How to Expand Your Manufacturing & Industrial Automation Business to Africa

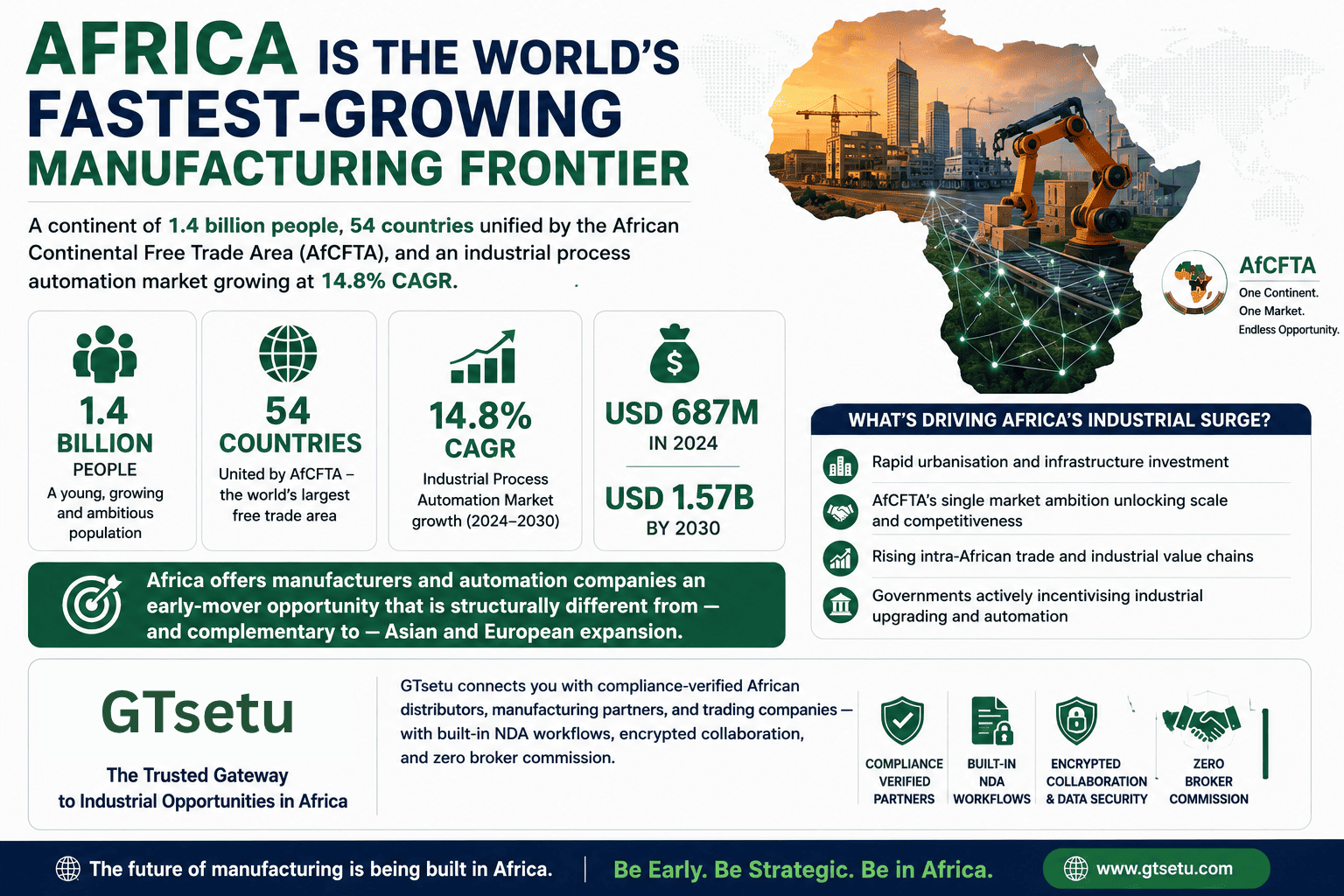

Direct Answer: Africa is the world’s fastest-growing manufacturing frontier, a continent of 1.4 billion people, 54 countries unified by the African Continental Free Trade Area (AfCFTA), and an industrial process automation market growing at 14.8% CAGR from USD 687 million in 2024 to USD 1.57 billion by 2030. Driven by rapid urbanisation, AfCFTA’s single market ambition, rising intra-African trade, and governments actively incentivising industrial upgrading, Africa offers manufacturers and automation companies an early-mover opportunity that is structurally different from, and complementary to, Asian and European expansion. GTsetu connects you with compliance-verified African distributors, manufacturing partners, and trading companies, with built-in NDA workflows, encrypted collaboration, and zero broker commission.

📅 June 2026⏱ 20 min read✍️ GT Setu Editorial Team🔄 Updated regularly

Africa’s industrial story is entering a new chapter. For decades the continent was viewed primarily as a source of raw materials, minerals, oil, agricultural commodities, exported with limited value addition. That model is changing, decisively and accelerating. Across North Africa, East Africa, West Africa, and Southern Africa, governments are pursuing ambitious industrialisation agendas, manufacturers are upgrading operations, and the world’s largest free trade agreement, the African Continental Free Trade Area (AfCFTA), is stitching together 54 countries into a single market of 1.4 billion people and USD 3.4 trillion in combined GDP.

For industrial automation companies and manufacturers, Africa presents something genuinely different from other expansion destinations: an early-mover market where automation penetration remains low, demand signals are accelerating rapidly, and the structural tailwinds, population growth, urbanisation, AfCFTA trade integration, and rising intra-African demand, are measured in decades, not quarters. This guide covers everything needed to make an informed Africa expansion decision: market sizing, the industry sectors driving automation adoption, the continent’s key manufacturing hubs, available entry modes, the regulatory landscape, and practical expansion steps. It also explains how GTsetu helps manufacturers and automation companies find and engage compliance-verified African partners, without the verification risk of unverified outreach.

🌍 Africa at a Glance

Population: ~1.4 billion (growing to ~2.5 billion by 2050). Combined GDP: USD 3.4 trillion across 54 AfCFTA member states. Manufacturing share of GDP: ~10–14% (below global average, creating structural growth potential). Key manufacturing sectors: agro-processing, food and beverage, mining and resources, oil and gas, textiles, pharmaceuticals, automotive assembly, FMCG. Major industrial hubs: South Africa (Southern), Egypt and Morocco (North), Nigeria and Ghana (West), Kenya and Ethiopia (East). Rockwell Automation, Schneider Electric, Siemens, ABB, and Honeywell all maintain active African operations.

SECTION 1

1 Why Africa for Manufacturing & Industrial Automation?

Africa’s manufacturing opportunity is often discussed in abstract terms, “the next frontier,” “the demographic dividend,” “the last large untapped market.” The commercial reality for automation companies is more specific: Africa has a continent-wide industrial modernisation agenda, a large and growing base of manufacturers who are operating legacy production infrastructure that urgently requires upgrade, and a political framework, AfCFTA, that is actively building the regulatory architecture for cross-border industrial trade at scale. The combination creates a structured, multi-decade demand profile that is neither speculative nor distant.

14.8%

Africa process automation market CAGR 2024–2030 (Next Move Strategy Consulting)

2.5B

Projected African population by 2050, the world’s largest consumer market in formation

$400B+

Projected global industrial automation market within the next decade, with Africa’s share growing

The Five Strategic Drivers

Driver

What It Means for Manufacturers & Automation Companies

Commercial Implication

AfCFTA, Africa’s Single Market

The African Continental Free Trade Area unifies 54 countries into a single market of 1.4 billion people and USD 3.4 trillion GDP. Phased tariff elimination on 90%+ of goods, harmonised rules of origin, and a services liberalisation protocol are progressively enabling manufacturers to produce in one African country and sell across the continent without the historic tariff barriers

Manufacturers establishing production in a strong AfCFTA hub, South Africa, Egypt, Morocco, Ethiopia, gain potential access to an integrated continental market. Automation companies can sell to manufacturers upgrading production to meet AfCFTA export standards

Industrial Modernisation Agenda

Governments across Africa are actively pursuing value-added manufacturing as a strategic priority, moving beyond raw material export toward processed goods, pharmaceuticals, electronics, and automotive components. National industrial policies in Nigeria, Kenya, South Africa, Egypt, Morocco, and Ethiopia explicitly target automation and Industry 4.0 adoption

Policy-driven procurement preferences, investment incentives (tax holidays, duty-free equipment imports), and special economic zones create structured, government-validated demand for automation technology and manufacturing FDI

Leapfrog Technology Adoption

Industry analysts and the ISS African Futures research programme note that Africa’s manufacturers have the opportunity to bypass legacy industrial systems entirely, adopting Industry 4.0 technologies from the outset rather than retrofitting around decades-old infrastructure. Smart sensors, cloud-based SCADA, predictive maintenance AI, and mobile-enabled production monitoring are being deployed directly in facilities that never had traditional automation

Cloud-native, IoT-first, mobile-accessible automation solutions have structural advantages in African markets over legacy on-premise systems. Companies that design for Africa’s connectivity environment, variable power, mobile-first, cost-optimised, compete more effectively than those porting developed-market solutions unchanged

Energy Efficiency Imperative

High and unreliable energy costs are among the most significant operational challenges for African manufacturers. As Schneider Electric’s East Africa Industry Business Leader documented, motors account for up to 60% of energy use in manufacturing environments, and variable speed drives with automated control can reduce this substantially. Energy-driven automation ROI is often faster in Africa than in lower-energy-cost markets

Energy efficiency automation, variable speed drives, predictive maintenance, automated load management, power monitoring, delivers measurable, rapid ROI for African manufacturers and represents a compelling commercial proposition independent of broader Industry 4.0 ambitions

Manufacturing Indaba & Growing Industry Ecosystem

Africa’s manufacturing industry event ecosystem is growing, Manufacturing Indaba 2026 (Johannesburg, July 2026) exemplifies the increasing sophistication of the continental manufacturing conversation, bringing together industry leaders, technology providers, policymakers, and investors to examine automation and Industry 4.0 solutions for African industrial development

A maturing industry ecosystem creates structured B2B engagement opportunities, industry events, technology showcase forums, and government-sponsored investment matchmaking programmes, that did not exist at scale a decade ago

💡 The Africa Early-Mover Advantage

Africa’s industrial automation market is at an earlier stage of development than Asia or Europe, which means the early-mover advantage for automation companies establishing brand recognition, distribution networks, and reference customer relationships is significantly more durable than in saturated markets. Rockwell Automation, Schneider Electric, Siemens, ABB, and Honeywell are all active in Africa, but the market is large, diverse, and fragmented enough that specialist automation companies, particularly those with Africa-adapted product configurations and service models, can build substantial market positions. See: technology partnership models for industrial sector expansion.

Africa’s industrial process automation market is one of the fastest-growing in the world by CAGR, driven by the intersection of industrial modernisation policy, AfCFTA trade integration, energy efficiency imperatives, and the growing capacity of African manufacturers to invest in productivity-enhancing technology. The 14.8% projected CAGR (2024–2030) is among the highest of any regional automation market globally, reflecting both the low starting base and the scale of the structural growth opportunity.

Market Metric

Value

Source / Period

Africa Industrial Process Automation Market Size

USD 687.2 million

2024 (Next Move Strategy Consulting)

Projected Market Size by 2030

USD 1,570.7 million (~USD 1.57 billion)

2030 projection (Next Move SC)

CAGR

14.8%

2024–2030 forecast period

Global Industrial Automation Market (10-year projection)

USD 400+ billion

Industry analysts (Manufacturing Indaba 2026 data)

Motor energy share in African manufacturing

Up to 60% of total energy consumption

Schneider Electric East Africa analysis, 2025

AfCFTA Single Market GDP

USD 3.4 trillion

African Union / AfCFTA Secretariat

African Population (2050 projection)

~2.5 billion

UN World Population Prospects 2024

Manufacturing share of African GDP

~10–14%

UNIDO / African Development Bank estimates

Key Growth Drivers in Detail

🤝

AfCFTA Manufacturing Integration

The African Continental Free Trade Area is the world’s largest free trade area by member count, and its progressive tariff elimination and rules of origin protocols are reshaping where and how manufacturers invest across the continent. Manufacturers producing in strong AfCFTA hub countries, South Africa, Egypt, Ethiopia, Morocco, can access a market of 1.4 billion consumers across 54 countries at preferential tariff rates. This is accelerating investment in production capacity and quality standards that require automation to achieve, creating structured automation demand in tandem with manufacturing FDI flows.

AfCFTA Driver

⚡

Energy Cost, Africa’s Unique Automation ROI Driver

Energy costs and reliability are among the defining operational challenges for African manufacturers, and automation delivers one of its most compelling ROIs in this context. Variable speed drives applied to motors (which account for up to 60% of energy use in manufacturing environments) deliver measurable energy savings from day one. Predictive maintenance automation prevents breakdowns that in Africa’s context can mean days of lost production while waiting for parts. Automated load management and smart power monitoring systems are being deployed across manufacturing facilities in South Africa, Nigeria, Kenya, and Egypt specifically to address energy cost and reliability challenges.

Energy ROI Driver

🚀

Technology Leapfrogging, Bypassing Legacy Systems

African manufacturers have a structural advantage that developed-market manufacturers do not: they are not encumbered by decades of legacy automation infrastructure that requires compatibility management. Many African production facilities are either greenfield or operating basic manual processes, meaning they can adopt cloud-native IIoT platforms, mobile-accessible SCADA systems, and AI-driven quality control from the outset, without the costly migration burden that constrains European and Asian automation upgrades. Digital twin technology, virtual reality training tools, and remote expert support platforms are already being deployed across East Africa to solve the skilled technician shortage challenge.

Leapfrog Advantage

🏭

Industry 4.0 Government Policy Across Key Markets

National industrial policies across Africa’s largest economies explicitly prioritise automation adoption and Industry 4.0 implementation. South Africa’s National Industrial Policy Framework, Egypt’s Industrial Development Strategy, Morocco’s Industrial Acceleration Plan, Ethiopia’s Manufacturing Industry Development Institute (MIDI) programme, and Kenya’s Big Four Agenda manufacturing pillar all incorporate smart factory and automation adoption targets with associated incentive packages. These policy frameworks are creating structured procurement demand, particularly among state-affiliated manufacturers and industrial zones, that responds to technology aligned with official government objectives.

Policy Driver

SECTION 3

3 Top Industry Sectors: Where Automation Demand Is Highest

Automation demand across Africa is sector-specific and regionally concentrated. The following eight sectors represent the highest-priority targets for industrial automation companies entering African markets, combining current adoption velocity, investment pipeline, government policy alignment, and structural demand fundamentals.

⛏️

Mining & Resources

Largest single automation segment; highest per-project spend

Africa holds approximately 30% of the world’s mineral reserves, gold, platinum, copper, cobalt, lithium, manganese, chromium, and iron ore. Mining operations across South Africa, DRC, Zambia, Ghana, Tanzania, and Guinea are among the world’s most significant by output. Safety regulations, labour productivity requirements, and the increasing depth of mining operations are driving adoption of process automation, remote monitoring, autonomous haulage, and predictive maintenance systems. Mining automation in Africa represents the single highest per-project automation spend on the continent.

Process ControlRemote MonitoringPredictive MaintenanceSafety Systems

Agriculture accounts for approximately 15% of African GDP and 60% of employment, but most agricultural commodities are exported raw, with limited value addition. AfCFTA is catalysing investment in agro-processing: grains, oilseeds, cocoa, coffee, cashews, fruits, and vegetables being processed into consumer goods for the continental market. Automated sorting, grading, cleaning, filling, and packaging systems for food-grade production are the primary automation investments being made by agro-processors from Morocco to Mozambique.

Africa’s fast-moving consumer goods sector, beverages, personal care, household products, packaged food, is one of the continent’s most dynamic manufacturing categories. Multinationals including Unilever, Nestlé, Procter & Gamble, Diageo, and AB InBev operate production facilities across Nigeria, South Africa, Kenya, Egypt, and Ghana. Domestic FMCG manufacturers are scaling up to compete with import goods under AfCFTA, driving investment in automated filling lines, packaging systems, labelling automation, and quality control infrastructure.

Filling LinesPackaging SystemsLabelling AutomationProduction MES

🛢️

Oil, Gas & Petrochemicals

Largest existing installed automation base; upgrade cycle underway

Africa’s oil and gas sector, Nigeria, Angola, Egypt, Libya, Algeria, Mozambique, Tanzania, has the continent’s largest existing automation installed base. Process automation (DCS, SCADA, flow metering, safety instrumented systems) is essential infrastructure for upstream, midstream, and downstream operations. Much of this installed base dates from the 1990s and 2000s and is due for technology refresh, creating a structured upgrade cycle. New LNG projects in Mozambique, Tanzania, and Senegal are bringing greenfield automation procurement to the continent.

The COVID-19 pandemic exposed Africa’s dependence on imported pharmaceuticals and created political and commercial momentum behind domestic pharmaceutical manufacturing capacity. The African Union’s Pharmaceutical Manufacturing Plan and country-level investments, Egypt’s pharmaceutical cluster, South Africa’s Aspen Pharmacare, Kenya’s pharmaceutical SEZ, Rwanda’s medical device manufacturing hub, are creating structured demand for GMP-compliant filling automation, environmental monitoring, serialisation, and quality control systems that meet WHO-GMP standards.

GMP Filling LinesSerialisationEnvironmental MonitoringQuality Systems

🚗

Automotive Assembly & Components

South Africa and Morocco anchor the continent’s automotive clusters

Africa’s automotive sector is anchored by two established manufacturing clusters: South Africa (Toyota, BMW, Mercedes-Benz, Volkswagen, Ford assembly operations exporting globally under AGOA and EU trade agreements) and Morocco (Renault, Stellantis, Hyundai under the Tanger Med industrial platform, exporting primarily to Europe). Both clusters are investing in automation upgrades to maintain export competitiveness. Kenya, Nigeria, and Ethiopia are developing nascent vehicle assembly capacity. EV assembly is a nascent but growing opportunity as AfCFTA creates demand for local EV production.

Body Assembly RobotsWelding AutomationPaint Shop SystemsQuality Inspection

Africa is experiencing a renewable energy investment boom, solar, wind, hydro, and increasingly green hydrogen, driven by abundant resources, falling technology costs, and energy access imperatives. South Africa’s REIPPPP programme, Egypt’s massive solar projects, Morocco’s Noor solar complex (one of the world’s largest), and Kenya’s geothermal capacity are creating demand for SCADA systems, energy management platforms, substation automation, and smart grid infrastructure. Off-grid solar manufacturing for the rural electrification market is also a significant emerging automation application.

East African cluster growing rapidly; AfCFTA opportunity

Ethiopia, Kenya, Tanzania, Rwanda, and Lesotho have attracted significant garment and textile manufacturing investment, supported by AGOA (African Growth and Opportunity Act) market access to the USA and competitive labour costs. Industrial parks in Addis Ababa (Hawassa Industrial Park) and Kigali are home to global fast fashion brands. As labour costs rise in East Africa’s textile clusters, automation of cutting, quality inspection, and packaging is becoming commercially viable, creating demand for modular automation solutions suited to the sector’s flexibility requirements.

Africa’s manufacturing landscape is not uniform, it is organised around regional clusters with distinct industrial strengths, regulatory environments, logistics infrastructure, and automation market maturity. Understanding which hub best aligns with your sector and commercial objectives is the foundation of an effective Africa expansion strategy.

🟡

North Africa, Egypt, Morocco, Tunisia, Algeria

Best for: Automotive, aerospace, electronics, pharmaceuticals, FMCG, oil and gas automation, EU export-oriented manufacturing. North Africa is Africa’s most industrially advanced region and the closest to European markets, a strategic advantage for manufacturers targeting both the African continental market and EU exports. Morocco hosts Europe-linked automotive clusters (Renault Tanger, Stellantis, 250+ automotive tier suppliers) and a growing aerospace sector, operating from Tanger Med, one of Africa’s most modern port and industrial platforms. Egypt is North Africa’s largest economy, a major pharmaceutical manufacturing hub, and home to one of Africa’s most developed industrial zone networks (SCZone, Suez Canal Economic Zone). Both countries have strong bilateral and multilateral trade agreements with the EU, making them attractive bases for automation companies serving European-standard export manufacturers. See also: expand manufacturing to Egypt for country-specific detail.

EU-Linked Manufacturing

🟢

West Africa, Nigeria, Ghana, Côte d’Ivoire, Senegal

Best for: FMCG, food processing, oil and gas, cement, packaging, consumer goods manufacturing. West Africa is home to Africa’s largest economy (Nigeria, GDP ~USD 500 billion), the continent’s largest consumer market, and significant oil and gas infrastructure. Nigeria is a major FMCG manufacturing base, Unilever, Nestlé, Dangote, and hundreds of domestic manufacturers produce for a domestic market of 220 million. Ghana offers West Africa’s most stable investment environment with functioning rule of law, a growing manufacturing sector, and specific incentives for agro-processing, pharmaceuticals, and light manufacturing. Côte d’Ivoire is the world’s largest cocoa producer and a growing agro-processing hub. Senegal’s Dakar Industrial Park and emerging oil and gas sector (Sangomar oil field) are creating new automation procurement opportunities.

Consumer & FMCG Hub

🔵

East Africa, Kenya, Ethiopia, Tanzania, Rwanda, Uganda

Best for: Agro-processing, textiles and garments, pharmaceuticals, light manufacturing, technology-enabled production. East Africa is the continent’s fastest-growing manufacturing region, attracting significant FDI in industrial parks and manufacturing SEZs. Ethiopia’s Hawassa Industrial Park (textiles and garments) and Kilinto Pharmaceutical Industrial Park are among Africa’s most modern manufacturing facilities. Kenya is East Africa’s most commercially sophisticated economy, home to a growing pharmaceutical manufacturing sector and the region’s logistics hub. Rwanda has built a distinctive reputation for ease of doing business and is a growing hub for medical device manufacturing and technology-enabled production. Schneider Electric, identified by name in East African automation case studies, is actively deploying solutions across the region to address energy efficiency and digital transformation needs.

Fastest-Growing Region

🟠

Southern Africa, South Africa, Zambia, Zimbabwe, Botswana, Mozambique

Best for: Automotive, mining, chemicals, energy, FMCG, the continent’s most sophisticated automation market.South Africa is Africa’s most industrially advanced economy and the continent’s largest automation market. Toyota, BMW, Mercedes-Benz, Volkswagen, and Ford operate assembly plants in the Eastern Cape and KwaZulu-Natal, producing vehicles for both domestic and export markets. South Africa’s mining sector, gold, platinum, iron ore, coal, manganese, is the continent’s largest consumer of process automation, predictive maintenance, and safety instrumented systems. South Africa’s well-developed infrastructure, established financial system, and sophisticated professional services ecosystem make it the natural regional headquarters for automation companies targeting Southern and Sub-Saharan Africa. See: expand manufacturing to South Africa for country-specific entry guidance.

Most Mature Automation Market

🟣

Central Africa, DRC, Cameroon, Republic of Congo

Best for: Mining automation, oil and gas process control, hydropower automation, resource processing. Central Africa hosts some of the world’s most significant mineral deposits, DRC’s cobalt (60%+ of global reserves), copper, coltan, and gold, alongside major oil and gas operations in Cameroon and the Republic of Congo. Automation demand is concentrated in resource extraction and processing, with significant hydropower infrastructure (DRC’s Inga Dam system has the potential to become Africa’s largest power generation project) requiring SCADA and grid automation. Market entry requires careful due diligence, local partnership structures, and patience, but the resource base creates long-term, high-value automation procurement opportunities that early entrants will be positioned to capture.

Resources & Mining

✅ Africa Hub Selection, Key Criteria

Selecting your primary Africa hub should assess: proximity to your target customer sectors; logistics infrastructure (port access, road network, air freight capacity); energy reliability (critical for precision manufacturing); rule of law and contract enforceability; language compatibility (English, French, Arabic, Portuguese); bilateral trade agreements (AGOA, EU agreements, AfCFTA preferential treatment); SEZ or industrial park incentive availability; and talent pool quality for technical and commercial roles. South Africa is the default regional headquarters choice for Sub-Saharan operations; Egypt for North Africa; Morocco for EU-linked manufacturing. Most companies use a hub-and-spoke model, establishing primary operations in one country and distributing across the region from there.

SECTION 5

5 Market Entry Modes for Manufacturers & Automation Companies

Africa’s regulatory diversity, 54 countries, each with distinct investment laws, company registration requirements, and trade frameworks, means that entry mode selection is closely tied to the specific countries being targeted. The modes below are applicable across the continent, though the specific implementation varies by country.

🏭

Local Manufacturing / Assembly Entity

Establish a wholly-owned or joint venture manufacturing or assembly operation in-country. Required for accessing industrial zone incentives, government procurement preferences, and local content requirements (particularly in oil and gas sectors in Nigeria, Angola, and Ghana). Most appropriate for companies with sufficient scale to justify the investment. Best entry point: South Africa, Egypt, Morocco, or Ethiopia.

High Control / Capital Required

🤝

Joint Venture with Local Partner

Partnership with an established African company, providing local market navigation, government relationships, and customer access while the foreign party brings technology, capital, or international market access. JVs are particularly valuable for navigating state-owned enterprise procurement, government tender processes, and local content requirements in resource sector automation. Requires careful JV vs. strategic alliance analysis and robust agreement structuring.

Shared Control / Local Access

🚚

Distribution Partnership

Appoint a verified African distributor or trading company to sell your automation products across one or more countries, without direct establishment. Fastest route to market revenue; zero capital requirement; suitable for automation equipment and solutions companies wanting commercial presence without operational commitment. GTsetu provides pre-verified African distributors with confirmed trade licences and sector capabilities. See: find international distributors and distribution agreement templates.

Fastest / Zero Capital

📋

Contract / Toll Manufacturing

Engage an African manufacturer to produce goods to your specification, lower capital requirement, faster market access, and useful for testing demand before committing to direct investment. Africa’s contract manufacturing ecosystem is most developed in South Africa, Egypt, Morocco, and Nigeria. Requires careful IP and quality control structuring. See: contract manufacturing and toll manufacturing guides.

Flexible / Lower Capital

🏢

Representative Office

Establish a market research and relationship-building presence, no commercial production or sales permitted. Appropriate for the initial 12–24 months of market exploration before committing to full investment. Useful for mapping customer relationships, regulatory requirements, and competitive landscape before allocating capital. Most practical in South Africa, Kenya, Egypt, or Nigeria due to professional services ecosystem depth.

Low Cost / No Revenue

🔬

Technology Licensing

License your manufacturing process or automation technology to an African partner who produces and sells using your technology, earning royalties without operational involvement. Suitable where your competitive advantage is technology IP rather than manufacturing capability. Requires robust technology transfer agreements and comprehensive IP protection provisions. See: licensing vs. distribution agreements.

IP-Based / Royalty Revenue

🔗

Co-Development Partnership

Partner with an African company to jointly develop products or solutions adapted for African market requirements, particularly valuable for IIoT, remote monitoring, and off-grid automation solutions where local market knowledge is essential to product-market fit. See: co-development partnerships and white label vs. private label manufacturing.

Innovation-Led Entry

🌐

Project-Based / Tender Entry

Bid directly for government, mining, or energy sector automation projects, either directly or through local agent partners. Common first entry mode for process automation companies targeting mining, oil and gas, or energy infrastructure projects. Requires registration with relevant procurement bodies in each country. Understanding local content requirements and procurement agent regulations is critical. See: international business development consulting.

Project-Based Revenue

⚡ Fastest Route to African Market Revenue for Automation Companies

For industrial automation companies that want to generate African market revenue within 3–6 months without establishing a legal entity, the Distribution Partnership route, appointing a compliance-verified, technically capable local distributor, is the commercially optimal starting point across most African countries. GTsetu pre-verifies African distributors against official business registry records, trade licences, and relevant technical certifications, giving automation companies confidence their partner can legitimately represent their products. See: market entry partnership structures and building a distributor network.

SECTION 6

6 Regulatory Framework: AfCFTA, FDI & Operating in Africa

Africa’s regulatory environment is diverse and country-specific, there is no single pan-African regulatory framework for manufacturing investment equivalent to the EU single market, though AfCFTA is progressively building towards this. The following covers the key cross-cutting frameworks and highlights country-specific considerations for the major manufacturing hubs.

Regulatory Framework

Description

Key Consideration for Manufacturers

AfCFTA, African Continental Free Trade Area

The AfCFTA agreement, fully operational since 2021, provides phased tariff elimination on 90% of goods across 54 member states, progressive services liberalisation, and harmonised rules of origin. The protocol on investment, intellectual property, competition policy, and e-commerce are in varying stages of negotiation and implementation

Rules of origin determine whether your products qualify for AfCFTA preferential tariff treatment when traded between member states. Verify whether your product’s value-addition in the manufacturing country satisfies AfCFTA rules of origin before designing your production strategy. Rules of origin requirements vary by product category

Investment Registration, by Country

Each African country has its own FDI registration process. South Africa: Companies and Intellectual Property Commission (CIPC) registration. Egypt: General Authority for Investment and Free Zones (GAFI). Nigeria: Corporate Affairs Commission (CAC) plus sector-specific approvals. Kenya: Business Registration Service (BRS). Morocco: Regional Investment Centres (CRI) plus AMDIE

Timeline ranges from 3 days (Rwanda, ranked top in Africa for ease of doing business) to 60+ days for complex sector-specific approvals. Engage a locally registered legal or corporate services firm in each country of operation. Do not rely on online registration portals alone, in-country support significantly reduces processing time and error risk

Industrial Zone & SEZ Incentives

All major African manufacturing hubs operate industrial zones or special economic zones with preferential tax and customs treatment: South Africa (IDZs, Industrial Development Zones); Egypt (SCZone, Suez Canal Economic Zone); Morocco (Free Zones including Tanger Free Zone); Ethiopia (Industrial Parks, Hawassa, Bole Lemi, Kilinto); Kenya (Export Processing Zones and Special Economic Zones); Nigeria (Free Trade Zones)

SEZ and industrial zone companies typically receive: corporate income tax holidays (5–20 years depending on country and zone); customs duty exemptions on capital equipment and production inputs; streamlined import/export procedures; and in some cases, subsidised land and utilities. Qualification requirements vary, most require minimum investment thresholds and employment creation commitments

Local Content Requirements

Several African countries mandate local content in specific sectors. Nigeria’s Local Content Act requires specific percentages of Nigerian goods and services in oil and gas projects. Angola has similar requirements. South Africa has B-BBEE (Broad-Based Black Economic Empowerment) compliance requirements affecting procurement preferences and operating licences

Local content and B-BBEE compliance are commercial prerequisites, not optional, for accessing major procurement opportunities in South Africa’s mining, automotive, and energy sectors, and for oil and gas projects in Nigeria and Angola. Factor compliance costs into market entry planning from the outset. Engage local legal counsel with sector-specific expertise

Product Standards & Certification

Electrical and electronic products sold in South Africa require SABS (South African Bureau of Standards) certification or LoA (Letter of Authority) from NRCS. Egypt requires EOS (Egyptian Organisation for Standardisation) certification for regulated products. Many African countries accept CE marking for EU-origin products in practice, but formal certification requirements vary

South Africa has the most developed product certification framework on the continent. For most other African markets, CE or IEC certification provides a practical baseline, though country-specific approvals may be required for regulated product categories. Engage a South Africa-registered certification agent as a starting point for Southern and East Africa market access

Foreign Exchange & Repatriation

Foreign exchange controls and profit repatriation restrictions vary significantly. South Africa has exchange control regulations (SARB oversight); Nigeria has periodic foreign exchange availability challenges that affect import payment capacity; Egypt has had USD liquidity constraints. East African markets (Kenya, Rwanda, Tanzania) generally have more open foreign exchange environments

Structure commercial terms with African distributors and partners to manage FX risk explicitly. USD or EUR-denominated contracts, advance payment or LC payment terms (see: advance payment vs. LC vs. open account), and explicit force majeure provisions for FX controls are standard risk management measures for Africa-specific commercial agreements. See: force majeure in global trade

Dispute Resolution

Judicial enforcement of commercial contracts varies significantly across Africa. South Africa has a well-functioning commercial court system. OHADA (Organisation for the Harmonisation of Business Law in Africa) provides a harmonised commercial law framework for 17 Francophone West and Central African countries. CIETAC Africa, ICSID arbitration, and LCIA are all used for international commercial dispute resolution across the continent

Specify international arbitration as the dispute resolution mechanism in all commercial agreements with African partners, LCIA (London), ICC (Paris), or KIAC (Kigali Arbitration Centre for East Africa). Avoid reliance on domestic courts alone for enforcement. Include governing law clauses explicitly. See: dispute resolution in international contracts

🌍 Key Africa Investment Incentives for Automation & Manufacturing

Industrial zone and SEZ investors across Africa’s major manufacturing hubs receive varying combinations of: Corporate income tax holidays (5–20 years, country-dependent); customs duty exemptions on capital equipment and production inputs; VAT relief on qualifying manufacturing imports; subsidised industrial land in government-developed industrial parks; streamlined work permit processing for technical and management staff; and export incentives where products are destined for markets outside the host country. Ethiopia’s industrial parks offer among the most competitive incentive packages on the continent for export-oriented manufacturing; Morocco’s free zones offer EU-proximity advantages; South Africa’s IDZs provide the continent’s most sophisticated infrastructure and skills base.

SECTION 7

7 Challenges & How to Mitigate Them

Africa’s manufacturing and automation opportunity is real and large, but the operational challenges are also real and require honest assessment and specific mitigation strategies. The following are the most significant challenges for foreign manufacturers and automation companies.

Challenge

Specifics for Automation & Manufacturing Companies

Mitigation Strategy

Energy Reliability & Infrastructure Gaps

Unreliable power supply is the single most commonly cited operational challenge for manufacturers across Sub-Saharan Africa. South Africa’s load-shedding programme, Nigeria’s grid reliability issues, and variable supply across many markets directly affect production continuity and automation system viability

Design automation solutions with power resilience built in, UPS systems, DC bus automation architectures, energy storage integration, and automatic power quality monitoring. Products specifically adapted for African power environments (wide voltage tolerance, surge protection, graceful degradation) have significant competitive advantage over products designed for stable European power grids. Variable speed drives for energy efficiency serve dual purpose as energy cost reduction AND power quality management

Skilled Technician Shortage

A shortage of trained automation technicians, PLC programmers, instrumentation engineers, SCADA administrators, is consistently identified as a barrier to automation adoption across East, West, and Central Africa. As CIO Africa’s analysis notes, digital tools now enable remote expert support and virtual reality training, but the skills gap remains a real adoption barrier

Build training and skills development as a product offering, not an afterthought. Partner with African universities (University of Pretoria, University of Nairobi, Cairo University, University of Lagos) for automation skills pipeline development. Offer remote monitoring and managed service models where your team provides ongoing technical support. VR training tools for technician upskilling are gaining traction across the region. See: technology partnership models for skills transfer

Regulatory Complexity & Multi-Country Diversity

Operating across multiple African countries means navigating 54 different regulatory frameworks, investment laws, product certification requirements, import duties, labour laws, and tax structures that differ significantly between countries and can change without consistent notice

Use a hub-and-spoke market approach: establish primary operations in one strong hub country (South Africa for Southern/Sub-Saharan Africa, Egypt for North Africa, Kenya for East Africa, Nigeria or Ghana for West Africa) and expand regionally from there. Engage local legal and regulatory counsel in each hub. See: risk allocation in cross-border deals

Capital Sensitivity of SME Manufacturers

The majority of African manufacturers are SMEs, often family-owned businesses with limited access to credit financing for capital equipment. High upfront automation costs are the primary barrier to adoption among this segment, which constitutes the majority of potential customers across most African markets

Develop Africa-appropriate commercial models: equipment financing partnerships with African DFIs (Development Finance Institutions, DEG, Proparco, IFC, CDC); lease-to-own or pay-per-use pricing; modular automation that allows incremental adoption starting at lower capital commitment; outcome-based contracts with ROI demonstration. Government subsidy programmes for SME automation in South Africa (IDC), Egypt (ITIDA), and Kenya (IFC-supported programmes) can co-fund qualifying investments. See: pricing structures and volume commitment models

Logistics & Supply Chain Reliability

Customs clearance delays, port congestion (Lagos, Mombasa), landlocked country logistics costs, and last-mile infrastructure limitations affect product delivery timelines and spare parts availability, critical issues for automation companies whose customers depend on rapid technical support

Build Africa-specific inventory and spare parts management strategies, regional spare parts warehouses in hub cities, bonded warehouse structures for efficient customs clearance, and local stocking distributors with minimum inventory commitments. Define Incoterms and lead time management in commercial agreements explicitly

Partner Verification Risk

Cold outreach to potential African distributors or manufacturing partners exposes companies to identity fraud, business registration misrepresentation, and competitive intelligence leakage, risks that are amplified in markets where formal verification infrastructure is less developed

Use GTsetu’s compliance-verified partner network, every African company on the platform has been verified against official business registries, trade licences, and relevant certifications before engagement. Execute built-in NDA workflows before sharing any pricing or product specifications. See: business verification, partnership evaluation criteria, and B2B secure collaboration

SECTION 8

8 Step-by-Step Expansion Process

Expanding a manufacturing or industrial automation business into Africa requires a structured, phased approach. The steps below apply whether you are entering through a distribution partnership, establishing a direct legal entity, or pursuing project-based market entry.

01

Africa Market Assessment & Hub Selection

Begin with a structured market assessment: which African regions and countries have the highest concentration of your target customer segments? Which hub country provides the best combination of market access, logistics infrastructure, regulatory environment, and incentive package for your specific sector? Assess the competitive landscape, which of Schneider Electric, Rockwell Automation, ABB, Siemens, and Honeywell are active in your target sector and geography, and where are the gaps? Quantify your realistic total addressable market within 3 years per hub. See: global expansion analysis and global collaboration examples.

02

Africa-Specific Product & Commercial Model Adaptation

Before entering African markets, assess whether your products and commercial models require Africa-specific adaptation: power resilience (wide voltage tolerance, UPS compatibility, graceful power-loss degradation); connectivity resilience (offline-capable IIoT systems, low-bandwidth SCADA options, mobile-first interfaces); language localisation (English, French, Arabic, Portuguese, Swahili depending on target market); and pricing models (financing partnership compatibility, modular adoption paths, SME-accessible entry points). Products not adapted for African operational environments will underperform relative to their technical capabilities. See: MOQ planning for initial market batches.

03

IP Protection Before Any Disclosure

Implement IP protection before sharing any technical information with African partners. Register trademarks in your priority hub countries, South Africa (CIPC), Egypt (EGPO), Nigeria (FIPO), Kenya (KIPI), Morocco (OMPIC), and through ARIPO (African Regional Intellectual Property Organisation) for Eastern and Southern Africa, or OAPI for Francophone West and Central Africa. Execute mutual NDAs before any technical disclosure. Use GTsetu’s built-in NDA workflow and encrypted document exchange for pre-contract information sharing. See: IP ownership in manufacturing and non-compete vs. non-circumvention.

04

Verified Partner Discovery

Identify and verify your African distribution, manufacturing, or technology partners before any commercial engagement. Use GTsetu’s compliance-verified platform to browse pre-vetted African companies by sector and capability, with anonymous discovery protecting your market entry strategy. Verify business registration, import licences, technical capability, and financial standing before committing. Reference-check with existing customers. See: business verification, partnership evaluation criteria, and our guide on finding international distributors.

05

Entry Mode Execution & Legal Entity (If Required)

Execute your chosen entry mode. For distribution partnerships: engage GTsetu to identify and verify African distributors; execute a comprehensive distribution agreement with explicit territory rights, exclusivity terms, and performance milestones. For legal entity establishment: engage a locally-registered corporate services firm in your hub country; complete FDI registration (CIPC, GAFI, CAC, BRS depending on country); apply for SEZ or industrial zone status if applicable; complete tax registration; open local banking. Timeline: 2 weeks (Rwanda) to 3 months (Nigeria, Angola) depending on country and sector.

06

Product Certification & Regulatory Compliance

Complete product certification requirements in your hub country: South Africa (SABS/NRCS LoA for electrical equipment); Egypt (EOS); Nigeria (NAFDAC for regulated products, SON for standards). For most other African markets, CE and IEC certification provides a working baseline, but verify country-specific import requirements before shipping. Engage a South Africa-registered certification agent as a starting point for pan-African certification strategy. Concurrent with product certification: complete import/export licensing, verify HS code tariff classifications under AfCFTA rules, and confirm whether your products qualify for duty-free treatment in your target markets.

07

Commercial Agreement Execution

Execute commercial agreements with African partners with careful attention to Africa-specific risk provisions: force majeure clauses for power outages, currency controls, and political risk; USD or EUR denomination to manage FX volatility; payment terms appropriate for African credit environments (LC or advance payment for new relationships); international arbitration as dispute resolution mechanism; and termination provisions with clear performance triggers. Have agreements reviewed by legal counsel in both your home jurisdiction and the hub country. See: business partnership contract structuring.

08

Go-to-Market & Ecosystem Engagement

Launch commercial operations: exhibit at Africa’s major industrial events (Manufacturing Indaba, Johannesburg; Agrifex, Nairobi; Nigeria Industrial Fair, Lagos; Cairo Industrial Fair; Mining Indaba, Cape Town); register on African B2B platforms and government supplier databases; develop local-language product collateral; build relationships with industry associations (South African Institute of Electrical Engineers, Automation Society of South Africa, Nigerian Society of Engineers). Connect with GTsetu’s B2B business network for verified lead generation. See: top places to find B2B leads and international wholesale distributors.

09

Service Localisation, Training & Regional Scale

As operations mature: build local technical support capability (rapid response time is a critical competitive differentiator for automation companies in Africa); establish regional spare parts warehousing in hub cities; develop skills training programmes in partnership with local universities and technical colleges; expand your distributor network to secondary African markets from your hub base; evaluate AfCFTA preferential origin qualification for products manufactured in your hub; consider expanding your supply chain partner network for local component sourcing; review cross-border business partnership structures as regional scale justifies deeper investment.

SECTION 9

9 How GTsetu Connects You with Verified African Partners

The most commercially productive route to African markets for manufacturers and industrial automation companies is through verified local partners, distributors with active trade relationships, manufacturing partners with proven capability, and system integrators with relevant technical credentials. Africa’s B2B landscape presents a unique verification challenge: business registration databases are less centralised than in Asia or Europe, trade licence verification requires country-by-country expertise, and cold outreach carries elevated fraud and misrepresentation risk. GTsetu pre-verifies every African company on the platform against official business registries, trade licences, and relevant certifications, so your commercial engagement starts from verified confidence.

🏛️

Multi-Country Verification

Every African company verified against official business registries (CIPC, GAFI, CAC, BRS and equivalents), trade licences, and certifications, eliminating identity fraud and credential misrepresentation risk across 54 African countries.

🕵️

Anonymous Discovery

Browse African partner profiles by sector and capability without revealing your market entry strategy, protecting competitive intelligence during your evaluation phase.

📄

Built-In NDA Workflow

Mutual NDA with digital signatures and full audit trail, executed before any pricing, product data, or IP is shared with an African partner candidate.

🔐

Encrypted Document Exchange

Technical specifications, product data sheets, and commercial proposals exchanged in AES-256 encrypted workspace, no unprotected email attachments or exposed cloud links.

🌍

100+ Countries Including Africa

Active network of verified manufacturers, distributors, and suppliers across Africa and 100+ countries, supporting your complete global partner strategy from a single platform.

🚫

Zero Commission

GTsetu takes no success fee on any partnership formed. Your deal economics with your African partner stay entirely between the two parties, no broker margin to factor in.

Africa’s B2B landscape presents elevated partner verification challenges relative to more centralised registry systems in Asia or Europe. Business registration fraud, licence misrepresentation, and identity impersonation are more prevalent in markets where verification infrastructure is less developed, and the consequences of partnering with an unverified entity (IP exposure, commercial non-performance, regulatory liability) are amplified in markets where legal enforcement is more complex. GTsetu’s multi-country verification infrastructure addresses this challenge directly, giving automation companies and manufacturers the confidence to engage African partners commercially without the delays and costs of building their own verification capability. See: supplier collaboration platforms and B2B secure collaboration.

🌏 Explore Other Manufacturing & Automation Expansion Destinations

Q Why is Africa a compelling destination for manufacturing and industrial automation expansion?

Africa presents a unique combination of structural advantages: a population of 1.4 billion growing to 2.5 billion by 2050, a rapidly urbanising middle class, the AfCFTA creating a single market of USD 3.4 trillion GDP across 54 countries, significant natural resource wealth, and governments actively incentivising industrialisation and automation adoption. Africa’s manufacturing sector currently accounts for approximately 10–14% of GDP, below the global average, which represents substantial structural growth potential as AfCFTA trade integration, industrial policy frameworks, and rising consumer demand drive manufacturing investment. For automation companies, the combination of a low penetration starting point, 14.8% CAGR growth, and the energy efficiency ROI driver that is uniquely compelling in African operating environments makes the continent one of the most commercially attractive automation expansion destinations in the world.

Q How large is Africa’s industrial automation market?

Africa’s industrial process automation market was valued at USD 687.2 million in 2024 and is projected to grow at a CAGR of 14.8% to reach USD 1,570.7 million (approximately USD 1.57 billion) by 2030, according to Next Move Strategy Consulting. The broader global industrial automation market is expected to exceed USD 400 billion within the next decade, with Africa’s share growing as AfCFTA accelerates manufacturing investment. The market’s 14.8% CAGR is among the highest of any regional automation market globally, reflecting both the low starting base and the scale of the structural growth opportunity. Key demand sectors are mining and resources, oil and gas, food and beverage processing, FMCG, pharmaceuticals, automotive assembly, and renewable energy.

Q Which African countries are the best entry points for manufacturing expansion?

The top African entry points depend on your target sector. South Africa is the default hub for Sub-Saharan Africa, it has the continent’s most sophisticated industrial base, strongest professional services ecosystem, and largest existing automation market; see our dedicated guide to expand manufacturing to South Africa. Egypt is North Africa’s premier manufacturing and FDI hub, with the Suez Canal Economic Zone (SCZone) offering world-class industrial infrastructure; see expand manufacturing to Egypt. Morocco is the leading hub for EU-linked automotive and aerospace manufacturing. Kenya and Ethiopia are East Africa’s fastest-growing manufacturing economies. Nigeria offers access to West Africa’s largest consumer market. Most companies adopt a hub-and-spoke approach, establishing primary operations in one country and distributing regionally from there.

Q What is AfCFTA and how does it affect manufacturing expansion into Africa?

The African Continental Free Trade Area (AfCFTA) is the world’s largest free trade agreement by number of participating countries, 54 African Union member states covering a combined GDP of USD 3.4 trillion and 1.4 billion people. Fully operational since January 2021, AfCFTA is progressively eliminating tariffs on 90% of goods traded between member states, harmonising rules of origin, liberalising services trade, and creating a continental investment framework. For manufacturers, AfCFTA means that producing in one African country, South Africa, Egypt, Ethiopia, Morocco, can provide preferential tariff access to the broader African market, making manufacturing FDI in Africa far more commercially viable than when each country represented a separate, tariff-divided market. For automation companies, AfCFTA is accelerating manufacturing investment across the continent, creating new factory installations, production quality upgrades, and export-standard production requirements that all drive automation demand.

Q What are the biggest challenges for industrial automation companies expanding into Africa?

The primary challenges are: energy reliability and infrastructure gaps (unreliable power supply requires automation products specifically designed for African power environments); shortage of skilled automation technicians (PLC programmers, instrumentation engineers) requiring companies to build training as part of their service offering; regulatory complexity and diversity across 54 countries requiring a hub-and-spoke country strategy; capital sensitivity of SME manufacturers requiring flexible commercial models (financing, leasing, modular adoption); logistics and supply chain reliability affecting spare parts availability and service response times; and partner verification risk in markets where formal verification infrastructure is less developed than in Asia or Europe. GTsetu addresses the verification and IP protection challenges through compliance-verified partner discovery with built-in NDA workflows, encrypted document exchange, and country-by-country business registry verification.

Q How does GTsetu help manufacturers and automation companies expand into Africa?

GTsetu connects manufacturers and industrial automation companies with compliance-verified African distributors, local manufacturing partners, and trading companies, across South Africa, Egypt, Nigeria, Kenya, Morocco, Ghana, Ethiopia, and throughout the continent. Every African company on GTsetu has been verified against official business registries, trade licences, and relevant certifications before they can engage on the platform, eliminating the identity fraud and misrepresentation risk that is elevated in markets where centralised verification infrastructure is less developed. Anonymous discovery protects your market entry strategy while you evaluate potential partners. Built-in NDA workflows ensure your pricing, product specifications, and commercial terms are contractually protected before any information is shared. All document exchange happens in an encrypted workspace. And unlike broker-mediated introductions or commission-based trade platforms, GTsetu charges zero commission on any partnership formed.

Find Verified African Manufacturing & Distribution Partners on GTsetu

Join 500+ verified manufacturers, distributors, and automation companies building international trade partnerships on GTsetu, with compliance-verified African partner profiles across South Africa, Egypt, Nigeria, Kenya, Morocco, Ghana, Ethiopia, and beyond. Built-in NDA workflows, encrypted document exchange, and zero broker commission.

They represents the product, and research team behind GTsetu, a global B2B collaboration platform built to help companies explore cross-border partnerships with clarity and trust. The team focuses on simplifying early-stage international business discovery by combining structured company profiles, verification-led access, and controlled collaboration workflows.

With a strong emphasis on trust, and disciplined engagement, Team GTsetu shares insights on global trade, partnerships, and cross-border collaboration, helping businesses make informed decisions before entering deeper commercial discussions.