and industrial equipment companies seeking to enter or expand in the New Zealand market, whether through a distributor partnership, technology licensing, joint venture, or direct establishment. It is also relevant for companies already serving New Zealand through their Australian operations who want to formalise their NZ market presence. If you are exploring other markets alongside New Zealand, see our country guides: Australia, India, Vietnam, Germany, and United Kingdom.

SECTION 1

1 Why New Zealand for Manufacturing & Industrial Automation?

🎯 The Strategic Case

New Zealand is not a volume market for industrial automation, it is a value market. Its 25,000+ manufacturing businesses are predominantly SMEs making deliberate, long-term technology investment decisions with an eye on export competitiveness, food safety compliance, and labour cost management. For international automation companies, New Zealand’s combination of high labour costs driving compelling automation ROI, sophisticated buyers who value quality and service over price, an innovation-supportive government funding landscape, and a Trans-Tasman relationship with Australia that enables dual-market entry creates a uniquely attractive proposition that larger-volume emerging markets cannot replicate.

50%+

Increase in New Zealand minimum wages over the past decade, creating powerful economic incentive for automation investment across all manufacturing sectors

25,000+

Manufacturing businesses in New Zealand, the majority are SMEs making active technology investment decisions, with food & beverage the largest single sector

1–3 days

Company incorporation timeline in New Zealand, one of the world’s fastest and simplest business registration processes, with no minimum capital requirement

💼

World-Class Business Environment

New Zealand historically ranks #1 globally for ease of doing business, transparent regulations, effective IP protection, no foreign ownership restrictions in most sectors, and a legal framework based on English common law that is familiar to companies from most major trading nations. Business setup takes 1–3 days with no minimum capital.

💰

High Labour Costs Accelerating Automation ROI

With a minimum wage of NZ$23.15/hour (as of April 2025) and skilled trades commanding NZ$35–60+/hour, New Zealand manufacturers face a compelling economics case for automation. Payroll-related costs including Kiwisaver (3% employer contribution), ACC levies, and leave entitlements add further to the relative ROI of automated systems versus manual labour.

🧪

Callaghan Innovation Funding Access

Callaghan Innovation provides 20% R&D Growth Grants on eligible R&D expenditure for New Zealand-incorporated companies. International automation companies establishing a New Zealand entity and conducting qualifying R&D, including product adaptation for NZ market requirements, can access this funding, significantly reducing technology development costs.

🌏

Trans-Tasman & CPTPP Trade Access

New Zealand’s Closer Economic Relations (CER) agreement with Australia creates a seamless Trans-Tasman single market, enabling companies with New Zealand presence to serve both markets from a single regional structure. The CPTPP (Comprehensive and Progressive Agreement for Trans-Pacific Partnership) further provides preferential market access to Japan, Canada, Mexico, Singapore, Vietnam, and other partners.

🍃

Premium Agri-Food Export Demand

New Zealand’s positioning as a premium food producer, clean, green, and sustainably produced, creates structural demand for food safety automation, traceability systems, and quality assurance technology that international buyers in Japan, the US, EU, and the Middle East increasingly require. This is a durable, export-driven automation demand driver.

🏥

Growing MedTech & AgriTech Sectors

New Zealand’s medical technology manufacturing sector, producing diagnostic equipment, surgical instruments, and wound care products, is growing rapidly and requires precision automation and clean manufacturing capability. The agri-tech sector, applying technology to primary industries, is one of New Zealand’s fastest-growing innovation areas with direct automation technology demand. See our technology partnership guide for structuring innovation-driven entries.

New Zealand’s industrial automation market is small in absolute dollar terms, reflecting the country’s population of five million, but punches above its weight in automation adoption intensity relative to GDP. Multiple industry signals confirm a sustained acceleration in automation investment across NZ manufacturing, driven by structural labour market pressures that industry bodies and government have both identified as requiring technology-led responses.

Market Signal / Source

Key Finding

Automation Implication

Advancing Manufacturing Aotearoa (AMA) / Industry Survey 2025–2026

NZ manufacturers are rapidly adopting robotics, collaborative robots (cobots), vision systems, and AI-driven quality inspection, with automation being applied to material handling, repetitive machining, quality checks, and high-precision assembly steps

Broad-based SME adoption wave, not just large manufacturers; cobots and modular automation are the dominant growth segment

Novotek Automation Robotics (NZ Automation Industry Report 2026)

NZ manufacturing faces growing pressure from rising labour costs, skills shortages, and export competitiveness requirements, driving adoption across food & beverage, logistics, and cosmetics packaging sectors

Palletising, packaging, logistics automation, and cobot deployments are the highest-growth application segments

EMA (Employers & Manufacturers Association) 2025

NZ manufacturing struggling with high operational costs, increasing global competition, outdated technology, and skills shortages, Industry 4.0 adoption identified as critical for sector competitiveness

Industry 4.0 technology investment, IIoT, digital manufacturing, smart factory systems, is now a strategic priority for NZ manufacturers

New Zealand Government / Beehive (Digital Tools for Manufacturing Productivity)

Government actively promoting digital tools and manufacturing technology adoption to boost productivity, including targeted support through Callaghan Innovation and sector-specific grant programmes

Government demand signal confirms policy-backed investment momentum in manufacturing technology adoption

University of Auckland, LISMS Research Centre

Active research in smart manufacturing, intelligent systems, and logistics, creating innovation-driven automation technology development with commercial pathway potential through Callaghan co-funding

Co-development opportunities for international automation companies seeking NZ market adaptation and R&D funding access

While New Zealand does not have the scale of automation markets like Germany, Australia, or India, its automation market characteristics are compelling for specific types of international companies: those offering cobot and flexible automation for SME manufacturers, food and beverage processing and packaging automation, agri-tech and primary industry automation, and modular IIoT and quality management platforms that can be implemented without large capital outlays. Average selling prices are high relative to volume, making New Zealand a quality rather than quantity revenue opportunity.

Key Market Drivers for International Companies Entering New Zealand

💰

Structural Labour Cost Pressure & Minimum Wage Growth

New Zealand’s minimum wage has grown from NZ$15.75/hour in 2018 to NZ$23.15/hour in 2025, a 47% increase in seven years. With further increases anticipated, the economic case for automation investment strengthens every year for NZ manufacturers. This is not a cyclical trend, it is a structural, policy-driven shift that makes automation ROI compelling even for mid-size SMEs who previously considered automation too capital-intensive.

Structural Driver

👷

Persistent Skills Shortage Across Manufacturing Trades

New Zealand’s manufacturing sector faces ongoing shortages of qualified tradespeople, welders, machinists, electrical engineers, and food processing technicians, with positions frequently unfilled for three to six months. Immigration-based solutions remain constrained. Automation is increasingly the only viable response to a skills shortage that cannot be resolved through conventional recruitment and is worsening as the manufacturing workforce ages.

New Zealand’s primary export markets, Japan, China, the US, EU, and the Middle East, are imposing increasingly stringent food safety, traceability, and sustainability documentation requirements on NZ food exporters. Meeting these requirements reliably and demonstrably requires food safety automation, vision inspection, serialisation, and digital batch record systems that only technology investment can provide at the scale and consistency demanded.

Export Driver

🤖

Cobot & Flexible Automation Democratisation

The availability of affordable collaborative robots (cobots), modular automation systems, and scalable IIoT platforms has dramatically lowered the entry cost of automation for NZ’s predominantly SME manufacturing base. What previously required NZ$500,000+ capital investment can now be achieved for NZ$50,000–150,000 with fast ROI timelines, opening the addressable NZ automation market far beyond large food processors and dairy cooperatives to thousands of mid-size manufacturers.

Callaghan Innovation’s R&D Growth Grant (20% of eligible R&D expenditure) and project co-funding are enabling NZ manufacturers to invest in automation technology adoption and adaptation that would otherwise be financially prohibitive. International automation companies whose technology qualifies as enabling R&D spend for NZ manufacturers can position their products as Callaghan-eligible investments, significantly reducing the effective customer acquisition cost in a cost-sensitive SME market.

Policy Driver

🏗️

Construction & Infrastructure Rebuild Demand

New Zealand’s ongoing construction sector boom, combined with the Christchurch rebuild legacy and current infrastructure investment, is driving demand for automated production of construction materials: precast concrete, structural steel, prefabricated building products, and engineered timber. This sector is less well-served by existing automation providers than food & beverage, creating opportunity for international entrants with construction materials automation expertise.

Emerging Driver

SECTION 3

3 High-Demand Sectors for Industrial Automation in New Zealand

Industrial automation demand in New Zealand is concentrated in specific verticals where labour cost pressures, export market compliance requirements, government support, and SME modernisation investment are creating the most active buying environment. Understanding which sectors offer the highest automation demand enables international companies to focus their New Zealand go-to-market strategy.

🥛Largest Sector

Dairy & Food Processing

New Zealand’s dairy processing sector, Fonterra, Synlait, Westland, and hundreds of specialty producers, is the country’s single largest manufacturing industry and the highest-value automation buyer. Milk processing, cheese manufacturing, infant formula production, and yoghurt/butter lines require high-hygiene automation, CIP/SIP systems, quality inspection, and packaging automation meeting global food safety standards.

New Zealand’s world-renowned wine sector, Marlborough Sauvignon Blanc, Central Otago Pinot Noir, and premium horticultural exports (kiwifruit, apples, stone fruit) require sophisticated automated sorting, grading, packaging, and traceability systems to meet export market requirements from Japan, the US, and the EU. Zespri and New Zealand Winegrowers members are active technology adopters.

New Zealand’s red meat and seafood export industries, beef, lamb, venison, and salmon, are under sustained pressure to automate primary processing tasks that are difficult to staff in regional locations. Robotic carcass processing, automated cut-and-portion systems, vision-based grading, and cold chain automation are all active investment areas for major processors including Silver Fern Farms, Alliance Group, and Sanford.

New Zealand’s medical technology manufacturing cluster, producing diagnostic devices, surgical instruments, wound care products, and veterinary equipment, is a growing precision manufacturing sector. Medsafe (NZ medicines regulator) and ISO 13485 compliance requirements drive investment in cleanroom automation, traceability, and quality management systems that international automation companies are well-positioned to supply.

New Zealand’s forestry and wood products sector, a major export industry producing timber, LVL, plywood, and engineered wood products, is actively automating processing lines to address remote location labour challenges and improve precision cutting, grading, and packaging. The sector’s move toward engineered timber (CLT, LVL, glulam) for construction applications is creating new automation demands for precision fabrication.

New Zealand has a disproportionately large and sophisticated marine manufacturing sector, producing luxury superyachts (export value over NZ$400M p.a.), commercial vessels, and advanced composite marine components. Composite fabrication automation, robotic finishing systems, and precision CNC machining automation are key technology demands in this premium, export-focused manufacturing cluster centred around Auckland’s Superyacht Hub.

New Zealand’s primary industries, dairy farming, sheep and beef farming, cropping, and horticulture, are adopting precision agriculture, robotic milking, automated irrigation, and AI-driven crop monitoring at accelerating rates. The agri-tech sector is one of New Zealand’s fastest-growing innovation areas, with companies like Robotics Plus, Pykl Plant, and Halter attracting international investment and creating demand for enabling automation technologies.

Key demand: robotic milking/harvesting, precision irrigation automation, IoT sensors, data platforms, drone systems

🏗️Infrastructure

Construction Materials & Prefab

New Zealand’s construction sector boom, driven by housing shortfall, infrastructure investment, and rebuilding from natural disasters, is driving demand for automated production of precast concrete, prefabricated building panels, engineered steel components, and modular building systems. Offsite manufacturing and prefabrication are growing rapidly, creating new automation opportunities in a sector historically characterised by manual production.

4 Key Industrial & Manufacturing Hubs Across New Zealand

New Zealand’s manufacturing geography is distributed across both islands, with distinct sector specialisations by region. Understanding this geography is essential for designing distribution networks and targeting initial sales efforts, New Zealand’s relatively compact geography means a well-structured national distributor with regional engineers can cover the entire market effectively.

🏙️ Auckland, Advanced Mfg, Marine & MedTech Hub

New Zealand’s largest city and commercial centre. Auckland hosts the highest concentration of advanced manufacturing, marine (superyacht manufacturing, composite boatbuilding), medical technology, electronics assembly, food and beverage processing, and cosmetics/FMCG manufacturing. The EMA (Employers and Manufacturers Association) and most major industry associations are based in Auckland.

Key clusters: Superyacht Industry (Henderson), South Auckland Manufacturing Corridor, MedTech Hub, Wiri Food Processing

🌿 Waikato & Bay of Plenty, Dairy & Agri-Food

The Waikato region is the heart of New Zealand’s dairy processing industry, Fonterra’s major manufacturing sites, Synlait’s facilities, and numerous specialty dairy producers. The Bay of Plenty is New Zealand’s kiwifruit capital (Zespri) with significant packhouse automation investment. Hamilton is a growing advanced manufacturing and engineering hub.

Key clusters: Fonterra Waikato Sites, Te Awamutu Dairy Processing, Bay of Plenty Packhouses, Hamilton Engineering

🍷 Nelson-Marlborough & Hawke’s Bay, Wine & Horticulture

Marlborough is New Zealand’s largest wine region, home to the world’s most famous Sauvignon Blanc production, with significant automated bottling, labelling, and palletising investment. Hawke’s Bay is the country’s premier horticultural region with apple, pear, and stone fruit packhouse automation. Nelson hosts significant wood products and aquaculture manufacturing.

Key clusters: Marlborough Wine Processing, Hawke’s Bay Packhouses, Nelson Wood Products, Gisborne Horticulture

Christchurch is New Zealand’s second manufacturing centre, hosting significant meat processing (Alliance Group), dairy (Open Country Dairy), engineering manufacturing, and agri-tech. The Christchurch post-earthquake rebuild created a modern, technology-forward manufacturing base. Canterbury hosts the Southern Manufacturing & Electronics show, New Zealand’s premier manufacturing trade event.

Key clusters: Rolleston Industrial Park, Christchurch Airport Innovation Precinct, Mid-Canterbury Dairy, South Canterbury Meat

🦌 Southland & Otago, Meat, Dairy & Marine

Southland is New Zealand’s southernmost and largest geographic region with major meat processing (Silver Fern Farms, Alliance Group’s flagship plants), dairy processing (Fonterra Edendale), and aluminium smelting. The Southland region has New Zealand’s highest automation investment intensity in meat processing. Dunedin hosts engineering and electronics manufacturing.

Northland hosts significant timber processing, wood product manufacturing, and cement production. Gisborne is the centre of New Zealand’s East Coast forestry and horticulture processing. These regions offer emerging automation opportunities in wood processing, timber grading, and packhouse operations where labour availability is most constrained.

For most international industrial automation companies entering New Zealand, a national distributor with an Auckland headquarters and engineering resources in Christchurch provides adequate coverage for the majority of the market. Waikato/Bay of Plenty regional coverage is essential for dairy and horticulture automation; Southland/Otago coverage is critical for meat processing. New Zealand’s compact geography (the North Island is roughly the size of England) means that a motivated national distributor with a mid-size team can realistically cover the entire country with targeted regional visits. The key differentiator is not geographic coverage per se, but sector specialisation, a distributor with deep food & beverage sector relationships is worth more than one with broad geographic coverage across unrelated industries. See our guide to building a distributor network.

SECTION 5

5 Market Entry Models: Choosing the Right Approach

New Zealand offers one of the world’s most straightforward regulatory environments for foreign company entry, 100% foreign ownership, no minimum capital requirement, fast online incorporation, and no foreign ownership approval requirements in most sectors. The right entry model depends on your product category, target sectors, and whether you are approaching New Zealand as a standalone market or as part of a Trans-Tasman Australia-NZ strategy.

Entry Model

How It Works

Capital Required

Time to Revenue

Best For

Key Reference

New Zealand Distributor / Channel Partner

Appoint a verified NZ company to stock, sell, and support your products, assumes inventory and credit risk, serves defined sectors or territories

Very Low

3–9 months

Industrial automation hardware, instruments, sensors, packaging machinery, standardised products with established NZ applications

Trans-Tasman Australian Distributor with NZ Operations

Serve the NZ market through an existing Australian distributor that also covers New Zealand, leveraging CER agreement and single Trans-Tasman market structure

None (if Australian distributor is already appointed)

Immediate (if Australian distributor has NZ capability)

Companies already in Australia seeking NZ market extension; standardised products with identical or near-identical NZ and Australian requirements

Incorporate a New Zealand Ltd, 100% foreign ownership permitted, no minimum capital, no NZ-resident director required (since 2022 regulatory change), online registration at companiesoffice.govt.nz in 1–3 days

Low–Moderate

3–6 months (setup + first revenue)

Long-term strategic NZ commitment; Callaghan Innovation grant eligibility; direct sales operations; government procurement qualification

Co-invest in a jointly owned NZ Ltd with an established NZ manufacturer, system integrator, or distribution group, shared equity, governance, and market access

Moderate–High (shared)

12–18 months (structure + setup)

Complex automation technology requiring deep local sector integration; markets where NZ engineering credibility or existing customer relationships provide decisive advantage

Partner with a New Zealand Crown Research Institute (AgResearch, Plant & Food Research, Scion, ESR) or university (University of Auckland, AUT, Lincoln) to co-develop NZ-adapted solutions

Shared

18–36 months (development cycle)

Adapting global platforms to NZ industry requirements; accessing Callaghan Innovation co-funding; building credibility with NZ agri-food and primary industry buyers

Many international automation companies approach the New Zealand market as an extension of their Australian strategy rather than a standalone entry. The CER agreement means products already approved for Australian sale under RCM mark are generally accepted in New Zealand without additional certification. If you have an established Australian distribution network, assess whether extending that distributor’s remit to cover New Zealand is more efficient than a separate NZ-specific appointment, particularly for standardised product lines with identical technical requirements in both markets. However, for sectors where NZ has distinct requirements, agri-food processing, dairy specifically, or primary industry applications, a dedicated NZ specialist with deep sector relationships will outperform an Australian distributor operating at arm’s length. See our territory rights guide for structuring Trans-Tasman commercial arrangements.

SECTION 6

6 Callaghan Innovation & Government Support Programmes

🏛️ Policy Overview

Callaghan Innovation is New Zealand’s government agency for business innovation, providing R&D grants, co-funding, technical expert access, and capability building to NZ-incorporated companies investing in research and development. For international automation companies establishing a New Zealand subsidiary or entering joint venture arrangements, Callaghan Innovation funding can significantly reduce the effective cost of adapting products to New Zealand market requirements, developing New Zealand-specific applications, or conducting R&D in partnership with NZ universities or Crown Research Institutes (CRIs). The flagship programme, the R&D Growth Grant, provides a 20% grant on eligible R&D expenditure for companies spending at least NZ$50,000 annually on qualifying R&D. New Zealand also provides a 15% R&D tax credit (since 2019) for companies that do not qualify for Growth Grants.

Key Government Support Programmes for Manufacturing & Automation Companies

Programme

Managing Body

Relevance to Automation Companies

Funding Mechanism

R&D Growth Grant

Callaghan Innovation

High, 20% grant on eligible R&D expenditure for NZ Ltd entities; covers software development, hardware adaptation, and application engineering qualifying as R&D under NZ definition

20% grant on eligible R&D spending above NZ$50,000 threshold; ongoing annual grant for qualifying companies

R&D Project Grants (Callaghan Co-funding)

Callaghan Innovation

High, project-specific co-funding for R&D projects with NZ universities or CRIs; enables international companies to part-fund NZ market adaptation projects

Up to 40% co-funding for qualifying project R&D; project duration typically 12–36 months

R&D Tax Incentive (RDTI)

Inland Revenue (IRD)

Medium, 15% tax credit on eligible R&D expenditure for NZ Ltd entities not qualifying for Growth Grants; accessible to most NZ-incorporated entities conducting qualifying R&D

15% refundable tax credit on eligible R&D expenditure; registered via IRD/Callaghan

New Zealand Trade and Enterprise (NZTE)

NZTE

High, NZTE provides free international investment facilitation, introductions to NZ manufacturers for international companies, and sector intelligence for market entry planning. Also facilitates NZ company export support that creates opportunities for international technology partners

Free advisory and introduction services; market intelligence; capability building grants for NZ exporters (indirect demand signal)

Primary Growth Partnership (PGP) & Agri-Tech

Ministry for Primary Industries (MPI)

Medium, Government-industry co-investment in primary industry productivity including agri-tech and precision agriculture automation. CRI co-development opportunities for international automation technology companies targeting agri and food sectors

Multi-year Government-industry co-investment; typically NZ$5M–50M scale partnerships

Regional Business Partner (RBP) Network

Regional economic development agencies + Callaghan

Medium, regional advisers help NZ SMEs access innovation funding and connect with technology providers; can be a direct channel for international automation companies to reach NZ SME manufacturer buyers

Subsidised advisory services and innovation vouchers for NZ SMEs, creates funded procurement budget for qualifying technology purchases

🇳🇿 Callaghan Strategy for International Automation Companies

The most effective way for international automation companies to leverage the Callaghan Innovation ecosystem is to position their NZ market entry as a co-development partnership rather than a pure distribution play. By establishing a NZ Ltd entity and partnering with a Crown Research Institute (Plant & Food Research for food sector, AgResearch for pastoral, Scion for wood products) to adapt your technology for NZ-specific applications, you can access Callaghan project co-funding while building the NZ reference installations that unlock broader commercial sales. This is a higher-effort entry path than pure distribution, but creates significant competitive barriers once NZ-specific product adaptations and CRI endorsement are established. Contact Callaghan Innovation’s Business Development team or engage NZTE’s investment facilitation service as early as possible in your NZ market entry planning. Explore our technology partnership and co-development partnership guides for structuring these arrangements.

SECTION 7

7 Regulatory & Compliance Requirements for Entry

New Zealand has one of the world’s most streamlined regulatory environments for foreign companies. The compliance requirements for manufacturing and industrial automation companies are specific and manageable with appropriate planning, and New Zealand’s government actively provides support for international companies navigating the regulatory landscape.

01

Business Registration, Companies Office (Ltd)

New Zealand’s business registration is managed by the Companies Office (companiesoffice.govt.nz) and is one of the world’s simplest, online registration takes 1–3 business days with a NZ$161 registration fee. A New Zealand Limited Liability Company (Ltd) requires at least one director (the 2022 Companies Amendment Act removed the previous NZ-resident director requirement, international directors are now acceptable) and at least one shareholder. No minimum share capital is required. All companies require a registered New Zealand address (available through commercial registered office service providers). The Ltd is the standard vehicle for commercial operations; a branch office of a foreign company (Overseas Company registration) is the alternative for those who prefer not to create a separate NZ legal entity.

02

GST Registration & Tax Compliance

New Zealand’s Goods and Services Tax (GST) applies at 15% on most commercial transactions. GST registration is mandatory for entities with NZ$60,000+ annual turnover and is straightforward through Inland Revenue (IRD). Income tax for NZ Ltd companies is at 28%. Employer obligations include PAYE (Pay As You Earn tax deduction), KiwiSaver employer contributions (3% of gross salary), and ACC (Accident Compensation Corporation) employer levies. For companies supplying goods from overseas to a NZ distributor without establishing a NZ entity, GST on imported goods is handled by the importer, assess the GST implications of your distribution structure with a NZ tax adviser. Transfer pricing rules apply to related-party transactions between a NZ Ltd and its overseas parent.

03

RCM Mark, Electrical & Electronic Equipment

New Zealand and Australia share the Regulatory Compliance Mark (RCM) for electrical, electronic, and telecommunications equipment, meaning that RCM-certified products approved for Australia can generally be sold in New Zealand without separate NZ certification. For international companies already CE-marked for European markets or UL-listed for North America, RCM compliance requires testing against applicable AS/NZS standards, which may partially leverage existing test data but typically requires some additional NZ/AU-specific testing. The Electrical Workers Registration Board (EWRB) in New Zealand also regulates electrical installation work, ensure your products come with appropriate installation documentation for NZ-licensed electricians. Plan 2–4 months for RCM compliance for most product categories.

04

Health & Safety at Work Act 2015 (HSWA)

New Zealand’s Health and Safety at Work Act 2015 (HSWA) establishes a duty of care framework for all persons conducting a business or undertaking (PCBUs), including designers, manufacturers, and suppliers of industrial plant and equipment. Manufacturers and importers of plant (machinery and equipment) must ensure, so far as is reasonably practicable, that the plant is designed and manufactured to be without risks to health and safety. This requires: hazard identification and risk assessment documentation, adequate information for installation and operation, compliance with relevant NZ standards where applicable, and appropriate safety guarding. For automation equipment, WorkSafe New Zealand (the regulator) actively monitors compliance with HSWA plant safety requirements, ensure your NZ distributor understands their PCBU obligations and your product documentation supports their compliance.

05

Privacy Act 2020 & New Zealand Privacy Principles

New Zealand’s Privacy Act 2020 establishes 13 Information Privacy Principles (IPPs) governing the collection, use, disclosure, and storage of personal information, applying to all entities collecting or using personal information of New Zealanders. For cloud-connected industrial automation products, IIoT sensors, condition monitoring, production tracking systems, data handling involving employee operational data or data that can be linked to individuals must comply with the IPPs. Cross-border data transfer provisions require the overseas recipient to provide comparable privacy protection. New Zealand’s privacy framework is broadly compatible with Australia’s and GDPR, but has NZ-specific requirements including mandatory breach notification to the Privacy Commissioner. See our B2B secure collaboration guide.

06

IP Protection in New Zealand

New Zealand’s Intellectual Property Office (IPONZ) manages trademark and patent registration, straightforward, fast, and well-enforced. Trademark registration in New Zealand takes 10–12 months for uncontested applications and provides 10-year protection renewable indefinitely. Patent protection (standard patent: 20 years; innovation patent not available in NZ) requires application through IPONZ and can leverage PCT national phase status for international filers. Copyright is automatic in New Zealand, no registration required, and is internationally recognised through New Zealand’s obligations under the Berne Convention. For software-embedded automation systems, document your copyright claims and version history. Execute trademark filings before significant NZ commercial activity, prior use alone does not establish registered trademark rights in New Zealand. See our IP ownership in manufacturing partnerships guide.

07

Food & Primary Industry Sector-Specific Compliance

For automation equipment deployed in food processing, dairy, or meat processing environments, New Zealand’s largest automation markets, additional sector-specific compliance requirements apply. MPI (Ministry for Primary Industries) regulated food processing facilities must meet specific hygiene, materials, and cleanability standards for equipment in contact with or adjacent to food, ensure your automation equipment is designed and documented to comply with MPI requirements and relevant food hygiene standards (3-A, EHEDG, or AS 4674 for NZ food facilities). Dairy processing facilities operated under Fonterra or regulated NZ dairy factory standards may have additional equipment approval requirements. Engage your NZ distributor to confirm sector-specific compliance requirements for your specific product category before initiating commercial sales into food processing accounts.

SECTION 8

8 Finding a Verified NZ Distribution or Technology Partner

For international manufacturing and industrial automation companies entering New Zealand, finding the right partner is the most consequential market entry decision. New Zealand’s business culture is relationship-driven and trust-based, referrals carry enormous weight, and a distributor’s existing customer relationships in your target sector are often more valuable than their geographic coverage or product range breadth. The right NZ partner opens doors that cold outreach cannot.

What to Look for in a New Zealand Industrial Automation Distributor or Partner

✅

Verified Business Identity

Companies Office (NZBN) registration, IRD number, GST registration, and relevant industry certifications (ISO 9001, HACCP for food sector, HSWA compliance management). Non-negotiable baseline, see business verification requirements.

Does the partner have genuine customer relationships in your target NZ sectors, dairy, meat, horticulture, marine, wood products, or MedTech? A distributor who can pick up the phone and call the engineering manager at Fonterra Waikato or Silver Fern Farms Southland is worth exponentially more than one with a broad but shallow national reach. Request a sector-specific reference list.

🔧

Technical Engineering Capability

New Zealand industrial buyers expect genuine application engineering support, not just product order processing. Does the partner have qualified engineers who can perform application consulting, system commissioning, and ongoing technical support? For food sector accounts, hygiene-aware installation knowledge and MPI regulatory understanding are essential.

🗺️

Regional Coverage & Field Service Capability

Can the partner provide service coverage in the regional locations where your target customers operate, Southland meat plants, Waikato dairy, Bay of Plenty packhouses, Marlborough wineries? Regional service capability is a significant competitive differentiator in a market where many food processing plants are in provincial locations hours from major cities.

🧪

Callaghan & Innovation Ecosystem Connectivity

Is the partner connected to the Callaghan Innovation ecosystem, able to position your automation technology as Callaghan-eligible R&D investment for customer grant applications? Partners who understand Callaghan grant structures and can help customers access funding for automation projects dramatically reduce the effective price point resistance in a cost-conscious SME market. See our partnership evaluation criteria.

💰

Financial Capacity & Working Capital

New Zealand distributors often operate with tighter working capital than their Australian or European counterparts, assess their capacity to maintain adequate stock, fund demonstration equipment, and carry the credit of 30–60 day NZ payment terms. Request trade references and consider whether inventory consignment or extended payment terms may be needed to support initial NZ market development. See our payment terms guide.

🌊

Trans-Tasman Connectivity (If Relevant)

If you are approaching NZ as an extension of your Australian strategy, does your prospective NZ partner have working relationships with your Australian distributor? A conflict between Australian and NZ distribution partners, over accounts, pricing, or parallel imports, can seriously damage both relationships. Define Trans-Tasman commercial boundaries in your agreements before complications arise.

🔐

Confidentiality & NDA Compliance

New Zealand’s business culture is candid and open, which is a commercial virtue, but requires careful management of confidential commercial information. Execute a mutual NDA governed by NZ law before sharing product roadmaps, pricing strategies, or key account targets. Use encrypted data sharing channels, see B2B secure collaboration.

Channels for Finding Verified NZ Partners

💻

GTsetu Verified B2B Platform

GTsetu provides access to verified New Zealand manufacturers, distributors, system integrators, and technology partners, with anonymous discovery, built-in NDA workflow, and encrypted collaboration at zero broker commission. The most efficient and secure channel for verified NZ partner discovery. Compare with alternatives to Alibaba and open directories for a full picture of channel options.

Best for Verified Discovery

🎪

Southern Manufacturing & FoodTech Packtech

Southern Manufacturing & Electronics (SME Expo, Christchurch) is New Zealand’s premier manufacturing trade event, covering automation, electronics, engineering, and advanced manufacturing. FoodTech Packtech (Auckland, biennial) is the primary event for food processing and packaging automation. EMEX (Auckland, biennial) covers engineering and manufacturing. These events are the primary face-to-face channel for partner assessment in NZ. See our top B2B networking places guide.

In-Person Channel

🏛️

NZTE (New Zealand Trade and Enterprise)

New Zealand Trade and Enterprise is the government’s international trade and investment agency, providing free market entry facilitation, investor introductions, and sector-specific intelligence for international companies entering New Zealand. NZTE offices in 40+ countries can facilitate warm introductions to NZ manufacturers and distributors in your target sector. First port of call for any serious NZ market entry.

Government Channel

⚙️

EMA, Manufacturers Network NZ & AMA

The Employers and Manufacturers Association (EMA) is the primary NZ manufacturing industry association, providing member directories and networking. Advancing Manufacturing Aotearoa (AMA) runs The Future Makers initiative promoting automation and technology adoption across NZ manufacturing. Manufacturers Network NZ offers SME manufacturer connections. Sector-specific bodies include the Food & Grocery Council, NZ Wine Growers, and Federated Farmers for agri-food targets. See our B2B business network guide.

Association Channel

🔬

Callaghan Innovation & CRI Network

Callaghan Innovation’s network of technical experts and business R&D advisers can facilitate introductions to NZ manufacturers with active R&D investment, your highest-propensity automation buyers. Crown Research Institutes (Plant & Food Research, AgResearch, Scion, ESR) maintain active industry networks in their respective sectors and can provide warm introductions for international companies with relevant technology for NZ primary industry. See our technology partnership guide.

Innovation Channel

SECTION 9

9 Step-by-Step New Zealand Market Entry Roadmap

01

Market Prioritisation, Validate Sector Fit First

Before committing resources specifically to New Zealand, validate whether your product has genuine fit with the NZ automation demand profile. Which sectors, dairy, meat, horticulture, wine, wood products, MedTech, marine, have the highest unmet demand for your specific automation solution? Is the Trans-Tasman route (extending an Australian distributor) viable, or does NZ’s sector specificity require a dedicated NZ specialist? Use GTsetu’s platform to anonymously browse potential NZ partners and assess sector coverage before revealing your market entry plans. A 2–4 week targeted desk research and partner assessment programme through GTsetu, NZTE consultation, and SME Expo attendance will answer these questions efficiently.

02

RCM Compliance & Food Sector Standards, Assess Early

For companies already RCM-certified for Australia, the NZ regulatory pathway is straightforward, the same RCM mark applies. If not yet RCM-certified, initiate the process immediately, 2–4 months lead time is standard. For food processing applications, assess MPI hygiene standards compliance for your specific equipment category early, food sector accounts (dairy, meat, horticulture) will require compliance documentation before any site demonstration can proceed. For MedTech applications, verify Medsafe regulatory classification for your product before pricing or quoting to NZ customers.

03

Ideal Partner Profile, NZ-Specific Criteria

Define your ideal NZ partner profile with NZ-specific criteria: sector specialisation (dairy / meat / wine / wood / marine / MedTech), regional engineering coverage (Auckland / Waikato-BoP / Canterbury / Southland as needed by sector), Callaghan Innovation familiarity, existing customer relationships in your target accounts, and technical team depth for your specific automation technology. For food sector distribution, also assess whether the partner has food-grade installation experience and understanding of MPI compliance requirements. A precise ideal partner profile makes every GTsetu discovery interaction immediately productive. See our international wholesale distributors guide.

04

Partner Discovery & Verification

Discover candidates through GTsetu’s verified platform, SME Expo/FoodTech Packtech attendance, NZTE introductions, and EMA or AMA member outreach. For every candidate, verify: NZBN (New Zealand Business Number) at companiesoffice.govt.nz, GST registration at IRD, trade references from existing principals, and personal reference checks with their existing customers. GTsetu performs compliance verification for all companies on its platform, eliminating the due diligence burden. See business verification requirements.

05

NDA Execution & Technical Exchange

Execute a mutual NDA governed by New Zealand law before sharing any technical data. NZ business culture is candid, partners will not be offended by an NDA request and typically appreciate the commercial professionalism it signals. GTsetu’s platform has the NDA workflow built in, activated before the encrypted workspace unlocks. Stage your technical disclosure: publicly available product information first, then confidential pricing, product roadmaps, and strategic plans only after NDA is in place and initial trust has been established through direct meetings.

06

Commercial Negotiation, NZ Market Specifics

Negotiate all commercial terms with NZ market specifics in mind: NZD pricing and exchange rate risk allocation; exclusivity structure (sector-specific vs. national; Trans-Tasman boundary treatment); payment terms (standard NZ: 20th of month following invoice; 30–60 days for large manufacturers); GST treatment on all transactions; minimum purchase commitments calibrated to NZ market SME sales cycle realities; regional service coverage SLAs; and Callaghan grant eligibility positioning as part of the commercial proposition. See our guides on pricing structures and MOQ frameworks.

07

Agreement Execution with NZ Legal Review

Execute the manufacturer-distributor contract with review by New Zealand-qualified legal counsel. NZ contract law (English common law basis, Contracts and Commercial Law Act 2017) is generally business-friendly with limited mandatory provisions, but Consumer Guarantees Act provisions for commercial goods and HSWA product supplier obligations require specific contractual treatment. Address dispute resolution, most NZ commercial agreements specify NZ courts or AMINZ (Arbitrators and Mediators Institute of New Zealand) arbitration. Review termination provisions, non-compete clauses, and force majeure provisions for NZ law enforceability.

08

Market Launch & Partner Enablement

A successful NZ launch requires specific enablement investment for the NZ market: joint customer visits to first target accounts within 60 days of agreement signing; co-development of NZ reference case studies from early installations (referrals travel fast in NZ’s small business community, one strong reference customer can unlock many others); SME Expo or FoodTech Packtech co-presence for market visibility; Callaghan grant application support for early adopter customers; and a clear service and spare parts commitment for regional NZ locations. New Zealand’s small, interconnected business community means that word-of-mouth from your first NZ reference customers carries disproportionate commercial weight, invest heavily in making early installations successful.

SECTION 10

10 Key Commercial Terms for New Zealand Partnerships

New Zealand commercial dynamics require specific adjustments to standard international distribution terms. NZ’s SME-dominated manufacturing base, relatively tight working capital environment, and Trans-Tasman commercial context create distinct commercial considerations.

Commercial Term

NZ-Specific Consideration

Reference Guide

NZD Pricing & Exchange Rate Risk

All NZ pricing is in NZD. The NZD can fluctuate significantly against USD and EUR, 10–20% annual swings are not uncommon. Structure annual price review mechanisms (NZD/USD rate bands) into your distribution agreement to address exchange rate movements systematically. NZ distributors cannot absorb unexplained mid-year price increases without contractual basis.

NZ GST (15%) applies to all domestic commercial transactions. If your overseas entity sells directly to a NZ buyer, the NZ buyer is the importer and pays GST on importation. Once a NZ entity exists, all domestic sales attract GST, ensure your invoicing and pricing structures correctly reflect GST from day one. NZ distributor agreements should specify whether prices are quoted exclusive of GST (standard practice for B2B).

Standard NZ commercial payment terms are 20th of month following invoice (approximately 30–50 days depending on invoice date). Larger manufacturers may push for 60 days. For new NZ distributor relationships, consider requesting advance payment or LC for first 2–3 orders before establishing open account credit. NZ company credit checks are available through commercial credit bureaux (Centrix, Illion NZ).

If you have both Australian and NZ distributors (or if one distributor covers both countries), define Trans-Tasman boundary conditions explicitly: can the NZ distributor sell to Australian customers? Can the Australian distributor sell into NZ? How are Trans-Tasman accounts handled? The CER agreement means goods can flow freely, unclear boundaries create channel conflict that is expensive to resolve after the fact.

Consider including Callaghan Innovation grant eligibility as a commercial tool, jointly identify which NZ customer automation projects qualify as eligible R&D under Callaghan’s definition, and support your distributor in helping customers apply. This effectively reduces the customer’s net acquisition cost by 20% without reducing your distributor margin. Document Callaghan-eligible application use cases in your NZ commercial materials.

Servicing automation equipment in regional NZ locations, Southland meat plants, Marlborough wineries, Bay of Plenty packhouses, involves significant travel time and cost. Define clearly in your agreement who bears regional service costs, what response time commitments apply, and how warranty travel costs are allocated. As with Australia, this is a recurring source of commercial dispute if not addressed explicitly at contract stage.

NZ SME sales cycles are typically 6–18 months for capital automation equipment. First-year minimums must be calibrated to NZ market realities, over-aggressive minimums that the distributor cannot realistically achieve create stress that damages the relationship before it has developed. Year 1 minimums should reflect a market development investment; performance thresholds in years 2–3 can ratchet up as reference installations are established and the pipeline matures.

If your NZ market entry involves any co-development with a NZ partner, university, or CRI, specify IP ownership provisions carefully, NZ universities and CRIs have their own IP commercialisation frameworks that may default to joint or institutional ownership of co-developed IP. Negotiate IP ownership terms before co-development work begins, not after. See IP ownership guide and tooling ownership.

New Zealand’s population of five million means absolute market volume is small, a successful NZ distributor may place 20–50 units annually of a mid-range automation system, not 200–500. If your business model requires high volume to be commercially viable, NZ should be positioned as a quality reference market alongside a larger regional strategy (Australia, APAC) rather than a standalone revenue target. Price point and margin strategy must reflect this reality.

💱

NZD Exchange Rate Volatility

The NZ dollar is a commodity-linked, relatively small currency that can experience 10–20% annual swings against major trading currencies. This directly affects the economics of NZD-priced, foreign-currency-sourced automation products. Build exchange rate risk management into your pricing strategy and distribution agreement from the outset, ad-hoc price increase requests destroy distributor trust.

🏘️

Small Business Community, Reputation Travels Fast

New Zealand’s manufacturing community is small and interconnected, engineering managers know each other at industry events, and word of mouth about supplier reliability travels extremely fast in both directions. A poorly supported first installation in the NZ market can reach dozens of potential customers within weeks. Conversely, a successful reference installation with enthusiastic customer advocacy can open an entire sector. Invest disproportionately in making your first NZ installations excellent.

🌊

Geographic Isolation & Spare Parts Lead Times

New Zealand’s geographic isolation from major manufacturing hubs means spare parts can take 5–15 business days to arrive from overseas, unacceptable for production-critical automation equipment in food processing or meat plants. Your NZ distributor must maintain adequate local spare parts inventory for your critical components. Define minimum spare parts holding requirements contractually and fund initial spare parts inventory as part of the market launch investment.

💻

Limited Local Technical Expertise Pool

New Zealand has a limited pool of automation engineers, and experienced integrators are in high demand. Your NZ distributor’s technical team may be smaller than you’d want, and turnover of key technical staff can significantly impact distributor capability. Build training programmes that develop your distributor’s team depth over time, and document your technology thoroughly enough that institutional knowledge is not lost with individual staff departures.

New Zealand has a strong sustainability culture, NZ manufacturers and their customers increasingly expect automation technology suppliers to demonstrate environmental credentials: energy efficiency, recyclable materials, reduced waste generation. Prepare sustainability documentation for your products (energy consumption data, lifecycle analysis, recyclability), NZ buyers, particularly in premium food sectors, may require this for procurement approval. This expectation is growing, not fading.

SECTION 12

12 How GTsetu Connects You with Verified NZ Partners

🇳🇿 GTsetu, Verified B2B Platform for New Zealand Market Entry

Discover Verified NZ Manufacturers & Distributors, No Broker Commission

GTsetu provides international manufacturing and industrial automation companies with direct access to compliance-verified New Zealand manufacturers, distributors, system integrators, and technology partners, across every industrial sector and all major New Zealand manufacturing regions. Every company in GTsetu’s NZ network has been verified through Companies Office (NZBN) registration, IRD/GST documentation, relevant industry certifications, and authority letter confirmation before appearing in the platform. You discover, qualify, and engage with verified NZ partners, without broker intermediaries taking a cut of your commercial economics.

🏛️

Multi-Layer Compliance Verification

Every NZ partner on GTsetu has been verified: Companies Office NZBN, IRD number, GST registration, relevant certifications, eliminating fraud risk and due diligence burden.

🕵️

Anonymous Discovery

Browse verified NZ partner profiles without revealing your identity. Protect your NZ market entry strategy until you choose to engage. Not possible via open directories or trade portals.

📄

Built-In NDA Workflow

Digital mutual NDA with timestamped signatures activated before sensitive technical or commercial data can be exchanged. NZ Privacy Act 2020-compliant data handling throughout.

🔐

Encrypted Document Workspace

AES-256 encryption at rest, TLS in transit. Role-based access controls. Full audit trail. NZ Privacy Act-aligned security baseline for all data exchange.

🚫

Zero Broker Commission

GTsetu charges zero commission on any partnership formed between international manufacturers and NZ distributors or partners. All commercial economics stay between you and your partner, always.

🌏

100+ Countries Including NZ & Australia

GTsetu’s verified network covers New Zealand and Australia together, enabling Trans-Tasman dual-market partner discovery from a single platform. Also supports expansion into India, Germany, and beyond.

QWhy should I expand my manufacturing or industrial automation business to New Zealand?

New Zealand offers a unique combination of market quality and business transparency that makes it an attractive entry point for international automation companies, despite its small population. It consistently ranks among the world’s top markets for ease of doing business, has no foreign ownership restrictions in manufacturing and technology sectors, and features a business community that values long-term supplier relationships over price-driven switching. The structural forces driving automation investment, minimum wages up 50%+ in a decade, persistent skilled trades shortages, export market food safety requirements, and Callaghan Innovation grant support, are durable and intensifying, not cyclical. New Zealand’s Trans-Tasman relationship with Australia under the CER agreement also enables companies to serve both markets from a shared regional distribution structure, effectively doubling the addressable market for companies already in or planning to enter Australia. See the broader context in our company global expansion guide and global collaboration examples.

QWhat are the best entry models for expanding an automation business to New Zealand?

For most international industrial automation companies, the recommended NZ entry sequence is: (1) First assess whether your existing Australian distributor (if applicable) can extend coverage to New Zealand, the CER agreement enables this commercially, and it avoids duplicating distribution costs in a small market. (2) If NZ-specific sector expertise is required (dairy, meat, marine, MedTech), appoint a dedicated NZ national distributor, fastest market access (3–9 months) with minimal capital. (3) After 2–3 years of validated NZ revenue, evaluate establishing a NZ Ltd for greater market control and Callaghan Innovation grant eligibility. NZ Ltd registration takes 1–3 business days with no minimum capital, one of the world’s simplest incorporation processes. Co-development partnerships with Crown Research Institutes (Plant & Food Research, AgResearch, Scion) are particularly valuable for companies targeting NZ primary industry sectors. See our complete analysis in market entry partnerships and licensing vs. distribution agreements.

QWhat is Callaghan Innovation and how does it benefit foreign manufacturers in New Zealand?

Callaghan Innovation is New Zealand’s government agency for business innovation, providing R&D grants, project co-funding, and technical expert access to NZ-incorporated companies. Its flagship R&D Growth Grant provides 20% of eligible R&D expenditure (minimum NZ$50,000 annual R&D spend) as a grant, reducing the effective cost of product adaptation, application development, and market-specific R&D. Foreign companies establishing a NZ Ltd and conducting qualifying R&D are fully eligible. For companies not yet meeting Growth Grant thresholds, the 15% R&D Tax Incentive (administered by IRD) provides an alternative pathway. Beyond direct grants, Callaghan’s most valuable role for international companies is as a demand signal and connection point, NZ manufacturers actively investing in R&D and accessing Callaghan grants are your highest-propensity automation buyers. Callaghan also offers project co-funding for collaborations with NZ universities and CRIs, which can offset the cost of developing NZ-specific product adaptations that unlock commercial sales. Contact Callaghan’s Business Development advisers (available nationwide) as part of your NZ market entry planning.

QWhich sectors in New Zealand have the highest industrial automation demand?

The sectors with the highest industrial automation demand in New Zealand in 2026 are: (1) Dairy and food processing, the largest NZ manufacturing sector; Fonterra, Synlait, and specialty dairy producers require high-hygiene processing automation, CIP/SIP, and quality inspection systems. (2) Meat processing and seafood, Silver Fern Farms, Alliance Group, and Sanford face persistent regional labour shortages driving carcass robotics and cold chain automation investment. (3) Horticulture and wine, Zespri kiwifruit packhouses and Marlborough wine producers require optical grading, packhouse automation, and palletising systems. (4) Medical technology, Medsafe-compliant assembly automation and quality inspection for a growing export-oriented sector. (5) Wood products and engineered timber, automated grading, CNC processing, and logistics for an industry with high regional labour constraints. (6) Marine manufacturing, Auckland’s superyacht industry requires composite fabrication automation and robotic finishing. (7) AgriTech, robotic milking, precision irrigation, and AI-driven primary industry applications. Waikato and Bay of Plenty (dairy, horticulture), Southland and Canterbury (meat), Auckland (marine, MedTech), and Marlborough (wine) are the priority geographic clusters for most automation companies.

QHow do I find a verified distributor for industrial automation products in New Zealand?

The most efficient route to finding a verified NZ industrial automation distributor is through GTsetu’s compliance-verified B2B platform, where every company has been verified through NZBN, IRD/GST registration, and industry certifications before appearing in the network, with anonymous discovery, built-in NDA workflow, and encrypted collaboration at zero broker commission. Supplement with trade show attendance at Southern Manufacturing & Electronics (SME Expo, Christchurch) and FoodTech Packtech (Auckland), the primary in-person events for NZ manufacturing. Engage NZTE for facilitated introductions and market intelligence. Contact EMA (Employers and Manufacturers Association) for member introductions in your target sector. Always verify candidates independently, NZBN at companiesoffice.govt.nz, GST at ird.govt.nz, before sharing product specifications or pricing. Consider also whether your Australian distributor (if applicable) can credibly extend NZ coverage as a Trans-Tasman arrangement before committing to a separate NZ-specific appointment. Review our finding international distributors and distributors and manufacturers frameworks.

QWhat commercial terms should I negotiate carefully in a NZ distribution agreement?

NZ-specific commercial terms requiring careful negotiation: (1) NZD pricing and exchange rate risk allocation, NZD can swing 10–20% annually against major currencies; define price review mechanisms explicitly. (2) Trans-Tasman boundary definition, if you have both Australian and NZ distributors, define which accounts, geographies, and online channels each can serve to avoid channel conflict. (3) Payment terms, standard NZ commercial terms are 20th of following month; start with advance payment for first transactions. (4) Callaghan grant positioning, define whether and how your distributor will position your products as Callaghan-eligible R&D investments for customers, and what support you will provide for grant applications. (5) Regional service coverage and spare parts holding, define minimum NZ stock levels and response time commitments for regional (non-Auckland/Christchurch) accounts. (6) Minimum purchase commitments calibrated to NZ SME market sales cycle realities, typically 6–18 months for first capital automation equipment sales. (7) IP ownership provisions for any co-development activities. See our complete guides on exclusivity clauses, termination clauses, business partnership contracts, and manufacturer-distributor contracts.

Ready to Expand Your Manufacturing Business to New Zealand?

Connect with verified New Zealand manufacturers, distributors, and technology partners on GTsetu, with compliance-backed verification, anonymous discovery, built-in NDA workflows, and zero broker commissions on every NZ market partnership you form.

They represents the product, and research team behind GTsetu, a global B2B collaboration platform built to help companies explore cross-border partnerships with clarity and trust. The team focuses on simplifying early-stage international business discovery by combining structured company profiles, verification-led access, and controlled collaboration workflows.

With a strong emphasis on trust, and disciplined engagement, Team GTsetu shares insights on global trade, partnerships, and cross-border collaboration, helping businesses make informed decisions before entering deeper commercial discussions.