How to Expand Your Manufacturing & Industrial Automation Business to Germany

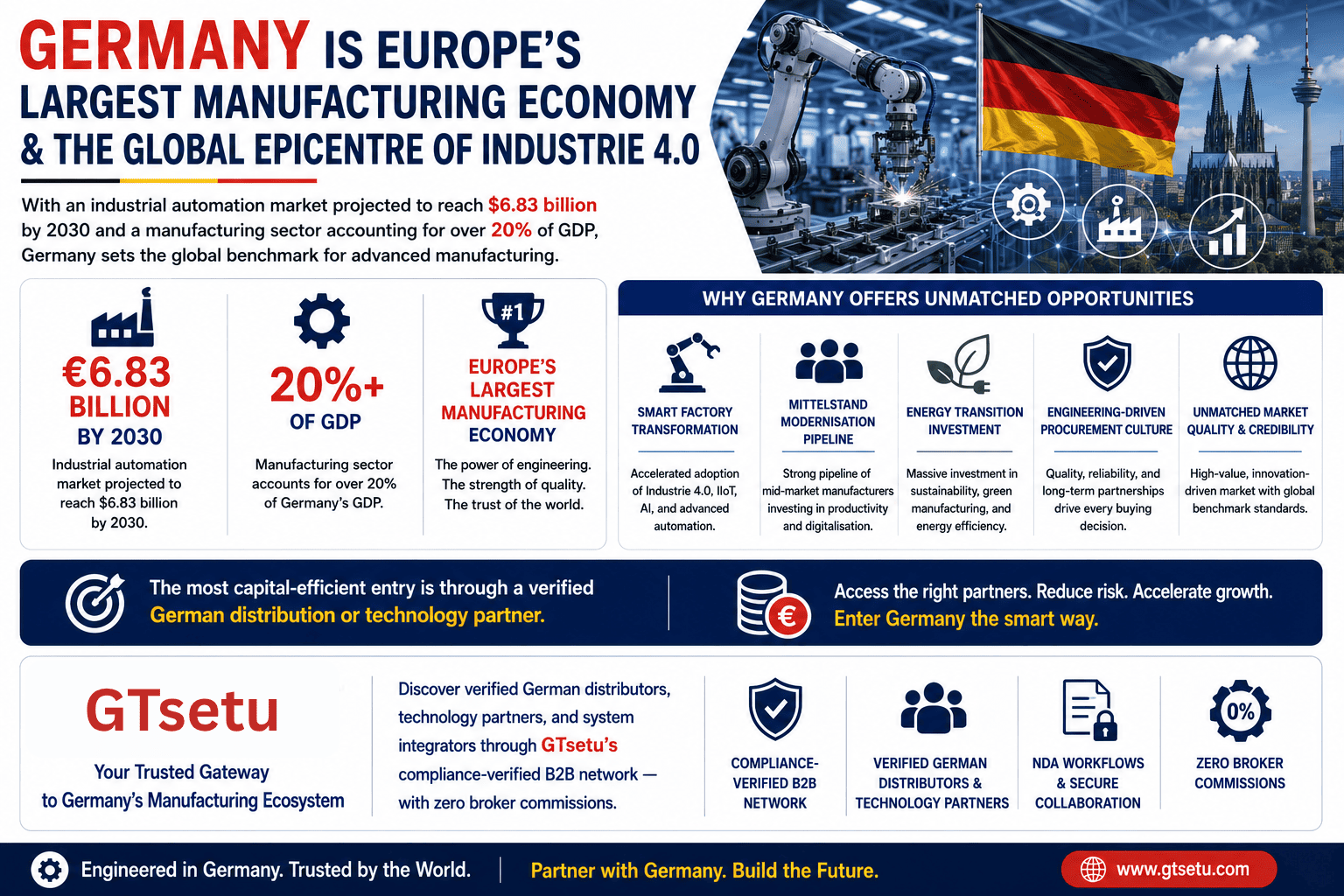

Direct Answer: Germany is Europe’s largest manufacturing economy and the global epicentre of Industrie 4.0, with an industrial automation market projected to reach $6.83 billion by 2030 and a manufacturing sector accounting for over 20% of GDP. Driven by smart factory transformation, the Mittelstand modernisation pipeline, energy transition investment, and a uniquely engineering-driven procurement culture, Germany offers unmatched market quality and credibility for international automation companies. The most capital-efficient entry is through a verified German distribution or technology partner, discoverable through GTsetu‘s compliance-verified B2B network with zero broker commissions.

📅 April 5, 2026⏱ 22 min read✍️ GT Setu Editorial Team🔄 Updated regularly

$6.8B+

Germany Automation Market by 2030

3.85%

CAGR 2024–2030 (Process Automation)

3.5M

Mittelstand Companies, Primary Buyers

0%

GTsetu Broker Commission

Germany occupies a unique position in global manufacturing and industrial automation: it is simultaneously Europe’s largest economy, the world’s third-largest exporter of manufactured goods, and the country that gave the world Industrie 4.0, the conceptual and policy framework that has defined the global smart factory transformation movement for the past decade. For international manufacturers, industrial automation OEMs, robotics companies, sensor and control system providers, and technology integrators, Germany in 2026 represents not just a large addressable market, but the most strategically important European market to establish presence in, both for the direct revenue opportunity and for the credibility and reference that a German market presence conveys globally.

But Germany’s market is also one of the most demanding in the world. German industrial buyers are technically sophisticated, standards-driven, and relationship-oriented in ways that require specific commercial and cultural adaptation from international companies. CE marking, GDPR compliance, the nuances of distributing through Germany’s Handelsvertreter (commercial agent) framework, and the patience required to build trust within the Mittelstand procurement culture all require careful navigation. This guide covers every dimension, from market sizing and sector opportunity to regulatory requirements, partner qualification, commercial terms, and the step-by-step roadmap for a successful Germany market entry. You can also explore our guides on advantages and disadvantages of global expansion and international business development consulting for broader strategic context.

🇩🇪 Who Is This Guide For?

This guide is written for international manufacturers, industrial automation OEMs, robotics and control system providers, technology integrators, and industrial equipment companies seeking to enter or expand in the German market, whether through a distributor partnership, technology licensing, joint venture, or direct establishment. It is equally relevant for companies already selling into Germany informally who want to formalise their European presence. If you are exploring other European or global markets alongside Germany, see our country guides: Poland, Romania, United Kingdom, India, and Vietnam.

SECTION 1

1 Why Germany for Manufacturing & Industrial Automation?

🎯 The Strategic Case

Germany is the country that invented the concept of the modern factory, and is now leading the world’s reinvention of it through Industrie 4.0. For industrial automation companies, a German presence delivers three compounding advantages simultaneously: direct revenue from Europe’s most technically demanding and highest-value industrial buyers; the credibility boost of a “made for German manufacturing” reference that accelerates sales across Europe and globally; and proximity to the technical standards bodies, research institutions, and innovation ecosystem that define the future direction of industrial automation worldwide.

20%+

Manufacturing as share of German GDP, the highest of any major EU economy and more than double the UK or France

80%+

German industrial companies that have initiated or completed Industrie 4.0 transformation projects, the highest adoption rate globally

#1

Global ranking for industrial robot density per 10,000 manufacturing employees (alongside Japan and South Korea), highest in Europe

🏭

Europe’s Manufacturing Core

Germany is home to over 3.5 million Mittelstand companies, the backbone of European industrial production. These mid-size manufacturers are the primary buyers of automation technology, and many are globally competitive OEMs with the engineering sophistication to evaluate and adopt cutting-edge solutions.

🤖

Industrie 4.0 Leadership

Germany coined Industrie 4.0 and remains its most advanced practitioner. VDMA, ZVEI, and the Platform Industrie 4.0 continue to define global smart manufacturing standards, companies active in Germany are participating in the standard-setting process, not just the commercial market.

🌍

EU Single Market Gateway

A German GmbH or distribution partnership provides CE-marked products with access to the entire EU single market of 450+ million consumers and thousands of industrial buyers, making Germany the highest-leverage single entry point for any European market expansion strategy.

🔬

World-Class R&D Ecosystem

Germany hosts the Fraunhofer Institutes, Max Planck Society, RWTH Aachen, TU Munich, and hundreds of applied research centres, creating co-development and technology transfer partnership opportunities for international automation companies that no other European market can match.

⚡

Energiewende Transformation Demand

Germany’s Energiewende (energy transition) to 80%+ renewable electricity by 2030 is driving massive investment in energy management systems, smart grid automation, hydrogen production equipment, and industrial process electrification, creating structural automation demand beyond the traditional factory floor.

📊

Premium Pricing Environment

German industrial buyers prioritise technical quality, service reliability, and long-term supplier relationships over lowest price, enabling premium positioning for high-quality international automation companies that is difficult to sustain in more price-competitive emerging markets. See our guides on pricing structures for how to navigate this.

Germany’s industrial automation market is one of the most precisely tracked segments in global manufacturing research. As Europe’s largest industrial economy, Germany represents approximately 25–30% of total European industrial automation demand. Multiple research firms publish Germany-specific automation market data with broadly consistent conclusions on market direction, though scope definitions vary.

Research Source

Market Scope

2024 Market Value

Forecast Horizon

Projected Value

CAGR

Next Move Strategy Consulting

Industrial Process Automation

USD 5.45 billion

2030

USD 6.83 billion

3.85%

IMARC Group / Nexdigm

Industrial Automation (broad)

USD 14.2 billion (2023)

2032

USD 22.4 billion

5.8%

VDMA (Mechanical Engineering)

Machine Tools & Automation Systems

EUR 15.4 billion (exports alone)

2026

EUR 16.2 billion

~2.5–3%

ZVEI (Electrical Engineering)

Industrial Electronics & Drives

EUR 9.2 billion

2027

EUR 11.0 billion

~4–5%

IFR (International Federation of Robotics)

Industrial Robots (Germany)

~26,000 units/year installed

2027

~30,000+ units/year

~4–6%

The apparent variance across research firms reflects different scope definitions, process automation only vs. full factory automation including robotics, drives, software, and services. The consistent signal: Germany’s industrial automation market is growing at a steady 4–6% CAGR driven by structural smart factory transformation rather than cyclical investment. Critically, Germany is not just a domestic market, German automation technology companies (Siemens, Beckhoff, Phoenix Contact, Bosch Rexroth, Festo, Pilz, and hundreds of Mittelstand specialists) are global market leaders whose procurement and technology decisions shape global industry standards.

Key Market Drivers for International Companies Entering Germany

Germany’s 3.5 million Mittelstand companies, many family-owned and facing generational succession, are investing heavily in automation to remain internationally competitive. A new generation of owners is accelerating Industrie 4.0 adoption, creating a sustained multi-year automation investment pipeline across every industrial sector.

Structural Driver

🔋

Energiewende & Energy Cost Pressure

Germany’s post-2022 energy price shock created urgent demand for energy management systems, process optimisation automation, and smart grid integration across all energy-intensive industries. Energy cost reduction through automation is now a primary ROI driver for German industrial buyers, expanding the addressable market significantly beyond pure productivity arguments.

Energy Driver

👷

Skilled Labour Shortage (Fachkräftemangel)

Germany’s acute skilled labour shortage, with over 2 million unfilled positions in manufacturing and engineering as of 2025, is the single most powerful argument for automation investment across every German industrial sector. Automation is no longer a productivity optimisation choice; it is increasingly the only viable response to an irreversible demographic and labour supply constraint.

Labour Driver

🚗

Automotive EV Transition Investment

Germany’s automotive industry, VW Group, BMW, Mercedes, and their vast Tier 1–3 supplier networks, is executing one of the world’s largest industrial technology transitions from ICE to EV production. Battery assembly automation, new robotic welding configurations, and EV-specific quality inspection systems are driving multi-billion-euro automation investment across the entire German automotive supply chain.

Automotive Driver

♻️

Carbon Neutral & EU ESG Compliance

Germany’s 2045 carbon neutrality target and the EU’s Corporate Sustainability Reporting Directive (CSRD) are driving investment in automated energy monitoring, emissions tracking, process efficiency systems, and lifecycle data management platforms across all German manufacturing sectors. Compliance deadlines create non-discretionary investment mandates.

ESG Driver

🌐

Reshoring & Supply Chain Resilience Investment

Post-COVID supply chain disruptions have accelerated German manufacturers’ reshoring and nearshoring of production, often making automation economically necessary to maintain cost competitiveness with lower-wage production locations. Companies reshoring to Germany from Asia are systematically automating at higher rates than existing German plants, creating high-value greenfield automation opportunities.

Reshoring Driver

SECTION 3

3 High-Demand Sectors for Industrial Automation in Germany

Industrial automation demand in Germany is concentrated in specific verticals where Industrie 4.0 investment, EV transition, energy transition, and Mittelstand modernisation are driving the highest and most sustained spending. Understanding which sectors are generating the strongest automation investment enables international companies to prioritise their go-to-market approach.

🚗Largest Segment

Automotive & EV Manufacturing

Germany’s automotive sector, VW, BMW, Mercedes, Porsche, and their Tier 1–3 supply chains, is the single largest buyer of industrial automation in Europe. The EV transition is driving the largest single wave of automation investment in the sector’s history: battery module assembly, laser welding for EV chassis, vision systems for cell inspection, and new flexible production architectures.

Key demand: EV battery assembly, laser welding robotics, AGVs, quality vision systems

⚙️Core Sector

Mechanical Engineering (Maschinenbau)

Germany’s mechanical engineering sector, with over €230 billion in annual output, is both a major buyer of automation (for its own production) and the primary creator of automated machinery for export. VDMA-member companies demand the highest precision motion control, servo systems, linear actuators, and intelligent tooling solutions available globally.

Germany’s pharmaceutical sector, Bayer, BASF Health, Boehringer Ingelheim, and hundreds of specialist manufacturers, is investing heavily in flexible automated production, serialisation, and digital batch records to meet EU GMP Annex 1 requirements and export market compliance. Cleanroom automation and advanced process analytics are priority investment areas.

Key demand: flexible filling lines, serialisation, process analytics, ATEX-rated equipment

🧪Large Base

Chemicals & Process Industry

Germany’s chemicals sector, BASF, Evonik, Covestro, Lanxess, operates some of the world’s most complex and highly automated chemical plants. Demand is centred on DCS/SCADA modernisation, advanced process control (APC), safety instrumented systems (SIS), and the integration of AI-powered predictive maintenance across multi-site production networks.

Germany is home to some of the world’s largest food and packaging equipment manufacturers (GEA, Krones, Multivac, Bosch Packaging), creating demand for sophisticated filling, packaging, and process automation. Export-oriented food producers are also investing in automated quality inspection and traceability systems for EU food safety compliance.

Germany’s accelerated renewable energy build-out, solar, wind, and hydrogen, is driving demand for SCADA systems, grid management automation, photovoltaic production line automation, and electrolyser assembly systems. The energy sector is now one of the fastest-growing automation investment segments in Germany.

Germany’s aerospace sector, Airbus, MTU, Liebherr, Diehl, demands the highest-precision automation for composite manufacturing, aircraft structural assembly, and precision machining. Defence spending growth post-2022 is driving new production line investment in ammunition, vehicle, and radar manufacturing, requiring specialist automated assembly solutions.

Germany’s electronics and semiconductor ambitions, anchored by the €30 billion EU Chips Act investment including new Intel and TSMC fabs, are creating demand for cleanroom automation, SMT assembly lines, wafer handling systems, and semiconductor process control equipment at a scale Germany has not previously experienced.

4 Key Industrial & Manufacturing Hubs Across Germany

Germany’s federal structure means manufacturing excellence is distributed across multiple strong regional clusters, unlike the capital-city-centric concentration seen in many other major economies. Understanding Germany’s industrial geography is essential for building an effective distribution and service network.

🚗 Bavaria (Bayern), Automotive & High-Tech Core

Germany’s wealthiest and most innovation-intensive state. Home to BMW, MAN, MTU, Siemens, Infineon, and a deep automotive Tier 1 network. Munich anchors the semiconductor and aerospace cluster; Nuremberg hosts SPS (Europe’s leading PLC/automation trade show); Augsburg leads textiles and mechatronics.

Key clusters: Munich Tech Valley, Nuremberg Automation Hub, Augsburg Innovation Park, Regensburg Electronics

⚙️ Baden-Württemberg, Mittelstand Engineering Heartland

Germany’s most export-intensive state and the global home of precision engineering. Stuttgart anchors the VW/Daimler/Bosch nexus; Heilbronn-Franken and Schwarzwald host thousands of Mittelstand machine tool and automation companies (Trumpf, Festo, Heidenhain, Balluff). The highest concentration of hidden champions globally is here.

Key clusters: Stuttgart Auto Valley, Schwarzwald Machine Tools, Rhine-Neckar Electronics, Bodensee Mechatronics

🏭 North Rhine-Westphalia (NRW), Industrial Scale

Germany’s most populous state and its industrial heartland. Düsseldorf (chemicals, engineering), Cologne (Ford, chemicals), Duisburg (steel, logistics), Aachen (RWTH, Europe’s leading engineering university) form the backbone of Germany’s process industry and heavy manufacturing base.

Hamburg is Germany’s primary trade and logistics hub, essential for international companies with import-intensive supply chains. Offshore wind energy manufacturing and service operations are concentrated in Schleswig-Holstein and Lower Saxony, creating new automation demand for wind turbine component production.

Key clusters: Hamburg Port Logistics, Bremerhaven Wind Energy, Hanover Messe City, Wolfsburg Auto Hub

🔬 Saxony & Eastern Germany, Semiconductors & New Investment

Dresden (“Silicon Saxony”) is emerging as Germany’s primary semiconductor cluster, home to Infineon’s largest fab, the new TSMC fab (under construction), and Bosch’s semiconductor plant. The eastern states offer EU structural fund incentives, lower operating costs, and strong technical university networks.

Key clusters: Silicon Saxony Dresden, Leipzig Auto Hub (BMW, Porsche), Jena Optics Cluster, Halle Chemical Park

🏙️ Berlin & Brandenburg, Startup & Digital Manufacturing

Berlin has emerged as Germany’s largest tech startup ecosystem, increasingly intersecting with manufacturing through industrial IoT platforms, AI-for-manufacturing companies, and new EV-related manufacturing. The new Tesla Gigafactory in Grünheide (Brandenburg) has created a new EV and battery automation cluster.

Key clusters: Tesla Gigafactory Brandenburg, Berlin Startup Manufacturing, Cottbus Energy Technology

💡 Distribution Network Design for Germany

For most international industrial automation companies entering Germany, the optimal first distribution network covers: a national HQ distributor ideally based in Bavaria (Munich/Nuremberg) or Baden-Württemberg (Stuttgart) to access the highest-density Mittelstand manufacturing clusters, with sub-regional coverage in NRW (process industry) and Hamburg (port logistics and international trade). SPS Nuremberg (November) and Hannover Messe (April) are the two essential trade show presences for any serious Germany market entry. See our guide to building a distributor network for the structural framework.

SECTION 5

5 Market Entry Models: Choosing the Right Approach

Germany offers several established entry structures for international manufacturing and automation companies, each with specific legal, commercial, and tax implications. Selecting the right model requires understanding both the German commercial law framework and the practical realities of building market presence with German industrial buyers.

Entry Model

How It Works

Capital Required

Time to Revenue

Best For

Key Reference

Handelsvertreter (Commercial Agent)

A self-employed agent acts in your name to solicit orders, earning commission. Governed by German HGB §84–92c, provides significant legal protections to the agent on termination

Very Low

3–9 months

Testing German market demand with minimal capital; established product lines with clear application fit

Germany’s standard private limited company, full commercial operations, 100% foreign ownership permitted, min. €25,000 share capital, requires at least one managing director (Geschäftsführer)

Moderate–High

6–12 months (incorporation + setup)

Long-term strategic commitment; direct sales and service operations; PLI-equivalent R&D grant eligibility

Partner with a Fraunhofer institute, German university (TU Munich, RWTH Aachen), or Mittelstand technology company to co-develop Germany-adapted solutions

Shared

18–36 months (development cycle)

Adapting global platforms to German industry standards; accessing EU Horizon research funding; building Industrie 4.0 credibility

Germany’s Commercial Agent Act (HGB §89b) grants commercial agents a mandatory goodwill compensation (Ausgleichsanspruch) upon termination, potentially up to one year’s average annual commission. This is non-waivable under German law regardless of what your contract says. Before appointing a German commercial agent, understand this liability and structure your compensation, territory, and termination provisions accordingly. Engaging a German-qualified lawyer before signing any commercial agent agreement is essential, see our guides on termination clauses and risk allocation in cross-border deals.

💡 Recommended Entry Sequence for Industrial Automation Companies

For most international industrial automation companies entering Germany for the first time: Year 1–2: Appoint a verified national distributor or technical sales partner specialising in your target sector (automotive, chemicals, food, pharma) to validate market fit and build reference installations. Attend SPS and/or Hannover Messe as an exhibitor or co-exhibitor. Year 2–3: Evaluate establishing a German GmbH as a local sales and service entity once validated revenue justifies the structure. Year 3+: Consider whether co-development partnerships with Fraunhofer or RWTH can create technical differentiation in the German market. Avoid the common mistake of establishing a GmbH before you have validated product-market fit, German operational costs (labour, compliance, accounting) are significant and should be justified by demonstrated demand.

SECTION 6

6 Industrie 4.0 & Government Innovation Programmes: What Foreign Companies Must Know

🏛️ Policy Overview

Industrie 4.0 is Germany’s national strategic initiative, originating from the German federal government and industry associations in 2011, for the digital transformation of manufacturing through cyber-physical systems, IIoT, AI, digital twins, edge computing, and autonomous production. While Industrie 4.0 is not a grant programme per se (unlike India’s PLI scheme), it defines the technical standards, reference architectures, and procurement requirements that German industrial buyers use to evaluate automation technology, making alignment with Industrie 4.0 frameworks a commercial necessity, not an optional positioning choice. The RAMI 4.0 (Reference Architecture Model Industrie 4.0) and the Asset Administration Shell (AAS) standard are the two most practically important technical frameworks for automation technology providers seeking German market credibility.

Key Innovation Funding Programmes Relevant to International Automation Companies

Programme

Managing Body

Relevance to Automation Companies

Funding Mechanism

Zentrales Innovationsprogramm Mittelstand (ZIM)

Federal Ministry for Economic Affairs (BMWK)

Very High, funds R&D cooperation projects between foreign companies and German Mittelstand; accessible to international companies with German GmbH

Grants up to 55% of eligible R&D costs; up to €380,000 per project phase

Horizon Europe (EU Framework Programme)

European Commission

High, funds collaborative R&D including Industrie 4.0, AI, robotics; companies in 100+ associated countries can participate

Grants up to 100% of eligible costs for R&D activities; multi-year multi-partner projects

Important Projects of Common European Interest (IPCEI)

EU / Federal + State governments

High, for battery, semiconductor, and hydrogen value chain participants; enables otherwise prohibited state aid for industrial projects

Direct subsidies, guarantees, and tax incentives; varies by IPCEI and national plan

EU Chips Act Investments (Germany)

European Commission / BMWK

High, €30B+ EU Chips Act includes major German semiconductor fab investments; automation suppliers to Intel, TSMC, and Bosch fabs benefit directly

Direct investment and state aid to fab construction; indirect demand for cleanroom and process automation

State-Level Investment Grants (Invest in Germany / GTAI)

Germany Trade & Invest (GTAI) / Federal States

Medium–High, German federal states (especially Bavaria, Baden-Württemberg, Saxony) offer investment grants, land subsidies, and tax incentives for manufacturing investments

Investment grants up to 25–35% for investments in structurally weak regions; available to foreign investors

Forschungszulagengesetz (R&D Tax Credit)

Federal tax authority

Medium, Germany introduced a 25% R&D tax credit in 2020 (up to €1M benefit/year), accessible to GmbH entities conducting qualifying R&D in Germany

25% tax credit on eligible R&D employee costs; up to €4M eligible spend per year

Even if your automation company does not immediately pursue formal Industrie 4.0 certification, aligning your product communication, technical documentation, and integration capabilities with Industrie 4.0 frameworks is commercially essential in Germany. Specifically: (1) Ensure your products support OPC UA (the standard communications protocol for Industrie 4.0 data exchange), German procurement specifications increasingly mandate it. (2) Document your RAMI 4.0 positioning, German engineering buyers expect suppliers to speak this language. (3) For IIoT-connected products, demonstrate GDPR-compliant data handling and cyber-security capabilities aligned with BSI (Federal Office for Information Security) guidelines. (4) Consider joining Platform Industrie 4.0, Germany’s central public-private Industrie 4.0 coordination body, as a participant to access networking, working groups, and credibility-building opportunities. Explore relevant supplier collaboration platforms and technology partnership approaches to accelerate your Industrie 4.0 positioning.

SECTION 7

7 Regulatory & Compliance Requirements for Entry

Germany operates within the EU regulatory framework while also maintaining significant national compliance requirements. For international manufacturers and automation companies, the CE Marking regime, GDPR, WEEE/RoHS, and the specific requirements of German product liability law create a compliance landscape that must be carefully navigated before products can be sold commercially in Germany.

01

CE Marking, The Non-Negotiable Gateway

CE marking is the mandatory market access requirement for virtually all industrial, electrical, electronic, and mechanical products sold in the EU/EEA, including Germany. CE marking demonstrates conformity with applicable EU Directives and Regulations, most commonly the Machinery Directive (2006/42/EC, transitioning to EU Machinery Regulation 2023/1230 effective June 2027), Low Voltage Directive (2014/35/EU), EMC Directive (2014/30/EU), and Pressure Equipment Directive (2014/68/EU). CE marking requires a technical file, declaration of conformity, and for many product categories, third-party assessment by a Notified Body (NB). For automation equipment entering Germany, allow 3–12 months for CE marking processes depending on product complexity, risk classification, and whether conformity assessment requires a Notified Body. CE marking costs typically range from €5,000–€80,000 depending on product scope.

02

GmbH Incorporation & Business Registration

For companies establishing a German legal entity, the GmbH is the standard vehicle: minimum share capital of €25,000 (with at least €12,500 paid up at incorporation), notarially executed articles of association, registration in the commercial register (Handelsregister), and appointment of a Geschäftsführer (managing director), who need not be a German resident. Incorporation takes 3–6 weeks with the right notary and local counsel. For companies operating through a German distributor rather than their own entity, a German tax registration may still be required if the distribution arrangement creates a fixed establishment for VAT purposes, assess this carefully with German tax advisors before entering distribution agreements.

03

VAT (Umsatzsteuer) Registration

German VAT (Umsatzsteuer, UStG) at 19% (7% for certain goods) applies to all commercial transactions in Germany. Foreign companies supplying goods or services to German buyers may be required to register for German VAT, particularly if they are holding inventory in Germany, conducting installation or commissioning services, or making intra-Community acquisitions. German VAT registration is managed through the relevant tax office (Finanzamt). Input VAT recovery on German business expenses is available to registered businesses. Ensure your invoicing, pricing, and distribution agreement structures are VAT-compliant from day one, German tax authorities audit closely and penalties for non-compliance are significant.

04

GDPR & BSI Cybersecurity Requirements

The General Data Protection Regulation (GDPR) applies to all entities processing personal data of EU residents, including operational technology systems in German factories where employee monitoring data or connected device data involving personal information is processed. For cloud-connected industrial automation products, GDPR compliance requires a legitimate processing basis, data processing agreements with customers, privacy-by-design architecture, and demonstrable security measures. Germany’s Federal Office for Information Security (BSI) publishes the IT-Grundschutz framework and the ICS Security Compendium, increasingly referenced by German industrial buyers in procurement specifications for OT-connected automation systems. BSI certification (while not universally mandatory) provides significant commercial credibility with security-conscious German buyers. See our B2B secure collaboration guide for relevant frameworks.

05

WEEE, RoHS & REACH Compliance

All electrical and electronic equipment sold in Germany must comply with WEEE (Waste Electrical and Electronic Equipment Directive 2012/19/EU, requiring manufacturer registration in the German EAR registry), RoHS (Restriction of Hazardous Substances Directive 2011/65/EU, restricting lead, mercury, cadmium, and other hazardous materials), and REACH (EU Chemicals Regulation EC 1907/2006, requiring registration of substances in articles above 0.1% concentration). For industrial automation equipment, WEEE registration with the stiftung ear (German take-back authority) is mandatory before first placing products on the German market. RoHS compliance requires technical documentation for each product. REACH requires chemical substance communication through the supply chain.

06

IP Protection in Germany & the EU

Germany has one of Europe’s most effective IP enforcement systems, with specialist IP courts (Landgericht Düsseldorf, Landgericht Munich) known for fast interim injunctions and strong enforcement against infringers. International companies should register trademarks at the EU level (EU Trade Mark via EUIPO, single registration covers all EU member states including Germany) and national German level (DPMA). Patent protection through the European Patent Office (EPO, headquartered in Munich) provides EU-wide coverage. For software-embedded automation systems, understand the limits of software patentability in Germany and consider whether trade secret protection combined with NDA frameworks provides more practical protection. Review our guides on IP ownership in manufacturing partnerships and non-compete vs non-circumvention clauses before entering German partner arrangements.

07

German Product Liability (ProdHaftG) & Industrial Safety

Germany’s Product Liability Act (ProdHaftG) implements the EU Product Liability Directive with strict liability for defective products, manufacturers, importers, and own-branders are all potentially liable. For industrial automation equipment operating in German factories, product liability exposure requires careful management through appropriate technical documentation, CE conformity, installation and operating manual requirements (in German), and adequate product liability insurance. German machinery safety requirements under the Machinery Directive (and the German Industrial Safety Regulation, BetrSichV) impose specific obligations on manufacturers of machinery sold or operated in Germany, including risk assessments, safety-relevant documentation, and conformity with relevant harmonised standards.

SECTION 8

8 Finding a Verified German Distribution or Technology Partner

For international manufacturing and industrial automation companies entering Germany, finding the right German partner, a distributor, system integrator, Handelsvertreter, technology licensor, or joint venture candidate, is the most consequential decision in the entry process. German industrial buyers build long-term, trust-based supplier relationships, the right German partner provides not just commercial channel access but the engineering credibility, Mittelstand relationship network, and technical service capability that German buyers demand from their suppliers.

What to Look for in a German Industrial Automation Distributor or Partner

✅

Verified Business Identity

Handelsregister registration, Steuernummer (tax ID), relevant industry certifications (ISO 9001, SCC, IATF 16949 for automotive), and confirmation of the signatory’s authority. This is the baseline, see business verification requirements.

🔬

Technical Engineering Depth

German industrial buyers expect their automation suppliers to provide genuine application engineering, not just product sales. Does the partner have qualified engineers (Ingenieure) capable of application consulting, demonstration, commissioning, and first-line technical support? Assess their technical team size and qualifications carefully.

🏭

Sector Specialisation & Mittelstand Relationships

Does the partner have genuine Mittelstand customer relationships in your target sectors? A distributor covering 30 unrelated product categories across 10 industries may lack the sector-specific depth to position complex automation solutions competitively in German engineering procurement situations.

🗺️

Regional Coverage & Service Infrastructure

Does their coverage match the industrial cluster geography relevant to your sector? A distributor based in Hamburg with no presence in the Mittelstand clusters of Baden-Württemberg or Bavaria is geographically incomplete for most industrial automation companies. Consider whether regional sub-distributors are needed.

📋

CE Competence & Regulatory Capability

Can the partner support your CE marking obligations, managing technical files, liaising with Notified Bodies, and ensuring ongoing conformity maintenance? A distributor who is the EU importer of record assumes CE-related responsibilities; confirm they understand and accept these obligations before contracting.

🤖

Industrie 4.0 Positioning & Digital Capability

Does the partner position themselves credibly within the Industrie 4.0 ecosystem? Can they discuss OPC UA, digital twins, IIoT integration, and edge computing with German engineering buyers? In 2026, Industrie 4.0 fluency is table stakes for any German industrial automation distribution partner. See partnership evaluation criteria.

🔐

Confidentiality & Data Security Practices

German industrial partnerships involve technically sensitive information, product roadmaps, pricing, application specifications. German data protection culture is strong; ensure your partner has demonstrably GDPR-compliant data handling practices and agrees to execute a mutual NDA governed by German law before any sensitive data exchange. Use encrypted channels for all sensitive sharing, see B2B secure collaboration.

🚫

Non-Competing Portfolio Check

Does the partner already carry directly competing products from established global automation brands (Siemens, Beckhoff, Phoenix Contact, B&R)? German distributors often carry complementary rather than competing product lines, but verify carefully. A distributor representing your direct competitor will never be your true advocate with German buyers.

Channels for Finding Verified German Partners

💻

GTsetu Verified B2B Platform

GTsetu provides access to verified German and European manufacturers, distributors, system integrators, and technology partners, with anonymous discovery, built-in NDA workflow, and encrypted collaboration. Zero broker commissions. The most efficient and secure channel for verified German partner discovery. Compare with alternatives to Alibaba and open B2B directories for a full picture of available channels.

Best for Verified Discovery

🎪

Hannover Messe & SPS Nuremberg

Hannover Messe (April, Hannover) is the world’s largest industrial technology trade fair, the single most important event for international automation companies seeking German and European market visibility and partner meetings. SPS (November, Nuremberg) is Europe’s premier PLC, drive, and automation show, highly targeted for automation technology companies. Both are mandatory for any serious Germany market entry programme. See top B2B networking places for manufacturers.

Premier In-Person Channel

🏛️

AHK (German Chamber of Commerce Abroad) & DIHK

The German Chamber of Commerce Abroad (AHK) network operates in 90+ countries and can introduce international companies to verified German counterparts. The Association of German Chambers of Commerce (DIHK) maintains extensive member directories and facilitates international business introductions. Strong starting points for relationship-building with the German business community.

Chamber Channel

⚙️

VDMA, ZVEI & VDI Industry Associations

VDMA (mechanical engineering, 3,200+ members), ZVEI (electrical engineering), and VDI (Association of German Engineers, 140,000+ members) all maintain active member directories and facilitate B2B introductions within their respective sectors. Sector-specific working groups within these associations provide the deepest access to the Mittelstand buyer community. A B2B business network approach through these associations creates warm introductions that cold outreach cannot match.

Association Channel

🌐

Germany Trade & Invest (GTAI)

Germany’s official inward investment promotion agency provides sector-specific market entry information, investor facilitation, introductions to federal and state investment agencies, and a network of international contacts in Germany’s key industrial clusters. GTAI’s sector experts in Berlin can facilitate targeted introductions for serious market entry candidates. Access at gtai.de/en/invest.

Government Channel

🔬

Fraunhofer Institutes & University Spin-Outs

Germany’s 76 Fraunhofer institutes are the world’s most commercially active applied research organisation, bridging between academic technology development and industrial deployment. Partnering with a relevant Fraunhofer institute (IPA for manufacturing automation, IWU for metalworking, IML for logistics) provides research credibility, EU funding access, and warm introductions to the Mittelstand companies they serve as research partners. See our technology partnership guide.

Research Channel

SECTION 9

9 Step-by-Step Germany Market Entry Roadmap

01

Market Prioritisation, Validate Before Committing

Before committing resources to Germany, validate your specific product’s fit with German industrial buyer requirements. Which Mittelstand sectors have the highest unmet need for your specific automation solution? What is the competitive landscape, which global automation brands have established German distribution, and where are the genuine gaps? What CE marking and standards compliance is required, and what is the realistic timeline? A 4–8 week targeted validation programme, combining GTsetu partner discovery, trade association conversations, and a Germany visit structured around SPS or Hannover Messe, will answer these questions more efficiently than any desk research. Use GTsetu’s platform to anonymously assess potential German partners before revealing your market entry plans.

02

CE Marking & Standards Compliance Programme

Initiate your CE marking and relevant standards compliance programme in parallel with market validation, not after partner selection. CE marking timelines of 3–12 months mean that delays at this stage delay your entire market entry. Engage a German or EU-qualified technical consultancy or Notified Body for a gap assessment of your product against applicable Directives and harmonised standards. Begin documenting your technical file, risk assessments, and declaration of conformity. For products requiring WEEE registration, begin the stiftung ear registration process at least 3 months before first German commercial sale.

03

Ideal Partner Profile Definition

Define precisely what you need in a German partner: sector specialisation (automotive / chemicals / food / pharma / mechanical engineering), geographic coverage (Bavaria, Baden-Württemberg, NRW, or national with sub-regional coverage), technical team depth (engineers by discipline), Industrie 4.0 positioning, existing Mittelstand customer relationships, and complementary product portfolio. A specific ideal partner profile makes every discovery interaction productive. The more specific your brief, the faster GTsetu’s verified network surfaces relevant German candidates. See our international wholesale distributors guide for qualification frameworks.

04

Partner Discovery & Verification

Discover candidates through GTsetu’s verified platform, targeted SPS/Hannover Messe engagement, VDMA/ZVEI member outreach, and AHK introductions. For every candidate, verify: Handelsregister registration (at handelsregister.de), VAT ID (via EU VIES), trade references from existing principals they represent, and personal reference checks with their existing customers if possible. GTsetu performs compliance verification for all companies on its platform, eliminating the due diligence burden from your discovery process. See our business verification requirements for the complete checklist.

05

NDA Execution & Secure Technical Exchange

Execute a mutual NDA governed by German law before sharing any technical data, product specifications, pricing, application notes, or go-to-market strategy. German data protection culture makes NDA execution straightforward; most serious German partners expect and respect it. All technical data exchange should occur through encrypted channels. On GTsetu, the NDA workflow is built in and activated before the encrypted workspace unlocks. For technical product evaluation, stage your data disclosure: publicly available information first, then confidential technical specifications only after NDA is signed and initial trust is established.

06

Commercial Negotiation, Navigate German Contract Specifics

Negotiate all commercial terms with full awareness of German contract law specifics. Key Germany-specific considerations: termination provisions and Handelsvertreter goodwill compensation obligations under HGB §89b; exclusivity structure (national vs. regional; sector-specific); pricing in EUR with clear handling of exchange rate risk; payment terms (standard in Germany: 30 days net, often with 2% discount for 10-day payment); Incoterms for German import; warranty obligations aligned with German consumer and commercial law; and minimum purchase commitments calibrated to realistic Mittelstand sales cycles.

07

Agreement Execution with German Legal Review

Execute the manufacturer-distributor or commercial agent contract with review by German-qualified legal counsel, specifically one experienced in commercial agency law (HGB §84–92c) or distribution law, as applicable. German contract law has mandatory provisions, particularly for commercial agents, that override contractual clauses attempting to waive them. Address dispute resolution explicitly: specify whether German courts have exclusive jurisdiction (standard for distribution agreements with EU parties) or whether international arbitration (ICC, DIS, German Institution of Arbitration) applies. Review force majeure provisions and non-compete clauses against German law enforceability limits.

08

Market Launch & Partner Enablement

A successful Germany launch requires investing specifically in the enablement priorities that German buyers demand: German-language technical documentation (Betriebsanleitungen must be in German for CE-compliant machinery sold in Germany, this is a legal requirement, not a courtesy); joint Hannover Messe or SPS presence for market visibility; co-development of reference case studies with early German customer installations (Referenzkunden are essential for Mittelstand sales); joint technical seminars at German customers’ facilities; and a defined service and spare parts availability commitment (German buyers demand clear service level commitments before signing purchase orders). The first 12 months in Germany require sustained investment in enablement to build the trust and references that unlock broader Mittelstand adoption.

SECTION 10

10 Key Commercial Terms for Germany Partnerships

Germany-specific commercial dynamics require important adjustments to standard international distribution agreement terms. German commercial law, procurement culture, and the Mittelstand relationship model all shape what effective German partnership agreements must contain.

Commercial Term

Germany-Specific Consideration

Reference Guide

Commercial Agent Goodwill Compensation

HGB §89b creates a mandatory goodwill compensation (Ausgleichsanspruch) payable to a Handelsvertreter on termination by the principal, up to one year’s average annual commission, non-waivable. Structure appointment type (agent vs. distributor), compensation, and termination provisions with this liability explicitly modelled and managed.

Standard German commercial payment terms are 30 days net, often with a 2% Skonto (early payment discount) for 10-day payment. German buyers expect these standard terms, price lists should account for Skonto economics. For new relationships, consider advance payment or bank guarantee for first orders before establishing open account credit.

Germany pricing must be in EUR. For non-Eurozone suppliers, EUR/home-currency exchange rate fluctuations affect supply cost economics. Structure annual price review mechanisms into distribution agreements to address exchange rate movements systematically, German buyers will not accept mid-year price increases without contractual basis.

German exclusivity is typically defined by NUTS-2 or federal state geography, or by sector (Automotive, Chemicals, Food). National exclusivity granted to a first-time German partner before validated performance is a strategic risk, consider sector-specific or regional exclusivity with expansion rights tied to performance thresholds. See also territory rights guide.

German commercial buyers expect clearly defined warranty periods (minimum 12 months on industrial equipment, often 24 months in competitive situations), defined service response times (4–8 hours for critical production equipment), and local spare parts availability. German law grants buyers a two-year statutory defect liability period (§437 BGB) for commercial sales, understand how this interacts with your warranty policy.

All operating manuals (Betriebsanleitungen) for machinery and equipment sold in Germany must be provided in German, this is a CE Marking legal requirement under the Machinery Directive, not just a commercial consideration. Safety instructions, installation guides, and maintenance documentation must all be in German. Budget for professional technical translation (not machine translation) as a mandatory cost of market entry.

Mittelstand sales cycles are longer than most companies expect, 6–18 months for first major account wins is not unusual for technically complex automation. First-year minimum purchase commitments must reflect this reality. Calibrate minimums to achievable market development targets, with ratchet provisions in years 2–3 as references are established and sales pipeline matures.

For partnerships involving German co-development or technology adaptation, specify clearly who owns jointly developed IP, default rules under German copyright and patent law may differ from your home country assumptions. Ensure IP ownership provisions explicitly address software modifications, firmware adaptations, and application-specific engineering developed by the German partner for German customer projects.

German Mittelstand buyers are thorough, cautious evaluators, especially for safety-critical automation components. Sales cycles of 12–24 months from first contact to purchase order are common for new supplier relationships. Plan your Germany revenue projections and partner performance expectations around Mittelstand-realistic timelines, not your domestic market benchmark.

🏆

Incumbent Supplier Loyalty

German industrial buyers value long-term supplier relationships highly, switching costs in terms of re-qualification, retraining, and integration risk mean that displacing an established automation supplier requires a compelling, demonstrable technical advantage rather than simply a better price. Lead with reference installations and technical proof-of-concept rather than commercial terms.

📋

CE Marking & Standards Complexity

Germany’s CE marking enforcement is among Europe’s most rigorous, product compliance failures risk market withdrawal orders and significant reputational damage with Mittelstand buyers. Begin CE marking preparation 12+ months before target market entry, engage a German-qualified compliance consultant, and never assume that certifications from other markets (UL, CSA, CCC) satisfy EU/German requirements without verification.

🔧

Service & After-Sales Infrastructure Gap

German industrial buyers will not adopt a new automation supplier without confidence in local service capability, on-site response times, German-speaking technical support, and local spare parts availability are non-negotiable requirements. Building this service infrastructure through your distribution partner is essential before pursuing major account opportunities. Align your supply chain partner relationships to support spare parts availability in Germany.

💬

German Language & Technical Communication Culture

While English is widely spoken in German industry, all formal commercial communications, contracts, technical documentation, and safety-critical materials must be available in German. Marketing materials, website content, and trade show presentations that are English-only signal a lack of commitment to the German market. Invest in professional German technical translation from day one.

⚡

High Operating Cost Environment

Germany has high labour costs, significant social security contributions (approximately 40% of gross salary), stringent employment law (strong worker protection, co-determination rights for works councils in companies with 5+ employees), and complex tax compliance requirements. Model your German operating cost structure carefully before committing to a German GmbH, ensure your revenue projections can sustain the operational overhead.

🤖

Intense Domestic Automation Competition

Germany is home to the world’s strongest industrial automation companies, Siemens, Beckhoff, Phoenix Contact, Lapp, Festo, Pilz, Kuka (now Chinese-owned), and hundreds of Mittelstand automation specialists. International companies must define a genuinely differentiated technology position, not just competitive pricing, to gain and sustain market share against incumbents who have 30-year relationships with key German accounts. Use our global collaboration examples for positioning inspiration.

🔋

Energy Transition Uncertainty

Germany’s energy policy, post-nuclear phase-out, renewable build-out timelines, grid stability, creates planning uncertainty for energy-intensive German manufacturers, occasionally causing capital expenditure deferrals. Understanding your target sector’s exposure to energy cost volatility and how this affects their automation investment cycle enables better sales forecasting and partner expectation management.

SECTION 12

12 How GTsetu Connects You with Verified German Partners

🇩🇪 GTsetu, Verified B2B Platform for Germany Market Entry

Discover Verified German Manufacturers & Distributors, No Broker Commission

GTsetu provides international manufacturing and industrial automation companies with direct access to compliance-verified German manufacturers, distributors, system integrators, and technology partners, across every industrial sector and all major German manufacturing regions. Every company in GTsetu’s network has been verified through business registration (Handelsregister), VAT ID, industry certifications (ISO, CE compliance documentation, sector-specific), and authority letter confirmation before appearing in the platform. You discover, qualify, and engage with verified German partners, without broker intermediaries taking a cut of your commercial economics.

🏛️

Multi-Layer Compliance Verification

Every German partner on GTsetu has been verified: Handelsregister, VAT ID, ISO certifications, by GTsetu’s compliance team. Eliminates fraud risk and due diligence workload.

🕵️

Anonymous Discovery

Browse verified German partner profiles without revealing your identity. Protect your Germany market entry strategy until you choose to engage. Not possible via trade directories or open marketplaces.

📄

Built-In NDA Workflow

Digital mutual NDA with timestamped signatures activated before sensitive technical or commercial data can be exchanged. Governed by German or mutually agreed law. GDPR-compliant data handling.

🔐

Encrypted Document Workspace

AES-256 encryption at rest, TLS in transit. Role-based access controls. Full audit trail. Exchange product specs, pricing, and technical proposals securely, never through unprotected email. BSI-aligned security baseline.

🚫

Zero Broker Commission

GTsetu charges zero commission on any partnership formed between international manufacturers and German distributors or partners. All commercial economics stay between you and your partner.

🌏

100+ Countries Including Germany

GTsetu’s verified network covers all major German industrial regions as well as the broader European market, supporting your Germany entry today and expansion into Poland, Romania, and India tomorrow.

QWhy should I expand my manufacturing or industrial automation business to Germany?

Germany is Europe’s largest manufacturing economy and the global epicentre of Industrie 4.0, making it the most strategically important European market for any industrial automation or manufacturing technology company. The German industrial automation market is projected to grow from $5.45 billion in 2024 to $6.83 billion by 2030, supported by a manufacturing sector accounting for over 20% of GDP, the world’s most advanced adoption of smart factory technologies, and 3.5 million Mittelstand companies actively investing in automation. Beyond direct revenue, a German market presence provides unmatched commercial credibility, a German Referenzkunde (reference customer) accelerates sales across Europe and globally. Germany also offers access to the EU single market of 450+ million consumers through a single CE-compliant market entry, world-class R&D co-development opportunities through Fraunhofer institutes and technical universities, and EU innovation funding programmes (Horizon Europe, ZIM, IPCEI) accessible through German entities. Explore the broader context in our global expansion guide.

QWhat are the best entry models for expanding a manufacturing or automation business to Germany?

For most first-time Germany entrants in industrial automation, the recommended entry sequence is: (1) Appoint a verified national or regional German distributor or Handelsvertreter (commercial agent), fastest market access (3–9 months to first revenue) with minimal capital. Note that Handelsvertreter agreements carry mandatory HGB §89b goodwill compensation obligations on termination. (2) After 2–3 years of validated German market presence and revenue, evaluate establishing a German GmbH (minimum €25,000 share capital) for greater market control and direct customer relationships. (3) If co-development or deep technology integration is strategically important, pursue partnership with a Fraunhofer institute or Mittelstand technology company, potentially with ZIM or Horizon Europe co-funding. Acquisition of an existing German distributor is the fastest route to established Mittelstand relationships for companies with the capital to execute it. See our full comparison in market entry partnerships and JV vs. strategic alliance.

QWhat is Industrie 4.0 and how does it affect my Germany market entry?

Industrie 4.0 is Germany’s national initiative for the digital transformation of manufacturing through cyber-physical systems, IIoT, AI, digital twins, and autonomous production, originating from the German federal government and industry associations (BITKOM, VDMA, ZVEI) in 2011 and now the globally dominant smart manufacturing framework. For international automation companies entering Germany, Industrie 4.0 defines both the technical standards (RAMI 4.0 reference architecture, Asset Administration Shell/AAS for digital product identity, OPC UA for machine communication) and the commercial expectations (smart factory integration capability, IIoT connectivity, data-driven services) that German industrial buyers use to evaluate automation suppliers. OPC UA support is increasingly a mandatory procurement specification, if your automation products do not speak OPC UA, your German market entry will be severely constrained. Industrie 4.0 fluency in your sales team and technical documentation is essential; your German distribution partner must be able to discuss these frameworks credibly with Mittelstand engineering buyers. Use supplier collaboration platforms and technology partnership frameworks to build Industrie 4.0 credibility with German partners.

QWhat CE marking is required to sell industrial automation products in Germany?

CE marking is mandatory for virtually all industrial, electrical, electronic, and mechanical products sold in Germany and across the EU/EEA. The applicable EU Directives for most industrial automation products are: Machinery Directive (2006/42/EC, transitioning to EU Machinery Regulation 2023/1230 by June 2027) for machines and safety components; Low Voltage Directive (2014/35/EU) for electrical equipment between 50V–1000V AC; EMC Directive (2014/30/EU) for electronic equipment; and Pressure Equipment Directive (2014/68/EU) for pressure-rated equipment. CE marking requires: technical file documentation, risk assessment, conformity with applicable harmonised standards (EN standards), Declaration of Conformity, and affixing the CE mark. For higher-risk product categories (machinery with safety functions, explosive atmosphere equipment), a Notified Body (NB) assessment is required. Allow 3–12 months for CE marking depending on product complexity. Operating manuals for machinery must be in German, a legal CE Marking requirement, not an option. Begin CE marking preparation at least 12 months before your planned German market launch.

QHow do I find a verified distributor for industrial automation products in Germany?

The most efficient and secure route to finding a verified German industrial automation distributor is through GTsetu’s compliance-verified B2B platform, where every company has been verified through Handelsregister registration, VAT ID, and industry certifications before appearing in the network, with anonymous discovery, built-in NDA workflow, and encrypted collaboration at zero broker commission. Supplement with targeted trade show engagement at SPS Nuremberg (November) and Hannover Messe (April), the two essential German automation trade events. Engage AHK (German Chamber of Commerce Abroad) for warm introductions, VDMA or ZVEI member directories for sector-specific companies, and Germany Trade & Invest (GTAI) for investment-facilitated introductions. Always verify every candidate independently, Handelsregister at handelsregister.de, VAT ID via EU VIES, or use a platform where pre-verification is already complete. Review our guides on finding international distributors and distributors and manufacturers frameworks.

QWhich industrial sectors in Germany have the highest automation investment demand?

The sectors with the highest industrial automation investment demand in Germany in 2026 are: (1) Automotive and EV manufacturing, the largest segment, with VW Group, BMW, Mercedes, and their Tier 1–3 supply chains executing the world’s largest EV production transition, driving robotics, battery assembly automation, and flexible manufacturing investment. (2) Mechanical engineering (Maschinenbau), VDMA members are both major automation buyers and the creators of automated machinery for export; demand is for precision motion control, servo drives, and condition monitoring. (3) Chemicals and process industry, BASF, Evonik, and Covestro are modernising DCS/SCADA systems and investing in advanced process control. (4) Pharmaceuticals and life sciences, EU GMP Annex 1 compliance and flexible production requirements are driving serialisation and cleanroom automation investment. (5) Energy and utilities, Germany’s Energiewende is creating SCADA, smart grid, and renewable energy production automation demand. (6) Electronics and semiconductors, new Intel and TSMC fabs in Germany are creating cleanroom and process automation demand at scale. Bavaria (Munich/Nuremberg), Baden-Württemberg (Stuttgart/Schwarzwald), and North Rhine-Westphalia (Rhine-Ruhr) are the highest-density industrial automation demand regions.

QWhat commercial terms should I negotiate carefully in a Germany distribution agreement?

Germany-specific commercial terms requiring careful negotiation: (1) Commercial agent (Handelsvertreter) appointment type vs. distributor (Eigenhändler), and the mandatory HGB §89b goodwill compensation liability if appointing an agent. (2) EUR pricing with clear annual price review mechanisms to manage exchange rate movements. (3) Payment terms, standard German commercial terms are 30 days net / 2% Skonto for 10-day payment; new relationships should start with advance payment or bank guarantee. (4) Territory and exclusivity, consider sector-specific exclusivity rather than full national exclusivity for first partnerships. (5) German-language documentation, operating manuals must be in German as a CE Marking legal requirement; budget for professional technical translation. (6) Warranty and service SLA obligations, define response times, spare parts availability commitments, and warranty period explicitly. (7) Minimum purchase commitments calibrated to realistic Mittelstand sales cycle timelines (12–24 months for major account wins). (8) Termination and exit provisions, understand HGB §89b obligations before structure. See our complete guides on exclusivity clauses, termination clauses, business partnership contracts, and manufacturer-distributor contracts.

Ready to Expand Your Manufacturing Business to Germany?

Connect with verified German manufacturers, distributors, and technology partners on GTsetu, with compliance-backed verification, anonymous discovery, built-in NDA workflows, and zero broker commissions on every Germany market partnership you form.

They represents the product, and research team behind GTsetu, a global B2B collaboration platform built to help companies explore cross-border partnerships with clarity and trust. The team focuses on simplifying early-stage international business discovery by combining structured company profiles, verification-led access, and controlled collaboration workflows.

With a strong emphasis on trust, and disciplined engagement, Team GTsetu shares insights on global trade, partnerships, and cross-border collaboration, helping businesses make informed decisions before entering deeper commercial discussions.